Author: Ada, Deep Tide TechFlow

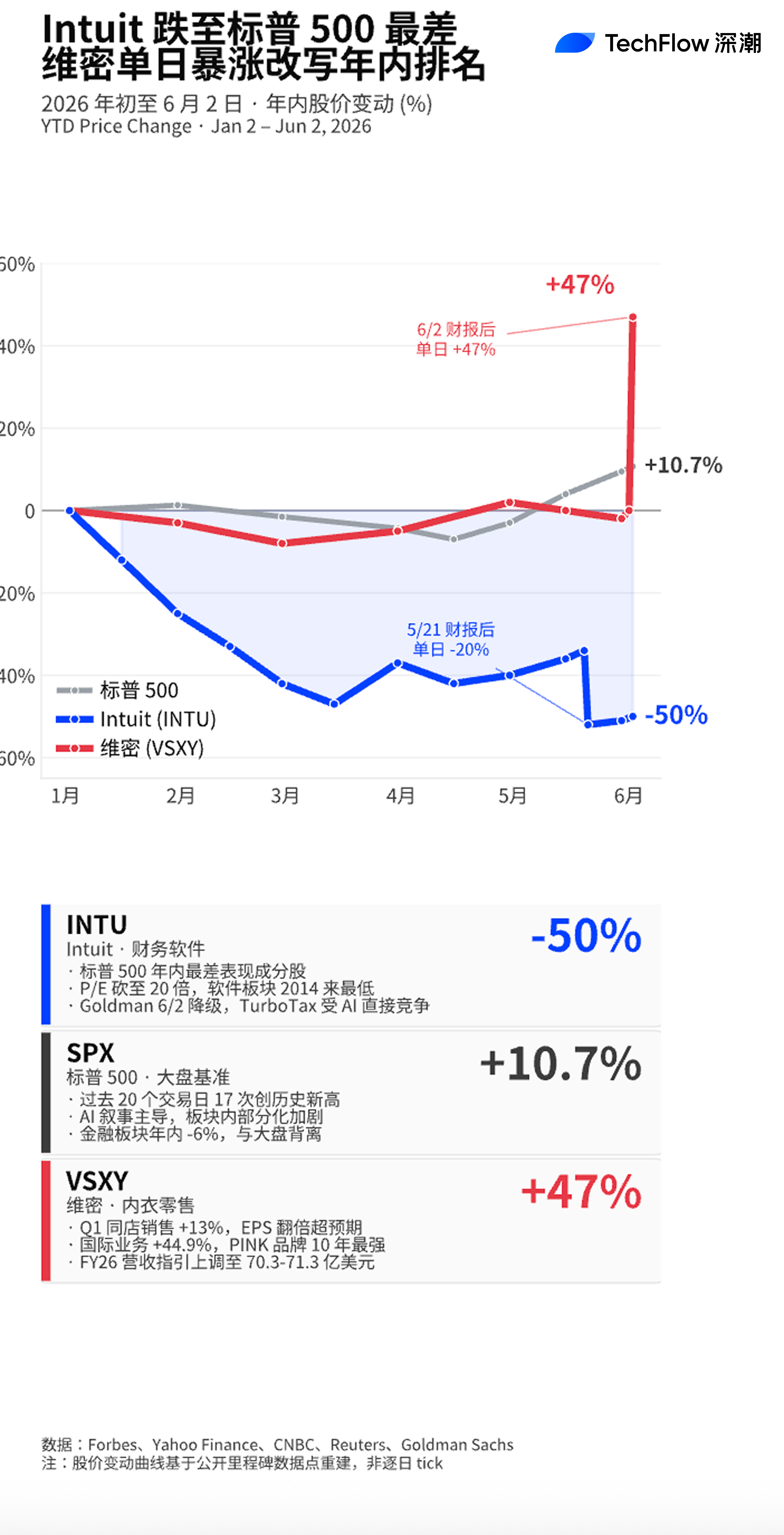

On the last trading day, Forbes published an article listing Intuit as the worst-performing component of the S&P 500 so far this year, while Goldman Sachs simultaneously announced a downgrade; Victoria's Secret surged 47% in a single day, thanks to a Q1 financial report that exceeded expectations. This is not simply a warm and cold comparison between two individual stocks; it reflects two sections of a latent fracture within the current U.S. stock market.

The narrative is repricing the market, showing typical industry differentiation in the U.S. stock market amid the current AI shock. Traditional retail can be rejuvenated by products and experiences, but the software sector is suffering a severe blow.

Forbes Stamps "Worst": Intuit Drops 50%, Goldman Issues Downgrade the Same Day

According to a report by Forbes on June 2, Intuit has become the worst-performing component of the S&P 500 so far this year. Data from Yahoo Finance and Motley Fool shows that as of early June, INTU has fallen about 50% year-to-date, with a decline of over 55% in the past 12 months, and its market value has shrunk to approximately $106 billion. On the same day, a team led by Goldman Sachs analyst Gabriela Borges downgraded its rating, stating that Intuit's stock price is likely to remain in a range-bound oscillation for the next few quarters, and investors need to lower their profit expectations to reflect a more severe competitive environment.

Ironically, the company's fundamentals have not shown significant deterioration. Intuit's revenue for the third quarter was $8.6 billion, a year-on-year increase of 10%; EPS exceeded expectations for the past four quarters; management raised the fiscal year 2026 profit guidance in May. However, the stock price crashed by 20% on the day after the May 21 financial report, becoming a key event that undermined market confidence. Motley Fool noted that the rarity of this drop lies in the fact that it occurred just after the company released multiple favorable signals that investors typically favor, including exceeding performance guidelines, raising annual expectations, expanding buybacks, and increasing dividends.

Goldman's core concern centers on TurboTax. This flagship product contributes about one-fourth of Intuit's revenue and operating profit but is facing direct competition from AI-driven tax tools. BofA also lowered its target price on May 27, stating that AI's substantial erosion of Intuit's "business model moat" needs to be repriced.

SaaS Sector Systematically Discounted, P/E Cut from 35 to 20 Times

Intuit is not alone. Auxier Asset Management noted in its Q1 2026 investor letter that "the SaaS (Software as a Service) industry is one of the most severely impacted areas in the Q1 market, as investor uncertainty regarding the potential disruption of AI continues to rise, with concerns that AI may commoditize the entire industry and compress profit margins."

Data confirms this assessment. Forbes previously reported that the forward price-to-earnings ratio of the software sector fell from about 35 times at the end of 2025 to 20 times in Q1, the lowest level since 2014. The iShares Expanded Tech-Software Sector ETF (IGV), which tracks the software sector, saw a quarterly drop of over 24% in Q1 2026, the largest quarterly decline since Q4 2008. Even after hitting a low of about $74 in April and subsequently recovering to around $92, IGV has still recorded historically negative excess returns relative to the S&P 500 year-to-date.

Jim Cramer from CNBC provided a more specific description in early February, stating that among the worst performers in the S&P 500 in January, the second, fourth, seventh, ninth, and tenth positions were all software companies, "with the same business model crushed by the same issue: the compression of P/E ratios due to AI." Intuit ranked as the second worst-performing stock in the S&P 500 in January, with a nearly 25% decline in a single month.

This process of valuation compression is almost unrelated to fundamental performance. Forbes relayed Auxier's statistics: companies like Intuit, Adobe, Salesforce, and FICO saw their stock prices fall by 30% to 37% in Q1, yet they all released strong earnings reports. The core concern for investors is that AI agents can replace most of the work currently performed by existing software companies at much lower costs.

Intuit's Turnaround: Collaborating with Anthropic, "If You Can't Beat Them, Join Them"

Intuit's management is not unprepared for the AI threat. CEO Sasan Goodarzi identified AI as a core strategy for the company long before mainstream software companies fully embraced it, repeatedly stating over the years that AI should be seen as a tool, not a threat. On February 24, Intuit announced a long-term partnership with Anthropic.

The bi-directional structure of the collaboration is quite symbolic. Intuit will connect core products like TurboTax, Credit Karma, QuickBooks, and Mailchimp through the MCP (Model Context Protocol) to Anthropic's Claude.ai, Claude for Enterprise, and Cowork products; conversely, Anthropic's AI models will drive customized agents on Intuit's platform. Trading Tips succinctly summarized this as: "If you can't beat the robots, hire them."

Ironically, Anthropic is one of the core forces behind market concerns about disrupting TurboTax. Intuit's pre-market stock price briefly rebounded when the collaboration news was announced, but mid- to long-term valuation pressure remained unrelieved. Goldman Sachs' downgrade report on June 2 pointed out that TurboTax is facing direct competition from AI-driven tax tools, a category that represents about one-fourth of Intuit's revenue and operating profit, determining the core of the company's valuation anchor.

On a deeper level of irony, Intuit has become an early example of the trend toward "second-class status" in the AI ecosystem. In the AI narrative, software companies at the application layer are expected to diverge in two directions: one aligning more closely with upstream foundational models (like Intuit collaborating with Anthropic), and the other being directly replaced by native AI products. The current market valuation for the former is not significantly higher than for the latter.

Victoria's Secret's Inverse Evidence: The Market Rewards Profit Visibility, Not Narrative

On the same June 2, Victoria's Secret (NYSE:VSXY, formerly VSCO, switched in May) saw its stock price surge 47% in a single day, reaching a historical high of $81.28 during the day. Over the past 12 months, the company's stock price has nearly tripled.

Driving the stock price is a robust earnings report. Q1 revenue was $1.56 billion (up 15% year-on-year, market expectation was $1.52 billion); adjusted EPS was $0.60 (market expectation was $0.30, nearly doubling); same-store sales growth was 13% (market expectation was 11.4%). On the operational front, operating profit jumped from $20 million to $76 million year-on-year; the company has repurchased 2.2 million shares this year at a cost of $100 million.

Benzinga data shows that North American store sales were up 11.3% to $802.8 million, direct channel sales were up 8.4% to $469.4 million, and international business was up 44.9% to $287.4 million, mainly driven by the Chinese market. The PINK brand recorded its strongest growth in ten years, with Beauty business growing by double digits; all three main brands of Victoria's Secret, PINK, and Beauty achieved double-digit sales growth.

CEO Hillary Super stated in an interview with CNBC: "We had a very strong start in 2026, exceeding revenue and profit guidance, continuing the momentum built in the second half of last year." She attributed the growth to product focus, reduced discounting, and a revival of brand enthusiasm, including the return of the lingerie show and Valentine's Day marketing. Earlier reports from Axios cited her description that the essence of the lingerie business should be "fun and pleasure," rather than a serious business.

CFO Scott Sekella pointed out that part of Q1 sales did benefit from tax refund spending, but the proportion is at normal levels, and even when the tax refund effect declines entering Q2, demand remains stable. The company simultaneously raised its FY2026 revenue guidance to $7.03-$7.13 billion (from $6.85-$6.95 billion), and adjusted operating profit guidance to $550-$580 million (from $430-$460 million). The single operating profit guidance alone was revised upward by more than $100 million.

More intriguingly, market structure reveals notable details. According to Ortex data, about 19% of VSXY's tradable shares are currently shorted, with some analysts believing this unusually high short ratio could provide additional impetus for the current rally.

A Dual Diagnostic Mirror

In June, when the S&P 500 continues to hit new highs and the AI narrative dominates the market, the inverse movement between the software sector and Victoria's Secret constitutes a diagnostic mirror. Intuit's 50% drop is not an isolated incident but an early discount by the market on "future risks": when the AI disruption narrative reaches its peak, even fundamentally strong SaaS leaders with consistent EPS exceeding expectations will be repriced in the lowest P/E ratio since 2014.

Victoria's Secret's inverse movement provides another set of evidence: in a market where the narrative compresses valuations, profit visibility itself is becoming scarce. The turnaround of same-store sales from negative growth to +13%, the execution of Hillary Super's team over the past year, and the explosive growth of international business at +44.9% are directly rewarded by the market in a single-day increase of 47%.

In other words, the market's bet in 2026 is not on "what AI can disrupt," but on "besides the AI narrative, what is actually making money." The answers to these two questions will determine the critical sector allocation direction for the second half of the year.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。