Original author: Long Yue

Original source: Wall Street Journal

At 20:30 Beijing time tonight, the U.S. Bureau of Labor Statistics will release the CPI data for May. This is also the most closely watched inflation data by the market before the policy interest rate meeting of the new Federal Reserve Chair Waller next week.

According to news from the Trading Desk, the four major institutions on Wall Street—Goldman Sachs, UBS, Deutsche Bank, and Morgan Stanley—are intensively releasing forward-looking reports on the eve of the data release. The forecasts from these four institutions vary but are aligned in direction: overall inflation may be very high, but core inflation may not be so hot. Energy prices push the overall CPI up, while factors like rent and car insurance suppress the core CPI.

Overall CPI may exceed 4% to create a three-year high, core CPI may be below consensus

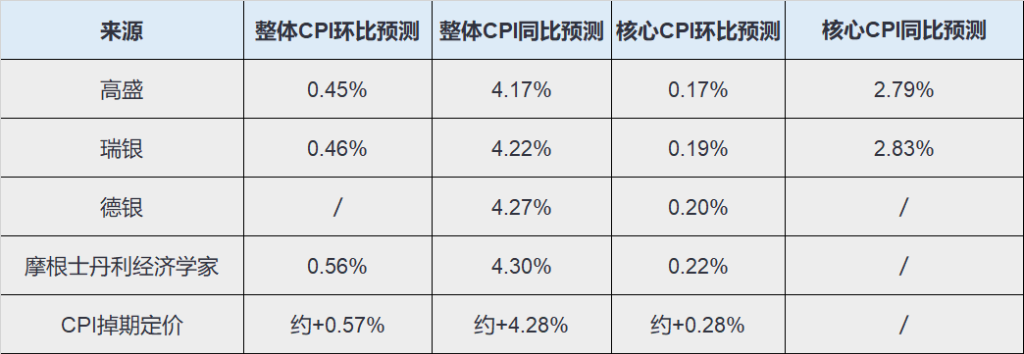

From the forecasts, the four institutions predict May's overall CPI year-on-year to be in the range of 4.17% to 4.3%, all higher than April's 3.81%. However, the month-on-month forecasts for core CPI are generally lower than the market consensus.

The trend of overall inflation and core inflation presents a clear divergence.

The "worrying" part is overall inflation. Goldman Sachs, UBS, Deutsche Bank, and Morgan Stanley all predict year-on-year figures above 4%. Deutsche Bank's estimate of 4.27% and Morgan Stanley's estimate of 4.3% are 46-49 basis points higher than April, and will be the highest since April 2023.

The "joyful" part is core inflation. Excluding food and energy, the month-on-month core CPI may only be 0.17%-0.22%, significantly lower than the mainstream market expectation of 0.27%-0.30%.

Overall inflation may break 4%: Energy is the "culprit"

Energy will be the core driving force for the potential surge in this inflation.

After the outbreak of war in Iran, U.S. retail gasoline prices soared, driving energy commodity prices to rise by about 6%-7% month-on-month in May, while the overall energy category saw a month-on-month increase close to 4%. This effect directly pushed the overall CPI year-on-year from 3.81% in April to 4.17%-4.3% in May.

Deutsche Bank's estimates show that energy inflation year-on-year may approach 24%; in February, this number was only 0.5%.

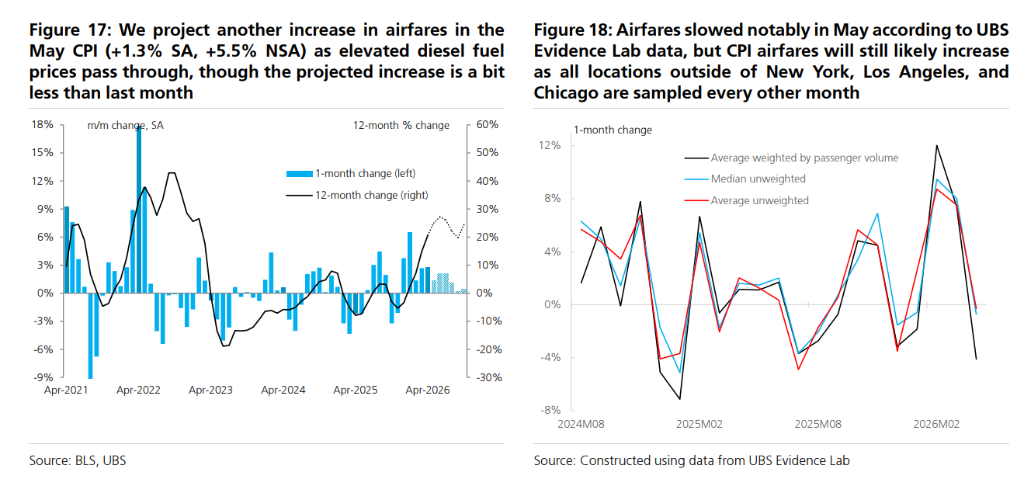

The increase in ticket prices is one of the most direct channels of transmission. The rise in fuel costs directly raises operating costs for airlines, and May's ticket prices are expected to increase by 1.3%-2% month-on-month.

The good news is that gasoline prices have dropped by about 40 cents per gallon since peaking on May 20. UBS expects this will lead to a month-on-month decline in overall CPI of about 0.13% in June, bringing the year-on-year figure back to around 3.81%. In other words, May is likely to be the peak of this round of overall inflation.

Why core inflation will be lower than expected hinges on the cooling of housing

The core CPI excludes food and energy. Precisely because these two hottest components are excluded, the core data for May will appear much milder.

In the U.S. CPI, housing has a very high weight, about 35%.

Goldman Sachs and UBS both predict that the owner’s equivalent rent (OER) and primary residence rent will increase by about 0.22%-0.23% month-on-month in May, continuing the slowdown trend. In April, these two components had increased month-on-month by 0.53% and 0.55%, respectively. Deutsche Bank also listed “the trend of housing inflation remaining moderate” as one of the reasons for the soft core inflation.

Due to the high weight of OER, even a drop from around 0.5% to just above 0.2% will significantly lower the core CPI reading.

Car insurance is also a cooling point.

Goldman Sachs expects car insurance prices to decrease by 0.1% month-on-month in May. Its online data model shows that changes in premiums are forming a downward signal for car insurance CPI. Deutsche Bank also mentioned that car insurance is expected to remain weak again.

The used car market does not exhibit significant upward pressure either. Goldman Sachs expects used car prices to remain flat, with new cars increasing by 0.1%; UBS expects used cars to decline by 0.26% and new cars to decline by 0.1%.

This means that several items that have often disrupted U.S. core inflation in recent years—housing, car insurance, used cars—are not signaling strong inflation this time. In other words, the low core CPI in May is not just a sudden cooling of a specific component.

Core inflation is not cooling across the board: Air tickets, IT products, and some services still face pressure

Low core CPI compared to consensus does not mean that all core items are cooling.

Air tickets are an upward item.

Goldman Sachs expects air ticket prices to rise by 2% in May. UBS expects a rise of 1.34%. The reason is that aviation fuel prices remained high for most of May and may be transmitted to ticket prices.

There is significant divergence in hotel price assessments. Goldman Sachs expects hotels to increase by 0.2%; UBS, based on Smith Travel Research data, has adjusted its accommodation forecast downward, expecting a 0.77% decline in lodging prices. However, UBS also notes that the CPI reflects prices at the time of booking, while STR data is closer to prices at the time of check-in, and this time lag could introduce upward risks, especially likely reflecting demand related to the World Cup.

There are also sticky pressures in goods.

UBS expects core goods prices to increase by 0.08% month-on-month, between March's 0.11% and April's 0.03%. Their assessment is that the impact of tariffs on 12-month core goods inflation may have slightly passed its peak, but the residual transmission will keep monthly core goods prices showing slight positive growth for the remainder of this year.

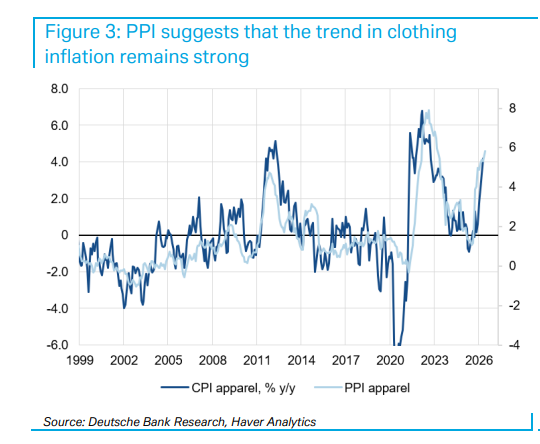

Deutsche Bank also mentioned that import prices indicate that IT product prices still have strong momentum, backed by global storage chip prices being at a high level. At the same time, clothing PPI shows that the trend of clothing inflation remains strong, although import prices are weak, and CPI momentum may slow compared to previous months.

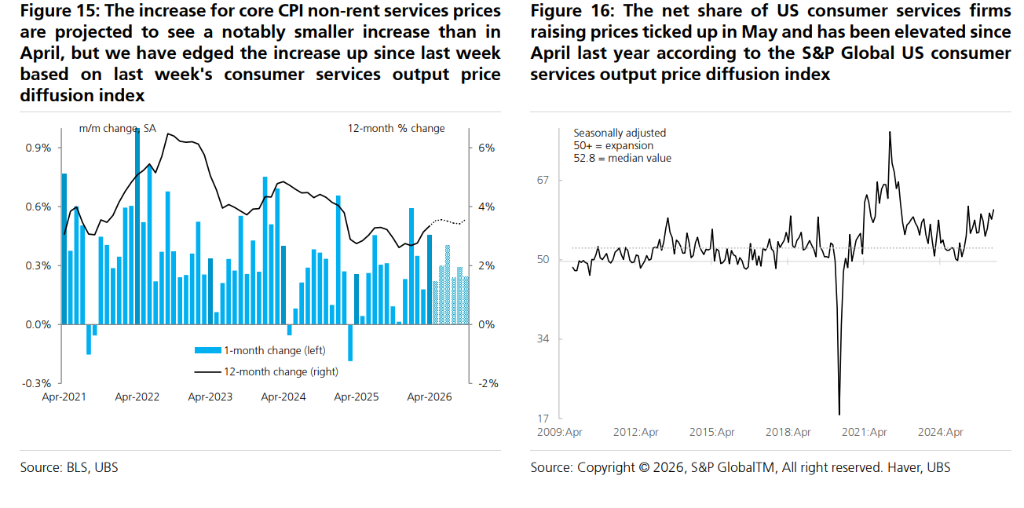

The service items are more complex.

UBS raised its forecast for non-rent core service prices from 0.17% to 0.21%, as the S&P Global U.S. Consumer Services Output Price Diffusion Index shows that the proportion of consumer service companies raising prices in May has increased, reaching the second highest level since 2009, except for the pandemic anomaly period.

What to truly watch tonight is not just an overall inflation above 4%

The surface figure of the May CPI may be high, but it is more critical to break it down.

If the overall CPI is high, mainly due to gasoline and energy, the market may combine the decline in gasoline prices in June to judge sustainability.

If core CPI is significantly lower than expected, the market will continue to look into where inflation is coming from: is it a slowdown in housing trends, or a one-time seasonal drag?

If air tickets, IT products, and non-rent services continue to show upward trends, the meaningfulness of the core cooling will be discounted.

Therefore, this CPI may convey two messages to the market:

On one side, overall inflation breaks 4% again, and may even reach a new high since April 2023.

On the other side, core inflation may only be around 0.2%, clearly below market consensus.

This is the most challenging aspect of tonight's CPI: overall inflation looks hot, core inflation may not be so hot; oil prices push the overall up, while housing and car insurance pull the core down.

Inflation swap pricing: The market bets on a surprise in the rise of the dollar

The rate swap market currently prices May's overall CPI at 4.27%-4.28%, slightly above the median of 4.2% from Bloomberg surveys.

Morgan Stanley strategist Molly Nickolin's analytical framework shows that in the past 12 CPI releases, inflation swap pricing accurately predicted the direction of year-on-year inflation 9 times. Current pricing suggests an implicit upward deviation of about 0.48 standard deviations from economist expectations.

Based on historical backtesting, an upward surprise of 0.48 standard deviations typically corresponds to a rise of about 0.14% in the DXY dollar index within one hour after the announcement. Among all G10 currencies, the Swedish Krona (SEK) performs the weakest on "bullish dollar" CPI announcement days, with the largest average decline.

Looking ahead: Oil prices are the biggest variable on the path of inflation

The trajectory of core CPI in the coming months depends on how long oil prices can be maintained.

The current baseline forecast is that the month-on-month core CPI remains around 0.2%. However, if the situation in the Middle East persists and the decline in oil prices is less than expected, the upward risks will be more pronounced—high oil prices not only directly push up energy prices but will also continue to seep into core inflation through intermediate links like air tickets and transportation.

Deutsche Bank's long-term forecast is even more pessimistic: even if oil prices start to decline in June, overall energy inflation year-on-year will still maintain above 10% until early 2027, and then turn negative. Core service inflation (excluding rent/OER) is also expected to remain above 3% for a long time.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。