Author: Chloe, ChainCatcher

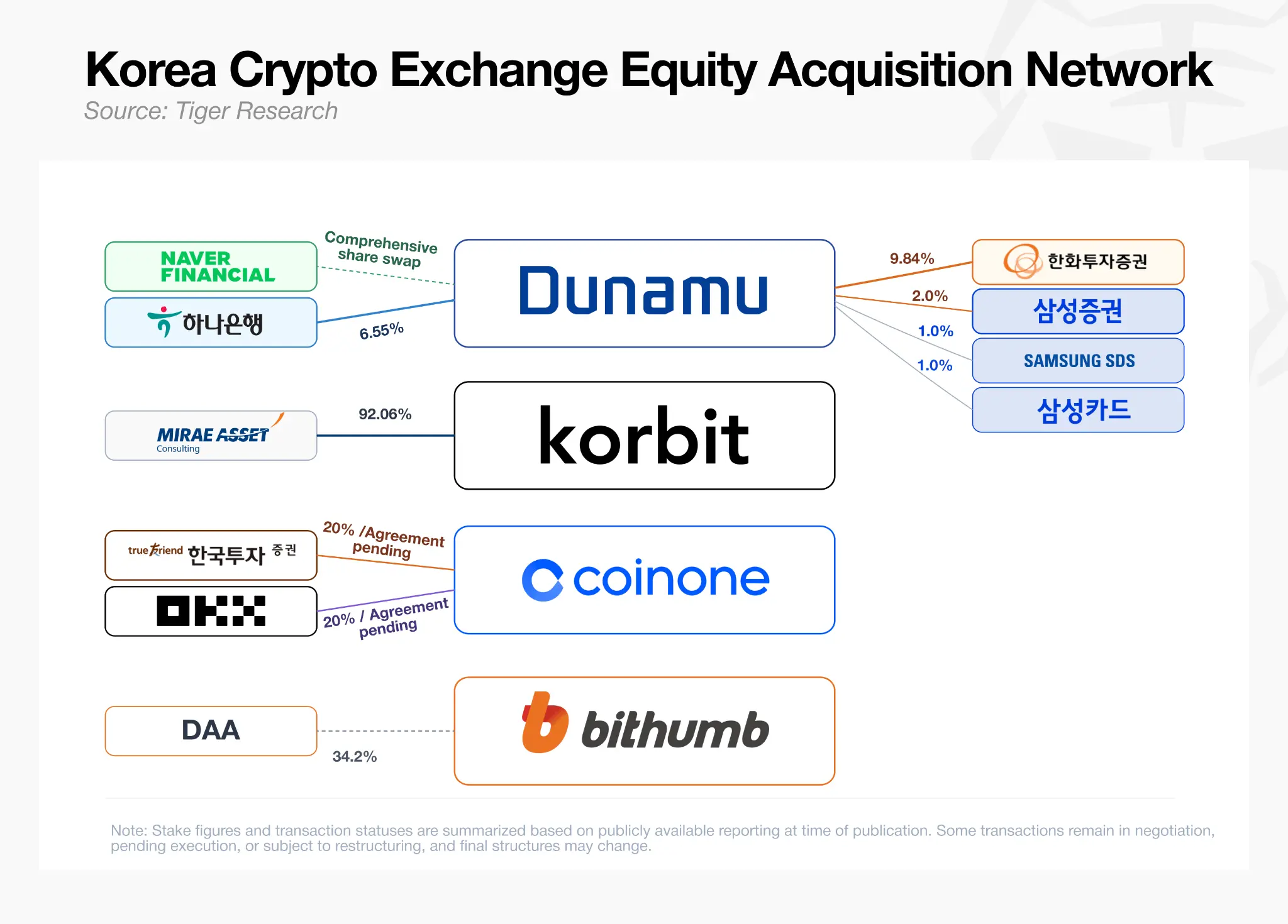

Last week, South Korean cryptocurrency exchange Coinone officially announced the introduction of two heavyweight new shareholders. The global exchange OKX's venture capital department, OKX Ventures, along with South Korea's major brokerage Korea Investment & Securities (KIS), will each invest 80 billion Korean Won (approximately 53 million USD) to acquire about 19.6% to 20% of the equity, totaling nearly 40%, making OKX Ventures and KIS the third-largest shareholders.

On the surface, this transaction is a story of “foreign capital opening the door to South Korea,” as after Binance acquired Gopax, OKX becomes yet another international player holding significant equity in a licensed South Korean exchange. However, when we zoom out, the real protagonist of this deal is actually the South Korean brokerage that is in line with OKX.

Korea Investment & Securities CEO Kim Sung-hwan also revealed the motive: “This is our first step transitioning from traditional finance to blockchain digital financial services.” For KIS, Coinone serves as a springboard to enter new battlegrounds such as the issuance and circulation of security tokens (STO), stablecoin-related services, digital asset brokerage, and institutional-level cryptocurrency business.

It can be said that even this transaction packaged as “foreign capital entering the market” is predominantly led by a local South Korean brokerage, while foreign capital appears more like a minority financial investor hitching a ride. Additionally, this transaction involving Coinone represents just the tip of the iceberg in the larger context of the South Korean crypto landscape over the past three months.

Samsung subsidiaries each bring a different calculation

Just a day before Coinone's signing, on May 28, three companies under the Samsung Group—Samsung Securities, Samsung SDS, and Samsung Card—jointly announced they would invest approximately 612.8 billion Korean Won (about 408 to 446 million USD) to acquire 4% equity in Dunamu, the parent company of South Korea's largest crypto exchange, Upbit. Samsung Securities would take 2%, while Samsung SDS and Samsung Card would each acquire 1%. The transaction will be conducted in cash to acquire about 1.39 million shares from the Kakao Group’s fund (including Kakao Investment, Kakao Ventures, etc.), with expected completion of delivery on June 19.

Notably, the valuation: at approximately 439,000 Korean Won per share, it means Dunamu's overall corporate value is estimated at about 15.3 trillion Korean Won, equivalent to around 1.11 billion USD. The seller, the Kakao Group fund, will completely exit Dunamu through this bulk transaction, symbolizing that the “old shareholders” in the South Korean crypto landscape are being replaced by “new faces.”

Moreover, the three Samsung subsidiaries bring their distinctive calculations to the table, and these three calculations almost perfectly correspond to the three main pillars of the "Digital Asset Basic Law," which South Korea plans to finalize by 2026:

Samsung Securities is focused on the issuance and circulation of security tokens and virtual asset-related services, corresponding to STOs and tokenized securities.

Samsung SDS, as the group's IT and cloud arm, plans to integrate artificial intelligence, information security, and data governance capabilities into Dunamu's blockchain operational infrastructure, corresponding to foundational technology infrastructure.

Samsung Card aims at the digital asset payment ecosystem, planning to integrate crypto payments into the unified platform Monimo of Samsung's financial network after launching the Korean Won stablecoin, corresponding to the stablecoin payment track.

In other words, Samsung is not treating this 4% as a simple financial investment, but rather as a piece of the group's financial services strategy for the next decade. A Samsung insider told the Korea Times that this move aims to strengthen the competitiveness of each subsidiary in the digital asset business and assist the group in achieving leadership in this market.

For one of South Korea's most prominent conglomerates, this essentially signals to the market that it is building a complete digital asset infrastructure rather than making a gamble.

Traditional funds are enthusiastic, is virtual asset a blue ocean?

Looking back in time a bit further, in mid-May, Hana Bank agreed to acquire 6.55% of Dunamu for about 1 trillion Korean Won (approximately 670 to 720 million USD), becoming the first South Korean financial holding group to directly hold equity in a cryptocurrency exchange. Less than ten days later, Hanwha Investment & Securities approved an additional investment of about 3.90%, raising its stake to 9.84%, spending an additional 597.8 billion Korean Won, and becoming one of Dunamu's largest non-founder shareholders.

Additionally, Mirae Asset had already signed a deal through its subsidiary Mirae Asset Consulting in February to acquire up to 92.06% of the fourth-largest exchange in South Korea, Korbit, for about 133.5 billion Korean Won. From the leading Upbit and the third-largest Coinone to Korbit, almost every major exchange in South Korea has, in just a few months, replaced its background with a new face from traditional finance.

So why are these traditional funds so eager? The financial figures from Dunamu provide part of the answer: for the fiscal year 2025, it reported revenue of 1.56 trillion Korean Won and a net profit of 708.8 billion Korean Won, claiming over 80% of South Korea's virtual asset trading volume. The significance of this large pie is naturally self-evident for banks and brokerages.

Market structure is chaotic, institutions are laying out their plans early

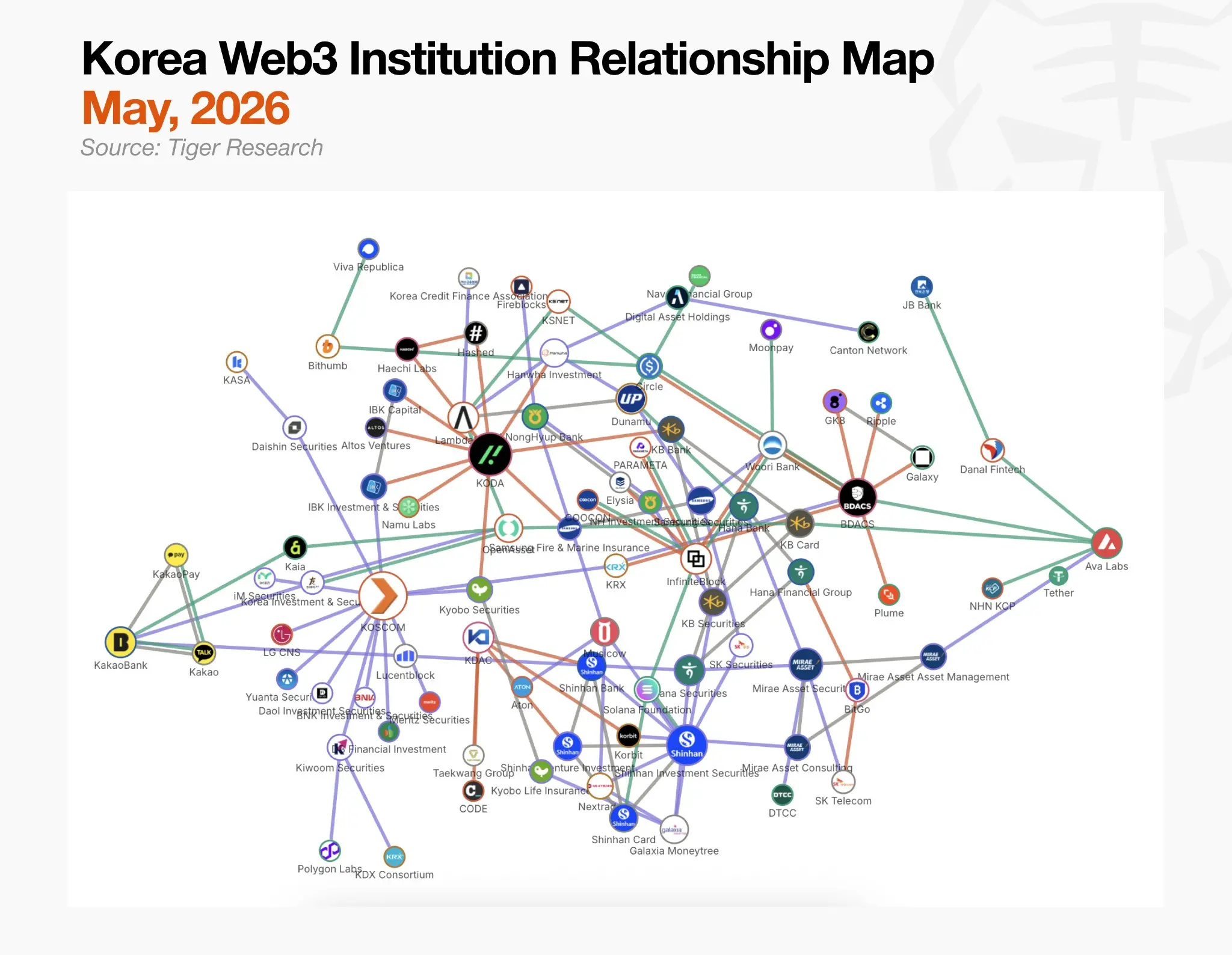

A report released last week by the research organization Tiger Research reviewed 150 Korean institutions and 196 partnerships and reached a key conclusion: currently, no single hub has gained dominant control of the market.

The overall relationship map is complex and accurately reflects the current market's chaos, revealing that various institutions are simultaneously laying out strategies across multiple tracks while regulations are still undecided.

This can be described as a "scramble for exchange equity," reflecting the series of actions by Hana, Hanwha, Samsung, Mirae Asset, and KIS. Analysts believe the essence of this competition is the “revaluation” of the value of cryptocurrency exchanges: they are no longer just platforms that collect fees but also key customer touchpoints for distributing stablecoins, custodial services, security tokens, and RWA products.

For banks and brokerages, investing in exchanges is equivalent to a shortcut: it allows them to indirectly obtain licenses such as VASP registration while simultaneously gaining access to an exchange's existing user base and liquidity.

Further analysis of this competition revolves around three key fronts: stablecoins, STOs, and custody.

The maturity of these three fronts varies. The most active is the custody sector, where several players have started providing services after crossing regulatory hurdles, with four major custodians—KODA, KDAC, BDACS, and BitGo Korea—each binding financial and technology partners; RWA and STO are mostly stuck at the contract or MOU stage, waiting for legislation to take effect; and stablecoins are also stagnated, with no party able to claim dominant control of the standard-setting process.

The biggest bottleneck is not technical but legislative. The Bank of Korea is pushing the "51% rule," arguing that only an alliance with banks holding the majority of shares can issue stablecoins, which has garnered strong backlash from fintech players, delaying negotiations between political parties.

Currently, this wave of collaboration and acquisition should not be interpreted as mere commercial development, but rather as institutions rushing to secure favorable arrangements before regulations are finalized, which can then be used to influence the final regulatory framework. The current alliances and partnerships are more about “designing regulation” than simply attacking the market.

Supporting this judgment is a clear shift in market focus. Analysts point out that the South Korean crypto market has undergone significant restructuring in just six months: the custody camp is forming, STO alliances are gathering, financial conglomerates are rushing to invest in exchanges, while retail trading volume is rapidly shrinking, with the combined trading volume of the top five exchanges decreasing by about 48% year-on-year. The market’s core is quickly transitioning from retail to institutional.

Conclusion

When piecing together segments such as OKX investing in Coinone, Samsung buying into Dunamu, Hana and Hanwha's increased stakes, and Mirae Asset acquiring Korbit, one discovers that they are actually different facets of the same story, which is led by brokerages and banks collaboratively reorienting the South Korean crypto landscape from "retail speculative trading ground" to a consolidated entry point for "traditional financial digital asset distribution."

However, since the operational aspects of the consolidation have yet to materialize, most collaborations remain as MOUs. STOs and stablecoins are still awaiting legislation, and the market remains cautious with reservations.

This transformation also changes the way overseas cryptocurrency projects enter the South Korean market. Just as Solana became a partner of Shinhan Card and Avalanche became a partner of Mirae Asset, projects entering the South Korean market have shifted their primary targets from exchanges to financial institutions and large enterprises.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。