Written by: David, Tide Research

Tide Reading Guide:

J.P. Morgan's Wealth Management Department released a mid-year outlook report for 2026 on June 1, which informs its high-net-worth clients how to invest in the second half of the year.

Against the backdrop of rising oil prices caused by the blockade of the Strait of Hormuz, a resurgence of inflation, and a shift in the AI narrative from frenzy to skepticism, the overall tone of this report is cautiously optimistic, albeit with a need to change specific investment configurations.

J.P. Morgan believes that the three major global risks (fragmentation, inflation, and AI's disruption) are being overly pessimistically priced by the market, and the current fluctuations are indeed an entry window.

The overall judgment is:

Continue to bet on the AI super cycle and U.S. stocks, hedge against inflation with physical assets and alternative strategies, reduce cash holdings, and pay attention to emerging markets.

If you hold positions in U.S. tech stocks, or are considering whether to increase or decrease your investments in the second half of the year, the framework and data from this report are worth a look; we have edited and interpreted the original report and rearranged the priorities according to investment relevance.

Six Key Conclusions:

① The AI super cycle has not ended, and the market is overly pessimistic.

The five major hyperscalers (Microsoft, Meta, Oracle, Google, Amazon) have a capital expenditure expectation exceeding $650 billion for 2026, which is an increase of $130 billion since the last earnings season. AI-related investments contributed 25 basis points to the U.S. real GDP growth in 2025. Taiwan's GDP growth rate exceeded 7%, the fastest since 2010, driven mainly by semiconductor exports. JPM believes the market is pricing in "AI peaking," but the data does not support this narrative.

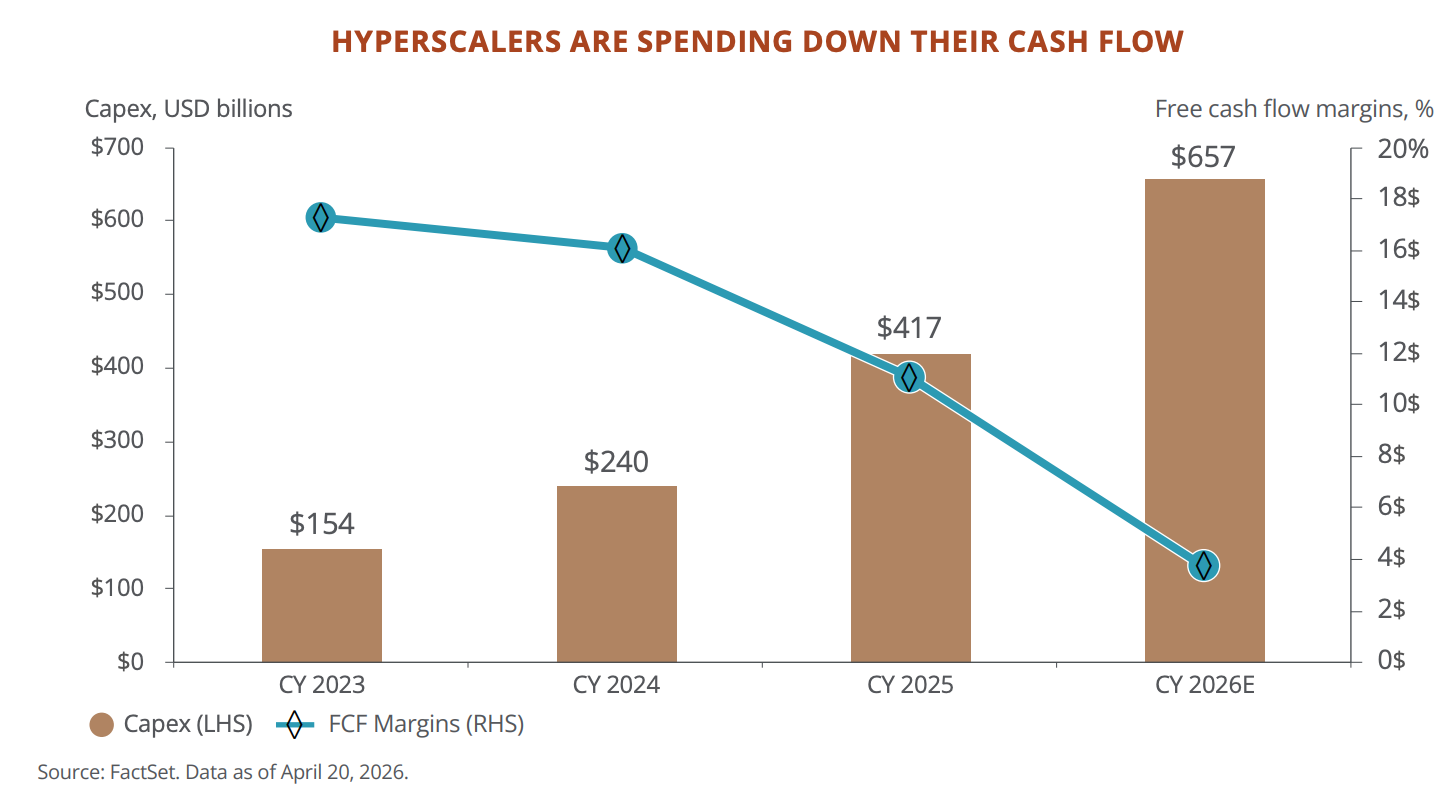

② However, the financial characteristics of hyperscalers are changing.

Free cash flow is expected to fall from $240 billion in 2024 to $73 billion by the end of 2026. Microsoft's forward P/E ratio has dropped from a peak of 35 times during the AI era to 22.5 times. These companies are transitioning from "light asset high return" to "heavy asset high investment," and the market is still digesting this shift.

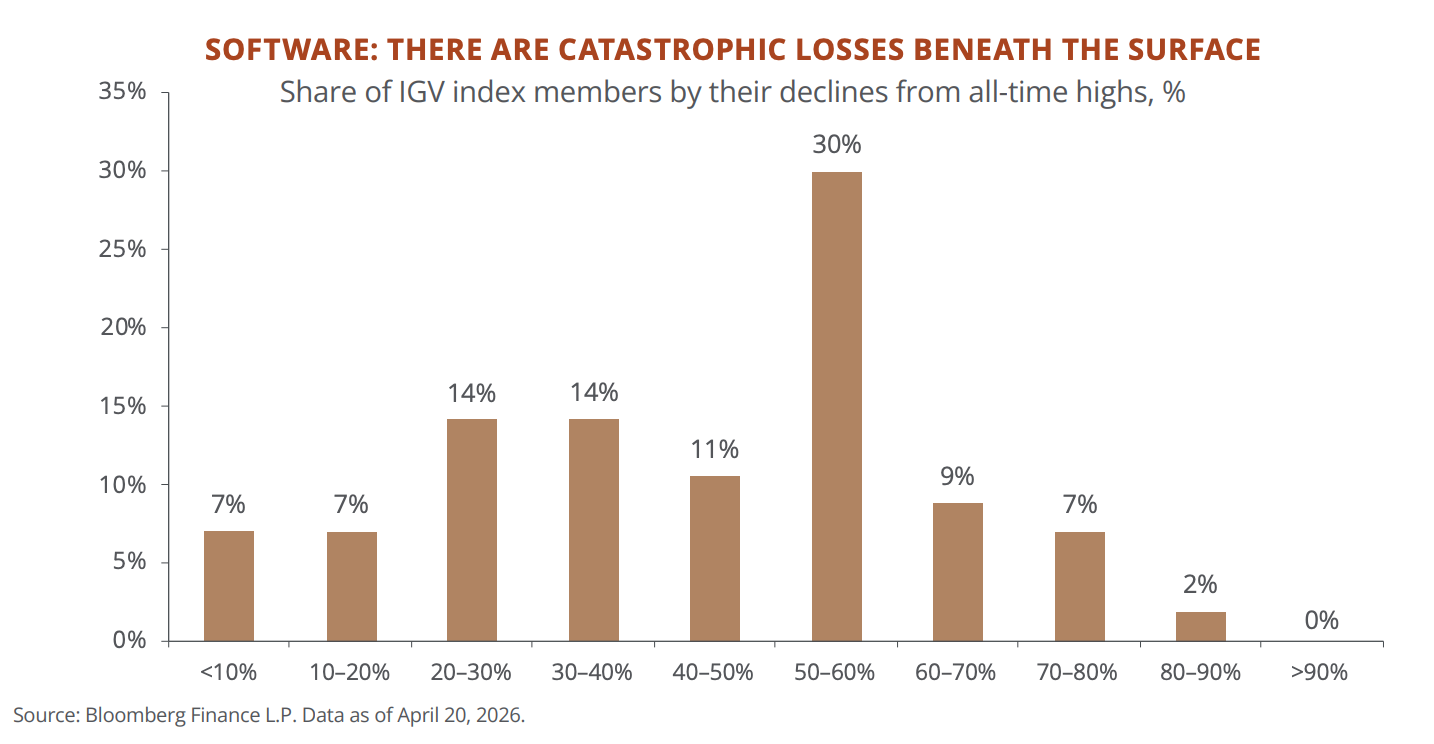

③ SaaS is undergoing a massacre below the surface.

About half of the constituents in the S&P software index (IGV) have fallen over 50% from their historical peaks. The "AI fragile targets" basket tracked by JPM has dropped nearly 20% this year. In the private credit market, 21% of exposure is to software companies, and together with tech and commercial services, it rises to 40%. The impact of AI on subscription-based software business models is already occurring.

④ The bottom of inflation is higher than before the pandemic, and cash is experiencing chronic loss.

The core PCE in the U.S. was already sticky at 3% before the energy shock. Consumer prices have risen 25% cumulatively since the 2020s, while core fixed income has only earned 6%. Nearly 20% of JPM's clients' assets are in cash and short-term bonds. The report's message is very clear: you think you are hedging, but in reality, you are losing money.

⑤ The blockade of the Strait of Hormuz represents the largest oil supply shock since World War II, but JPM believes it should be seen as a buying opportunity during the dip.

Oil prices have nearly doubled, and U.S. stocks experienced a roughly 10% pullback, with the S&P 500's P/E ratio briefly falling below 20 times. JPM's historical data shows that buying after the VIX exceeds 30 yields a 70% to 83% probability of positive returns within six months, with an average return of 12.4%.

⑥ Emerging markets may present opportunities in the second half of the year.

Expected earnings growth for EM companies is 46%, with a P/E of only 11.8 times. Taiwan and South Korea are core nodes in the AI hardware supply chain. Latin America boasts over 40% of global copper and nearly 60% of lithium reserves. Chinese stocks are at the deepest discount to other Asian markets in 20 years, and JP's stance is "cautiously warming."

About AI: The market has priced in "peaking," but JP Morgan believes it's too early

JPM opens by stating that Wall Street's narrative around the AI super cycle is "too pessimistic."

The core data supporting this judgment:

- The five cloud computing giants—Microsoft, Meta, Oracle, Google, Amazon—have a combined capital expenditure expectation exceeding $650 billion for 2026, cloud rental prices for GPUs (the core chips for training AI models) have risen 40% since last October, and supply still cannot keep up with demand. Nvidia's stock price is priced 40% below the average P/E over the past decade, the market is pricing as if "chip sales have peaked," but cloud business revenue is still accelerating.

Simultaneously, the financial characteristics of these five companies are changing. Free cash flow is expected to fall from $240 billion in 2024 to $73 billion by the end of 2026, and Microsoft's P/E ratio has dropped from a peak of 35 times during the AI era to 22.5 times. The light asset model that has attracted investors over the past decade is being rewritten by heavy capital investments. JPM believes that the current focus should be on revenue growth rather than cash flow, but this also means that if demand slows, these investments may become a drag.

Several other judgments regarding AI can be considered as localized risk warnings under the big trend:

Traditional software companies are the first true victims of AI. About half of the constituents in the U.S. software sector index have fallen over 50% from their peak, and the median operating profit margin is only 4%. The logic of this shock is simple: SaaS (subscription software) charges by headcount, and AI reduces headcount. This has already transmitted to the lending market, where about 21% of the borrowings in the direct loan market in the U.S. are to software companies, and the prices of publicly traded tech loan funds have fallen close to the lows of the last cycle. JPM's stress tests indicate that in extreme cases, leverage losses could reach 4%, but do not yet constitute a systemic risk.

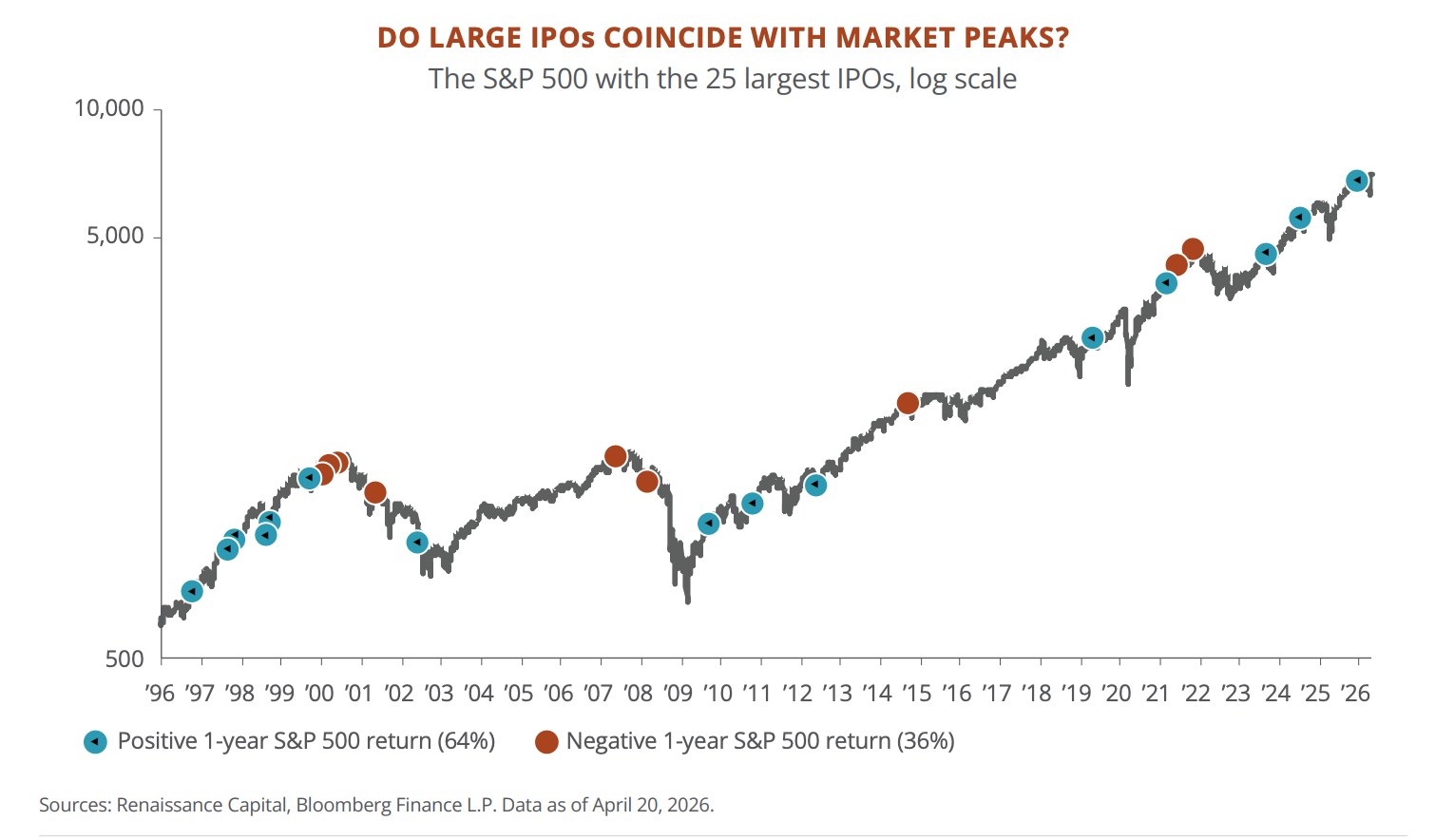

SpaceX, Anthropic, and OpenAI could cluster for IPOs this year, which is historically not a good sign. In the past 25 major IPOs, the median new stock underperformed the market by 30 percentage points in the first year, with 12 out of 18 declining in the first year. The years with extremely large IPOs had a median annual return for the market of only 3%, far below the long-term average of 10%. JPM did not say it would definitely peak, but clearly observes SpaceX's IPO response as a thermometer for the cycle.

About Inflation: Inflation will not return to 2%, your cash and bonds are losing money

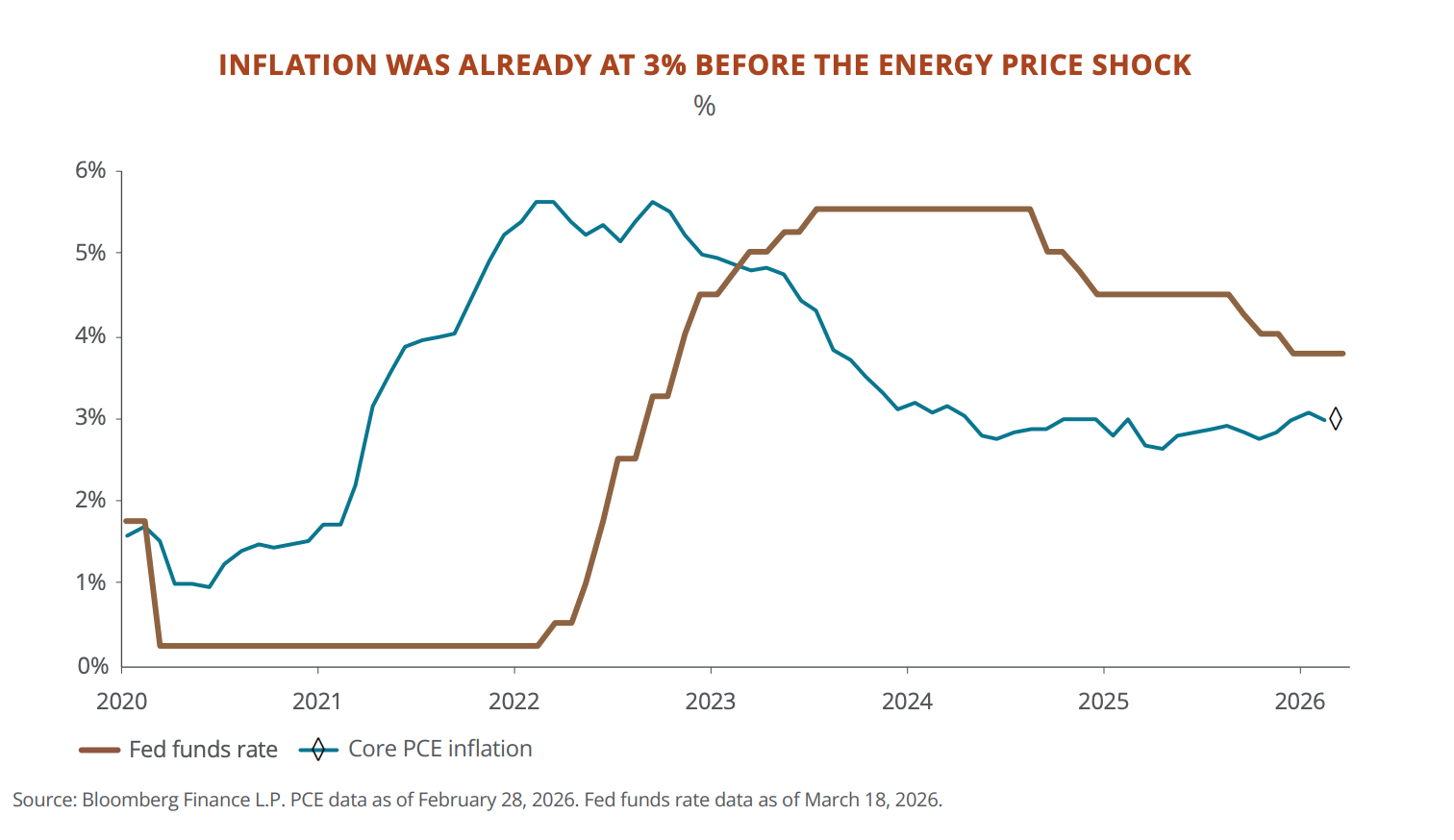

The key point of this inflation section is not that the blockade of the Strait of Hormuz pushed oil prices up, but that before oil prices were pushed up, U.S. inflation had not returned to normal levels.

In January 2026, the core PCE year-on-year was 3.1%, with categories such as dining and personal care seeing particularly solid increases. Then oil prices doubled. The Federal Reserve's model shows that for every $10 increase per barrel in oil prices, inflation rises by about 0.3 percentage points; this time, it rose by $40.

JPM believes that the probability of a full replay of the 1970s is low. The labor market has not seen a wage-price spiral, the voluntary resignation rate is decreasing, housing inflation has fallen from over 5% at the end of 2024 to just above 3%, and China's excess capacity is also pressing down global commodity prices. However, the bottom of inflation is higher than before the pandemic and is likely to hover around 3%.

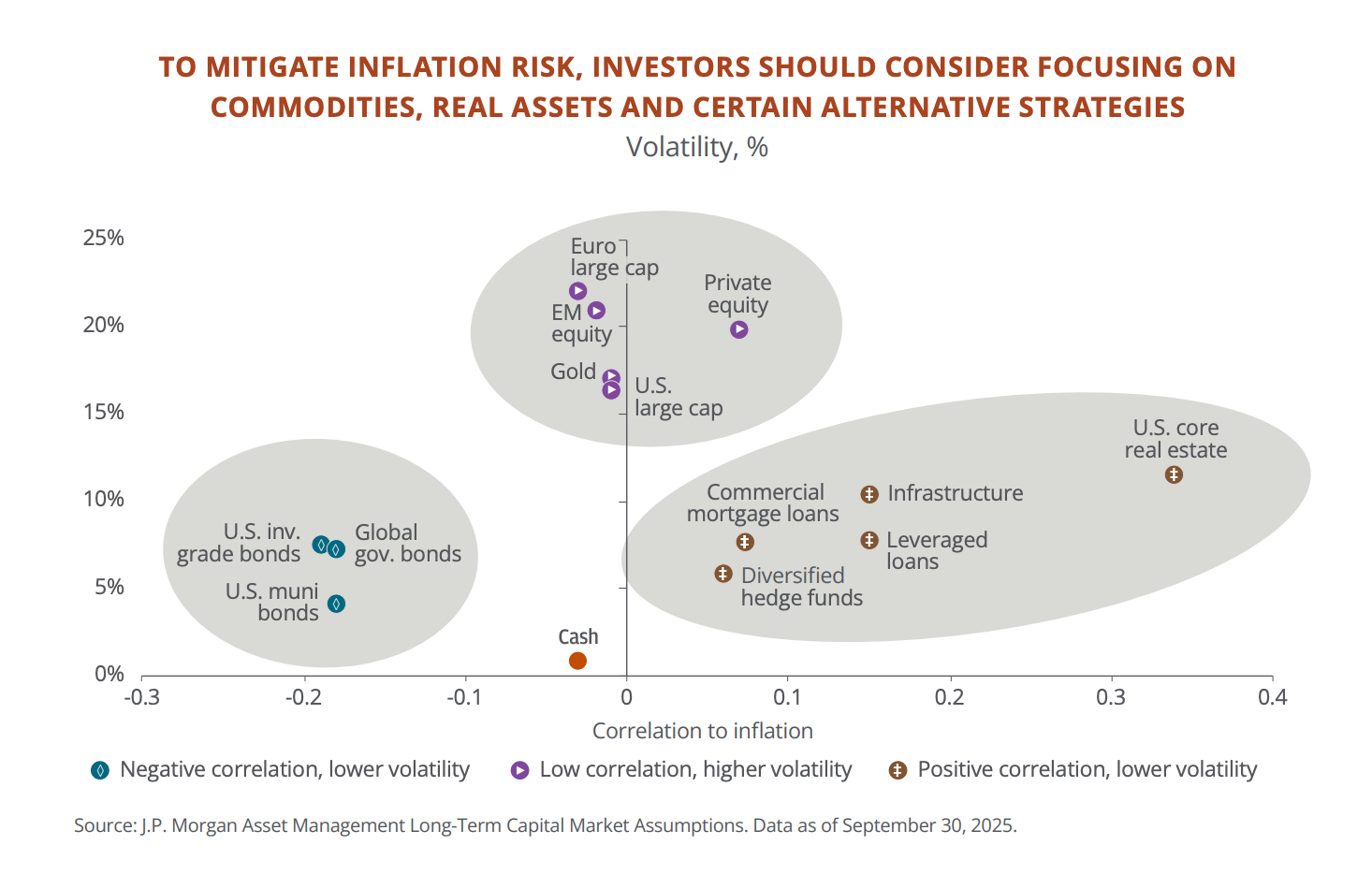

JPM's recommendation for countering is to increase allocations to physical assets.

Since 2020, U.S. prices have risen cumulatively by 25%, while bonds have only earned 6%, and cash even less. You think your money is sitting idle, but it is actually shrinking every year. Among JPM's own clients, nearly 20% of assets are still in cash and short-term bonds.

Therefore, their advice is to move some money into inflation-linked assets:

- Commodities, infrastructure, and real estate, which will rise along with prices, are recommended to account for about 5% of the portfolio.

- Gold is recommended individually at 3% to 6%.

- Additionally, hedge funds, which made 9% in macro strategies when both stocks and bonds fell in 2022. However, JPM also acknowledges that 94% of its private banking clients have never invested in hedge funds, and 86% have never bought infrastructure-related products.

In summary:

Inflation may not become uncontrollable, but it will not return to 2%. If your portfolio still follows the traditional 60-40 stock-bond ratio plus a bunch of cash, JPM believes you are preparing for a world that no longer exists.

About Geopolitics: Chinese stocks may see structural revaluation

This section covers the most diverse content, from Middle Eastern conflicts to U.S.-China competition to European dilemmas. We will only highlight the parts directly related to investment decisions.

1. The blockade of the Strait of Hormuz is the largest market shock in the first half of this year. About 20 million barrels of oil pass through this channel daily, accounting for one-fifth of global oil consumption. After the U.S. and Israel's joint strike on Iran, oil prices nearly doubled within a few days, and European natural gas prices surged nearly 100% in two days. The CEO of Qatar Energy stated that 15% of LNG (liquefied natural gas) production capacity may be offline for up to five years. Qatar also supplies about 30% of the world's helium, which is essential for chip manufacturing, and South Korea has already warned of possible plant shutdowns for chip production.

JPM believes the conflict is moving toward de-escalation, but physical damage to facilities and the energy risk premium will not disappear quickly.

Therefore, their advice to investors is: take advantage of the adjustment to increase holdings in U.S. stocks.

In the first half of the year, U.S. stocks fell about 10%, and the S&P 500's P/E ratio once fell below 20 times. Historically, buying after the VIX (volatility index) exceeds 30 yields a 70% to 83% probability of positive returns within six months, with an average profit of 12.4%.

2. The U.S. and China are building their respective ecosystems, and the market may accelerate its division into two camps. The U.S. is restricting chip exports to China, collaborating with the Netherlands and Japan to restrict semiconductor equipment. China is expanding exports to non-U.S. markets, with its Belt and Road investment reaching a historic high in 2025, investing $53 billion in Brazil in one year, with total trade with Latin America surpassing that with the U.S. JPM's judgment is that future investment returns may increasingly depend on which camp your assets belong to, rather than solely on the company's growth itself.

But fragmentation is also creating opportunities, especially in emerging markets.

JPM listed several directions:

- Latin America possesses over 40% of global copper and nearly 60% of lithium, with rich resources in nickel, rare earths, and agriculture. Foreign direct investment has doubled over the past two decades, and central banks' ability to control inflation is stronger than in developed countries, with politics shifting towards more pragmatic, business-friendly governments.

- Gulf countries in the Middle East are building AI data centers with oil revenues. Saudi Arabia has partnered with Blackstone for a $3 billion data center project, with costs 30% lower than in the U.S.

- East Asia (Taiwan, South Korea) controls key nodes in the AI hardware supply chain. If AI capital expenditure continues to accelerate, the export and pricing power of these economies will continue to strengthen.

- Chinese stocks are at the deepest discount to other Asian markets in 20 years, with 80% of Chinese consumers excited about AI products (compared to 38% in the U.S.), and electricity costs are approximately half of that in the U.S. JPM's stance is "cautiously warming," and if clearer business-friendly signals emerge from policies, Chinese stocks may face structural revaluation.

In contrast, Europe is the market where JPM's attitude is the most conservative. Electricity prices are two to four times that of the U.S., R&D spending is only 2.2% of GDP (3.6% in the U.S., 5.2% in South Korea), and venture capital scale is only one-tenth of that in the U.S.

The energy shock is forcing the European Central Bank to consider raising interest rates again. JPM only recommends investing in defense and infrastructure-related assets in Europe, avoiding cars and consumer goods.

What JPM is betting on, and what it is not betting on

Summarizing the 60-page report in one sentence: Volatility is an entry opportunity, but the way to enter needs to change.

You should bet on:

- AI infrastructure chain (chips, optical modules, electricity), emerging market stocks and bonds, physical assets (commodities, infrastructure, gold), defense-related assets, and Chinese AI concepts (cautiously increasing positions).

You should not bet on:

- Cash, traditional subscription-based software companies, European cars and consumer goods, and investment models that rely purely on a 60-40 stock-bond ratio to withstand the second half of this year.

Original report link:

https://www.jpmorgan.com/content/dam/jpmorgan/documents/wealth-management/mid-year-outlook-2026.pdf

This article is a整理与解读 of J.P. Morgan Wealth Management's mid-year outlook report for 2026 by Tide Research. The judgments and recommendations quoted in the text are JPM's views and do not represent Tide Research's position, nor do they constitute any investment advice.

Sell-side reports are inherently biased towards the positive, and JPM is also the investment banking service provider for several of the companies mentioned. The value of the report lies in its framework and data, not in any single conclusion. Focus on logic, don’t just look at direction.

Investment involves risks; decisions should be made independently.

Data sources: J.P. Morgan Wealth Management Mid-Year Outlook 2026 · Bloomberg · FactSet · U.S. Bureau of Labor Statistics · IEA · METR · Renaissance Capital

Tide Research · 2026 June 4

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。