The future index rise will rely on profit realization, rather than valuation expansion.

Written by: Li Jia

Source: Wall Street Watch

The non-farm data triggered global market fluctuations, while Citigroup countered the trend by increasing their bullish outlook on U.S. stocks: raising the S&P 500 target, believing the AI bull market has only reached halfway; while also maintaining expectations for rate cuts within the year.

On June 5, the Nasdaq Composite Index fell by 4.18%, marking the largest single-day drop since April 2025; the Philadelphia Semiconductor Index plummeted by 10.26%, with the chip sector losing over a trillion dollars in a single day, the most severe performance since the March 2020 circuit breaker. Following that, in the early trading on Monday, the South Korean KOSPI index opened down more than 8%, triggering a circuit breaker by dropping below 7500 points, leading to a collective decline in the Japanese and South Korean stock markets.

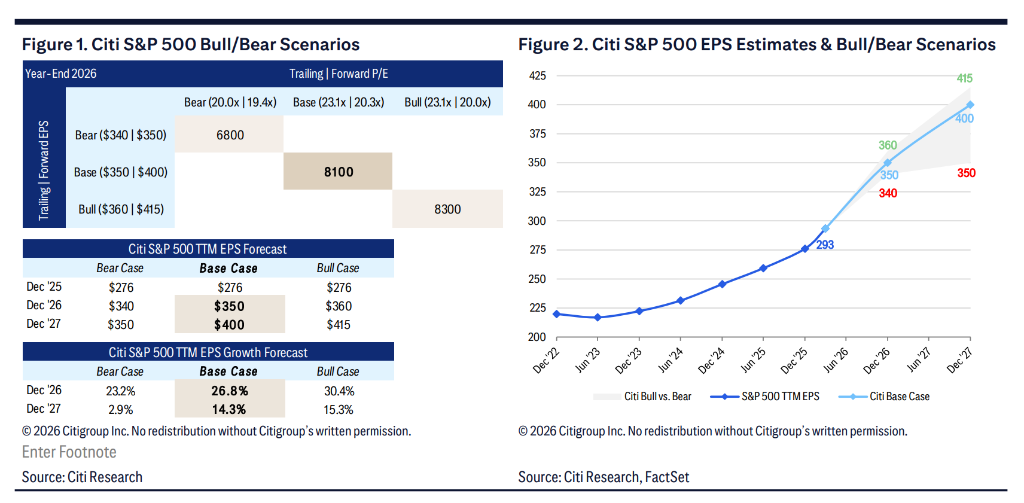

Also on June 5, according to Trading Desk, Citigroup significantly raised the year-end 2026 S&P 500 index target to 8100 points based on the "unprecedented" AI capital expenditure super cycle.

Currently, Wall Street is in a state of extreme fragmentation: at the micro level, AI-driven profit momentum is reshaping the fundamentals of U.S. stocks at an unprecedented pace; at the macro level, inflation and employment data have forced nearly all institutions, except Citigroup, to abandon their rate cut expectations for 2026, and some even began to price in rate hikes.

Citigroup also warned in their report that as the index climbs to 8100 points, the downside skew risk is accumulating. Under the backdrop where the interest rate swap market has fully priced in a rate hike in December, the future trajectory of U.S. stocks will highly depend on whether companies can fulfill their AI profit promises. Investors must be cautious of the valuation pressure brought by tightening liquidity while embracing the AI dividend.

Profit Forecasts Surge: AI is the Real Disruptive Force

Profits are being revised upward at a rare pace, forcing Citigroup to revisit its full-year forecast for U.S. stocks in 2026.

The baseline forecast set by Citigroup for S&P 500 earnings per share entering 2026 was $320, which was already considered high. Their bullish scenario suggested $330, which at the time was seen as "seemingly optimistic." However, the actual performance in the first quarter greatly exceeded expectations.

Actual earnings for the S&P 500 in that quarter were about 13.4% higher than market consensus, a level of outperformance historically only seen in the early stages of recovery after an economic recession—yet there is currently no recession backdrop. Citigroup admitted they had never seen such a situation in the past forty years.

Based on this, Citigroup raised their full-year profit forecast for 2026 to $350. The specific path is: assuming a quarterly outperformance of about +5% over consensus estimates in the second to fourth quarters, corresponding to approximately $81 in the second quarter, about $88 to $93 in the third quarter, and around $90 to $95 in the fourth quarter, this leads to an implied full-year profit of about $355, which was ultimately slightly adjusted down to $350 as a "conservative and reasonable" single point estimate.

For 2027, Citigroup provided an initial forecast of $400, corresponding to an approximate 14.3% profit growth rate (baseline scenario), while also noting the continued uncertainty of the AI fundamental dividend beyond 2027.

This is a Capital Expenditure "Super Cycle," Not a Traditional Cycle

Citigroup explicitly refuses to define the current environment as a "traditional cycle," arguing that a more accurate description is: a one-time capital expenditure super cycle. We are currently in a "middle innings" situation, meaning:

- Profit growth momentum has not yet peaked, but the fastest growth phase may have passed;

- Future price-to-earnings ratios will be under pressure, whether trailing or forward-looking, should expect some contraction;

- The future rise of the index will increasingly depend on profit growth itself rather than valuation expansion.

Citigroup particularly noted that the investment logic of "AI shovels and picks" (the infrastructure suppliers for AI) has been fully recognized by the market. This is precisely the root cause of the asymmetrical expansion of downside risk— the more widely acknowledged a theme is, the quicker the market pricing reversal will be once slowdown signals appear.

Positive Outperformance or Continuation, but the Magnitude Will Narrow

From a short-term catalyst perspective, Citigroup believes that positive earnings surprises above normal levels may still occur in the second to third quarters, primarily from two sources:

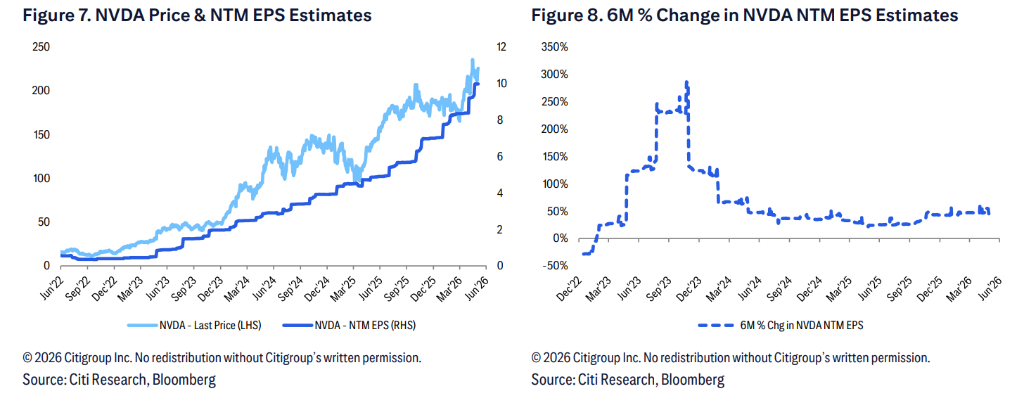

First, the lagging effects of analyst predictions are still ongoing. Taking Nvidia as an example: its fastest upward forecast revisions occurred at the end of 2023, with the NTM EPS adjustment magnitude reaching as high as 285% within six months. Subsequently, analysts gradually "caught up," the magnitude of outperformance narrowed, but the stock price continued to rise. Currently, the six-month change in NTM EPS for the equal-weighted tech sector is still increasing, indicating that the collective adjustment of analysts may take one to two quarters to catch up to reality. This dynamic has spread from Nvidia to memory chips and further to tech hardware and downstream data centers.

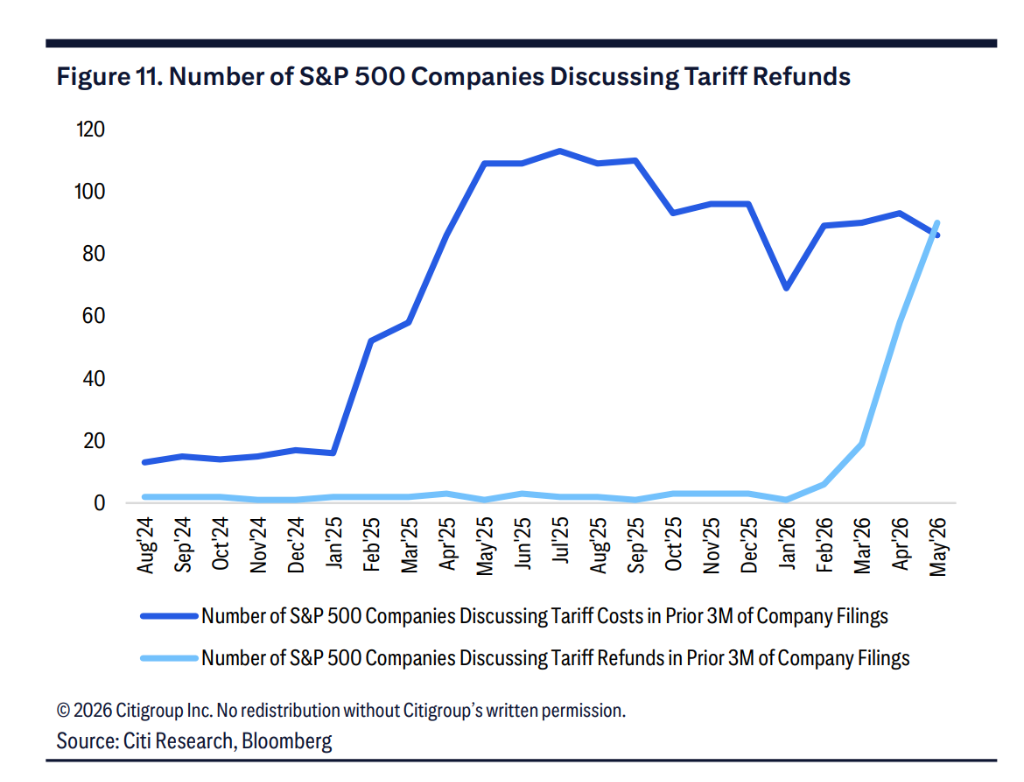

Second, tariff refund effects could bring short-term one-time gains. In the first quarter, some companies already recorded expected refunds as receivables, while another group of companies took a wait-and-see approach. The refunds from the former are already on the books, and the actual refunds for the latter may manifest as earnings surprises in the second quarter; additionally, refunds obtained by suppliers may benefit purchasing companies in the form of lower sales costs (COGS) in the second half of the year.

Valuation Cliff and Asymmetric Risks

Despite Citigroup raising the target price, the report is filled with warnings about the "valuation cliff." Citigroup clearly states that the future driving force for the index will be profit growth, not valuation expansion. In fact, the target price of 8100 points implies a lower historical price-to-earnings ratio than previously.

The market has fully recognized the trading logic of "selling shovels," and it is highly likely that AI-related growth has been priced into 2027. However, the fundamental transmission from 2028 to 2030—that is, the transmission from AI providers to a broader range of AI users, converting into real productivity—remains opaque.

Combined with the large drops last Friday and this Monday, the situation for investors is quite clear: this is a market with extremely low tolerance for error. Growth stocks' forward price-to-earnings ratios should not need significant compression to converge towards the ten-year average, but due to their high weight in index earnings, such valuation would amplify the impact on the S&P 500. As Citigroup warned, as the index rises, profit momentum has increasingly been factored into prices, and investors must prepare defensively for the severe fluctuations brought by emotional fervor and interest rate fluctuations in the coming months.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。