Author: C Labs Crypto Observation

Recently, new regulations on external investment have sparked heated discussions both domestically and internationally, and Bloomberg has reported that despite the Chinese foreign exchange management bureau imposing a $50,000 annual limit on currency exchange per person, an estimated $150 billion still flows out of the country each year through various gray and underground channels.

How This "Wall" Was Built

1994: The Starting Point of the Wall

The foundation of China's current foreign exchange control system is the dual-track framework established in 1994 of "convertibility of current accounts, strict control on capital accounts."

In simple terms: money for goods trade can go out, but personal and capital money must be strictly controlled.

In 2007, the foreign exchange bureau officially set the annual currency exchange limit for individuals at $50,000 per person, a figure that has remained unchanged to this day.

However, for a long time, this regulation was effectively a void and not enforced.

2015: The First True Stress Test

In August 2015, after the yuan's devaluation, a panic currency exchange wave was triggered. In the second half of that year to 2016, China's foreign exchange reserves plummeted from nearly $4 trillion to below $3 trillion, with a maximum outflow of nearly $100 billion in a single month.

The foreign exchange bureau's response was to quickly tighten controls:

Individuals were required to fill out detailed declaration forms when purchasing foreign exchange, clearly promising not to use the funds for overseas property purchase, investment in securities, and life insurance;

Banks were required to conduct "substantive" reviews of large currency purchases and could not release funds solely based on declarations;

Organized crackdowns on "ant migratory" behaviors began.

2017: Channels for Hong Kong Insurance and Overseas Real Estate Blocked One by One

Another popular channel for capital outflow—using UnionPay cards to pay large insurance premiums in Hong Kong—was directly cut off in 2017: UnionPay explicitly prohibited domestic cards from being used for premium payments for Hong Kong savings and investment insurance.

During the same period, regulatory authorities began special rectifications regarding "illegal outflow of foreign exchange funds for overseas property purchases."

2024-2026: Comprehensive Upgrade of Digital Blockades

The core of this round of intensification is the substantial upgrade of algorithms and data infrastructure.

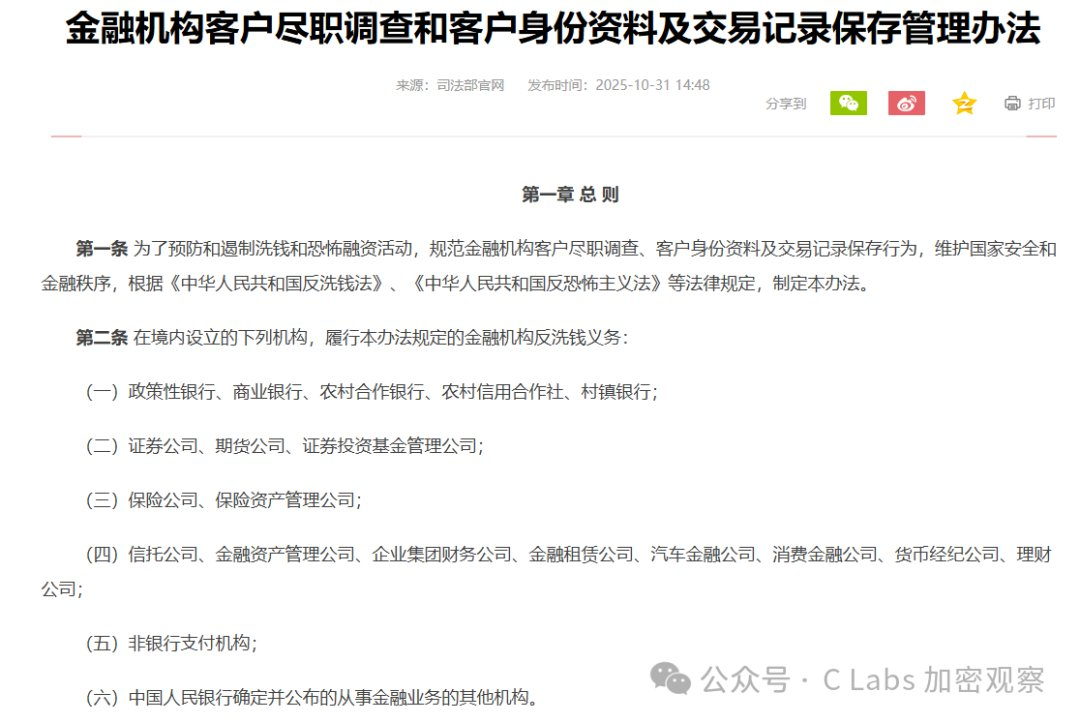

Starting January 1, 2026, the "Administrative Measures for Financial Institutions' Customer Due Diligence and Customer Identity Data and Transaction Record Keeping" will officially take effect. The key change is that for cross-border remittances exceeding RMB 5,000 or the equivalent of $1,000 in foreign currency, banks must verify the accuracy of the remitter's identity information.

This threshold appears low—but in fact, it is intentionally set very low.

The regulatory authorities' goal is clear: not to stop genuine small-scale cross-border needs, but to ensure that every fund leaves a traceable digital footprint, sharply increasing the "cost" of large-scale dispersed transfers.

Meanwhile, China has officially incorporated the Common Reporting Standard (CRS) into its domestic enforcement framework in 2024. This means that over 100 contracting countries will regularly automatically report the balances and income of Chinese residents' foreign accounts to Chinese tax authorities. Accounts hidden in Singapore, Canada, and the UK are, in theory, already "transparent" to Chinese tax authorities.

In May 2026, the China Securities Regulatory Commission specifically named Futu Securities, Tiger Brokers, and Changqiao Securities, identifying them as unlicensed cross-border operations and demanding rectification—this is the latest link in the regulatory chain.

How Money Leaves: Bloomberg Outlines Five Major Paths

The wall continues to rise, but the flow of money has never stopped. The core value of Bloomberg's report lies in its systematic dismantling of this "anti-wall" grassroots engineering.

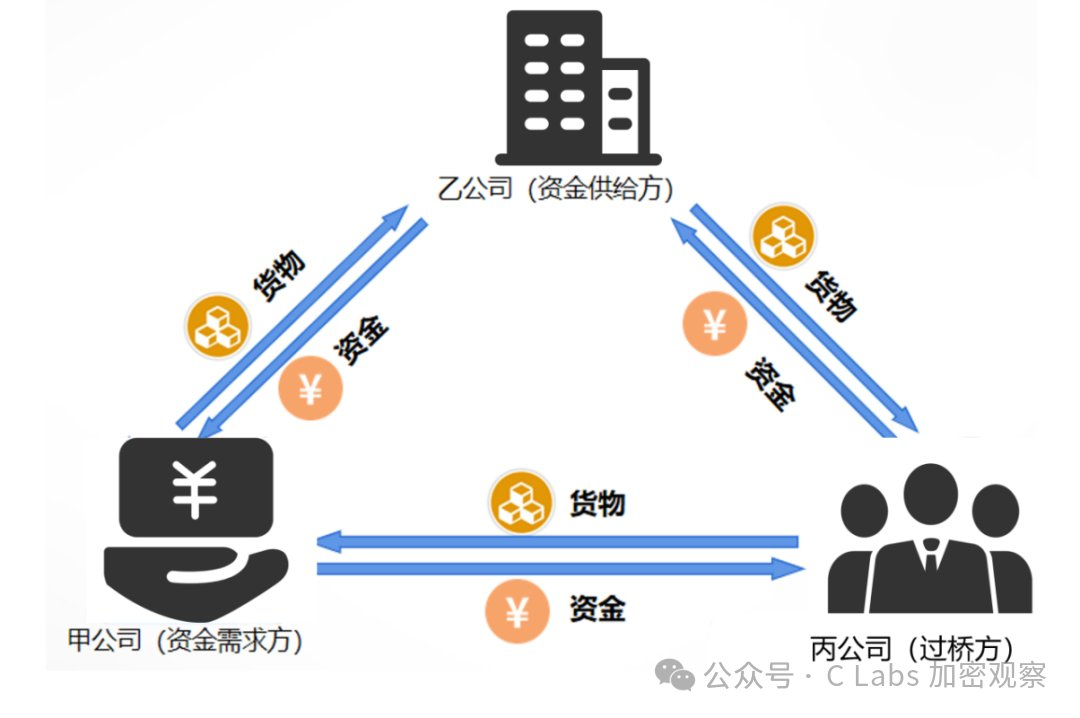

Path One: Tied Deals Network—Largest Scale, Renminbi Does Not Leave the Country

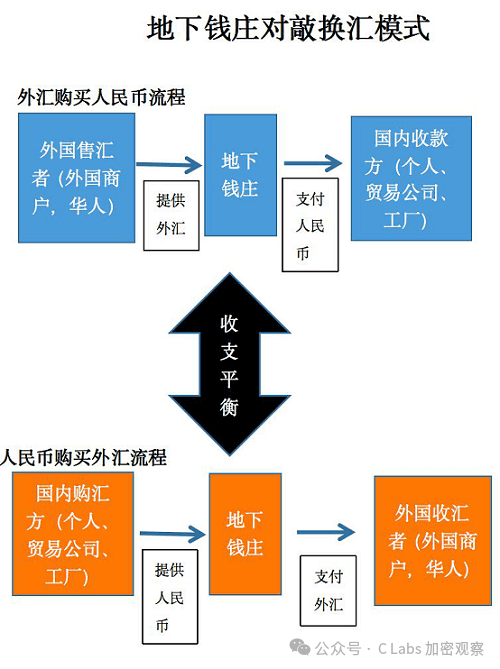

This is currently the primary channel for high-net-worth individuals to transfer large amounts of funds, known in the circle as "Duiqiao," corresponding to the term Hawala in the international anti-money laundering framework.

The operational logic is exceptionally clever: not a single cent truly crosses China's borders.

Specific process: domestic investors transfer Renminbi into a certain domestic account controlled by an underground money house; the money house then directly deposits an equivalent amount of foreign currency into the client’s foreign account from its associated institutions overseas (typically in Hong Kong, Singapore, or Vancouver). Both ends settle separately, with only "information" crossing borders, not "funds".

This system is logically flawless—precisely because there is no real cross-border capital flow, traditional monitoring methods from the foreign exchange bureau are difficult to capture directly.

Where is the risk? First, the handling fee; as regulation tightens, the cost is no longer at the early levels of 1%; secondly, the source of foreign currency funds in underground money houses is complex; if mixed with international criminal funds, clients' foreign accounts may be directly frozen by local judicial authorities without their knowledge; thirdly, once caught domestically, they face administrative fines of over 30% of the transferred amount and potential criminal prosecution.

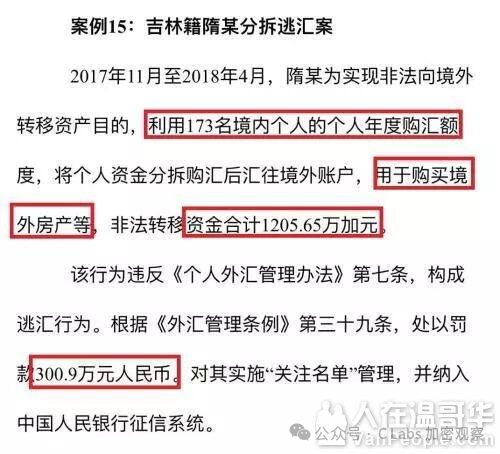

A typical case disclosed by the Beijing procuratorate in 2025 shows that five individuals, including Lin, received illegal foreign exchange funds through bank cards under their names and completed cross-border payments using virtual currency, ultimately being sentenced to two to four years in prison and fined for illegal business operations.

Path Two: Ant Migration—"Distributed Computing" of Legal Quotas

More well-known than tied deals is the so-called "Ant Migration"—using each person's legal quota of $50,000 annually for "distributed" transfers.

Operational method: a core investor mobilizes relatives, employees, and even pays unrelated individuals to each legally exchange $50,000 using their own ID and banking app, then simultaneously remitting the foreign currency to the same account abroad.

This route is being systematically hunted down by algorithms. The anti-money laundering model deployed by the foreign exchange bureau specifically identifies the pattern of "multiple unrelated domestic accounts remitting to the same foreign account within a short period." Once triggered, related accounts will be frozen, and involved parties may face a years-long foreign exchange trading ban.

Path Three: Trade Invoice Fraud—"Current Account" Legal Cloak

This is the most commonly used tool by private entrepreneurs with import and export businesses, technically known as Trade-Based Capital Flight, exploiting a regulatory loophole: remittances for goods trade are not subject to the $50,000 personal limit, and banks must release funds as long as they see compliant trade invoices.

Import Overreported Invoice: A domestic company secretly purchases equipment from its controlled shell company in Hong Kong or the Cayman Islands, with a real value of $500,000 but falsely invoiced at $1 million. The bank releases the $1 million, with the excess $500,000 safely parked in the overseas shell company’s account.

Export Underreported Invoice: A reverse operation. $1 million worth of goods exported to an overseas related party at a "low price" of $200,000, which then sells to the actual buyer at market price, keeping an $800,000 profit overseas.

The core advantage of this route is that it wears a completely legal cloak. Its downside is that it requires real trade activities as a cover, and in recent years, data cross-referencing between customs and the foreign exchange bureau has become increasingly meticulous.

Path Four: Channel Migration—From Internet Brokers to State-Owned Bank Wealth Channels

After regulatory hammering, funds have noticeably migrated to different channels.

According to Bloomberg's observations, the wealthy class is shifting in two directions: one is through cross-border wealth management lines of major institutions like Bank of China (Hong Kong) and HSBC, which have high compliance costs and require detailed proof of source of funds and tax payment, but the operational paths are completely legal; the other is using state-approved QDII (Qualified Domestic Institutional Investor) quotas to invest in overseas funds, but these quotas are strictly controlled by the state and cannot be directly used to hold foreign properties or bespoke assets.

In plainer terms: wealthy individuals are spending higher costs, taking narrower compliance paths, to send the same money abroad.

Path Five: Structural Arrangements—Trusts, Insurance, Immigration Investments

This is the preferred path for ultra-high-net-worth individuals, with the highest technical content, involving the combination of offshore family trusts, Hong Kong life insurance (with part of small premiums still usable for card payments), immigration investment projects (EB-5, various provincial investment immigration programs in Canada, etc.).

All Chinese citizens who legally immigrate to other countries or regions have only one opportunity to apply to the foreign exchange bureau for the opportunity to transfer immigrant assets.

A significant characteristic of this route is that the compliance costs are extremely high, but the legal gray areas are relatively small. If executed properly, what gets transferred is not the "money" itself, but the legal structure of asset ownership.

The Ultimate Response from Regulation: Extending the Wall to Individuals

Faced with the never-ending flow of money year after year, the core strategy of regulatory authorities has undergone a qualitative change—not only focusing on money but now targeting individuals.

From "regulating enterprises" to "regulating individuals."

The previous regulatory framework for external investments primarily targeted corporate entities. Asset transfers carried out by individuals through complicated proxies, overseas consulting contracts (remitting funds abroad under the pretense of "consulting fees"), and intellectual property transfers had long remained in a gray regulatory area.

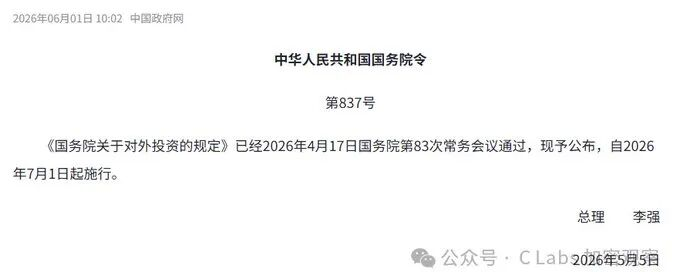

The revised foreign investment regulations by the State Council clearly extend regulatory reach to "individual residents," and all of the aforementioned individual-level structural arrangements are now included in the national security review and anti-money laundering monitoring framework.

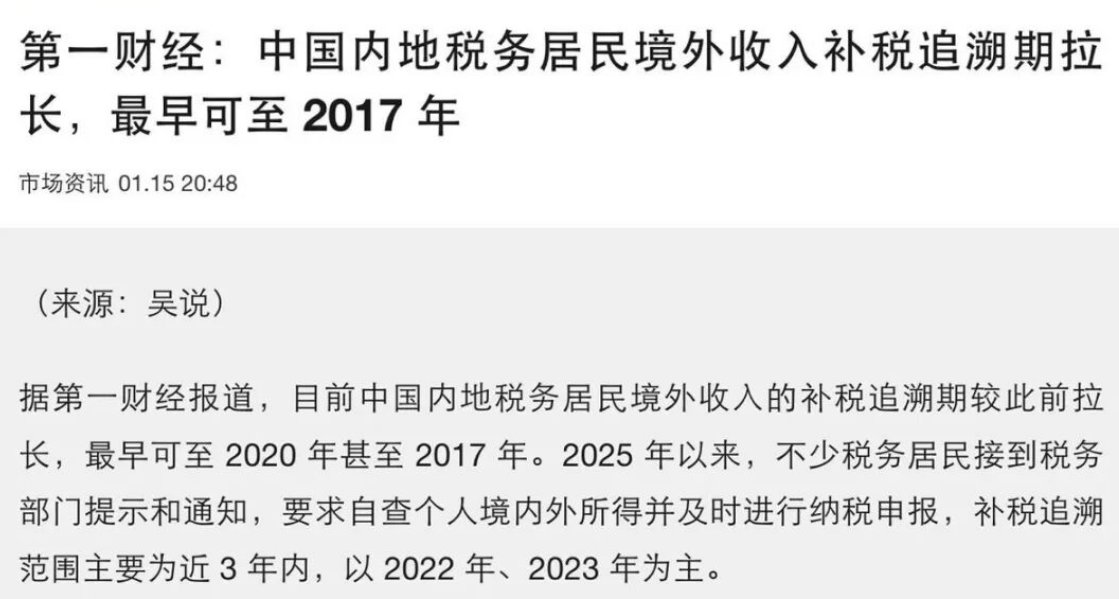

CRS: The Sharpest "Retrospective" Weapon

The full integration of CRS into the domestic enforcement system in 2024 is the most technologically sophisticated step in this round of blockading.

The operation logic of CRS is that over 100 countries/regions participating in this framework automatically report information each year to the Chinese tax authorities regarding the account balances, interest, dividends, and income from the sale of financial assets of Chinese residents.

This means that assets transferred out through various channels and quietly lying overseas over the past decade are now exposed to the eyes of Chinese tax authorities. It is not a matter of "possibly being discovered," but rather that they have already been recorded.

Cryptocurrency: A "New Channel" Under Judicial Scrutiny

Bloomberg's report touches on cryptocurrency channels only briefly. However, this is precisely the gap that is worth supplementing in the report.

From existing judicial cases in China, using stablecoins like USDT for cross-border currency exchange has already become a key target of prosecutorial efforts. A typical case from the Beijing procuratorate in 2025 explicitly defined "utilizing virtual currencies for cross-border settlements" as illegal business operations.

This means that cryptocurrencies are not a "hole" in the wall, but rather a special channel that is already under surveillance and is being systematically closed.

Bloomberg's report concludes with a background figure: China has over 6.2 million wealthy families with assets exceeding $1 million.

In the context of the collapse of the real estate myth, declining domestic asset returns, and rising geopolitical uncertainties, the motivation for this vast group to allocate wealth overseas will not disappear just because of a wall.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。