Author: Tom Dunleavy, Head of Venture Capital at Varys Capital

Translation: Yuliya, PANews

Editor's Note: The current market generally views Ethereum as a traditional business, calculating its price-to-earnings ratio based on the fees it generates and concluding that it is overvalued. However, Tom Dunleavy proposes a radically different framework: fees are not revenue but network friction; Ethereum is not a company but a "vault" that protects hundreds of billions of dollars in assets, with ETH itself being the lock. Here is the translated original text:

TLDR

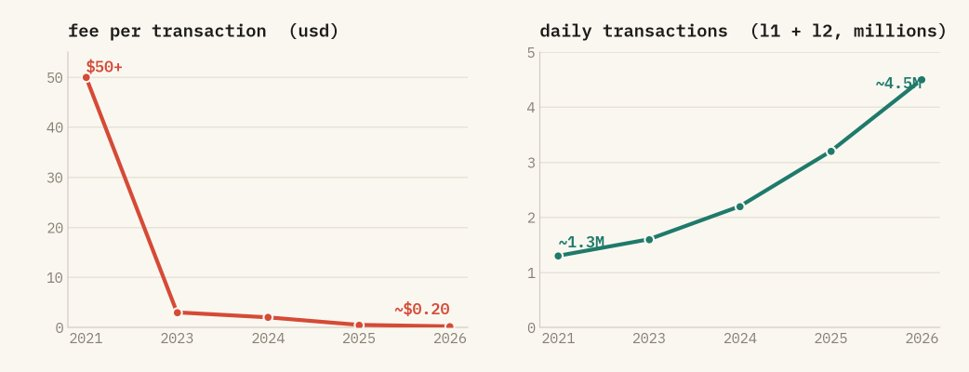

Stop using fees to value Ethereum. Fees are actually a stumbling block; a successful network will certainly find ways to drive fees down to zero. Currently, ETH fees have dropped from over $50 in 2021 to around $0.20 now, yet transaction volume has more than tripled. The plummeting fees indicate the network is very successful, not that it's about to cool off.

After transitioning to proof of stake (PoS), ETH became the lock protecting the asset vault. To attack Ethereum, one must control the staked ETH. Controlling one-third would disable the network, while controlling two-thirds would allow altering records. Regardless, the cost of malicious actions is calculated in ETH, and once harmful actions are taken, these ETH would be directly destroyed by the system. This tightly binds the value of ETH to the security of the network. No network operated this way before the staking mechanism appeared.

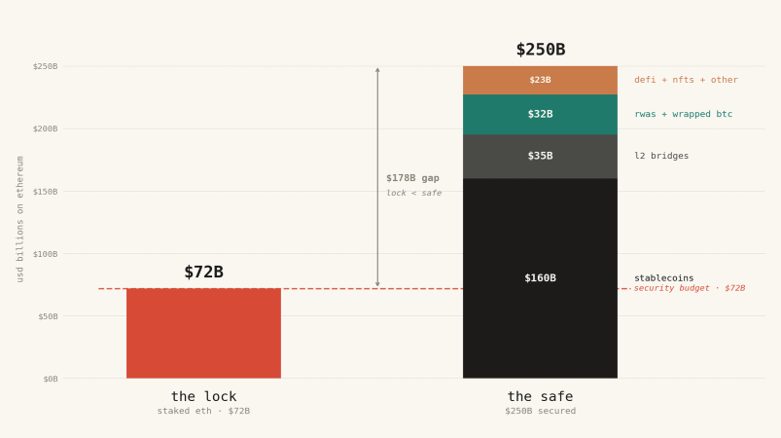

Currently, there are approximately $250 billion worth of assets on the Ethereum chain (including stablecoins, tokenized assets, cross-chain funds on L2 networks, etc.), but the staked ETH protecting these assets is only worth about $72 billion. It’s like using a cheap, broken lock to protect a safe full of gold bars. The reasonable price for ETH should be around $6,900 (currently it is only $2,070). If the on-chain assets rise to trillions, the price of ETH must increase to tens of thousands of dollars to fulfill its security responsibilities.

Some say "Ethereum is like free Linux" or "like DTCC (the U.S. Depository Trust & Clearing Corporation)," but that is incorrect. The sense of security provided by Linux and DTCC comes from others (like the open-source community working on goodwill or the legal assurances from governments and banks). However, Ethereum's security is purchased with its own token, ETH. Therefore, ETH must be valuable, while Linux does not need to be.

If ETH fails, Crypto is likely to fail too.

Fees are not income, but friction

Last week, Bankless founder David Hoffman said he finally sold all of his ETH, which caused quite a stir in the crypto community. While I respect David's decision, I believe the way everyone assesses ETH and other PoS public chains is outdated. I have talked about my new framework with many people on shows, but it seems no one listened (maybe it was my expression), so today I will clarify everything at once.

New things must be seen with fresh eyes. So let me introduce a brand new valuation model for ETH.

Many people treat Ethereum as a company and consider the fees collected as the company's revenue. When they see fees drop, they think this "company" is failing and that the token is overpriced. This is completely misguided; once you understand, you will never see it this way again.

In reality, fees are like taxes; the higher they are, the less inclined people are to use it. Lower fees make people more willing to get involved, and applications and funds on-chain will increase. The data doesn't lie: the single transaction fee has dropped from over $50 in 2021 to about $0.20 now, but transaction volume has reached a historical high, more than tripling from 2021, with L2 now handling about 85% of transactions. It has become cheaper to use, and more people are participating. A successful settlement network should indeed aim to reduce tolls to zero.

Ethereum's fees have plummeted while transaction volume has reached new highs. It has become cheaper, and more people are using it. L2 now carries about 85% of the throughput.

So, if fees are the wrong metric, what is the right metric?

Ethereum is a great vault, and ETH is that lock

Stop treating Ethereum like a company; think of it as a super vault. This vault contains about $160 billion in stablecoins, $20 billion in RWA (like U.S. Treasury bonds, money market funds, and private credit), $35 billion in L2 cross-chain assets, with L2 networks inheriting Ethereum’s consensus by design. Additionally, there is about $12 billion in wrapped Bitcoin and about $20 billion spread across DeFi positions, NFTs, and on-chain vaults. Overall, the on-chain total assets are around $250 billion, growing every quarter.

The security of the vault relies entirely on that lock. Yet somehow everyone has miscalculated the value of this lock. On Ethereum, this lock is made of ETH.

Under the old proof-of-work (PoW) system, you protected the network using mining hardware. The lock was bought externally, and its cost was unrelated to the value of the tokens. But now it has changed to staking (PoS), and everything is different. Now, to attack Ethereum, you can only purchase and control that staked ETH. The lock is made from the tokens themselves. This means that the level of security of the vault and the market price of the token have become one and the same. You cannot separate them.

The current situation where locks are cheaper than safes

This is the problem the market is ignoring. Today, the total value of the staked ETH protecting Ethereum is only about $72 billion. Yet they protect assets worth as much as $250 billion. The money in the safe is more than twice as valuable as the lock protecting it.

This is dangerous. If what you need to protect is more expensive than the cost of doing harm, then your vault is not up to standard. To securely protect this $250 billion on Ethereum, the staked capital for defense must exceed $250 billion, not even be close to one-third of that.

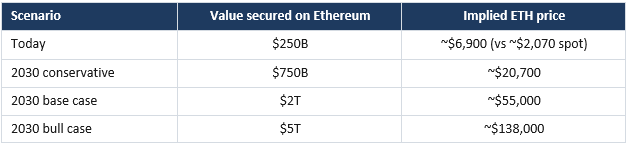

Currently, about 30% of ETH is staked. Therefore, to make this 30% of staked funds equivalent to the on-chain assets, the total market value of ETH must be more than three times the on-chain assets (1 divided by 0.30). Currently, the market value of ETH is roughly equal to the assets it protects (about 1 time). But according to my logic, it should be above 3 times. Based on the current $250 billion, the reasonable price for ETH should be around $6,900, not the current $2,070. This means that even without a single dollar entering the market, based solely on the assets it currently protects, the price of ETH should more than triple. This is very close to the directional model presented by BitMine’s chairman Tom Lee.

“But Circle can freeze USDC, so it doesn’t need ETH for protection at all.”

Every time I say this, someone comes out with that rebuttal, but that is completely wrong for several reasons:

People think that if Ethereum is attacked, the issuer of USDC, Circle, can simply freeze the bad actor's address and reissue the coins. Therefore, these hundreds of billions should not count towards Ethereum's security responsibility.

But consider that Circle’s freezing mechanism operates based on smart contracts and executes on Ethereum, relying on Ethereum’s ledger. If Ethereum’s consensus is compromised, there would be no recognized honest chain, and the freezing mechanism would fail to work.

Moreover, Circle could have opted not to use Ethereum and just create a private database. They chose Ethereum because they value its neutrality, deep liquidity, and compatibility with other projects. Having enjoyed these benefits, the trade-off is that USDC’s lifeline is now tightly coupled with Ethereum's security. If you want to benefit, you must bear the risk of reliance.

Additionally, people often assume attackers aim to steal USDC. But that's not the case; if Ethereum collapses, the $150 billion is not stolen, but rather trapped on a consensus-less chain, unable to be redeemed, leading to chaos in all loans and transactions based on that chain. The value of these assets would not be seized by thieves but would be destroyed. This destroyed value is an important factor that security must consider.

Attackers don’t even need to steal funds to profit. They can short ETH, short the entire ecosystem, or they could simply be a hostile force; as long as they can paralyze the network, they stand to gain significantly. The more money is on-chain, the greater the incentive to cause disruption. Therefore, our security budget must rise in tandem with the total on-chain assets, rather than just guarding against the small fragments thieves could steal.

Whenever you place money on Ethereum, you are consuming its security, regardless of whether you have that "freeze" button. All of the money must be considered.

“Ethereum is just like Linux” or “Ethereum is DTCC.”

There is another rebuttal favored by the clever crowd.

The first assertion: Ethereum is like the Linux system. It is the underlying infrastructure driving the entire internet, but as an asset, it is worthless. Open-source infrastructure is a free public good; the applications running on it make money, not the underlying protocols. So ETH will be similar: extremely important but completely worthless.

The second assertion: Ethereum is like DTCC, serving as the infrastructure behind nearly all U.S. securities transactions. DTCC processed $370 trillion in transactions in 2024, earning about $2.5 billion in revenue, but its profit was less than $500 million. It is crucial, regulated, yet its value constitutes only a small part of transaction volume. Infrastructure costs are low; even if you can't do without it, even when Ethereum handles more transactions in the future, it will only capture a negligible amount of practical profit—nothing more.

Both assertions are wrong for the same reason.

The security of Linux and DTCC is derived externally. Linux relies on the open-source community, reputation, and decades of code review. DTCC depends on U.S. law, federal regulatory bodies, and the major banks backing it with dollars and treasury bonds. Their security assurances come from outside the system. This is exactly why DTCC can settle vast wealth without capturing any value. It is a member-owned utility that operates on a cost basis. It doesn't need a valuable token because trust is provided by the government and banks.

Ethereum lacks these external protections. There is no government enforcing it. No member banks supporting it. There are no laws to reverse stolen settlements. The only barrier between Ethereum and attackers is the market value of the staked ETH used to protect it. Ethereum must purchase security for each block in the public market using its own assets.

That is the fundamental difference. Linux is software; no one is required to hold a scarce asset to run it. DTCC offers collateral in dollars, external to itself. Ethereum’s collateral is ETH, intrinsic to itself. You cannot commoditize its value to zero because security is not a line of code; it is a quantity of value that must be locked and exposed to risk. By stripping away the value of ETH, you are not creating a leaner version of Linux. You are creating an unsecured chain, and no one would trust it with a dollar.

So, don’t compare Ethereum to Linux or DTCC. You should compare it to the dollars and treasury bonds backing DTCC. No one assesses the value of the dollar based on how much fees DTCC makes. You would evaluate the clearinghouse fees separately and assess the dollars and treasury bonds that serve as collateral for the entire system, worth trillions of dollars. ETH is not a clearinghouse. ETH is the collateral that builds the clearinghouse. That is the asset you are purchasing.

Linux never needed a treasury. Ethereum’s security budget is a treasury, and it is priced in ETH.

Looking Ahead and Market Dynamics

Following this thought, this model does not consider fees or market speculation. It only focuses on one core question: how much money will settle on Ethereum in the future? What must ETH be worth to protect that money?

Stablecoins are about to surpass $1 trillion this year. Tokenized RWA could reach several trillion by 2030. Coupled with various on-chain applications, the assets Ethereum will need to protect will soar from the current $250 billion to several trillion. As long as the "more than triple" security factor remains constant, you can calculate how high ETH's price must rise as more funds flow in.

Even if you are more pessimistic and lower the security factor a bit, that's fine. On-chain funds are increasing (that's a variable), the security factor (that's leverage), and no matter how you calculate it, the overall direction is upward.

“This is blind optimism. The market will never price it like that.”

This is the most accurate rebuttal; indeed, I say what ETH "should" be worth, not what the market will "immediately" give it. There is no mechanism for enforced arbitrage to flatten the price differential. Moreover, my "ETH should rise" logic has indeed been challenged by price performance in recent years. Let’s break this down:

Regarding what can bridge the gap: Ethereum is not about arbitrage, but demand for dollar-denominated assets across the system. As value settles on Ethereum, ETH is used as collateral, paired trading assets, and staked to earn the underlying network returns. This demand grows with the activities it supports. Reserve assets are not priced based on income; they are priced based on how urgently the surrounding system needs to hold them. Gold is worth over $18 trillion but generates no cash flow. ETH is the reserve asset for on-chain finance, and this framework simply measures how large that reserve must be.

About the staking multiple: my mental model views the staking multiple as a range rather than a fixed target. At the current staking rate, parity (staked ETH equals protected value) is approximately 3.3 times. The reasonable range varies from a loose end of 1.7 times to a strict end of 5 times, at the strict end, the cost of initiating an attack with two-thirds of the staked share must equal the total protected value. Prices will track the protected value under some multiple within this range. Fixating it at a specific number would undermine rigor, and this is where rational people can diverge without compromising the model.

Regarding reflexivity: the model indeed has more than one equilibrium point, and nothing deterministically selects the highest one. Today, Ethereum is sufficiently secure at a coverage below the lower limit because obtaining one-third of the staked shares has poor liquidity, the slashing mechanism is extremely harsh, and the social layer can fork out attackers. This is genuinely true, but these defenses determine whether an attack is successful, not whether the coverage is enough as risks rise. When protecting $250 billion, weak coverage can be tolerated. When it comes to trillions or tens of trillions of regulated institutional funds, coverage is no longer an academic issue. As adoption increases, the gradient to bridge the gap will monotonically rise.

Finally, the most contradicting evidence is the price of ETH over the last 5 years. Logically, it should rise, but practically, it has consistently fallen. I believe the main reason is that there hasn’t been enough money on-chain for people to consider security as a major issue. When there was only $50 billion on-chain, no one was worried; when it rose to $175 billion, people started to feel something was off; and when it hits $1 trillion, the first question those major institutions will ask as they enter will definitely be: “Is this chain secure?” The answer to that question fully hinges on the price of ETH. My model cannot predict when it will rise, but it tells you that as more funds arrive on-chain, the upward pressure will grow stronger, and the fact that "more funds are coming on-chain" is something even the bears cannot deny.

Some rebut people by comparing to Bitcoin, claiming that Bitcoin's security budget is negligible compared to its market value. But Bitcoin primarily protects itself. Ethereum protects others' dollars and various assets, which is a heavier responsibility! Additionally, the trend is already clear: more ETH is being staked, compliant products continually buy ETH, and as on-chain activity rises, the burning mechanism keeps destroying ETH. All of this validates my assertion of growing demand.

Those who only focus on fees and cash flow will continue to claim ETH is overvalued. They have completely reversed the causal relationship. There must be on-chain activity first, and then security becomes necessary. ETH needs to be valuable to safeguard the entire ecosystem’s security. Fees are the stumbling block you should aim to eliminate, not the chip you use to value ETH.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。