Author: danny

Most people who have been to Thailand have visited 7-Eleven. You probably bought something to eat inside—fresh shrimp wontons, fried chicken, sausages, a box of fried rice, eggs, peanuts..... If you take a closer look at the packaging, you will see two letters: CP.

It is Charoen Pokphand Group.

Most tourists will only see it on the packaging once; but Thai people may encounter it dozens of times a day.

Thai people face three things in their lives: life and death, taxes, and Charoen Pokphand Group CP.

And it is far more than that pack of fresh shrimp wontons. The 7-Eleven you entered has its franchise rights in its hands; the phone card you casually bought may be from True, which is controlled by it; the discount wholesale supermarket Makro downstairs belongs to it; the chicken you eat, from feed to broiler to slaughter processing, mostly passed through its hands. In Thailand, you can go a whole day without leaving the coverage of this company—eating its eggs in the morning, buying food at its convenience store at noon, using its network to call in the afternoon, and shopping for groceries at its hypermarket in the evening.

When a company penetrates to this extent, it is no longer just a business in the Thai economy; it itself is a segment of this economy.

And the starting point of all this is a bag of vegetable seeds.

I. A Bag of Vegetable Seeds

The story begins over a hundred years ago.

In the late 19th century Chaozhou and Swatow, land was scarce and population was dense, and Chenghai County by the sea was particularly poor. There was a type of ocean-going sailboat with a red-painted bow that the Chaozhou and Swatow people called the "red-headed boat," which carried those who could not survive to the South Seas from Zhanglin Port. Most of the people on board only brought a few clothes and a little money, and upon arriving in Siam, Malaya, or Singapore, they would first carry their bags at the docks and work at rice mills. The Chaozhou language calls this journey "guo fan."

Xie Yichu came to Bangkok this way. In 1921, he and his younger brother Xie Shaofei rented a small shop on Yaowarat Road in Chinatown, hanging a sign that read "Zhengda Zhuang," selling vegetable seeds shipped from their hometown Shantou.

Why choose the business of "selling seeds"? There were many Chinese in Bangkok who had the same taste for vegetables as in Lingnan and needed Chinese vegetable seeds, but there were none locally in Siam, so they had to rely on boats for transport. More importantly, seeds have a temper: you cannot tell their quality when you buy them; you have to plant them, see the sprouts, and watch the plants grow to know whether that bag of seeds was good or whether it could make a profit. A farmer spends money to buy a pack of seeds, betting on the harvest for the entire season and the livelihood of the family.

If a farmer buys his seeds and plants them, and the seedlings come out evenly and the vegetables grow well, he sells more and earns more, and he will return next season; not only that, he will also bring along others from the same village. In the next season, there will be a new batch of faces. In the following seasons, as others see them earning well, they will come as well.

The two words "Zhengda" became a brand among the fellow townsmen from Chaozhou and local farmers in Thailand, with Xie Yichu's counter displaying seeds, but what was really sold was the phrase "Trust me, there's profit" (Chao Pinyin: sìn uài, ū zěng / gàn).

This phrase was worth far more than the seeds.

II. A Chicken

It was Xie Yichu's youngest son, Xie Guomin, who turned this seed shop into a multinational group.

Xie Yichu named his four sons Xie Zhengmin, Xie Damin, Xie Zhongmin, and Xie Guomin, and when read together, the middle four characters are "Zhengda China"—a Chaozhou person doing business in the South Seas, incorporating his thoughts of his homeland into his sons' names. (By the way, most people first learned about Charoen Pokphand Group from "Zhengda Variety Show"🤣) When Guomin took over, Zhengda had already moved from selling seeds to selling feed.

Xie Guomin went a step further and completely transformed chicken farming.

A broiler went through many stages from hatching to market: broilers, feed, disease prevention, fattening, slaughter, and sales. A farmer working alone might be risking his life at any one of these stages—an overnight outbreak of avian flu could wipe him out, and if chicken prices drop, he could face the same fate. Xie Guomin's solution was to hold both ends: he produced broilers and feed upstream, and handled slaughter, processing, and sales downstream while leaving the most costly and labor-intensive stage of fattening to the farmers. Farmers provided the chicken houses and labor, he supplied the chicks, feed, and technicians, and once the chickens grew large enough, he would buy them back at a pre-determined price.

This transaction provided both sides with what they wanted. Farmers gained certainty—the price of the chicken would be settled by contract, regardless of how it fluctuated; however, the costs of disease and daily management still fell on the farmers. Xie Guomin gained the "leadership voice" of the entire industrial chain: what breeds to raise, how many to raise, what feed to use, and what standards to meet for market—everything was decided by Charoen Pokphand Group. Profiting from the price difference of a single chicken was minor compared to the whole chain being under his control. Moreover, the chain was built using the land, labor, and capital of thousands of farmers, effectively allowing him to expand by leveraging the resources of others, which is faster than accumulating all of it himself.

Suppose there is a farmer named Songcai on the outskirts of Chiang Mai. He wants to raise chickens, but can't afford the broilers, can't acquire the right feed, nor bear the price fluctuations.

At this moment, Charoen Pokphand offers him a contract: CP will provide chicks, feed, vaccines, and technicians; after the chickens grow big enough, CP will buy them all back. Songcai only needs to build the chicken house. He then takes a loan from the bank using the land passed down from his ancestors.

From that day on, he is nominally an independent farmer, but in reality, he has already become part of Charoen Pokphand's industrial chain. Songcai's chicken house can now only raise Charoen Pokphand's breeds, feed its feed, meet its standards for market, and sell the chickens exclusively to Charoen Pokphand; however, if one day an avian flu outbreak occurs, leading to empty shelters, dead chickens, and an inability to repay the bank loan, it falls on Songcai.

Thousands of Songcais built the foundation of this chain for Charoen Pokphand. The company does not need to construct chicken houses, hire workers, or bear the losses caused by avian flu affecting a specific barn—it only needs to manage the two ends, supplying chicks and feed while buying and selling chickens, arranging everything and the risks in between with just a contract. This is the most practical form of "company + farmers" and also the smartest aspect of this business model: expansion is through thousands of Songcais' chicken houses and loans while the risks remain on their chicken houses and loans. This model outsources the most dispersed, hardest to manage, and labor-dependent sections to farmers.

III. A Country

Chickens can be raised, collected, and sold; the remaining task is to apply this logic in various directions.

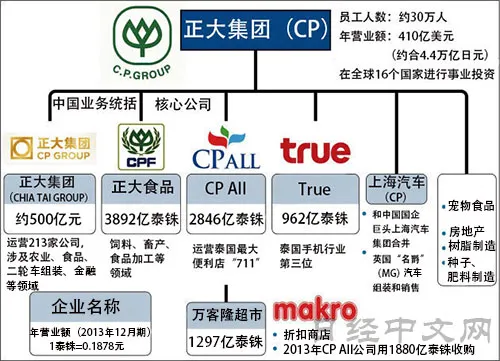

Downstream, the objective is to turn chickens into food on the dining table, leading to the CP shrimp pack and box of CP chicken rice that you see at 7-Eleven. With products needing places to sell, they entered retail: securing the exclusive franchise for 7-Eleven in Thailand, transforming convenience stores into essential infrastructure on every street corner, and acquiring hypermarkets and wholesale supermarkets—the hypermarkets in China were named Yichu Lianhua (now called "BJC Lianhua"), with "Yichu" being Xie Yichu's name, and his son hung his father's name as the sign for the retail flagship. Further out, they entered telecommunications, establishing True; and ventured into finance, becoming a significant foreign investor in China Ping An.

With this step, I believe no one would dispute that CP is a pillar enterprise of Thailand. It operates thousands of 7-Eleven stores in Thailand, making it the largest operator of 7-Eleven outside Japan; it supports tens of thousands of contracted farmers and employs hundreds of thousands of people; a significant part of Thai people's breakfast eggs, chicken, and pork comes from its broilers and feed. From morning till evening, a Thai person eats, buys, uses, and connects online—all repeatedly going back to the same company.

At this scale, it is inextricably linked with Thai politics, regardless of who comes to power. The prices of feed and food it sets directly impact inflation, farmers' income, and the livelihoods of hundreds of thousands of people; its movements are a variable on the macro financial statements that every government must consider. Conversely, many businesses it operates—convenience stores, telecommunications licenses, large infrastructure projects—require national approval to proceed and thus cannot avoid the government. Both sides are interdependent.

Thailand has experienced a series of coups for decades, with civilian and military governments alternating, while CP's existence has not relied on any single side, comfortably engaging with any party in power. The benefits flow down through its franchises and major projects: the 7-Eleven franchise and telecommunications licenses are pathways that require government approval before proceeding; it led the consortium that won the high-speed rail connecting the three major airports; later, True and DTAC merged, capturing the mobile market into two players, which passed the approval process; and acquiring Lotus's hypermarket while facing concerns about monopolies also received approval. Each of these deals was not forged in the market, but negotiated with the government. There is an added layer—this is the very company that obtained China’s first foreign investment license number 0001 in 1979, and for decades has been one of the most important economic conduits between Thailand and China, with Xie Guomin maintaining relationships in Beijing.

Over a hundred years, from a bag of seeds to this point, the path is clear: secure the only entry a buyer can trust → vertically integrate to control output → transfer the heaviest, most capital-intensive elements through contracts to farmer signatories, leveraging others' resources to expand → embed itself into citizens' daily lives, binding itself to the state. Each step amplifies the control of the previous. Completing these four steps, a bag of seeds has surprisingly grown into a power chain holding an entire nation.

The interesting part is here: the same path is currently being retraced step by step by the AI computational power chain.

IV. Chips Are the New Vegetable Seeds

First, look at the entry point. Chips are that bag of "profit and hope" seeds—the FLOPs in the specifications do not equate to the effective computing power gained once you truly build the clusters and run the models; the interconnected efficiency, utilization, stability, and yield after scaling—all require the machines to be set up and go through a cycle before being known, similar to seeds waiting to sprout. The sources are equally narrow: NVIDIA designs them, TSMC builds them, HBM is produced by just three companies, and lithography machines are solely by ASML, with local capabilities being nonexistent, meaning they can only be sourced from these few hands.

However, chips come with an added layer of complexity. Farmers can switch seed suppliers next year if the seeds provided by Charoen Pokphand do not perform well; purchasing an NVIDIA card comes with millions of lines of code, a complete set of operator libraries, and tooling that are all built on CUDA, making it hard to switch. It does not merely monopolize seed quality but also the use of that shovel needed for the field. This dual lock-in is something Charoen Pokphand never faced in the seeds—it sold seeds that were low-margin and replaceable; CUDA is neither of those.

The "company + farmers" approach aligns perfectly. NVIDIA doesn't only supply GPUs but also reference architectures and CUDA, sometimes even investing directly in these companies, mirroring the provision of seeds, materials, technicians, and credit. Neocloud and those sovereign and regional data centers, providing capital and taking on operational maintenance, represent the farmers. The long-term computational power exclusive contracts signed with mega-companies and model laboratories reflect that promise of guaranteed returns, similar to Charoen Pokphand's agreement on collection prices.

When Charoen Pokphand sought rare permissions, they were granted as government franchises and major projects; today's rare permissions include electricity, land, power grid interfaces, and chip quotas, all still held in state hands. Whoever advances to areas rich in electricity and capital earns a first-mover advantage, relying not on market competition but on negotiations with the government. Charoen Pokphand filled the industrial chain across Thailand along the path of permits, while today's computing power players are moving their clusters into different countries through agreements with national AI. At the top of this chain, it has always been connected to the state.

At this point, does it not seem like AI is duplicating the model set by Charoen Pokphand? However, there are two reversed aspects to note.

V. Two Reversed Aspects

First, the depreciable items have flipped their positions.

In the livestock production chain, the cheap and consumable items are the inputs (chicks, seeds), while the valuable and durable assets (land, chicken houses) belong to farmers, whose capital is less likely to depreciate;

while in AI, it is the opposite: the most expensive GPUs are also the ones that deprecate quickest, with a useful life of only two or three years (the exact number is still debated within the industry, but no one thinks they will last decades like a factory). Once a new generation is released, the previous generation instantly loses value. The ones holding this rapidly depreciating asset are the neoclouds that function like farmers.

Even if Xie Guomin’s farmers suffer heavy losses, they still have land; however, if neocloud's cabinets exist for two or three years, the result is a pile of old cards that can only be sold at a loss. Although both hold the position of farmers, what they carry is worlds apart.

Second, the quality of downstream demand is reversed.

Why is CP's collection stable? Because the downstream is driven by essential needs like chicken consumption, with daily requirements leading to repeat purchases, and the output required to feed the entire chain is clearly less than the volume being bought with ready cash by urban residents; behind the contracts stand visible and accessible cash flows.

But AI faces different challenges. It is not that demand does not exist—ChatGPT, Claude, Copilot, and others are already collecting real subscription fees and business income; therefore, it is excessive to say "AI demand has not been proven." The real unanswered question has shifted one level: the income generated for these companies, does it suffice to cover today’s global CAPEX spent on computing power? The demand downstream for CP is clearly greater than the production of this chain; while AI's downstream demand does exist, whether it can support the investments in this chain remains uncertain.

Moreover, there is a concept of "internal circulation" in the computing power industry chain: NVIDIA invests in the companies buying its cards, and these companies use this money along with borrowed funds to build clusters and purchase more cards, with their revenues relying on procurement commitments from laboratories, while funding for laboratory expansions partially comes from upstream suppliers and investors. Money circulates around this cycle, appearing as both an additional line of demand and revenue on the books. This cycle is authentic, inflating the apparent demand. Nonetheless, real cash is also coming in from outside—cost-cutting initiatives from corporates, private deployments, and consumer subscriptions. Currently, it is a race: does the speed of incoming real cash keep up with the GPU depreciation speed of once every two or three years? If real funds don't fill the void quickly and outdated cards become worthless, long-term exclusives become mere empty promises; if sufficiently fast, the chain can become sustainable on its own.

On the same scaffolding, for CP it acts as a stabilizer—risk is distributed to those who can bear it, with real demand underlying it; while for AI, it serves as an amplifier—if external real funds lag behind depreciation, assets, debts, and contracts will shrink together.

VI. Another Possibility

However, it must be said that this reasoning is based on a crucial logical premise: AI demand may not catch up to the already deployed capacity.

Of course, this premise may not hold true, but it offers another perspective on the issue.

Railways, power grids, and optical fibers have all traversed the same segment. Capacity was built ahead of demand, and the first group of people who invested was buried in a bubble, yet it left behind rail tracks, cables, and optical fibers, which were ultimately used as demand gradually caught up. The dark fibers laid in the 1990s were surplus for several years but later found full usage. If AI reasoning ultimately becomes daily consumables like electricity or bandwidth, today’s speculative exclusive contracts could transform into stable cash flows; the quick depreciation of GPUs may not be fatal because constant high-load utilization would amortize depreciation over time. This path exists, and its chances are significant.

Thus, not intending to bet on which path will succeed, it is pertinent to state that regardless of who wins in the demand race, the risks and cash flows shouldered by each position in this chain have always been different, and this distribution was determined on the day the chain was constructed.

VII. Who Stands in Which Position

The power within the industrial chain has never stemmed from scale itself, but rather from how risks and cash flows are distributed.

Many people believe that power within the industrial chain comes from scale. In reality, scale is merely an outcome. What truly determines power is how risks and cash flows are distributed.

Whoever holds the cash flow bears the depreciation; whoever bears the demand fluctuations faces financing pressure.

This is where the power of the industrial chain sprouts.

So, who plays the role of CP?

CP's most valuable position has never been at the seed end. It may have relied on seeds as its starting point, but what truly holds power is the demand entry points like 7-Eleven, Lotus's, and Makro, as well as its ability to integrate the entire chain, without ever shouldering the heaviest assets itself. NVIDIA occupies a different position—one that is locked in by CUDA, nearly monopolistic, and captures significant profits. This position is enviable, one that those who once supplied seeds to Charoen Pokphand could never dream of; however, it is not the same as the position CP occupies today. The real holders of the CP position are the AI platforms and model laboratories that control demand entry, user relationships, and cash flows—they connect with the 7-Eleven end while NVIDIA exists at the seed end.

The remaining role, which controls financing, operational maintenance, and holds the asset that depreciates the fastest, living on contracts, is the farmers, represented by neocloud and sovereign computing power.

Today's power purchasers in computing are far more aggressive than the Thai farmers of yore. To acquire monopolistic seeds, they pledge freshly purchased GPUs—mortgaged to private credit institutions and invested in various structured finance products, leveraging several times over, and then using the funds to buy more cards. They hold the assets that depreciate the fastest in the history of technology while carrying debts that are inflexible. Positioned between monopolistic seed vendors and laboratories that have yet to clarify their accounts, they appear to be the new power players in computing, but in reality, they are using their balance sheets to undergird the entire chain. Therefore, when an endpoint issue arises, they face asset depreciation, debt maturity, and contract nullification all at once, without any buffer.

In essence, neocloud is the Songcai of the AI era. Songcai wagered a chicken house and a bank loan, while neocloud bets on cabinets full of GPUs that lose value in two to three years and several times over in leverage. However, their retreats diverge significantly: even if Songcai's shelter is empty, the land beneath his feet remains; once neocloud's cards become outdated, they are left with e-waste burdened by unmanageable debts. While both undergird the entire chain, the AI version experiences deeper extraction.

The story of Charoen Pokphand reveals that what is truly valuable has little to do with whether they operate in chicken or seeds. The most precious part is that they occupy the most comfortable position on the entire industrial chain: holding demand entry and integration power while leaving the heaviest, most depreciating assets on others' balance sheets; clutching cash flows without involving in the underlying operational risks.

The AI computing chain is also seeking this position today. Ultimately, determining the outcome is not about who possesses the most GPUs but about who can place the fastest depreciating assets on others' balance sheets while securing the most stable demand. Power in the industrial chain has never stemmed from mere scale but from how risks and cash flows are distributed.

By this measure, the conclusion relates little to whether AI wins the demand race. Those who control the entry and demand replicate the power CP has secured—if demand wins, they reap the rewards; if demand loses, they are the ones hurt the least; while those financing depreciating assets through contracts represent the risk CP never allowed its farmers to face—demand wins, they share a portion, demand loses, they’re the first to exit.

Which path leads to success and who gets the profits or takes the burden was already determined on the day the industrial chain was structured.

A hundred years ago, Songcai pledged land and a chicken house. Today, the new Songcai pledges GPUs and leverage. Both believe they are riding the tide of an era.

The difference lies only in:

Songcai is backed by the chicken and eggs that Thai people consume daily.

Whereas today’s Songcai lacks certainty about what demands lie behind them; no one has yet provided an equally definitive answer.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。