Author: Claude, Deep Tide TechFlow

Deep Tide Commentary: Goldman Sachs presented a forecast to potential investors stating that the revenue of SpaceX's AI business will soar from $3.2 billion in 2025 to $322 billion in 2030, an increase of about 100 times. This forecast comes from the lead underwriter of the SpaceX IPO, while the actual operating loss of this business in 2025 is projected to be as high as $6.4 billion. Morningstar's fair value estimate during the same period is only $780 billion, less than half of the IPO target valuation.

The SpaceX IPO roadshow officially started this week, with Goldman Sachs as the lead underwriter presenting a set of eye-popping numbers to potential investors.

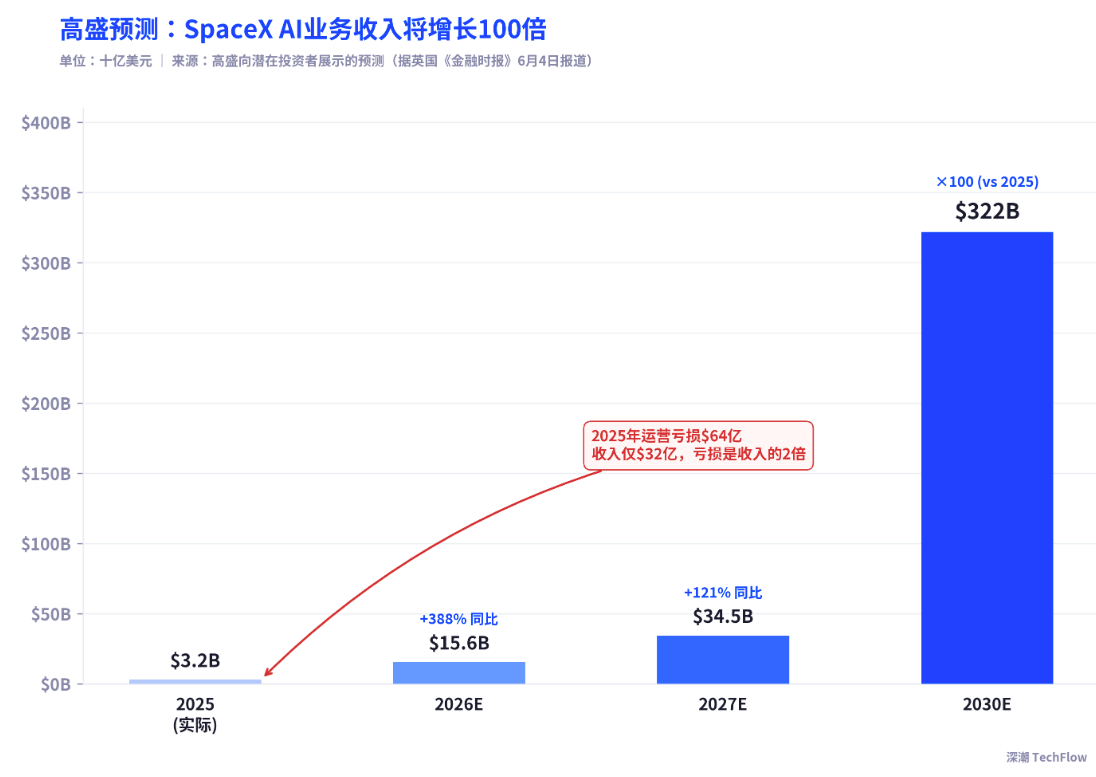

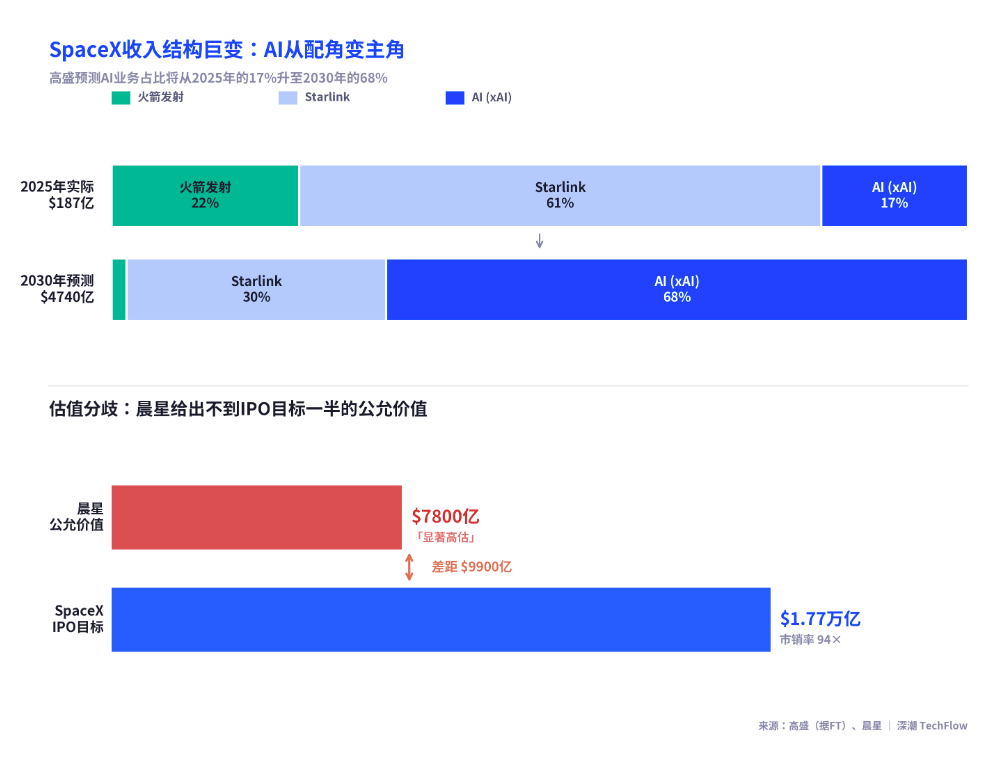

According to a report by the Financial Times on June 4, Goldman Sachs expects SpaceX's AI business (the merged xAI division) revenue to skyrocket from $3.2 billion in 2025 to $322 billion in 2030, with a five-year growth of about 100 times. Goldman also predicts that SpaceX's total revenue will increase from $18.7 billion in 2025 to $474 billion in 2030. These figures appearing in the roadshow materials are not coincidental: SpaceX plans to go public on NASDAQ on June 12, with an issuance price of $135 per share, a target valuation of $1.77 trillion, and a fundraising of $75 billion, which, if successful, would be the largest IPO in history.

But the problem is: Goldman Sachs, who provided this forecast, is also the lead underwriter for this transaction. And xAI is projected to have an operating loss of $6.4 billion in 2025, with revenue of only $3.2 billion, meaning the losses are twice the revenue.

Goldman Sachs' Growth Path: From $3.2 Billion to $322 Billion

According to information cited by Reuters from informed sources, Goldman Sachs expects SpaceX's AI business revenue to grow by 388% year-over-year in 2026 to $15.6 billion, reaching $34.5 billion in 2027, and $322 billion by 2030. If this forecast holds true, AI will account for 68% of SpaceX's total revenue in 2030, far surpassing the estimated $144 billion from Starlink satellite internet services and $8.3 billion from rocket launch services.

This means Goldman Sachs expects investors to trust that an AI division with only $3.2 billion in revenue and losses of $6.4 billion in 2025 will grow in five years to a revenue scale that exceeds that of the vast majority of current global tech giants. By comparison, Meta's total revenue in 2025 is around $164 billion.

The key assumption behind Goldman Sachs' forecast is the large-scale commercialization of AI infrastructure. SpaceX's S-1 prospectus defines the total addressable market (TAM) for the xAI business as $26.5 trillion, close to the U.S. GDP for the fiscal year 2025. The significance of this number lies in the fact that it is not a product-level market definition, but rather includes “all economic activities that can be replaced or enhanced by AI.”

Conflict of Interest in Underwriter Forecasts: Goldman Sachs as Both Referee and Player

Goldman Sachs' role in this transaction is worth examining. According to CNBC, Goldman Sachs is the lead underwriter for the SpaceX IPO, with Morgan Stanley, Bank of America, Citigroup, and JPMorgan also participating in the transaction. As lead underwriter, Goldman Sachs' core responsibility is to help SpaceX complete the issuance under the best possible conditions.

According to FactSet, based on a valuation of $1.77 trillion and revenue of $18.7 billion in 2025, SpaceX’s price-to-sales ratio is about 94 times. In comparison, the overall price-to-sales ratio of the S&P 500 index is about 3.38 times; Tesla's price-to-sales ratio at the end of 2025 is about 16.73 times. In other words, SpaceX's pricing is nearly 6 times that of Tesla and close to 28 times that of the S&P 500.

To justify this pricing, underwriters must prove to investors that revenue will experience explosive growth. A forecast of "a hundredfold increase in five years" conveniently completes this argument cycle.

xAI's Financial Reality: Loss of $6.4 Billion, Cumulative Burn of $20 Billion

According to disclosures in the SpaceX S-1 document, xAI/AI business is expected to generate revenue of $3.2 billion in 2025 but will face an operational loss of $6.4 billion. The primary source of the losses is the large-scale capital expenditures for AI infrastructure: total AI capital expenditure for 2025 is about $12.7 billion, with the first quarter of 2026 alone reaching $7.7 billion, producing an annualized run rate of over $30 billion.

In terms of revenue structure, according to TechCrunch, of the $3.2 billion revenue for xAI in 2025, about $465 million is from “AI solutions and infrastructure revenue” (including $365 million from X and Grok subscription revenue, and $88 million from data licensing revenue), with advertising revenue around $116 million. The bulk of the remaining revenue comes from computing power rentals, with Anthropic being the largest client.

According to the SpaceX S-1 document, Anthropic has signed a deal to pay $1.25 billion per month to rent the Colossus 1 supercomputing cluster located in Memphis (approximately 220,000 Nvidia GPUs, with a power of 300 megawatts), with a contract period until May 2029, totaling over $40 billion. However, the contract includes a 90-day termination notice clause, allowing either party to exit.

On the user data front, as of March 2026, the X platform had about 550 million monthly active users, of which about 117 million use the Grok AI feature, and the number of paid subscription users is about 6.3 million (including about 4.4 million X Premium users and about 1.9 million SuperGrok users). The paid penetration rate is less than 1% of the total X user base.

Morningstar's Cold Water: Fair Value Only $780 Billion, Less Than Half of IPO Target

In the same week that Goldman Sachs was pitching the "AI growth story" to investors, the independent research firm Morningstar provided a markedly different judgment.

According to CNBC's report on June 3, Morningstar analyst Nicolas Owens estimated SpaceX's fair value at $780 billion, less than half of the IPO target valuation of $1.77 trillion. Morningstar's discounted cash flow model values the core business (rocket launches + Starlink) at about $611 billion, while the AI business contributes only about $170 billion (based on scenario analysis weighted by probability).

Owens explicitly stated that he believes Grok is not one of the leading AI labs currently and pointed out that the future of this AI business depends on unproven technologies such as orbital data centers. Morningstar simulated three scenarios for the AI business: in the most optimistic scenario, AI infrastructure could create around $1.3 trillion in value, but there is only a 7% probability; the stagnation scenario has a probability as high as 43%, which would destroy over $81 billion in value.

Morningstar also stated that in the short term, due to the low proportion of circulating shares and the strong line-up of underwriters, the stock price may rise or even soar, but "long-term investors will have the opportunity to buy with a larger margin of safety."

The Core of Market Disagreement: Are You Buying a Rocket Company or an AI Company?

The trillion-dollar valuation gap between Goldman Sachs and Morningstar essentially reflects a clash of two narratives.

Goldman Sachs' narrative is: SpaceX is no longer a rocket company, but an AI infrastructure company with a unique orbital deployment capability. The S-1 document indicates that SpaceX has applied to launch up to 1 million space data center satellites, with deployment as early as 2028. If orbital computing power becomes a reality, SpaceX would possess a physical infrastructure advantage that other AI companies cannot replicate.

Morningstar's narrative is: Starlink and rocket launches are SpaceX's core assets, and they are already reasonably priced. The AI business is currently suffering significant losses, has a very low user payment rate, faces fierce competition from OpenAI and Anthropic, and the feasibility of orbital data centers remains highly uncertain in both scientific and economic terms.

According to Al Jazeera, SpaceX is projected to have a net loss of $4.9 billion in 2025 and a net loss of $4.3 billion in the first quarter of 2026, with cumulative losses reaching $41.3 billion. IG analyst Yip compared SpaceX to Tesla at the time of its IPO: Tesla was also a loss-making company when it went public in 2010, and only after achieving profitability in 2013 did its stock price truly take off. SpaceX's investors are making a similar bet, albeit on a much larger scale.

The SpaceX roadshow has already started on June 4, with pricing expected on June 11 and trading on NASDAQ scheduled for June 12, under the stock code SPCX. Whether Goldman Sachs' projections can be realized will soon be judged in the first round by the market.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。