The U.S. Consumer Price Index (CPI) in May increased by 4.2% year-on-year, reaching a more than three-year high.

Written by: Maher, Foresight News

On the evening of June 10, Beijing time, the U.S. Bureau of Labor Statistics officially published the Consumer Price Index (CPI) data for May 2026. The report shows that a significant rebound in inflationary pressure occurred in the U.S. due to the sharp rise in energy prices triggered by geopolitical conflicts, leading to a further cooling in market expectations for the Federal Reserve's rate cut path this year. According to the U.S. Bureau of Labor Statistics data, May's CPI increased by 0.5% month-on-month (seasonally adjusted), slightly slowing from April's 0.6%, but increased by 4.2% year-on-year (not seasonally adjusted), significantly accelerating from April's 3.8%, reaching the highest level since April 2023. Core CPI (excluding food and energy) rose by 0.2% month-on-month, lower than the market expectation of 0.3% and April's 0.4%; year-on-year, it increased by 2.9%, slightly up from the previous value of 2.8%, in line with market expectations.

Energy prices are the core driving factor of this month’s inflation rebound. The energy index increased by 3.9% month-on-month and surged by 23.5% year-on-year. Among them, gasoline prices rose by 7.0% month-on-month and skyrocketed by 40.5% year-on-year; fuel oil rose by 58.9% year-on-year. The U.S. Bureau of Labor Statistics clearly pointed out that the energy index contributed to over 60% of the overall CPI month-on-month increase in May. Iran and related geopolitical conflicts have continued to push up international oil prices since February, with WTI crude oil briefly surpassing $100 per barrel, directly impacting gasoline and energy service costs in the U.S.

After the data was released, by the close on June 11, the S&P 500 index fell by approximately 1.62%, and the Nasdaq index dropped by 1.98%. The U.S. dollar index strengthened, and the U.S. Treasury yield curve shifted upwards overall.

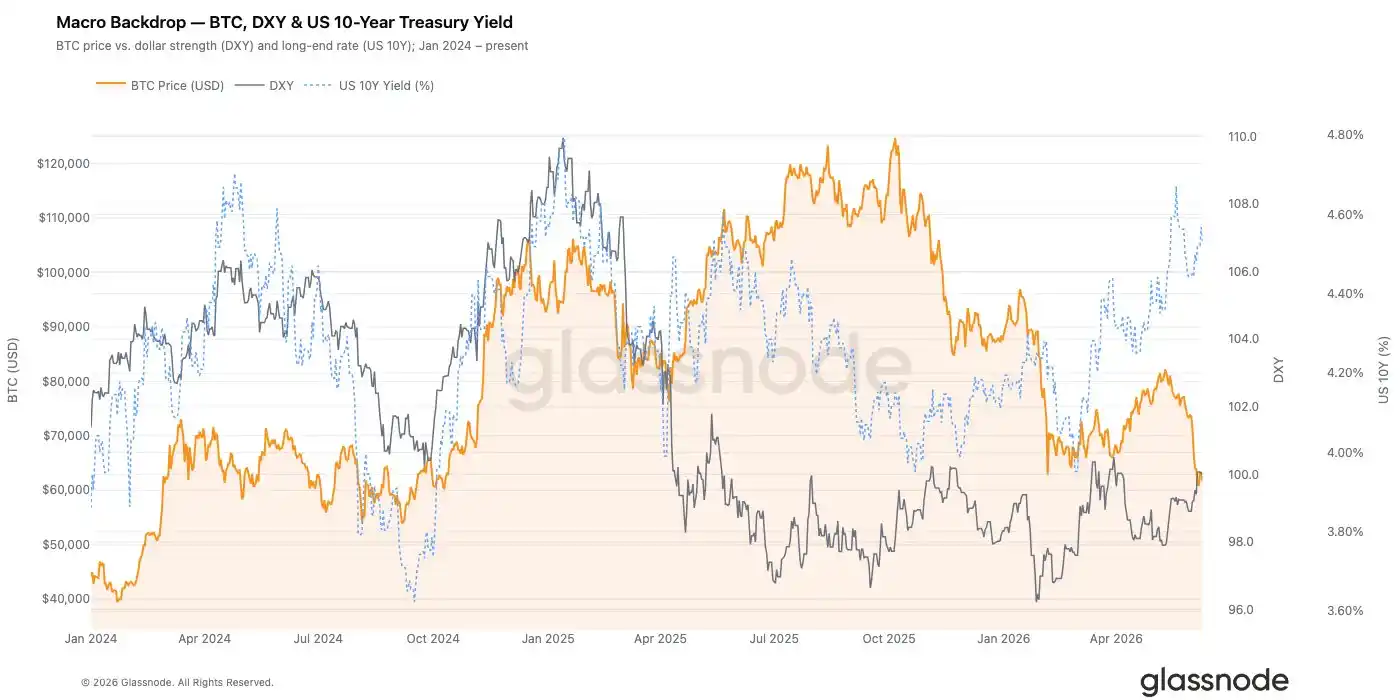

The cryptocurrency market, as a typical risk asset, is also facing significant pressure—Bitcoin prices fluctuated in the range of $61,000 - $62,000 before and after the data was released, with the market concerned that hot data may further compress liquidity expectations.

This Year’s Fed Rate Cut is Hopeless?

More critically, there is a repricing in the interest rate derivatives market. According to the CME FedWatch Tool, the probability that the FOMC meeting on June 16-17 will maintain the federal funds rate in the current target range of 3.50%-3.75% exceeds 96%. The probability of rate cuts for the entire year has significantly decreased; some traders have even begun to factor in the possibility of the first rate hike at the end of 2026 or in 2027. Previously, the market expected the possibility of 1-2 rate cuts of 25 basis points in 2026, but this path has now been significantly delayed or canceled.

Most institutions believe that this CPI has strengthened the expectation of "high rates being maintained for longer," but there is still distance to truly restart the rate hike cycle.

Olu Sonola, Chief U.S. Economist at international credit rating agency Fitch, stated: "Overall inflation is indeed very hot and is still rising, but this is not a story that necessitates panic-style rate hikes." He believes that core inflation remains relatively controlled, providing the Federal Reserve with room to remain on hold. In the future, the core inflation and inflation expectation data in the coming months will truly determine the policy direction.

Seema Shah, Chief Global Strategist at Principal Asset Management, stated that although overall inflation above 4% is still concerning, energy is the main driving force, and housing inflation is easing, with no widespread "second-round inflation effects" observed yet. Therefore, the Fed still has reasons to remain patient.

She also noted that market pricing for future rate hikes may currently be too high.

J.P. Morgan Asset Management believes that this data may be close to a peak in this round of inflation cycle. Chief Global Strategist David Kelly stated that although inflation levels remain above the target range, the "most likely decision" at the upcoming meeting is to keep rates unchanged, continuing to observe subsequent data changes.

Kalshi's latest data shows that the market bet on the Fed remaining on hold this year has risen significantly to 72%, while the probability of a rate cut once (25 basis points) has dropped to 18%.

This presents a sharp contrast to market expectations at the beginning of the year. In early 2026, the market widely believed that the Fed would start a rate cut cycle against the backdrop of sustained declining inflation. The April CPI year-on-year had risen to 3.8%, and May's data further confirmed the inflation rebound trend, making the high-rate policy environment the mainstream narrative once again. While external shocks from energy prices have a certain temporary nature, if they are transmitted to core service prices, they will force the Fed to reassess neutral interest rate levels.

For the newly elected Chairman Waller, the June meeting is an important debut. Waller officially took office as Chairman of the Federal Reserve in late May 2026, succeeding Jerome Powell, whose term has ended. The June meeting will release a new economic forecast summary and dot plot, and the market will closely monitor officials’ latest assessments of the inflation path, employment market, and policy interest rates.

From a deeper analysis, the slowdown of the core CPI in May to 0.2% provides a certain easing signal, indicating that potential inflationary pressures have not fully spiraled out of control. However, the Fed has historically placed more emphasis on the "trend" of core indicators rather than single-month fluctuations, especially in the context of severe energy price volatility. The persistent stickiness of housing costs, potential second-round effects (energy costs pushing up prices of other goods and services), and geopolitical uncertainties all increase the complexity of policy-making.

Cryptocurrency and U.S. Stocks

The Fed's policy path is a core anchoring factor for the global liquidity environment. High rates or delayed rate cuts are usually accompanied by a strengthening dollar, rising U.S. Treasury yields, and pressure on valuations of risk assets. The correlation between Bitcoin and growth assets like the Nasdaq has significantly increased in recent years, with marginal changes in liquidity expectations often reflected first in BTC prices and ETF fund flows.

SoSoValue data shows that since May of this year, there has been continuous large net outflow from Bitcoin spot ETFs, leading to pressure on Bitcoin prices; BTC briefly fell below the $60,000 mark and has since fluctuated around $62,000, with the potential to drop below that level again at any time.

The current cryptocurrency ecosystem is much more mature than during the 2022-2023 bear market, but in the short term, CPI data may still trigger a rollback in risk appetite, deleveraging, and amplified short-term volatility.

The latest weekly report from Glassnode shows that Bitcoin continues to show characteristics of late-stage adjustments, with recent buyers facing significant losses, and realized losses remaining high, while several major sources of demand have weakened significantly. Bitcoin prices dropping near $60,000 triggered a significant deleveraging event that cleared a large number of speculative positions from the market. Although this helps reset leverage levels, spot demand has not shown substantial recovery. The options market remains defensive, with implied volatility staying high and strong demand for downside protection, and trader positions concentrated around current spot levels. Additionally, lower institutional participation and slowing accumulation of corporate bonds indicate that risk appetite remains subdued.

Overall, the market seems to be further entering a phase of surrender. Although leverage has basically been reset and valuation indicators have reached historical lows, the demand response typically associated with long-term market bottoms has not yet occurred.

Historical experience shows that when inflation is primarily driven by supply-side factors such as energy and core data remains relatively controllable, the market often gradually repairs expectations for a "soft landing" after digesting the initial shocks.

As for U.S. stocks, major investment banks maintain an optimistic outlook. However, J.P. Morgan Asset Management believes that this data may be close to a peak in this round of inflation cycle. Chief Global Strategist David Kelly stated that although inflation levels remain above the target range, the "most likely decision" at the upcoming meeting will be to keep rates unchanged and continue observing subsequent data changes.

J.P. Morgan notes that energy shocks and other "one-time shocks" may become the new normal. The AI investment cycle continues, but also warns that inflation is now above pre-pandemic levels, and the correlation between stocks and bonds may structurally rise, putting more pressure on the 60/40 portfolio.

Goldman Sachs recently raised its S&P 500 year-end target to 8000 points (up from 7600), forecasting a 24% EPS growth in 2026. They believe that earnings growth remains the main driver of the stock market; however, they pointed out in recent comments that the probability of the Fed lowering rates this year has significantly decreased.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。