In the past two years, the access for Chinese users to crypto payment cards has been disappearing one by one.

Written by: ChandlerZ, Foresight News

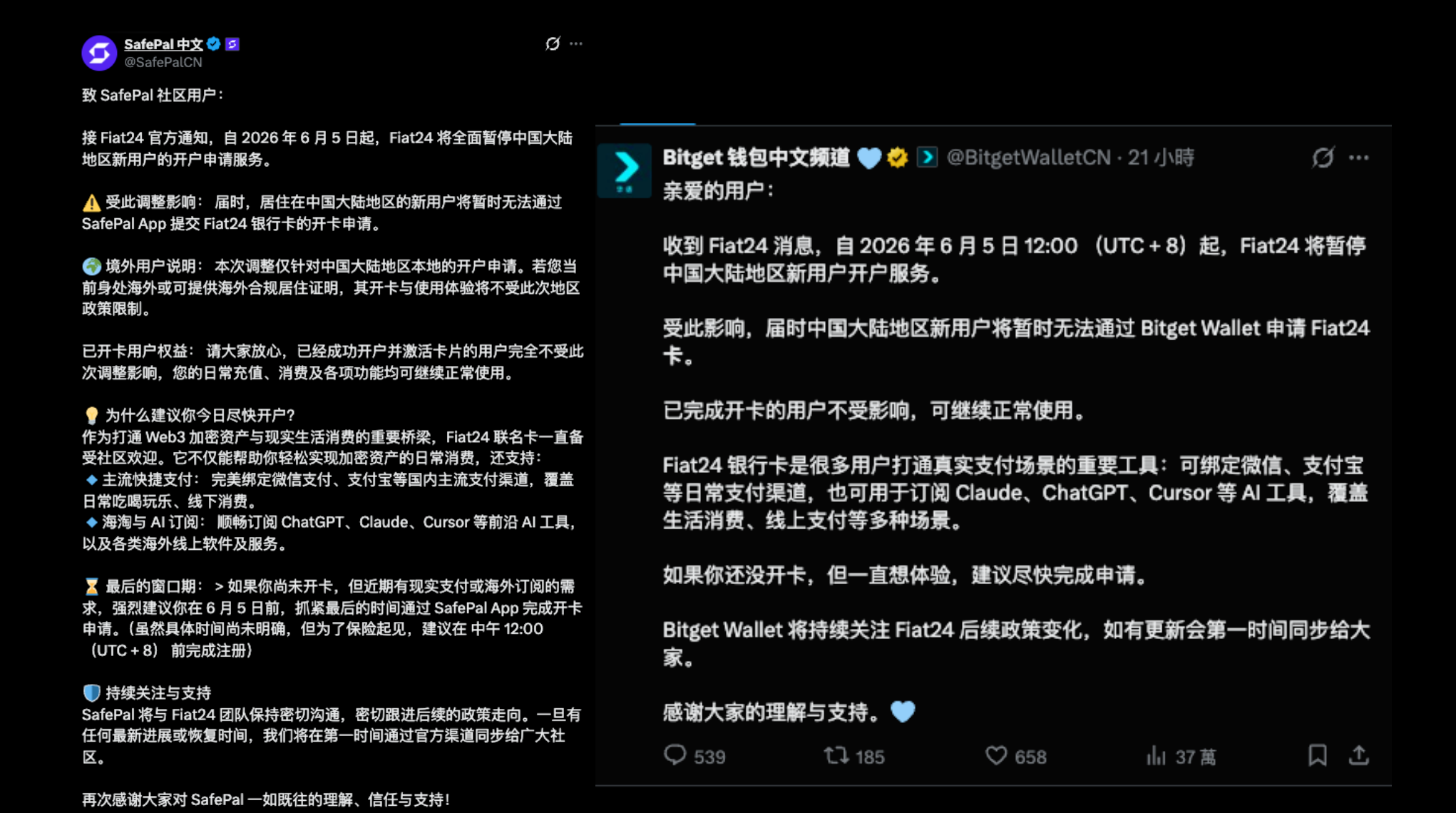

Crypto wallet SafePal and Bitget wallet announced on June 4 that their U Card project received an official notification from Fiat24, stating that it will fully suspend the application for new user accounts in mainland China starting from June 5. As a result of this adjustment, new users residing in mainland China will temporarily be unable to submit applications for Fiat24 bank cards through the SafePal App.

It is reported that this adjustment only applies to mainland China, and if new users are currently overseas or can provide proof of legal residency abroad, the opening and usage experience will not be affected. The rights of existing cardholders will not be impacted by this adjustment, and daily top-ups, consumption, and various functions can continue to be used normally.

Fiat24 is a payment platform operated by Swiss fintech company SR Saphirstein AG, holding a Fintech license issued by FINMA (Swiss Financial Market Supervisory Authority) and built on Arbitrum Layer 2. After completing KYC, users receive a real Swiss bank account (including IBAN), which can be linked to WeChat Pay and Alipay for domestic consumption, can subscribe to overseas services such as ChatGPT and Claude, and can activate cross-border remittance channels like Wise.

The realization of the above rights is one of the important funding channels for any long-term cryptocurrency holder, but this window has also begun to gradually narrow under the current broader context.

Currently, there are at least three mainstream wallets on the market, including SafePal Card, Bitget Wallet Card, and imToken Card, all based on Fiat24, sharing the same Swiss bank account system and KYC process. These three wallets chose to connect with Fiat24 rather than issuing their own cards because Fiat24 provides bank licenses and compliance infrastructure that they cannot obtain on their own. The suspension of registrations in mainland China also means that the new user channels for these three channels are simultaneously closed.

SafePal closed the identity verification channel after January 23, 2026, and in April, community feedback indicated that users who registered U Cards with passports last year generally received simultaneous notifications of CRS declarations from Fiat24. The email mentioned that according to new regulatory requirements CRS/DAC8, all financial platforms need to collect users' tax residency information, and if not provided, accounts may be restricted.

What Should U Card Users Do

Users who already hold Fiat24 cards do not need to panic for the time being, as the SafePal announcement clearly stated that users who have opened and activated their cards are unaffected, and top-ups, consumption, and all functions can be used normally. However, the temporary lack of impact and long-term security are two different matters. From identity cards to passports to tax number notices to the suspension of registrations, Fiat24's restrictions on mainland users have been continuously escalating, and no one can guarantee that the next step will not affect existing users. It is recommended to avoid keeping large amounts of funds in the card for a long time and to prepare a backup card as soon as possible.

The remaining U Cards on the market, whether issued by exchanges or independent projects, are mostly prepaid card models, allowing users to top up crypto assets and convert them into fiat currency for consumption. They can solve daily payment needs such as subscribing to ChatGPT and binding to Alipay but do not have the functionality of a bank account. For users with needs for cross-border receipts, SEPA transfers, Wise deposits, etc., the suspension of Fiat24 means a short-term channel that is difficult to replace has been closed.

In terms of alternative options, the U Card market is concentrating around exchanges, and some exchanges have their own issued payment card products; they do not profit from the card itself, as profits from trading activities are sufficient to cover compliance and operating costs for issuing cards. Some independent card-issuing projects are still operating, but they face the same pressure as OneKey and Infini. Specific card options, KYC methods, rates, and supported regions change rapidly, so it is recommended to directly consult the official channels of each platform for the latest policies and not rely on outdated information in third-party tutorials.

A Business of Feathering One's Nest

The U Card that users see is a simple product: top up USDT, bind WeChat or Alipay, and consume directly. However, behind this card is a long industrial chain. Users top up stablecoins, the card issuer converts the stablecoins into fiat currency through off-ramp service providers, and the payment networks (Visa or Mastercard) complete the clearing with issuing institutions and banks. Each link has independent participants, and each party takes a cut.

In this chain, the real power lies with the upstream players, such as payment networks and banks. Card brands stand at the end of the chain and have the weakest bargaining power. The various brands of U Cards seen by users often rely on the same group of technology providers behind them. These technology providers offer what is known as "issuing cards as a service," which includes a full set of infrastructure for transaction authorization, fund conversion, risk management, etc. The card issuer only needs to call the API to launch a card, making the threshold very low. But this also means that card issuers have almost no control over the foundational operations of their products. If upstream technology providers or banks have issues, downstream card brands can only passively bear the consequences.

On the cost side, the costs are rigid; technical maintenance requires real-time processing of transactions and ensuring security, and customer service must handle various personalized scenarios such as refunds, failed top-ups, and card binding issues. KYC and AML compliance checks are basic thresholds, especially for markets in North America and Europe, where the U.S. FinCEN registration and EU MiCA regulations impose further requirements. USDT is naturally associated with money laundering, score running, and other gray industry scenarios, which increases the risk control pressure significantly compared to ordinary payment products. For projects registered overseas but operating teams within China, the Chinese government's policy stance on cryptocurrencies poses additional legal risks.

Thin margins, rigid costs, and uncontrollable upstream dynamics. These three factors combined determine that the U Card is an extremely fragile business. Any change in one link, whether it is tightening cooperation from upstream banks, regulatory policy adjustments, or a money laundering case involving an issuer, could directly lead to business termination.

Many Have Folded in Two Years

Looking at the timeline, Fiat24 is just the latest.

In September 2024, OneKey announced the cessation of new registrations and recharge functions, officially ceasing operations on January 31, 2025. OneKey Card was one of the earliest crypto payment cards targeting Chinese users, covering the Visa network and supporting Alipay bindings. The official closure did not specify detailed reasons, but the industry speculated that it was related to breaking cooperation with upstream payment service providers.

In June 2025, Infini co-founder Christine announced on X the cessation of consumer-facing U Card operations, stating that the to C card business consumed 99% of the company's time and resources, contributing almost no revenue. All three product lines were suspended, and the company shifted focus to wealth management and B-end services.

In November 2025, crypto payment card provider Dupay announced its shutdown, stating that due to compliance issues and obstacles in fund circulation that cannot be fundamentally resolved, it would officially terminate all services and shut down servers on November 30. The announcement mentioned that a previously frozen large sum of money had not yet been unfrozen, and the funds had been advanced by Dupay.

In June 2026, Fiat24 suspended registrations for new users in mainland China.

A general risk control principle is not to put all demands on one card. The history of the U Card industry over the past two years has already proven that any one of them may suspend or shut down services suddenly. A multi-card approach, spreading risks, and using them temporarily is currently a more realistic strategy.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。