How to jump out of the storm and view the big picture?

Written by: Smac, Partner at Compound VC

Translated by: Saoirse, Foresight News

Editor's note: Current market hotspots emerge one after another, with the AI boom sweeping through everything, while some question whether it will repeat the bubble of the metaverse. In the midst of the noisy market, people are often swept along by the current hotspots and fail to see the long-term trends. To make rational judgments, one must learn to elevate their perspective. In this article, Compound Partner Smac uses meteorological analogies to break down the market logic behind the successive bubbles.

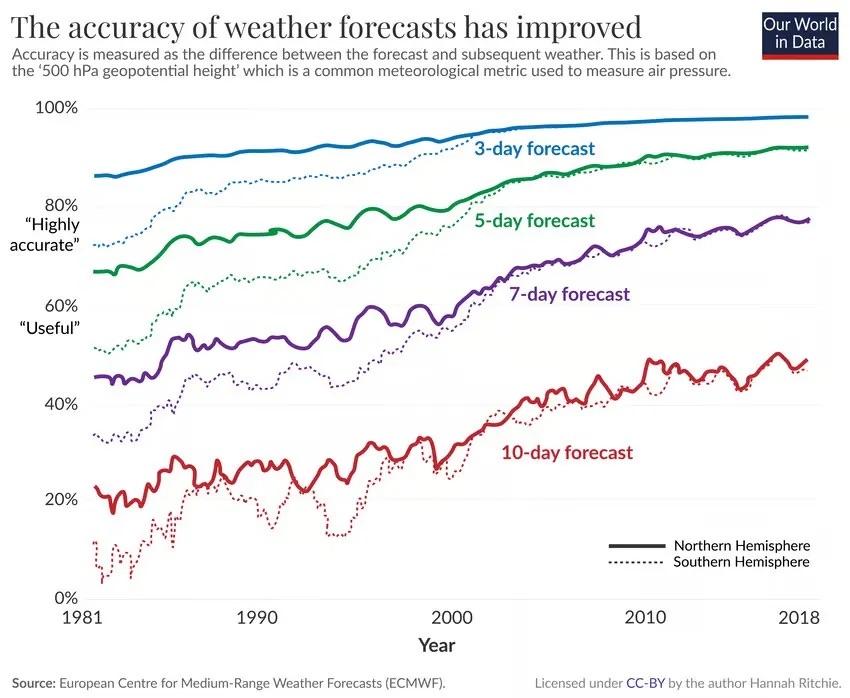

Meteorology is a very interesting field. Over the past fifty years, various weather forecasting tools have continued to iterate, and the accuracy of weather forecasts has improved accordingly. Today's five-day weather forecasts are as accurate as one-day forecasts were thirty years ago.

To most people, weather is a coherent moving system: clouds gathering, raining, stopping, and clearing. Imagine a winter front approaching; the image that comes to mind is likely a vast expanse of gray clouds covering hundreds of miles and dropping heavy snowfall. Meteorologists refer to this type of weather as stratiform clouds. In simple terms, it is like a layered cake, where the areas covered by the cloud experience the same weather changes.

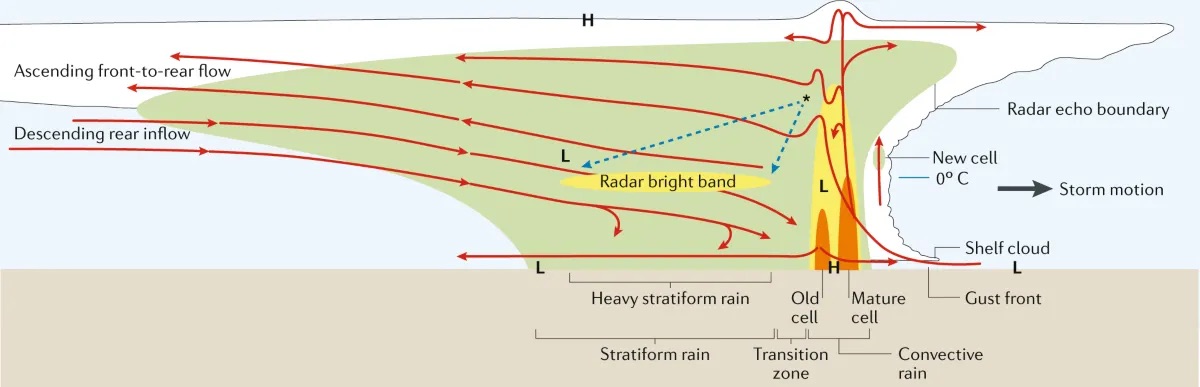

However, weather does not come in only this form. If you have seen summer thunderstorms in flat areas, you will find that their dynamics are entirely different. A single convective cloud will first form: warm, humid air near the surface rises and, upon encountering cooler air at higher altitudes, the water vapor condenses, forming towering cumulonimbus clouds. In just an hour, hail, lightning, and torrential rain ensue, with visibility dropping below a hundred meters.

After the cloud reaches its peak, the energy is completely released and then gradually dissipates. The cold air from the storm sinks, spreading outward at speeds up to 40 miles per hour. When this cold air collides with the surrounding warm, moist air that has yet to form a storm, it acts like a wedge, pushing the warm air upward once again.

As long as there is sufficient instability in the atmosphere, this "cold air wedge" can generate new convective clouds about ten miles away from the original storm.

The new clouds cannot form independently; although energy has already built up in the atmosphere, there is a lack of triggering conditions, and the dying storm just provides this opportunity. Subsequently, the new cloud will repeat the evolution process of the previous storm.

When multiple convective clouds form consecutively, they create a mesoscale convective system. People on the ground will only encounter each storm one by one; each storm seems to represent the entirety of the weather system. On one side, it may be calm, and people are oblivious to the approaching storms; on the other side, it may be raining and then clearing. But from a satellite perspective, one can see a series of independent clouds connected in a line, each in different stages of development, moving forward until they exhaust the warm, moist air along the way.

Supercell storm clouds near sunset in Amistad, New Mexico

This continuous storm system forms under entirely different conditions than single front weather, relying on a specific atmospheric environment:

- The near-surface air is warm and moist, equivalent to the "fuel" for the storm;

- The upper air is dry and cold, prompting the warm air to rise continuously, creating atmospheric instability;

- Wind directions vary at different altitudes, causing storms to rotate and move laterally, known as wind shear.

When all three conditions are met simultaneously, continuous storms will occur in succession.

Having discussed so much meteorological knowledge, let’s return to the main point: the meteorological phenomena described above are nearly identical to the current state of the financial markets.

The past market resembled a stratiform weather system: alternating bull and bear markets, with sector rotations occurring slowly over years. From 1982 to 2000 was a long-term bull market, followed by the internet bubble, then the real estate and credit cycles from 2003 to 2007. These market cycles were lengthy and had clear narratives. Even if investors had a timing discrepancy of several years, as long as they understood the overall trend, they could ultimately profit.

However, today’s market has changed drastically. We are currently in a chain of convective storm-like market trends: one hotspot sector after another emerges like successive storms, and those involved feel that this market is unstoppable and omnipresent.

Funds flow out of fading themes and spur a new round of trends in adjacent areas. The pace of switching market themes has accelerated significantly, including AI infrastructure, GLP-1s (a class of diabetes medication that has gained popularity for its remarkable weight loss effects and has become a hot investment area), stablecoins, quantum technology, nuclear energy, distributed autonomous technology, robotics, and aerospace... Each field will ignite a complete wave of market enthusiasm, drawing in a loyal group of participants, going through a full narrative cycle, and eventually leading to a market downturn. And the "cold air" that spreads after the previous market recedes will ignite the next round of hotspots in new areas.

To deny that the current market has fundamentally changed is essentially self-deception. People love to joke about the phrase "this time it's different," but if one deliberately ignores the permanent changes in the financial market environment, it is either mental laziness or stubbornly living in a fantasy of the old market.

The Market Landscape Is No Longer the Same

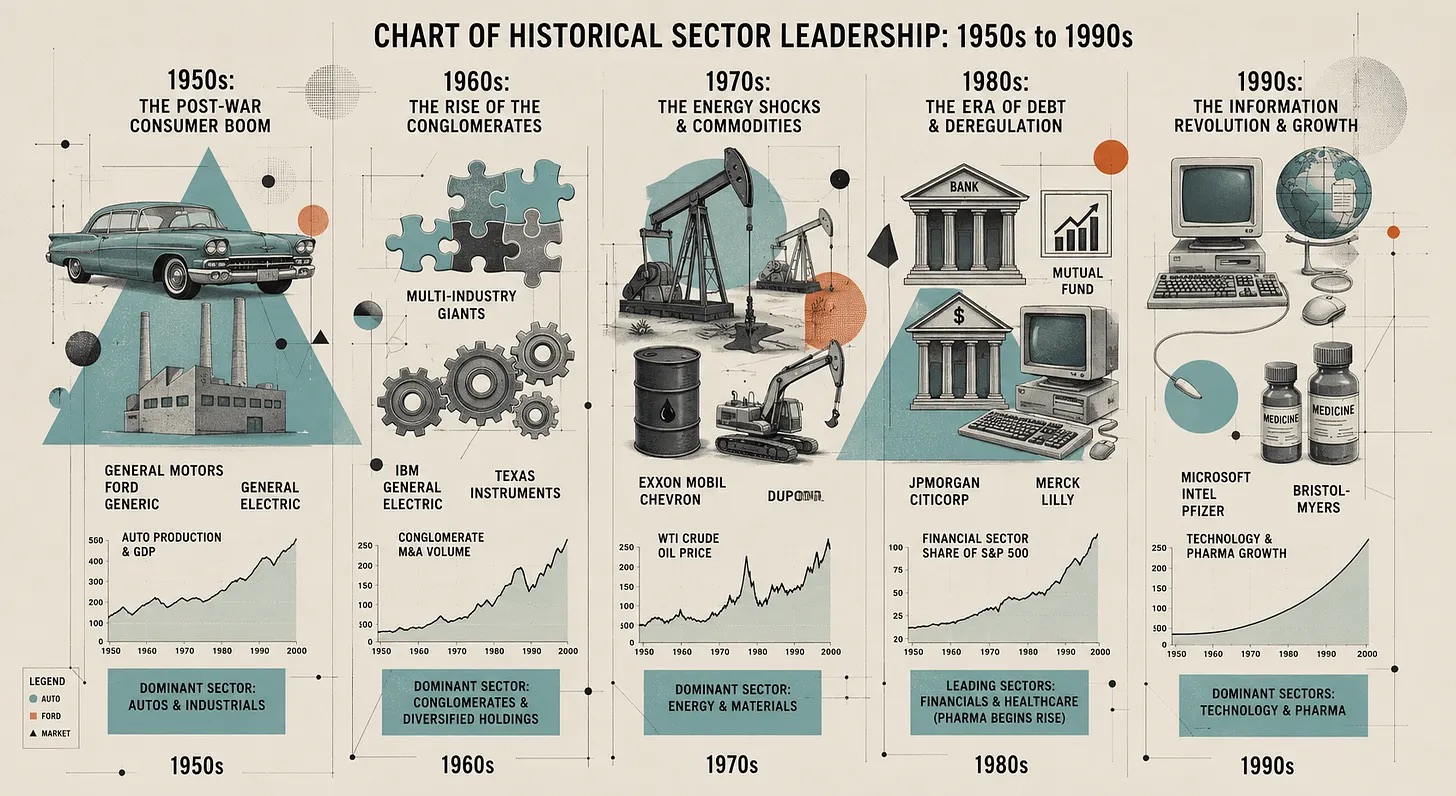

For a long time after World War II, the rhythm of the financial markets resembled a slowly moving weather system. A bull market could last ten, fifteen, or even twenty years, with sector rotations always revolving around long-term overarching trends.

Industry themes and leading sectors approximately in timeline

At that time, sector switches occurred under a unified macro environment, and only at certain significant turning points did the whole market landscape undergo a complete upheaval, such as the collapse of the Bretton Woods system, Volcker's implementation of anti-inflation policies, the internet bubble peak, and the global financial crisis.

The formation of such a market form stemmed from various structural factors: high transaction costs in the past led to very low participation rates among retail investors, who were forced to adopt a long-term holding habit; pension funds were the primary carriers of residents' retirement assets; the S&P 500 index constituents were dominated by manufacturing, energy, banking, and retail companies, with top companies' profit growth rates essentially in sync with overall economic growth, leading to stable and highly predictable trends. Meanwhile, the speed of information dissemination was slow, and after an annual company report was released, most investors would often take weeks to learn the content.

Volatility in the past markets was also relatively balanced. After a bull market, there would be a profound pullback, the market leverage would gradually clear, and the adjustment cycle would be long; rebounds during bear markets were equally gradual. The market would remain in different emotional ranges for extended periods, and significant changes in the overall landscape often occurred on a quarterly or annual basis.

In relation to the meteorological analogy, the past market: fuel was moderate, atmospheric stability was strong, and wind shear was weak, leading to lengthy and stable trends, allowing investors to plan calmly. But now, all environmental conditions have changed, and some conditions have even completely reversed, leading to fundamental changes in market structure.

Where Do These Changes Come From?

Numerous interwoven changes amplify each other, and each reform itself is sufficient to reshape the entire market. In summary, there are eight core transformations:

- Universalization of speculative groups

- Formation of perpetual buying

- Passive investment creates inflexible trading counterparts

- Emergence of multi-strategy funds and high-frequency trading, disappearance of market intermediaries

- Volatility is artificially suppressed

- Complete change in index component structure

- Information delays have disappeared completely

- Transition in fiscal and monetary environment

Universalization of Speculative Groups

The participation subjects of today’s market have visibly changed. In the 1990s, retail trading accounted for only 10% of the total trading volume in the U.S. stock market. Influenced by high commissions, retail investors mostly held stocks long-term, with very few engaging in active speculation.

Robinhood was the first to launch commission-free trading and pioneered the payment for order flow model; in the autumn of 2019, Schwab followed suit by eliminating trading commissions, and subsequently, Fidelity, TD Ameritrade, E*Trade, and others followed suit, completely rewriting industry rules.

The COVID-19 pandemic further accelerated this trend: fiscal subsidies were distributed, people stayed home, and mobile trading apps intentionally gamified trading. From 2020 to 2021, retail trading volume surged to 25%. Many thought this was just a short-term phenomenon, but the high participation rate of retail investors has persisted to this day. On April 29, 2025, market volatility triggered by tariff policies saw retail orders account for a historic peak of 48%. On regular trading days, retail trading volume exceeded twice that of pre-pandemic levels; during significant market fluctuations, this ratio could reach as high as 35%.

Deeper changes can be seen in the types of trades made by retail investors. Individual stock options became the mainstream choice for retail investors, with short-term options witnessing explosive growth. The new participants are primarily young people, with highly concentrated positions, trading closely tied to market themes. More critically, these investors often use special means to leverage (which doesn't show up in conventional margin data), and their trading decisions follow price movements more than company fundamentals, making them easily influenced by the actions of others.

According to meteorological theory: the "warm, moist air" near the ground in today's market is more abundant than ever, with accumulated potential energy reaching historical highs.

Formation of Perpetual Buying

I have previously analyzed this point. In short, the U.S. retirement system has shifted from defined-benefit pensions to defined-contribution plans. Today, individuals must plan their retirement investments themselves. Reflecting this at the market level means that with each pay period, there will be a substantial amount of passive funds continuously buying stocks, unaffected by price movements, creating an automated perpetual buying effect.

The operational logic of traditional pensions is entirely different: fixed-income pensions need to manage duration risk against their liabilities. Managers actively assess market valuations and, if they believe stock prices are too high, will adjust asset allocations by increasing bond holdings. Even if the pace of asset reallocation is slow, it is far more proactive than today's purely passive perpetual buying.

This is crucial: the marginal trading funds in the market now have far more influence over prices than before.

Passive Investment Creates Inflexible Trading Counterparts

The essence of passive index investment is to ignore price levels, buying and selling strictly according to component stock weights. The higher the market capitalization of an individual stock, the larger the amounts bought by passive funds, and conversely, the less it is bought. This mechanism naturally embeds momentum effects into the underlying logic of the market: the stronger the asset's trend, the more passive funds it attracts, and the strong performance of the seven major technology giants in the U.S. stock market largely stems from this.

For years, many articles have analyzed the phenomenon of index weight concentrating on leading companies. Of course, the leading companies themselves possess outstanding profitability and growth capabilities, which makes this concentration not entirely unreasonable. However, the core issue lies in the fact that passive funds do not have a natural "profit-taking switch."

Emergence of Multi-Strategy Funds and High-Frequency Trading, Disappearance of Market Intermediaries

Alongside the formation of passive perpetual buying, the active trading field has also undergone significant changes, with a hallmark being the rise of multi-strategy trading institutions. Institutions like Citadel, Millennium, Point72, Balyasny, and others have gathered hundreds of independent fund managers, with each responsible for specific trading strategies while being subject to strict risk control constraints. These institutions have seen explosive growth in asset management scale, with funds increasingly flowing toward the top, mirroring the trend of concentration among stock index constituents.

Meanwhile, high-frequency trading now accounts for 50% to 60% of trading volume in the U.S. stock market and reaches as high as 75% in the futures market. This combination has created an extremely fragile market environment: trading firms mainly trading against each other's orders have weakened the market's price discovery function. The large trading volumes seen are merely internal fund flows within the market.

Under normal conditions, market bid-ask spreads are extremely narrow, which is certainly good. But once thematic logic breaks down, or the market positions are extremely unbalanced, or if risk control thresholds are simultaneously triggered across multiple institutions, the microstructure of the market can instantly fail. All fund managers’ risk exposures tend to converge; stop-loss rules are generally consistent, and if one institution is forced to reduce its position, the others will collectively follow suit. The market crashes seen in February 2018, August 2019, March 2020, and August 2024 are typical cases. The market structure that gives rise to such patterns is now deeply entrenched and will continue to recur in the future.

Traditional long-short fundamental hedge funds are gradually being squeezed out of the market: these funds rely on in-depth research for stock selection, holding 20 to 40 individual stocks, with investment horizons spanning several quarters. Nowadays, these institutions are either absorbed by major asset management platforms or shift to the primary market, family offices, or single-strategy funds. In my view, understanding the logic of thematic switching and maintaining patience amid short-term fluctuations can still uncover substantial excess return opportunities.

Volatility is Artificially Suppressed

Combining the above four points, the current trends in volatility become clear. Data shows that since 1990, the VIX index has closed below 20 on two-thirds of trading days; the day-to-day correlation of volatility stands at 85%, meaning that the day's volatility levels generally continue the previous day's state.

However, the patterns of market volatility transitions have become extreme and unbalanced: numerous studies indicate that once long-suppressed volatility breaks through a threshold, it will explode violently within a few days; conversely, the process of volatility retreating tends to be sluggish and can last for weeks.

There are multiple structural reasons behind this: the market has given rise to a vast "short-volatility" industry. The proliferation of short-term options has further suppressed day-to-day volatility through the hedging activities of market makers. The market has remained in a low-volatility, calm state for a long time, with risks continually accumulating; when tail risks emerge, all participants will flee collectively.

In simple terms, the distribution of volatility in today's market has become increasingly distorted: long periods of low volatility lead to a more intense risk release.

Complete Change in Index Component Structure

The sixth transformation involves the composition of the stock index itself. In 1980, the S&P 500 index was mainly composed of manufacturing companies, with industrial, materials, energy, financial, and essential consumer goods dominating. The profit growth rates of these companies were roughly synchronous with GDP, resulting in stable growth curves and reasonable valuation multiples reverting around centrist ranges. Even estimating the future five-year profits of companies like Procter & Gamble would not yield vast discrepancies.

However, the situation has changed dramatically now. Information technology, communication services, along with tech-oriented companies in discretionary consumer sectors like Amazon and Tesla, now account for over 40% of the S&P 500 index's weight. The profit models of these companies no longer develop linearly: the marginal distribution costs of software products are almost zero; and the artificial intelligence sector is particularly fraught with uncertainty—whether AI labs will become the most core infrastructure for the next fifty years or a bottomless pit of burn money varies drastically in market perception.

For these companies, it is challenging to estimate short-term profits, and long-term value is full of variables, hence their valuations fluctuate significantly. Company valuations no longer rely solely on financial statements; market narratives have become the core influencing factor. For investors who can anticipate the trajectories of cutting-edge technologies, see through competitive barriers, and position themselves in emerging markets, there lie ample opportunities for excess returns.

The production capacity expansion of traditional manufacturing companies is gradual, and the results of discounted cash flow modeling are relatively stable, making it easier to revert valuations to reasonable intervals. Nowadays, however, the highs and lows of a company’s valuation largely depend on the market's recognition of its developmental story. I do not believe that traditional valuation systems have become ineffective; it is just the objective reality of today’s new enterprises.

Currently, mainstream indices are filled with these long-duration enterprises that rely on narrative drives. The steeper the atmospheric temperature gradient, the more energy is accumulated; similarly, the more of these companies there are, the stronger the underlying potential energy of the market, and once triggering factors appear, market fluctuations will become more intense.

Information Delays Have Disappeared Completely

Everyone can intuitively feel this, but its impact is often underestimated. Throughout much of financial development history, the dissemination of market-related information has been limited by the channels of release. Today, information has almost achieved zero-delay transmission.

Especially for holding information, the speed of transmission far exceeds the past. Investors can see real-time responses from well-known practitioners in the industry to news, and increasingly more people will voluntarily disclose their holdings. This flood of real-time information continually breeds a comparative mentality, with profit screenshots everywhere and instances of "turning a thousand yuan into millions" frequently going viral, further fueling the anxiety of missing out.

Transition in Fiscal and Monetary Environment

This point requires no further elaboration, with key conclusions summarized as follows:

- The U.S. monetary policy has been largely loose for a long time, with real interest rates operating at low levels;

- Quantitative easing continues to expand the Federal Reserve's balance sheet;

- Low discount rates push up all long-duration asset prices;

- Fiscal policies have ramped up, with various subsidies and industrial acts being launched;

- In the context of full employment, fiscal deficits have reached wartime levels;

- The economy shows a K-shaped divergence, with financial markets decoupling from the real economy.

How Do Storms Form?

Combining all these changes, the successive bubbles in the market become an inevitable result.

The evolution of market trends can be divided into several stages, with a clear and understandable logic:

- Market dormancy period: Each track is successively overlooked by the market, with low levels of interest. But even when not favored, there are still those who persist in cultivating within the industry.

- Market activation: Technical breakthroughs, policy adjustments, and unexpectedly good performances manifest, initially captured by seasoned industry researchers.

- Narrative formation: Hot themes create a unified market concept, significantly lowering the barriers for dissemination. Even if some dislike this simplified interpretation, it cannot be denied that a straightforward story allows ordinary investors to quickly understand and participate.

- Cognitive divergence: The market sees significant discrepancies. Apart from steadfast supporters, potential buyers from outside continually dwindle, and the gap in long and short valuations keeps widening.

- Market collapse: Looking back, market turning points are always clear. Today's market participants rush to predict the tops, which has become a norm fostered by online discourse and competitive comparison. After thematic logic begins to crack, funds collectively reduce positions, and the outflowing money starts seeking new investment directions.

- Birth of a new hotspot: The fleeing funds flow into new tracks, acting like the cold air wedge of a storm, reigniting the next round of market activity.

Future Outlook

The impact of this new market structure is very profound. We can predict the overall shape of the market trend, but we cannot precisely locate the specific timing of each round of hotspot explosions.

After the COVID-19 pandemic, many people believed that anomalous market activities were merely short-term abnormalities or products of a low-interest-rate environment. While some of these views hold truth, it is now clear: the shift in the overall market landscape is permanent. The eight transformations mentioned earlier will not reverse:

- Trading commissions will not rise again;

- The scale of passive investment will not shrink;

- Traditional fixed-income pensions will completely exit the mainstream;

- Social media and information dissemination will only accelerate;

- Large multi-strategy trading institutions may have uncertainties, but given their scale and profitability, they will not vanish in the short term;

- Information dissemination delays will not lengthen again.

The current market environment has become a new "normal climate." Expecting to return to the slow-layered markets of the 1980s and 1990s is simply a refusal to face reality.

Another perspective suggests that the duration of successive hotspot markets will continually shorten. This prediction is hard to draw conclusions about, as the market will fall into a cycle of "mutually predicting each other's actions." But one thing is certain: each round of market movements will familiarize participants with the rules, thereby accelerating the rhythm of the next round. Cryptocurrency market traders are also gradually adapting to the ways of traditional financial markets. However, narrative-driven trends have a natural cyclical lower bound and cannot accelerate infinitely.

This rolling bubble market primarily favors two types of investors: the first type is deep industry researchers. They can clarify the technical barriers, regulatory rules, supply chain relationships, and profit logic behind the themes and determine whether market expectations can materialize. AI tools may lead many to believe they belong to this professional group, but this hides significant risks. The second type is trend observers. The vast majority of investors belong to this category, with the core work being to judge the behavioral trends of mainstream professional participants.

At the same time, there are still many rich themes worth speculating on in the future: AI infrastructure and applications, robotics, physical AI, precision medicine, cryptocurrency, materials science, nuclear fusion and advanced nuclear fission, grid energy storage, aerospace, brain-computer interfaces, quantum technology. Even within the same broader track, fluctuations will occur in different subsectors and technological links.

Retail investors currently hold a natural advantage in today's market: freedom of time, operational flexibility, not needing to hold investment decision meetings like institutions, and not facing short-term pressures from quarterly redemptions. The effective strategy of "buying the dip" has also provided a profit foundation for retail investors over the years. Therefore, as long as risk control is well managed, retail investors have significant potential in the new market.

Jumping Out of the Storm, Overlooking the Big Picture

The analysis of the formation of the market structure may lead one to feel that I possess subjective judgments about the current market state. Indeed, I have my own opinions. In primary market investments, we can still choose projects that do not exacerbate negative social effects. But in secondary market investments, the most common mistake is to predict the market based on how one ideally envisions it should be.

This is an emotional weakness ingrained in human nature; historically, Newton also suffered significant losses in investments for this reason.

Emotion is a huge barrier to investment returns. Over the years, it has been common to see various asset management practitioners predicting market downturns in the media, but their statements repeatedly appear with little fulfillment.

The market can no longer revert to its former state. Has this chain of storm-like trends become more distorted than traditional markets? I cannot conclude. But objectively speaking, the many changes that have contributed to the current landscape overall carry positive significance: reduced investment thresholds, the proliferation of automated retirement planning, a wealth of passive investment tools, and more real-time information dissemination, all of which provide the general public with more opportunities to participate in financial markets.

From the ground level, every storm feels all-encompassing, and people's vision is limited by the current market conditions. This is also the true feeling of all participants caught in each round of sector hotspots: the market is like a black hole, absorbing all market liquidity. Only by actively elevating one’s perspective can the complete chain be seen: one hotspot ends, and the next one takes its place, in an endless cycle. Participants in every round of trends are deeply immersed in the enthusiasm or anxiety of the current moment.

The allure of financial markets lies in their perpetual state of change and the fact that price discovery is still led by human beings. Humans are inherently emotional and will repeatedly make past mistakes. This contradiction leads to everything we see today: the seemingly chaotic and restless present unfolds as a series of rolling bubbles when viewed from a higher perspective.

The core intention of this article is to encourage everyone to step out of the immediate storm and observe the market from a higher dimension, clearly seeing the direction of the main market line and trying not to be swept along by the emotions brought on by a single hotspot.

This concept is simple in theory but tests one's self-discipline significantly; knowing is easy, but doing is hard.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。