Kalshi has been approved to launch the first compliant perpetual contract in the United States, marking the formal legalization of the $90 trillion perpetual market in the U.S.

Written by: Vaidik Mandloi

Translated by: Saoirse, Foresight News

Perpetual contracts (Perps) surpassed a transaction volume of $90 trillion last year, a figure that exceeds the combined economic output of the top ten countries by global GDP. Currently, perpetual contracts account for three-quarters of the total trading volume in cryptocurrency derivatives, growing at a pace that outstrips nearly all financial products in recent history.

However, until recently, no institution in the United States was legally able to conduct perpetual contract trading, a deadlock that was broken last Friday. On May 29, the U.S. Commodity Futures Trading Commission (CFTC) approved Kalshi for listing the first compliant Bitcoin perpetual contract in the nation; on the same day, it also allowed Coinbase to channel its users' orders for global perpetual and options products through the Dubai Deribit platform.

Following this news, the platform token HYPE of the leading on-chain perpetual platform Hyperliquid surged by 30%. Hyperliquid is currently the largest decentralized perpetual exchange in the world, and the platform does not open to U.S. users. CFTC Chairman Michael Selig, in a column published by CoinDesk, defined perpetual contracts as "an essential risk management and price discovery tool for the global cryptocurrency asset market." Those in the crypto industry witnessing this regulatory change firsthand inevitably feel a profound shock; the subsequent sections will detail the far-reaching implications of this event.

What is a perpetual contract? How did it grow to a $90 trillion scale?

The concept of perpetual contracts was first introduced in 1993 when Nobel laureate Robert Shiller published a paper proposing a futures product with no expiration date: homebuyers could use this type of contract to hedge against the risk of falling home prices without actually disposing of their owned properties.

Source: WSJ

Although the idea had theoretical value, it was limited by the derivative market rules of the time, rendering the conditions for implementation completely immature. At that time, all futures across the industry had fixed delivery dates, with a clearing system and margin risk management built around these expiration dates; agricultural futures were settled monthly, and bond futures were tied to interest payment dates, leaving a lack of underlying infrastructure suitable for perpetual products. This theory remained only in academic literature for decades thereafter.

In May 2016, Arthur Hayes, Ben Delo, and Sam Reed founded BitMEX in Hong Kong, delivering an improved version of Shiller's perpetual concept: launching Bitcoin futures with no expiration date, introducing a funding rate mechanism to anchor the spot price, supporting leverage trading of up to 100 times. Eighteen months after its launch, BitMEX became the leading exchange for global cryptocurrency derivatives.

The operational logic of perpetual contracts

Traditional futures contracts stipulate fixed delivery dates; for example, a Bitcoin futures contract expiring in June 2026 must be settled at market price at expiration, and traders wishing to maintain their positions must roll over to the next cycle's contract; frequent position rolling generates transaction costs and creates exposure gaps.

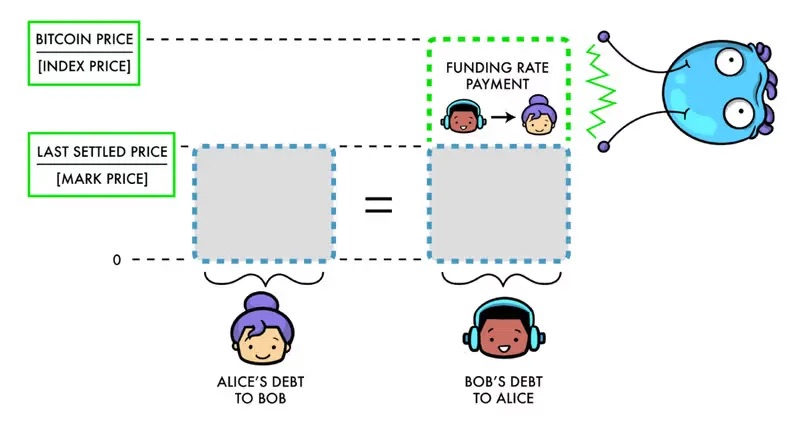

Perpetual contracts eliminate the expiration mechanism entirely, allowing users to hold their positions indefinitely and choose whether to close them in five minutes or five months. However, lacking an expiration-triggered settlement anchoring the spot price, they rely on funding rates to continuously smooth the price differences between contracts and spot prices, ensuring that prices align with the true market conditions of the underlying asset.

Source: Paradigm.xyz

The core advantage of the rapid rise of perpetual exchanges: traditional futures split liquidity across quarterly contract order books for 3/6/9/12 months, while perpetual contracts gather all liquidity into a single order book, significantly improving trading efficiency. Financial markets exhibit a compounding efficiency effect: the more traders there are, the narrower the bid-ask spread, further attracting additional capital into the market.

Offshore perpetual transaction volume soared from $28 trillion in 2023 to over $90 trillion by 2025; decentralized on-chain perpetual trading grew even faster, with transaction volume expected to reach $6.7 trillion in 2025, a staggering year-on-year increase of 346%. On average, the daily transaction volume of perpetual contracts is 10 to 15 times that of the spot market, leading to a complete domination of pricing power by derivatives in cryptocurrency assets: a 5% price fluctuation of Bitcoin in a single day primarily originates from the perpetual market, with leveraged liquidation chain reactions causing either sell-offs or rallies, leading spot prices to follow passively.

Before the recent regulatory approval in the U.S., the perpetual market that controlled the pricing of the entire market had consistently kept its doors closed to domestic institutions.

What changes does the U.S. legalization of perpetual contracts bring to the industry landscape?

Although the U.S. has legalized perpetual contracts, domestic compliant products and the global offshore market's perpetual contracts are not the same category. Even Coinbase requires its Bermuda subsidiary to route user orders to the Dubai Deribit; the offshore market has accumulated vast liquidity over years of regulatory gray areas and cannot quickly flow back to the U.S. market in the short term.

The leverage limit for U.S. compliant perpetual contracts is capped at 10 times, with funds fully protected under the CFTC's customer asset segregation rules; meanwhile, offshore markets generally offer leverage of 50 to 100 times: under 100 times leverage, a $1 principal can control a $100 position, allowing for a double or complete loss of principal with just a 10% price move. For the same 10% market scenario, conventional one-month Bitcoin call options can only yield about 3 times profit due to the upfront premium payment and the time value decay. High leverage is the core selling point for offshore perpetuals, while the risk control for U.S. compliant products is conservative, making their attributes completely different.

This difference is also key to the contrary rise of HYPE after the CFTC approval: the market initially feared that funds would flow from Hyperliquid to U.S. compliant platforms like Kalshi and Coinbase, but that was not the case. Last year, Hyperliquid achieved a revenue of $907 million, all without U.S. users. The two user groups are naturally segregated: speculative retail traders opening 50 times shorts on meme coins at midnight would not go to U.S. platforms to trade 10 times Bitcoin contracts; institutions needing compliant custody and asset segregation would not be entering Hyperliquid in the first place.

The regulatory approval in the U.S. essentially certifies the legality of the perpetual market where Hyperliquid operates, constituting a fundamental positive for the platform.

Currently, U.S. compliant exchanges have only been approved to launch a single Bitcoin perpetual contract, while Hyperliquid has already extended beyond cryptocurrencies: under community governance proposal HIP-3, anyone can launch any category of perpetual contracts on the platform, with several varieties already trading in practice. In February this year, the daily transaction volume of silver perpetual contracts surged to $4 billion, and in April, the periodic transaction volume of crude oil perpetual contracts temporarily surpassed that of Bitcoin.

Jeffrey Sprecher, CEO of Intercontinental Exchange (ICE), the parent company of the New York Stock Exchange, remarked at a Bernstein industry conference just before the CFTC approval: "The Hyperliquid we are talking about has already surpassed Nasdaq in scale." Now, the ICE team is actively engaging with Hyperliquid to learn about its product architecture and to question regulators why traditional exchanges cannot replicate similar products. Wall Street is starting to learn from this decentralized exchange, established only two years ago without windfall investments.

Perpetual contracts are increasingly encroaching on the traditional derivatives market across all categories

The deep impact of this round of regulatory approval is that perpetual contracts are no longer confined to the crypto space; they have begun to penetrate the entire financial market across all categories.

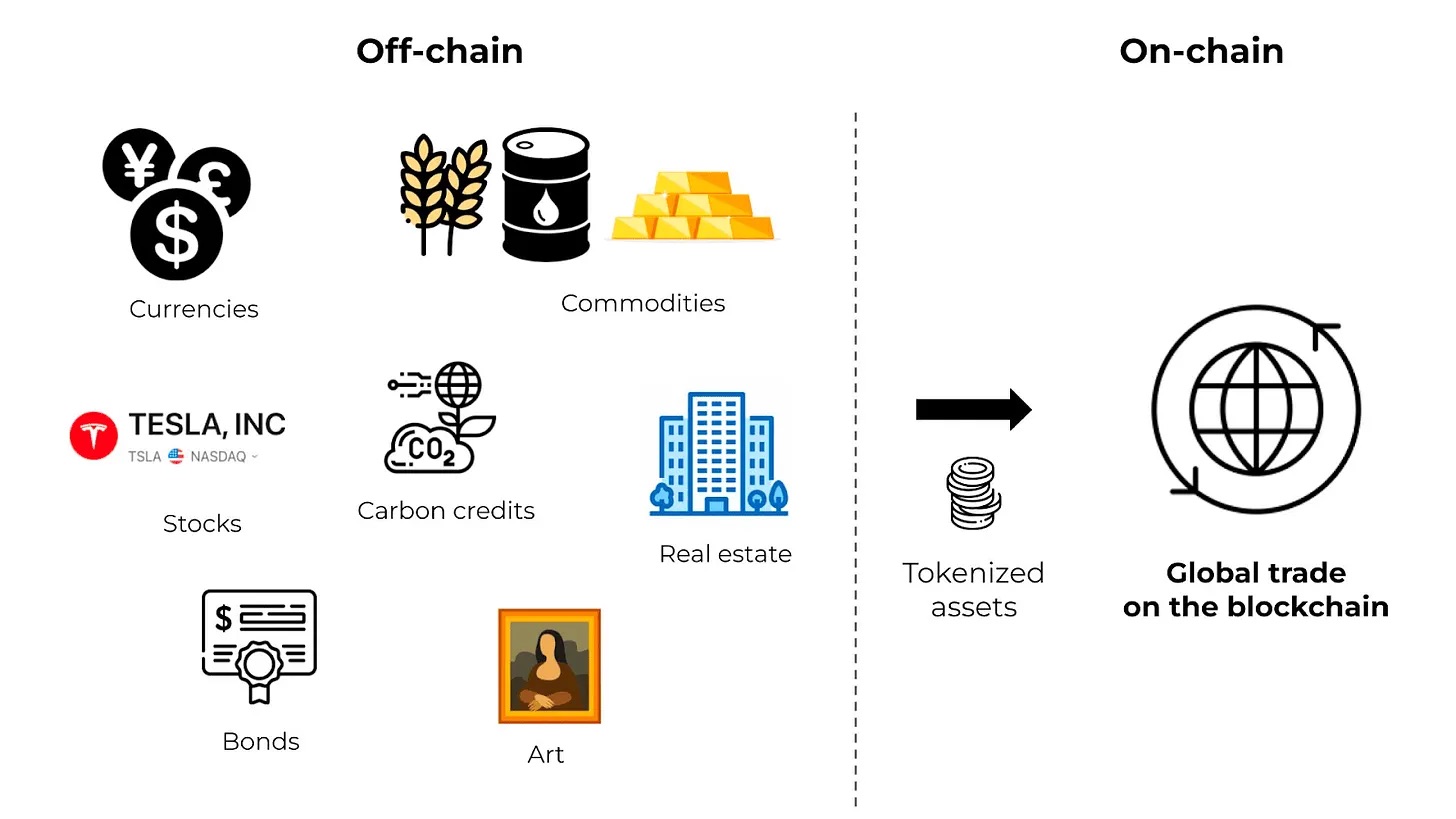

The product evolution path: from native Bitcoin to all kinds of altcoins; then extending to commodities like gold, silver, and crude oil; expanding to individual stocks such as Nvidia and Tesla, as well as equity in unlisted companies like SpaceX and OpenAI; leveraging proposal HIP-4, the platform has already launched predictions market-type perpetual products.

Source: EBC Financial Group

In just two years, perpetual contracts have evolved from a niche innovative tool in the crypto sphere to standardized financial products for all-day, 24-hour trading, with no expiration and eliminating the intermediary clearing links, tied to any global asset. Traditional derivatives originated in an era of manual trading in physical exchanges, where exchanges would close at fixed hours, and contract cycles were designed to fit the then-paper settlement rules.

In today's 24/7 globally interconnected digital market, traditional products that trade in fixed periods naturally have gaps in pricing: oil traders wanting to set positions before weekend geopolitical tensions arise have no corresponding trading tools in traditional compliant venues, while Hyperliquid can open positions at any time. The CFTC's official research summary also explicitly states: relying on digital infrastructure and globalization attributes, derivatives linked to cryptocurrencies are naturally suitable for 7×24 uninterrupted trading.

The upcoming focus of industry competition: whether U.S. compliant traditional exchanges can quickly iterate their products to retain their share. Comparing fee dimensions: traditional centralized exchange futures fees are about 4 basis points, while Hyperliquid charges only 2 basis points; spot fees on traditional platforms are 15 basis points, while Hyperliquid charges as low as 5 basis points. Users can switch platforms in just a few minutes, allowing funds to naturally migrate to lower-cost venues.

In the week following the approval, analysts from Compass brokerage downgraded Coinbase's rating to sell, citing increasing competition in the derivatives market, which continues to squeeze the platform’s pricing power and profit margins. In Q1 2026, Coinbase's perpetual business generated $50 million, but revenue from spot retail traders fell to a new low since Q3 2024: as the perpetual scale expands, it continues to divert high-margin spot business.

The profitability logic of all-category derivatives is being compressed by perpetual contracts: with perpetual contracts, investors do not need to frequently extend quarterly futures contracts due to position rolling (incurring double transaction fees each time); most short-term traders hold positions only for several hours to a few days, and the no-expiration experience of perpetual contracts far exceeds that of traditional contracts requiring periodic rolling.

Short-term options also face replacement pressure: short-term options and perpetual contracts can both realize directional leveraged trading, and the only advantage of options is that losses are capped at the premium. In 2025, the average number of 0DTE single-day options traded on U.S. stocks reached 2.3 million contracts, with the majority of trades speculating on short-term price movements; this demand can be fully absorbed by low-cost perpetual contracts.

This article does not assert that perpetual contracts will completely replace options and traditional futures; the unique loss capping and non-linear returns of options are characteristics that perpetual contracts cannot replicate. However, for the short-term leveraged speculative demand, which holds the highest market share, perpetual contracts, with their low cost and no expiration advantages, provide a superior solution; the $90 trillion transaction volume has already verified the market value of the product.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。