Author: Curry, Trend Research

Abstract: SpaceX is scheduled to price after the market closes on June 11 and debut under the code SPCX on June 12, with an issue price of $135, valuing the company at approximately $1.75 trillion and raising $75 billion, making it the largest IPO in history.

However, data compiled by Motley Fool on 30 prominent tech IPOs shows that the median returns after 6 and 12 months are both -9%, with the median maximum drawdown in the first year at 54%, with no exceptions. Morningstar has only given a fair valuation of about $780 billion, less than half of the issue price.

This Friday (June 12), SpaceX will list on NASDAQ under the code SPCX. According to a Reuters report on June 3, the issue price is set at $135 per share, with approximately 556 million shares issued, raising $75 billion, corresponding to an estimated valuation of about $1.75 trillion (some sources estimate it at $1.77 trillion based on post-issue equity). Regardless of the method of calculation, this is the largest IPO in stock market history, with an underwriting group led by Goldman Sachs involving as many as 21 investment banks, and the final pricing will be determined after the close of U.S. markets on June 11.

The enthusiasm is undeniable. SpaceX stated in its S-1 filing that the company has "identified the largest actionable total addressable market in human history," quantifying its scale at $28.5 trillion. The retail allocation ratio has been set at 30% of the float, roughly three times the conventional level for large IPOs.

The problem is, for ordinary investors rushing in on the opening day, the historical data offers a rather unflattering answer.

Median Ledger: Slight Profit in the First Three Months, Collective Loss After Six Months

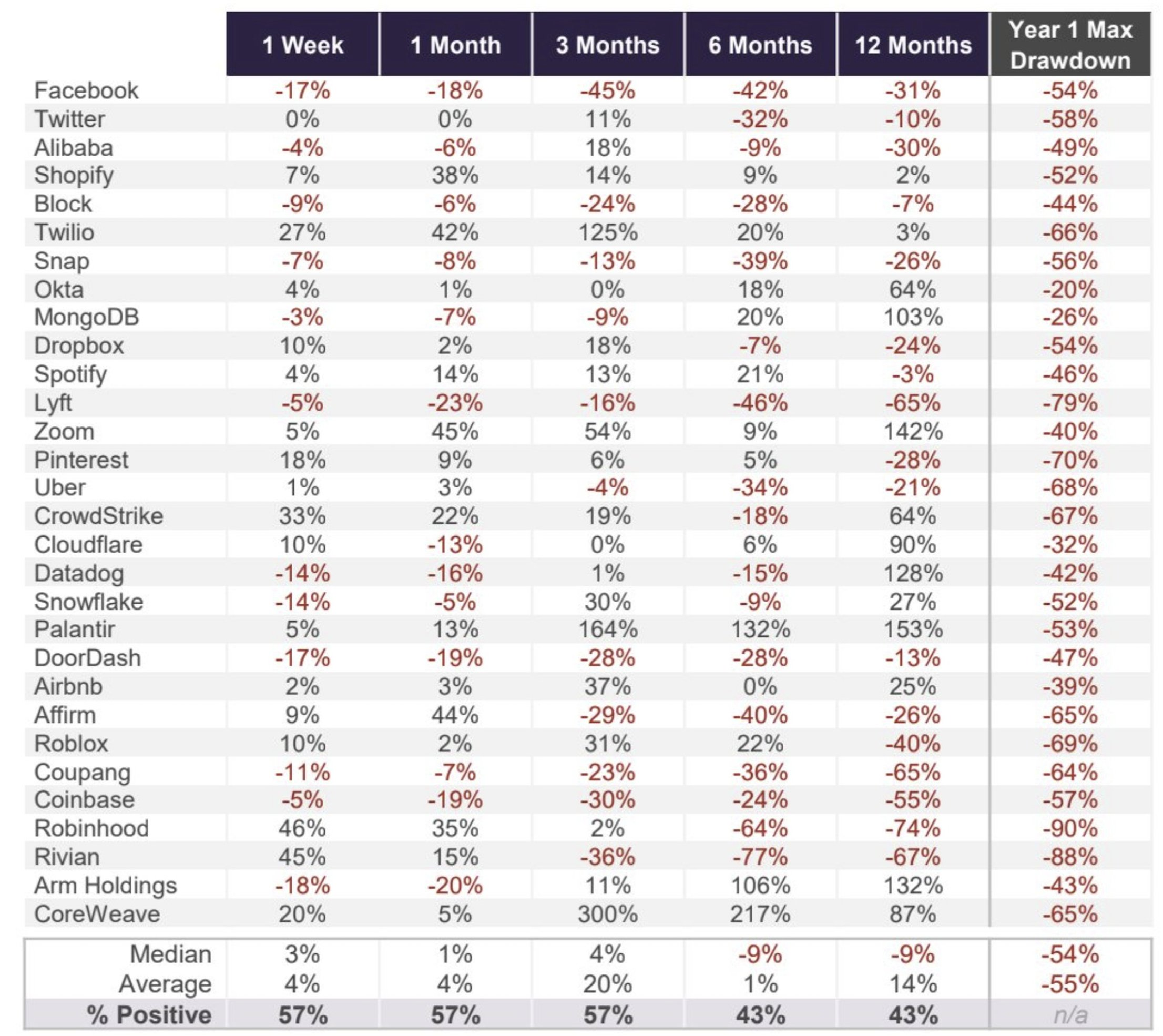

In an article published on June 9 by Motley Fool analyst Ryan Vanzo, the performance of 30 prominent tech companies since their IPOs in 2012 was analyzed, spanning from Facebook and Twitter to Coinbase, Robinhood, Rivian, Arm, and CoreWeave.

The shape of the median curve is telling: Median return in the first week is +3%, +1% in one month, +4% in three months, which is still acceptable so far. However, extending to six months, the median turns into -9%; and after twelve months, it remains -9%. The proportion of companies recording positive returns also collapses simultaneously, maintaining at 57% for the first three months, dropping to 43% for both the six-month and twelve-month marks. In other words, after a full year, most late buyers lose money.

The differentiation at the individual stock level is significant. CoreWeave surged 300% in three months, Palantir gained 164% in three months, and Zoom rose 142% after twelve months. But there are equally dense cases on the downside: Lyft dropped 65% after twelve months, Robinhood fell 74%, Rivian lost 67%, and Coupang decreased 65%. There is no stable relationship to be seen between the star halo and the returns post-IPO.

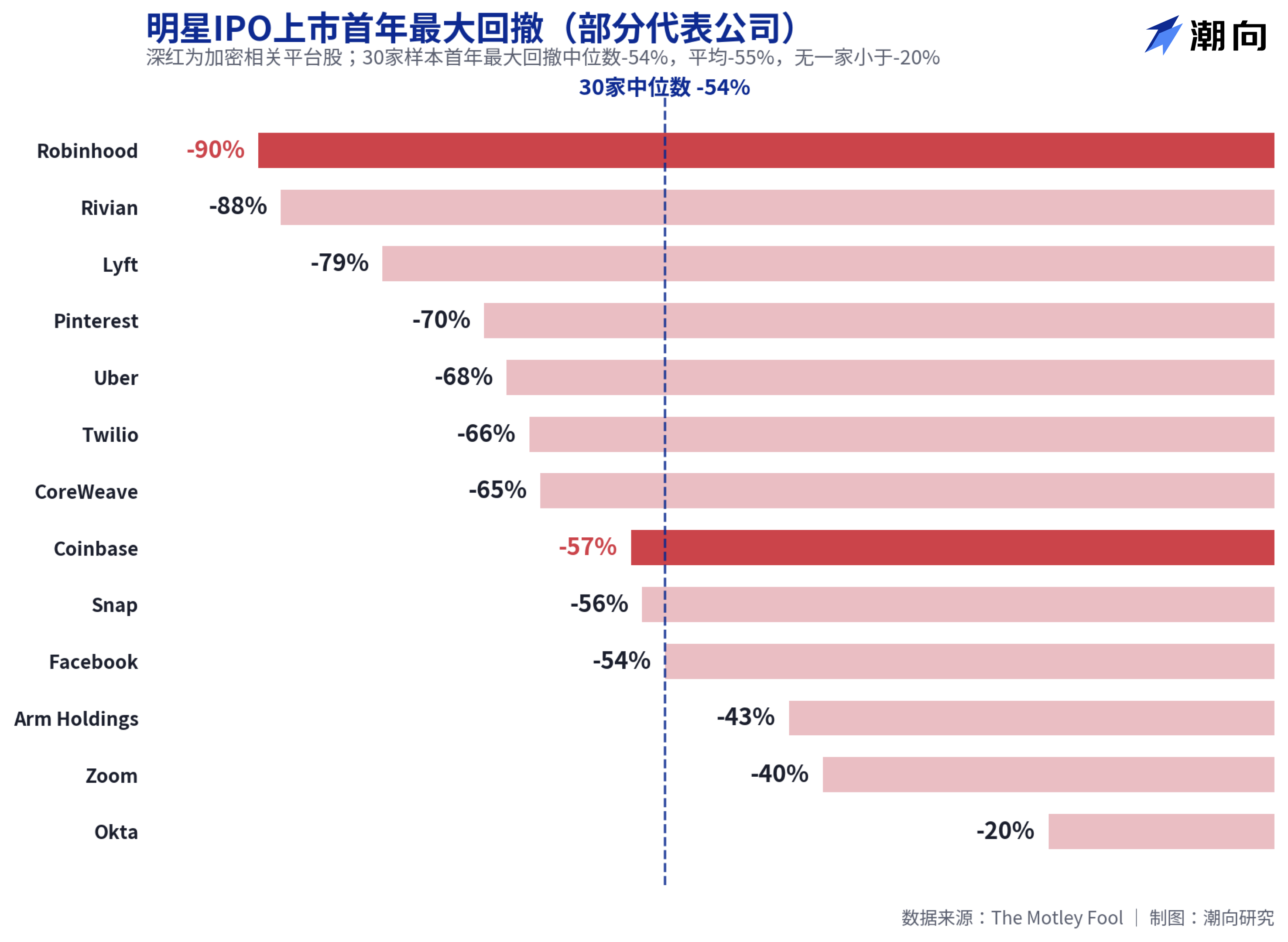

Median Maximum Drawdown of 54% in the First Year, Robinhood and Coinbase Both Dropped Over Half

More striking than the returns are the drawdown data. The median maximum drawdown in the first year for the 30 companies is 54%, with an average of 55%, and even the company with the smallest decline, Okta, retreated 20%, with no one escaping unscathed.

Two platforms familiar to crypto users are in the disaster zone. Robinhood saw a maximum drawdown of 90% in its first year, the highest among the 30; Coinbase had a drawdown of 57%. Even companies later validated as strong stocks were not exceptions: CoreWeave had a 65% drawdown in its first year, Palantir 53%, and Meta (then Facebook) 54%. This data points to a simple conclusion: even if you pick the right company, buying at the opening price likely entails first suffering a significant unrealized loss.

Academic research gives a similar picture. Jay Ritter, director of the IPO research project at the University of Florida, tracked 1,479 IPOs from 2012 to 2021, showing an average first-day return of up to 23.6%, but the average total return over the next three years is only 10.6%. The Wall Street Journal cited Ritter's data, stating that investors who bought on the first day and held for three years had returns about 21% lower than those who bought a market-cap-weighted index directly. The excitement of the first day essentially oversubscribed subsequent gains.

SpaceX's Ledger: $18.7 Billion in Revenue, Supporting $1.75 Trillion Valuation

Returning to SpaceX itself, the valuation debate is more specific than historical rules.

According to financial data cited by The Motley Fool, SpaceX is expected to generate $18.7 billion in revenue in 2025, a 33% year-over-year increase, but it will incur a net loss of $4.9 billion, reversing a profit of about $790 million in 2024. According to S-1 data compiled by BitMEX, the net loss for the first quarter of 2026 is expected to reach $4.28 billion, with cumulative losses of $41.3 billion, including AI business (after merging with xAI), burning about $2.5 billion each quarter. Based on a $1.75 trillion valuation, the price-to-sales ratio exceeds 90 times.

Morningstar's stance is the most direct. Analysts at the firm call SpaceX "severely overvalued," believing long-term investors will have the opportunity to buy at better margins after the IPO, setting a fair valuation at about $780 billion, less than half of the issue valuation. A reference point is that in December 2025, SpaceX's private buyout offer corresponds to an estimated valuation of about $800 billion, more than doubling in just six months.

There is also a logic for the bulls. The rocket launch business holds over 80% market share in the U.S., and Starlink has over 12 million subscribers and has become profitable, which forms the foundation for this valuation. Vanzo's own judgment is that SpaceX will likely perform well on its first trading day, but given the valuation level and historical data, it wouldn't be surprising if the stock price struggles in the next 12 months.

For those preparing to place orders on Friday, the data from these 30 companies is at least worth a glance: history does not guarantee a replay, but a drop of half in the first year is the norm for this game over the past fourteen years.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。