Source: Wall Street Watch

The analysis institution SemiAnalysis, a star in the AI industry chain, released a report directly pointing out that the two core technology paths for AI data centers will be delayed, triggering a violent shock in the optical communication sector on June 10, while also sparking intense debate in the investment and industrial worlds regarding future technology routes and investment opportunities.

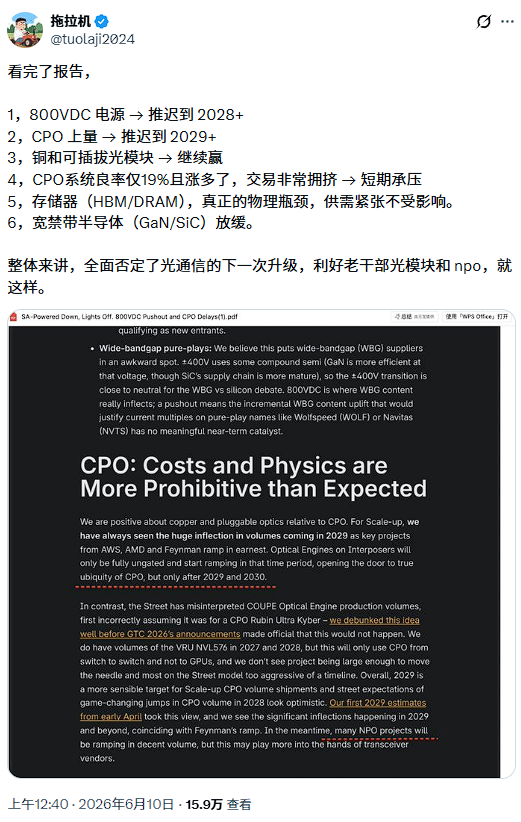

The report believes that the shipping of NVIDIA's 800VDC power architecture will be delayed until 2028, and the mass production of CPO (Co-Packaged Optics) may be postponed until 2028 or even 2029. The simultaneous downward revision of these two expectations caught the market off guard.

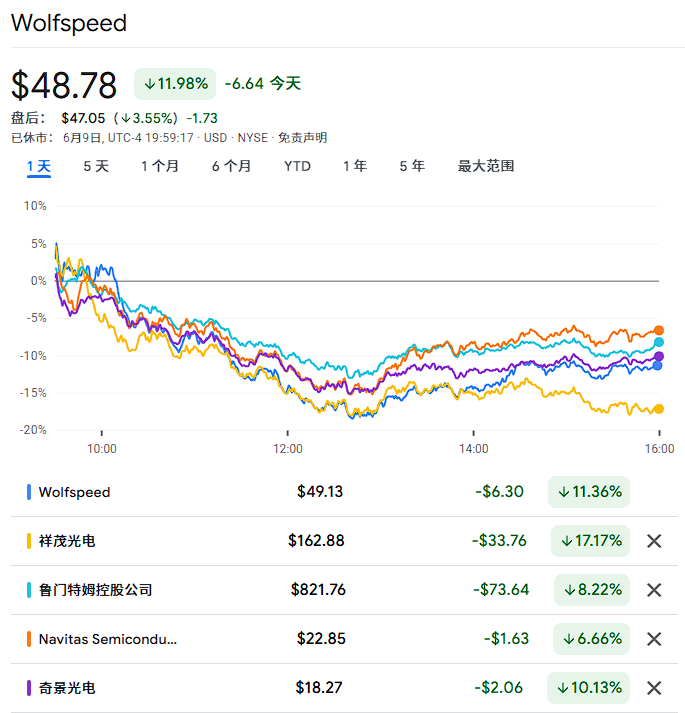

After the news broke, the US optical communication sector saw widespread declines. AAOI fell by as much as 17% in a single day, Lumentum dropped about 8%, and companies such as HIMX, Navitas Semiconductor Corp, and Wolfspeed, which were named in the report as holding a cautious attitude, also faced significant pressure.

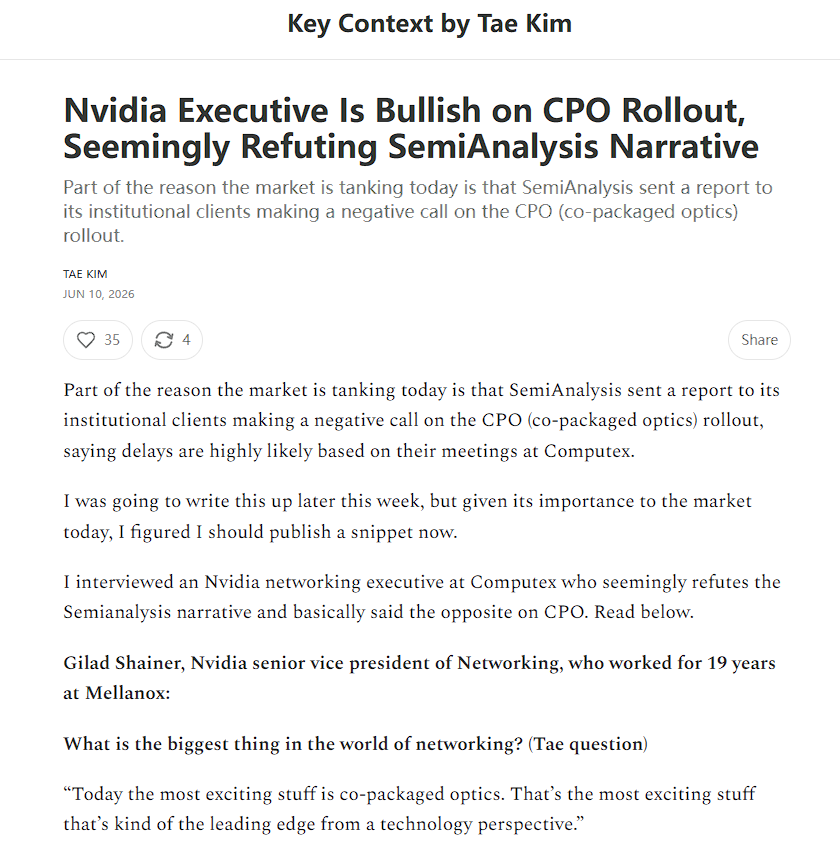

At the same time as the SemiAnalysis report was released, an interview with NVIDIA executives was also published. According to senior semiconductor and technology investment journalist Tae Kim, NVIDIA's Senior Vice President of Network Business, Gilad Shainer, expressed a starkly optimistic stance on CPO at the 2026 Computex, stating that "CPO is the most exciting technology right now," and mentioned that mass shipping will begin in the second half of the year, which sparked a heated debate on the CPO timeline on social platforms.

It is noteworthy that several market observers pointed out that the delay of CPO does not mean that the demand for optical interconnects has disappeared, but is more likely to redirect capital flow back to traditional pluggable optical modules and NPO (Near Package Optics) tracks—this logic led some investors to seek opportunities in panic selling.

Core of the SemiAnalysis Report: Both Technology Paths Delayed

In this research note sent to institutional clients, SemiAnalysis provided two core judgments that have far-reaching impacts on the market.

The 800VDC power architecture will be delayed until after 2028.

The report pointed out that NVIDIA's original plan to massively adopt single-ended 800VDC power designs has seen a significant delay in the shipping window. Large-scale cloud vendors currently prefer to stick with mature low-voltage solutions or gradually transition to 400VDC, rather than rush to switch to 800VDC.

The report argues that the marginal efficiency gains of 800VDC under current grid power conditions are insufficient to justify its system complexity. In contrast, the 400VDC products are expected to begin mass shipping in the second quarter of 2026, with significant growth anticipated in 2027.

The mass production rhythm of CPO is significantly behind market expectations.

The report states that the shipment volume of CPO in 2027 will be significantly lower than previously aggressive predictions, with the time point for mass production possibly delayed to 2028 or even 2029. The main bottlenecks are concentrated in three areas:

The yield of optical engine connections (optimistically about 95%, but the CPO production driven by a single ASIC is still extremely limited), the integration difficulty of ASICs, and overall cost economics.

The shipment volume of scale-out CPO switches faces downside risks, and shipments relying on new platforms like Rubin Ultra/Kyber will also be postponed to the 2028 window.

At the stock level, SemiAnalysis maintains a relatively positive view on Amphenol, Vertiv, and Legrand, while holding a cautious attitude toward Lumentum, HIMX, Navitas Semiconductor, and Wolfspeed.

However, the report itself also acknowledges that CPO as an important direction for future data center network architecture has not been denied, and the core reason for the delay is that engineering challenges have yet to be fully overcome, rather than the disappearance of demand.

At the same time, the report also points out that some NPO projects may accelerate.

NVIDIA Executives Publicly Disagree, Tae Kim's Exclusive Interview Draws Attention

At the same time that the SemiAnalysis report was widely circulated among institutions, senior semiconductor and technology investment journalist Tae Kim published a transcript of a one-on-one interview with NVIDIA's Senior Vice President of Network Business Gilad Shainer during Computex in his Substack column, which sharply contrasts with the judgments made by SemiAnalysis.

Shainer stated in the interview, "The most exciting thing today is co-packaged optics, which is the leading direction at the forefront of technology."

He further revealed that NVIDIA is ready to start shipping, and partners like Lambda have published blogs confirming that they have received CPO switches, with mass CPO deployments set to accelerate in the second half of the year and extend from scale-out to scale-up scenarios. "If it were up to me, I would want CPO to be used everywhere optical networking is needed."

Tae Kim added in the article that Shainer's overall demeanor and body language during the interview showed great enthusiasm for the near- and long-term volume increase of CPO. He expressed that this statement "seems to directly contradict the narrative of SemiAnalysis."

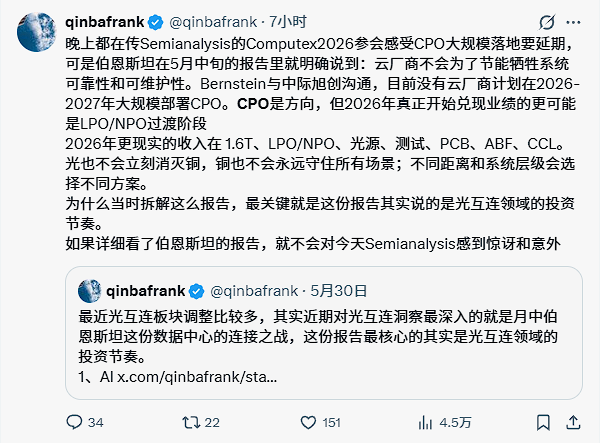

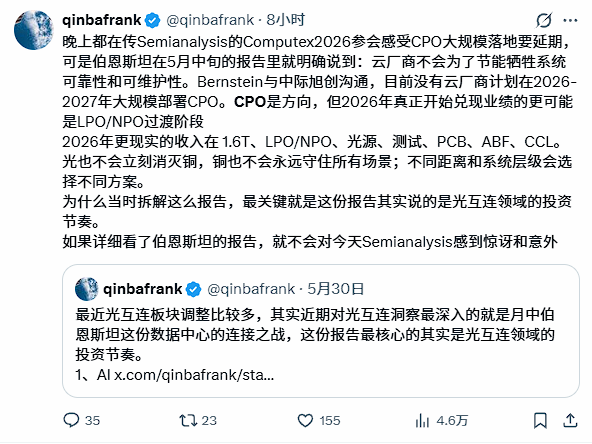

This contrast has plunged the market into an information war. A user on the social platform X, @qinbafrank, pointed out that Bernstein made it clear in a mid-May report that cloud vendors will not sacrifice system reliability for energy savings, and currently, no cloud vendor plans to deploy CPO on a large scale between 2026 and 2027, "If you had looked closely at Bernstein's report, you would not be surprised by today's SemiAnalysis."

Netizens Debate: Is the CPO Delay a Negative or a Misjudgment?

The market turbulence triggered by the report quickly spread to social media, with significant differences in opinions surrounding the investment logic of the CPO delay.

Bearish View: Yield and Reliability are Real Bottlenecks.

SemiAnalysis emphasized in the report that under the CPO architecture, the optical engine is co-packaged with large ASICs worth tens of thousands of dollars on the same substrate. If the optical engine fails due to laser aging or fiber damage, it often requires the entire motherboard to be disassembled and returned for repair, resulting in maintenance costs and downtime risks far greater than traditional pluggable modules. This engineering challenge is viewed as a core obstacle to the large-scale implementation of CPO in the short term.

Bullish View: CPO Delay Actually Benefits Pluggable Modules and NPO.

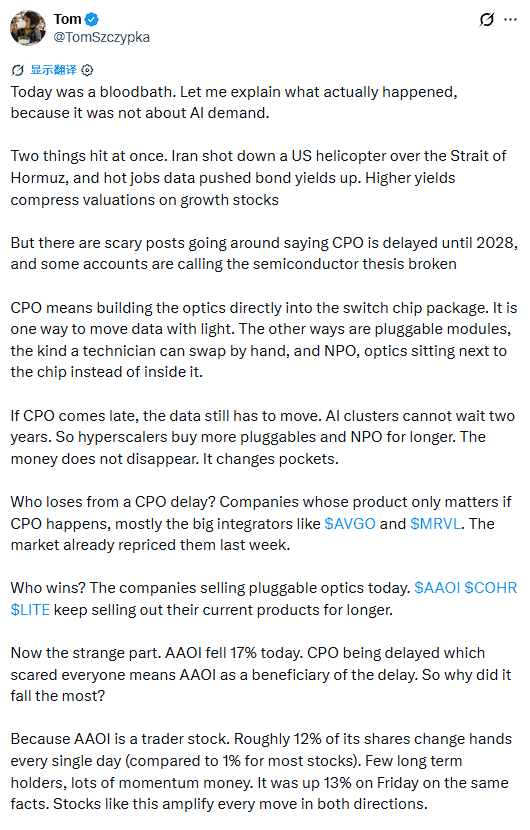

A user on social platform X, @TomSzczypka, analyzed, "If CPO is delayed, data still needs to be transmitted, AI clusters cannot wait two years, large-scale cloud vendors will buy more pluggable modules and NPO for a longer time, the money will not disappear, it has just changed pockets."

He also noted that the phenomenon where AAOI's drop (17%) significantly exceeded Lumentum's (8%) indicates that the market's selling that day was not based on rational analysis but was a clean-out of the weakest holdings.

User @michaelsikand stated that currently any revenue from CPO for photonics companies is zero, and the current high-speed growth comes from huge, unmet NPO opportunities, "the timeline may be delayed, but the TAM will not."

Voices Questioning the Logic of the Report Also Exist.

User @cherryPayment published a lengthy article pointing out internal contradictions in the SemiAnalysis report: on one hand, the report states that the supply chain will not be ready by 2027; on the other hand, it predicts that Celestial AI (acquired by Marvell) will achieve a revenue run rate of $1 billion by the end of 2028, and that Amazon has signed contracts for Trainium 4, "You cannot suddenly have $1 billion by the end of 2028 if the supply chain was not prepared for anything in 2027."

He further noted that the target readers of SemiAnalysis are procurement decision-makers at large-scale cloud vendors, and their conclusion is "not yet time to go all-in," rather than a timing judgment for capital markets, "they are analyzing deployment rhythm, not investment timing."

User @Herman Jin on platform X criticized the timeliness of information from US investment research institutions, stating that the delays of CPO and 800VDC "are just a matter of time," and that relevant information has long circulated in institutional circles; SemiAnalysis's report merely formalizes already known information.

Unexpected Beneficiaries: Copper Connections and Pluggable Modules

In the context of widespread market pressure, some analysts have turned their attention to potential beneficiaries of the CPO delay.

User @qinbafrank summarized that more realistic revenue opportunities in 2026 are concentrated in 1.6T pluggable modules, LPO/NPO, light sources, testing, PCB, ABF, and CCL, "light will not immediately eliminate copper, and copper will not forever dominate all scenarios; different distances and system levels will choose different options."

Lumentum's CEO recently stated that interest in NPO among NVIDIA's non-customers has significantly increased over the past two months.

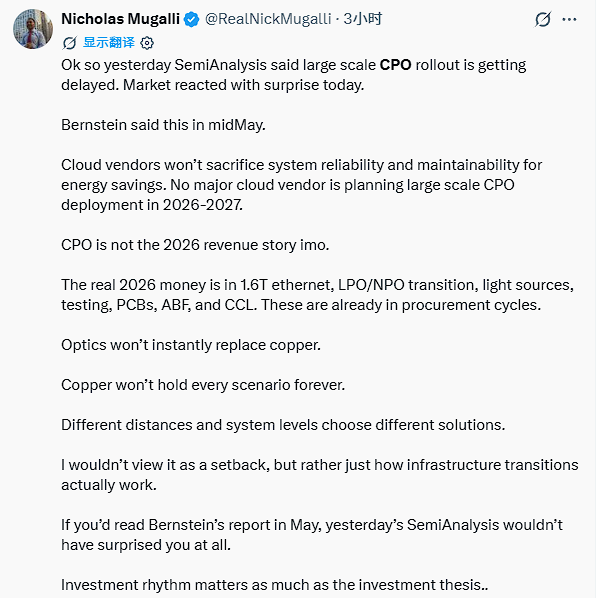

User @RealNickMugalli analyzed that at a rate of 1.6T and 200G per channel, copper cables have already reached physical limits even when combined with retimer technology, and optical solutions will become a mandatory option over reasonable distances rather than an optional one, with the potential market size for NPO possibly exceeding that of CPO.

SemiAnalysis also pointed out in its report that some NPO projects may accelerate, and 400VDC products will start mass shipping in the second quarter of 2026. For companies like Amphenol and Vertiv, the report maintains a relatively positive stance, believing they will benefit from the continued demand during the 400VDC transition period.

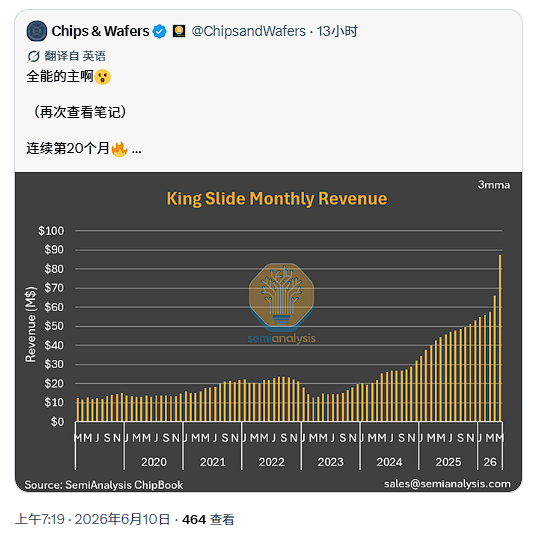

User @TomSzczypka cited industry chain data from this week to corroborate that AI infrastructure demand has not weakened:

Fujikura raised data center cable prices because almost all US hyperscalers placed orders simultaneously; King Slide's Rack Rail revenue increased by 47% month-on-month; Google ordered 6 million TPUs from Intel; and SK Hynix signed a long-term storage cooperation agreement with NVIDIA.

"The real bottleneck for AI is power, storage, and GPU, none of which has worsened today."

Meanwhile, @tuolaji2024 posted on social platform X stating that memory (HBM/DRAM) as a real physical bottleneck is completely unaffected by this technology delay event.

Analysis points out that considering various viewpoints, the market fluctuation triggered by the SemiAnalysis report reflects more of a recalibration of the technology roadmap timeline rather than a fundamental reversal of overall AI data center demand.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。