Humans can be without a future, but will never stop plundering.

Written by: Crypto Weituo

Fiat currency is the most efficient, discreet, and iterative plundering tool in human history.

It can be created out of thin air by regimes -- they just need to continuously prove that this currency can be unconditionally exchanged for the core materials necessary to maintain the operation of human society.

The problem is that the true threshold for human survival is merely food and reproduction, low enough that it cannot consistently prove the need for fiat currency and regimes. Therefore, the fiat currency system must continuously raise the cost of human survival around a certain "material" to justify the reasonableness of plundering. This process is what we call "development" -- continuously creating mismatches in essential demand, using new mismatches to rationalize the previous round of mismatches.

This is the Ponzi scheme of fiat currency, including the US dollar.

This material was once gold, then oil. After the 1974 Saudi agreement, petrodollars supported the dollar system for a full 50 years. However, this mechanism began to structurally fail after 2024 -- Saudi Arabia accepting RMB settlement, OPEC dollars no longer automatically flowing back into US Treasuries, and dollar printing happening faster year after year.

It needs a new material to support the next 50 years and must do so before the complete failure of petrodollars.

This time, it has chosen AI. I refer to it as "USD-AI Ponzi."

This "AI Ponzi theory" will be scoffed at by traditional US stock "orthodox players." But for native players in the cryptocurrency circle who are already familiar with the three-market theory and have honed their Ponzi instincts and adversarial thinking through countless zero-sum trades -- there is no need to belittle oneself or give up their strengths.

This series aims to help these players quickly establish an understanding of narrative-driven stocks without conflicting with underlying cognition, so they can enter the stock trenches in the most advantageous posture and maximize benefits in this still unfolding "stock market cryptocurrency integration."

The series is divided into three parts: upper, middle, and lower, with this being the upper.

Final Water Source of AI Upstream -- Systematic Cognition of Dollar Ponzi

The dollar itself is the best Ponzi textbook.

The mismatch between funding demand and expected returns creates a "gap," and this "gap" can only be filled by further mismatches.

- Funding Demand: The US Treasury has an annual deficit of $2T+, and the government needs to continuously spend; the Federal Reserve must continuously print money to meet the liquidity needs of the financial system.

- Expected Returns: Holders of dollar assets (bonds or cash) -- their actual purchasing power does not shrink, outpacing inflation.

- Gap: The composite growth of government spending + interest (with an annual deficit of $2T+, accumulated national debt of $36T, and interest payments already at $1T+) and the actual amount of debt the economy can absorb is destined to become irreconcilable in the long run.

In the short term, new debt can be issued to fill the gap -- but issuing new debt requires someone to buy it. Domestic capacity is limited, while overseas structural selling (China's holdings decreasing from $1.3T to $0.7T) leaves only the Federal Reserve's printed money for monetization. Regardless of whether more debt is issued or the Fed prints money, it ultimately dilutes the purchasing power of each dollar -- creating a natural conflict with the expectation of "real returns outpacing inflation" for holders.

Therefore, the dollar always requires a "material" that can absorb the printing speed of the Federal Reserve and has rapidly growing demand.

If there is no material to absorb: The dollar pushes up prices → The purchasing power of dollar asset holders is diluted → They sell dollar assets → The scale of selling exceeds the capacity of any buyer to absorb → The Fed can only monetize and take over → It prints more money → Inflation spirals further out of control → More selling.

The dollar system continuously creates bubbles and seeks new materials to absorb dollar inflation; this is the dollar's essential survival need.

Using the three-market integration to view the dollar:

- US Treasuries are the dividend market. Central banks, money market funds (MMF), US banks, and life insurance invest money in US Treasuries to earn interest. The Treasury continuously issues new debt, with interest paid from taxes + new debt -- a relay-style deposit. This is geometrically identical to a dividend market, except this dividend market has the backing of the US military + global settlement demand, supporting it for 80 years.

- The closed loop of the Fed - Treasury - banks is a mutual aid market. The Fed prints money for banks, banks buy Treasuries, and the Treasury uses this money for spending, which returns to the banking system as deposits, allowing banks to buy more Treasuries. A→B→C→A completes the accounting cycle. The core of this mutual aid market is the Fed's own balance sheet -- it expands to double its size, amplifying the cycle. It expanded five times from 2008 to 2014 and expanded again by one time in 2020.

- The dollar split market breaks down dollar demand to be absorbed by a global "material." The printed dollars must have a destination; otherwise, the return flow results in inflation. This absorbing material is the material mentioned earlier -- historically, it was gold, then oil, and now it is AI.

AI is the largest split market for dollars currently

This time is different? This time is the same.

People outside the cryptocurrency circle are most likely to rebut: "AI is truly useful, ChatGPT really boosts productivity, OpenAI has $25B in annual revenue, how can it be a Ponzi?"

Brothers, at this moment, it is just like then: "L2 really has ordering fees, ZK can truly generate returns, how can it be a Ponzi?"

L2 and ZK are both split markets of ETH.

The fees of L2 are real. But it must rely on the continuous issuance of new assets to absorb external liquidity -- without new tokens, new protocols, or new applications coming in, revenues dry up immediately, and TVL is withdrawn. Failed L2s almost all die from this.

As early as the end of 23, I predicted the greatest disaster for ETH -- the main stage for asset issuance was taken over by Solana / BSC, and ETH gas + destruction mechanisms immediately fell into structural stagnation, prices against BTC hit new lows. It wasn't a technical retrogression of ETH; it was its split market that collapsed.

At this time, someone might retort: "But the downstream semiconductor industry is different -- NVDA / TSMC / Marvell are genuinely producing things, with real cash flow, isn't that just basic?"

Producing tangible items is certainly true, and cash flow is also true. However, the current long-term profit expectations of semiconductor companies are entirely built on the premise of "the dollar system continuously injecting liquidity + the cloud giants maintaining AI capital expenditure of $300B+/year."

The $1T+ annual expansion speed of this AI chain far exceeds the actual revenues that downstream AI companies can create -- and the majority of this real revenue essentially replaces human labor with AI, causing irreversible job losses. It must rely on an ongoing influx of external funds to sustain.

Once the Ponzi input from the dollar system stops → AI narrative valuation stalls → cloud giants' capital expenditures stagnate → NVDA's future revenue declines → future PE explodes → overall valuation re-prices → semiconductors return to cyclical stock valuations.

This is akin to L2 / ZK, the only difference is the sources of external liquidity relay. It is entirely possible to compare the current "fundamentals" of semiconductors with the TVL, address count, transaction volume, and mainstream adoption of L2 in 23/24 -- they are all narratives driving split markets.

After all, back then Trump said to monetize debt with cryptocurrencies; isn't AI serving as a connection for dollar inflation also a form of monetizing debt? The core is all about making this liquidity relay seem more reasonable.

Three Thousand Worlds -- Disassembling the Ponzi Structure of the Internal AI Industrial Chain

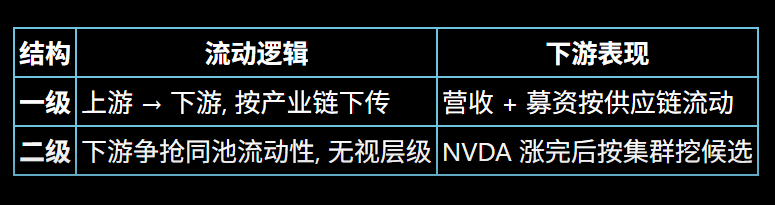

AI upstream is itself a mutual aid market.

Having reached this point, the logic of AI as a split market for the dollar becomes clear. But within AI, the upstream (end applications + cloud giants + chip design) itself constitutes a mutual aid market -- supporting each other's revenues, objectively stabilizing the total market value of various companies (which is the "liquidatable asset" in the mutual aid market):

- Microsoft invests $13B in OpenAI + Azure cloud service credits → OpenAI spends $12.4B on computing power on Azure.

- NVDA lends money to CoreWeave to purchase NVDA's own GPUs.

- Google invests in Anthropic, Anthropic spends on Google Cloud.

- Oracle - OpenAI five-year contract bundled.

The money never leaves this cycle but creates a mutually beneficial accounting: OpenAI's annual revenue is $25B + Azure AI revenue grows 50%+ year-on-year + Mag-7 stock prices reach new highs. This is geometrically identical to the mutual aid structure of the Fed - Treasury - banks, just at a smaller scale.

If you cannot see AI as a Ponzi, just look at Microsoft giving OpenAI money to spend on Azure.

This upstream mutual aid market is the "initiating ground" for AI CAPEX capital expenditures -- it determines the direction and magnitude of AI capital expenditure and decides how many orders the entire downstream supply chain can obtain.

The inter-investment in upstream stabilizes the liquidatable assets on the books (Mag-7 + total market value of AI companies) at high levels; any individual shareholder wanting to exit can reclaim cash close to the book price. It is this expectation of being able to exit "whenever" that keeps retail investors/ETFs/401k continuously buying in.

This is the core mechanism allowing the AI split market to maintain an annual expansion of $1T+.

Dual Paths within AI's Split Market

Returning to the definition of a split market:

"A split market is a kind of Ponzi system, where the total funds remain constant at a given time, but the amount of rights or assets corresponding to each unit of fund is exponentially increased, while the price of newly generated rights or assets is proportionally lowered to attract subsequent capital inflow."

As AI is the split market of the dollar, it needs to attract capital inflow. This capital inflow comes through two pathways:

- Primary market: Through capital expenditure as revenue and primary fundraising, it is transmitted down the supply chain to downstream manufacturers.

- Secondary market: It does not follow supply chain hierarchies but has all AI downstream entities competing for the same pool of liquidity.

Having discussed the upstream, now we look at the overall split market of AI downstream:

- Supporting semiconductor industry: Marvell, HBM manufacturers (SK Hynix / Samsung / Micron), optical modules (Lumentum / Coherent), power supplies (Vertiv / Eaton), data center REITs (Equinix / DLR).

- Foundry + equipment: TSMC, Samsung Foundry (foundry); ASML, Lam, KLA, Applied Materials (equipment).

- Upstream energy + end tail: SMR nuclear power / power PPA / perilla leaves / long-tail narrative small cap.

Each player downstream is shaped like a dividend market -- investing in fabs / production capacity (sunk costs) → waiting for upstream orders to be fulfilled → profit distribution / buybacks. SK Hynix invests in HBM fab, Lumentum invests in optical module production lines, TSMC invests in wafer foundry, all are the same market shape.

Of course, it is important to emphasize that the Ponzi attributes of the downstream do not come from themselves but rather from the upstream AI transmission. Excluding the revaluation led by the AI frenzy, these companies' valuations would revert to cyclical stock levels. The Ponzi referred to here is this premium, not their original "fundamentals."

Primary vs. Secondary, Two Structures

Up to this point, we have only seen liquidity transmission in the primary market (revenue + capital expenditure). However, speculative capital in the secondary market is not restricted by supply chains but moves according to narrative clusters.

When the gains of the upper levels are no longer α but β (for example, NVDA has risen, and the market agrees), speculative capital will seek underpriced candidates in the same narrative regardless of their supply chain level.

For example, under the "AI choke point narrative" cluster initiated by the white-haired stock god @aleabitoreddit:

- Vertiv (data center power/cooling)

- Marvell (NVDA ASIC collaboration)

- Equinix / DLR (data center REIT)

- Lumentum (optical modules)

- Lam / KLA (equipment)

These entities vary by layer in the supply chain but compete for the same pool of "AI choke point narrative liquidity" in the secondary market.

Thus, the condition of a split market "splitting rate being too high" materializes in the secondary market not as "suddenly more competitive enterprises appear" but as:

This narrative logic becomes widespread, leading to an accelerated discovery and attention to lower-valued targets in lower supply chain layers, resulting in increasingly rapid capital rotation in the secondary market -- which is the tactic of "diversion" familiar to trench players.

Corresponding to P Xiaojang's approach, it can be interpreted as: buying at the bottom, going out to promote, profiting (whether to take profit or not is another matter). His perilla leaf theory is a logically sensible theory that is hard to falsify, resembling the meme as cult theory proposed by @MustStopMurad.

White teacher is completely correct, but the most important aspect of his trading strategy is still "buying at the bottom" -- such as Raspberry Pi and SIVE.

The Rationality of "Trench Trading" in the Stock Market's AI Split Market

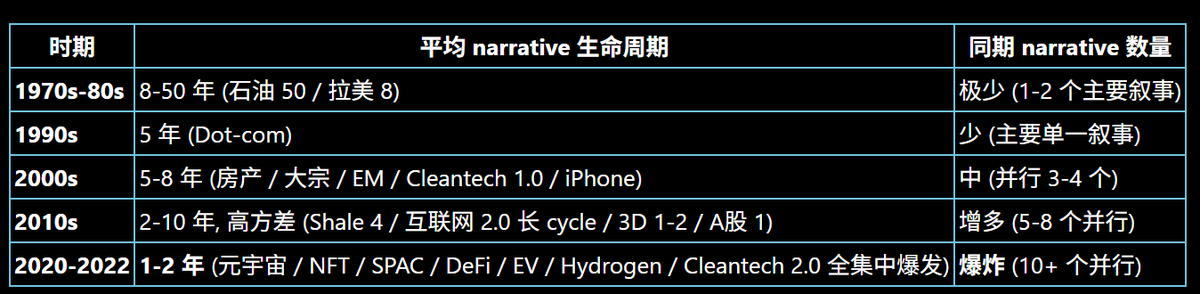

There is no need to argue whether stock trading should be "value investment" or "long-term holding." In fact, even in the US stock market, since the 2001 dot-com bubble, the life cycle of narratives has significantly shortened:

- Speed of information dissemination: newspapers (days) → television (hours) → internet (minutes) → social media + algorithm recommendations (seconds)

- Capital cross-border mobility: especially after 2014 with the involvement of Asian speculative capital. Chinese capital brings a completely different tactical system for capital speculation -- cryptocurrencies are essentially a branch evolved from cross-border Asian speculative capital flow, bringing a logic entirely different from traditional US stock institutions.

- Institutional HFT (high-frequency trading): Contrary to many people's assumptions, most institutions are not "value investing" but rather high-frequency algorithmic quantitative trading -- accounting for 50% of current US stock trading volume. Institutional trading teams' algorithms are continually converging in competition, displaying features of "together we build high rises, together they collapse."

- Increased retail participation: The conclusion that “US stocks are institutionally dominated” has long been outdated. With various brokerages promoting retail trading, retail trading volume in US stocks has exceeded 25%, making meme stocks like GME possible. Furthermore, retail investors, especially the young, have seen their attention spans shorten over the past decade -- this has become a physical limitation in their trading logic.

Traditional markets refer to this as reflexivity; in the three-market theory, this is "the audience determines the market shape."

Having reached this point, my readers should now understand:

- The upstream mutual aid market is more stable than the downstream split market; within the downstream, the closer to the core of the AI choke point (TSMC / ASML / HBM), the more stable it is; the further out (perilla leaf theory / long tail), the more fragile it is -- the ability of the mother market to lock in capital and expectations does not decline along the supply chain but diminishes along the center distance of the secondary narrative cluster.

- The goal of trading is to exit these split markets before any signs of even a short-term collapse appear.

When playing stocks, there is only one secret: buy low, buy early.

The kid who "shined Rockefeller's shoes" might be a chosen stock trading prodigy, but the entire market at a specific point in time has a limited amount of remaining shares to absorb, a specific size of 100,000 soldiers. If you arrive late, you can only become that "cost," becoming the exit liquidity for Rockefeller.

And how to judge whether you bought low, bought early, and where you stand in the liquidity hunter queue is a lifelong pursuit for every player in the market.

This does not differ materially from trench trading by P Xiaojang's approach: you are not judging the fundamentals but rather how many people believe in the "fundamental narrative," and then act as early capital -- just that the tools and grips for judgment are different.

So, on what basis to judge?

Grand narratives can deceive, liquidity expectations cannot.

The next article will discuss how to understand and judge your relative position for entry from "capital inflow and outflow" liquidity.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。