Written by: Ada, Deep Tide TechFlow

On June 4, Eastern Time, U.S. tech stocks experienced severe volatility triggered by Broadcom's earnings guidance, causing the narrative around AI valuations to crack for the first time.

The results released by Broadcom for FY2Q were not bad in themselves, with revenues of $22.2 billion and EPS of $2.44, both exceeding consensus expectations, and AI semiconductor business growth of 143% year-over-year. However, its guidance for the current quarter failed to match the market's already elevated expectations. CEO Hock Tan revealed during the conference call that major custom chip customer Google might diversify its supply chain and mentioned that the expansion of chip business would drag down gross margins. This combination shattered the core narrative supporting AI trades over the past few months, leading to intense capital rotation on that day.

The Dow Jones Industrial Average surged 1.7% in a single day, driven by traditional sectors, reaching a new historical high; however, the Nasdaq Composite index fell 0.09%, and the Nasdaq 100 dropped 0.5%. Within this "dumbbell" diversified market, AI and semiconductor stocks faced widespread selling pressure: Broadcom -12.59%, Micron -7%, Marvell briefly down 7% pre-market, AMD dropping over 4% pre-market.

Yet amidst this sell-off, AAOI exhibited an independent trend that stood in stark contrast to the sector's sentiment.

Broadcom's guidance breaks expectations, AI sector faces its first valuation pullback

Broadcom became the catalyst for crushing AI trades not due to poor performance but because its guidance failed to align with the market's inflated expectations.

Hock Tan disclosed during the earnings presentation that AI chip sales for the fiscal year (ending October) would reach $56 billion. Although this number is vast, it falls short of market expectations. Coupled with its statement about Google's diversified supply chain, the market's confidence in Broadcom's valuation premium, which was supported by ASIC business over the past year, wavered. Intraday, Broadcom hit a low of $403, wiping approximately $300 billion off its market value for the day, marking the largest single-day drop since January 2025.

The selling pressure quickly spread across the entire AI computing chain. The storage sector also faced a sell-off, with Micron being viewed as the core supplier of AI accelerator HBM, deeply tied to AI capital expenditure sentiment, falling about 7% in a single day. Storage-related stocks such as SanDisk and Western Digital also weakened simultaneously. CrowdStrike, despite having a decent Q2 revenue guide, faced indiscriminate selling in the context of overall cooling in AI trades.

Ray Dalio, founder of Bridgewater, joined the ranks warning about AI valuations that day, clearly distinguishing between “buying AI stocks” and “investing in AI technology,” cautioning that current valuations “may be getting excessive.” This echoes recent warnings from JPMorgan CEO Jamie Dimon and Apollo CEO Marc Rowan regarding AI capital expenditures and high valuations.

The direction of capital rotation also carries significant signals, flowing towards traditional economic stocks represented by the Dow Jones index, rather than an overall withdrawal from risk assets. This indicates that the market is not engaged in systematic risk aversion but is conducting structural de-risking within the AI sector.

AAOI's independent trend: Over 10% increase in a single day, reaching a new short-term high

In this environment, AAOI achieved a single-day increase of 11.76%, climbing from around $171 to $209.64 intraday, closing at $202.89, sharply contrasting with the significant declines of Broadcom, Micron, and others.

AAOI has already experienced multiple rounds of intense volatility. On May 13, the stock reached a historic high of $233.67, fell 9% in a single day on May 29, rebounded 17.18%-18.81% on June 1, and then recorded another 11.76% independent trend on June 4. In just the past 30 days, there have been more than four trading days with a fluctuation of over 10%. This level of volatility has now become a norm in AAOI's current valuation structure, with trading volume on May 11 reaching 214% of the three-month average.

The mid-term catalysts driving AAOI's strength are relatively clear. On May 8 (the day after the company announced Q1 results), Rosenblatt raised AAOI's target price from $140 to $220, reaffirming its "buy" rating and listing it as a "preferred stock." Raymond James simultaneously raised its target price from $72.50 to $160, while B. Riley increased its target price to $129 but maintained a neutral stance. The core logic from Rosenblatt includes the commencement of revenue contribution from the 800G optical modules from Amazon; expected qualification certification with Oracle could open a second revenue line; and a comprehensive increase in demand for products ranging from 100G/400G/800G to the emerging 1.6T.

The supporting data for the company's fundamentals is also specific. AAOI has disclosed that orders for its 800G and 1.6T optical modules total over $324 million; it received $20.9 million in grants from the Texas Semiconductor Innovation Fund in April 2026 to expand its factory in Sugar Land, Texas to 210,000 square feet; and it announced an additional capacity increase of 388,000 square feet in Pearland, aiming for a monthly production capacity of 700,000 units for 800G and 1.6T optical modules by 2027. Management guides that revenue from the optical module business will reach an annualized level of $1.4 billion by Q3 2027.

However, AAOI's fundamentals are not without flaws. Its Q1 2026 results fell short of expectations, with a GAAP net loss of $14.3 million and revenues of $151.1 million, both slightly below market consensus expectations. After adjustments, Q2 guidance for EPS is between -$0.03 and +$0.03, hovering around the breakeven point. B. Riley pointed out while maintaining a neutral rating that AAOI's mass production of 800G will be delayed until the second half of the year, and there is execution risk due to excessive reliance on customer forecasts. Furthermore, AAOI executives collectively sold about $12.6 million in stock in mid-May, and although the remaining holdings are still substantial, the timing of the sale corresponds precisely with the stock's peak prices.

In short, AAOI is currently situated in a tension of "strong narrative, weak Q1 earnings, significant valuation premium,” which is the fundamental reason for its ability to generate high price fluctuations in a single day.

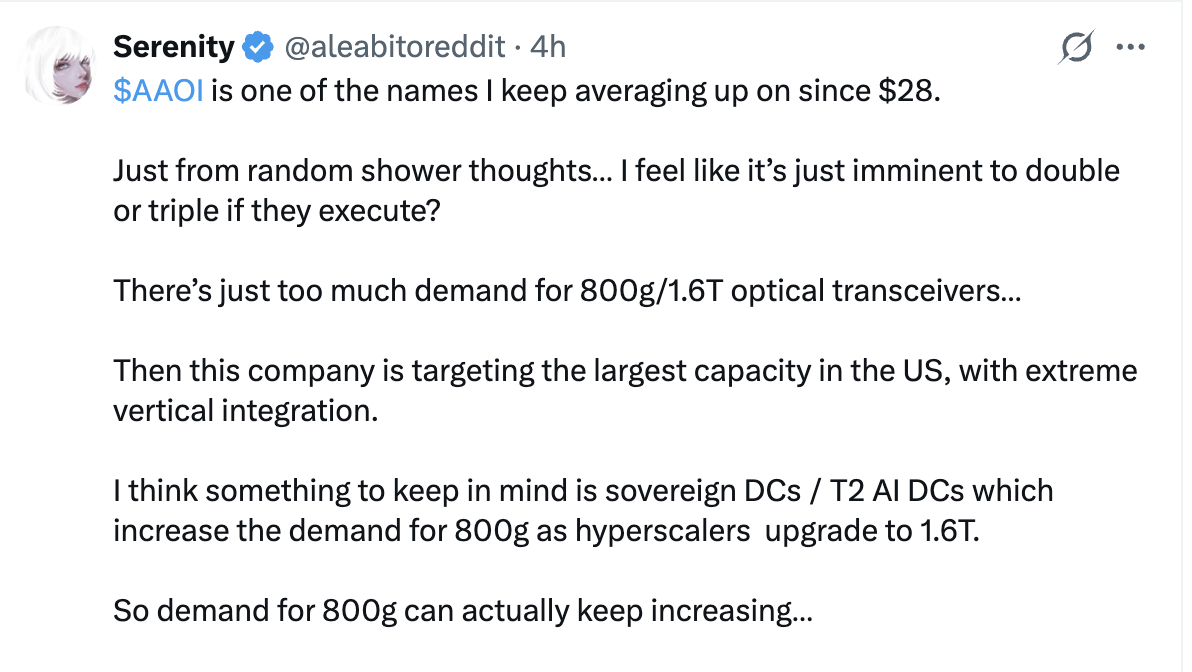

Notably, AAOI has another possible additional driver, which is Serenity, known as the "new stock god" in the Chinese circle, who has posted several times expressing optimism about AAOI, considering it his most favored exposure in the U.S. stock market in optical communications, starting to build a position at $28, potentially becoming "the next SanDisk."

The logic of rising against the trend: "Discriminatory pricing" within the AI sector

AAOI's strength against the trend on June 4 should not be interpreted as a counterexample to concerns about AI valuations, but rather as an early signal of the market beginning to implement "discriminatory pricing" within the AI sector.

One of Serenity's public judgments in April was that the downside resilience of optical communication stocks could exceed that of large-cap tech stocks: “Even if the S&P 500 drops 20% again, optical communication companies could still outperform.” This logic is rooted in supply chain scarcity, with InP substrates, laser light sources, and 800G optical module capacity being in structurally tight conditions in the medium to short term, with pricing power residing on the supply side rather than the demand side.

The sell-off triggered by Broadcom's guidance essentially corrects the "custom ASIC + high customer concentration" narrative rather than a correction of the overall demand for AI infrastructure. From this perspective, optical communication stocks, which are strongly correlated with downstream computing power deployments, do not directly overlap with Broadcom's core issues (customer concentration, Google's potential diversification of supply chain).

However, risks also exist. The current stock price of AAOI corresponds to a valuation that includes extremely high execution expectations, with the market assuming it will achieve an annualized optical module revenue of $1.4 billion by Q3 2027 and maintain high margins. If Q2 and Q3 earnings reports fail to validate the pace of 800G mass production, or if there are any fluctuations in customer concentration risks (such as from Amazon and Microsoft), the valuation structure may experience severe reversals. The actual Q1 earnings report was already weak, and this crack is currently masked by narratives of order growth and capacity expansions, but it has not been completely eliminated.

For observers in the Chinese market, what is worth noting about AAOI's reverse market trend is not the price increase itself, but the directional choice of capital differentiation within the market when the overall AI narrative begins to show its first cracks. The willingness of capital to increase its position in AAOI right at the time of Broadcom's sell-off indicates a judgment that Broadcom's issues do not equate to those of all AI capital expenditures, and optical communications remain recognized as the "physical bottleneck" narrative. Whether this judgment holds true will ultimately depend on the actual earnings reports in the coming quarters.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。