SpaceX's super IPO is about to land; Musk aims for a trillion-dollar fortune, while early allies reap hundredfold returns.

Written by: Nancy, PANews

As the storage sector surged, with Micron and SK Hynix each breaking the one trillion dollar market value barrier, Musk is also accelerating the creation of his trillion-dollar wealth myth.

SpaceX is rapidly moving towards the capital market with a sky-high valuation. This super IPO, which may rewrite the history of wealth, is pushing Musk towards becoming the world's first trillionaire and allowing early allies to achieve astonishing returns of hundreds or even thousands of times their investment.

However, for this expensive narrative of human history in space to continue, new payers are ultimately needed. As massive pension funds are "forced to buy in," American retirement funds are becoming the fuel for Musk's space dreams.

Musk is making American retired men and women “explode coins.”

The countdown to the largest IPO in history; early allies profiting immensely

Wall Street has been waiting for SpaceX to go public for many years.

Over the past decade, the company has grown from a startup valued at only $27 million to a super unicorn now valued at nearly $1.75 trillion to $2 trillion, becoming one of the highest valued private companies globally.

Now, this super IPO is set to be officially listed on June 12 at the earliest. This is not only the largest IPO event in human history but also signifies the moment when a wealth feast begins to be cashed out. Musk's long-time followers have finally reaped substantial returns.

For example, Google emerged as the largest external winner through early investments. By the end of 2025, it holds about 6.11% of SpaceX shares. An investment of only $900 million years ago now corresponds to a value nearly reaching $120 billion; Valor Equity Partners, as the second-largest shareholder after Musk, holds more than 500 million Class A shares of SpaceX, with a value range of around $90 billion to $140 billion; Peter Thiel's Founders Fund holds approximately 3.5% of shares, with a book profit exceeding $60 billion due to multiple rounds of additional investments; Fidelity, as one of the main institutions in the joint funding of 2015, has its shares valued at about $35 billion; even Sequoia Capital, which entered relatively late, is expected to gain over $20 billion in returns.

As for Musk himself, he is also poised to become the world's first trillionaire.

Bank of America strategist Michael Hartnett warned in a recent report that once super IPOs like SpaceX and OpenAI go public, the weight of tech stocks in stock benchmark indices will easily exceed about 48%, surpassing the market concentration levels during all major bubble periods in history, including the 1920s "Roaring Twenties," the 1970s "Nifty Fifty," the 1980s Japanese bubble, and the 1990s tech bubble.

However, who will ultimately take on such a massive valuation?

To reduce the selling pressure after the listing and maintain stock price stability, SpaceX has also made certain adjustments. For example, internal shares will adopt a phased unlocking mechanism rather than the traditional six-month lock-up period common in IPOs; at the same time, the company has approved a stock split plan of 1-for-5 to lower the psychological thresholds for retail investors and enhance liquidity. Musk has explicitly stated that he will not sell any shares of SpaceX.

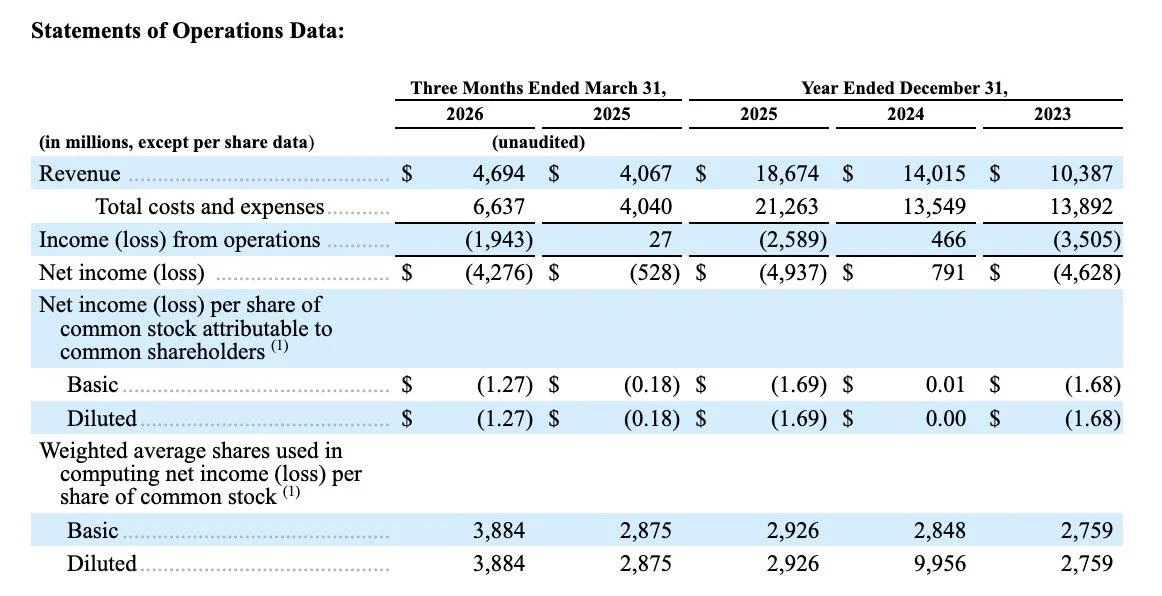

But market concerns have not dissipated as a result. Setting aside the uncertainties of the grand narrative about Mars, simply looking at the financial data, SpaceX remains a company that is burning cash at a fast pace. The prospectus shows that in the first quarter of 2026 alone, SpaceX's net loss was nearly $4.3 billion, almost equivalent to the total loss level for the previous year. Meanwhile, Musk controls 85% of the absolute voting power, meaning the board almost cannot fire him, and outside shareholders have little ability to push for any significant business decisions.

To some extent, SpaceX can be considered a highly Musk-centric company, with its valuation, governance, and even future expectations deeply tied to Musk himself.

After all early investors have profited tremendously, who would still be willing to buy into this already exorbitantly priced spaceship ticket?

Wall Street paves the express lane for indices; American pensions become the "backstop" buyers

American pensions may become the potential fuel for Musk's space dreams.

Wall Street has begun to open a fast lane for the super IPO. On May 1 of this year, new Nasdaq rules officially took effect, whereby newly listed companies that rank within the top 40 of the Nasdaq 100 index by market capitalization can be included in the index in just 15 trading days, whereas it typically required waiting about three months before.

Similarly, the S&P began consulting in May to shorten the minimum listing period from 12 months to six months and is considering exempting profitability requirements for ultra-large companies. FTSE Russell has also relaxed restrictions, allowing significant IPOs to be quickly evaluated for inclusion in the Russell U.S. Equity Indexes (including Russell 1000, Top 200, etc.) on the fifth trading day after listing, without waiting for quarterly reviews.

Major American indices are quietly relaxing their rules, undoubtedly setting up a dedicated runway for SpaceX.

According to Business Insider, SpaceX may quickly enter mainstream indices and ETFs after going public, with passive fund allocation potentially far exceeding previous major IPOs. For instance, the CRSP index corresponding to Vanguard VTI and growth ETF VUG could include SpaceX within just five trading days post-IPO; the Nasdaq 100 index tracked by QQQ may include SpaceX within 15 trading days after its listing; the S&P 500 index tracked by SPY might include SpaceX as early as 2027 following the rule modifications.

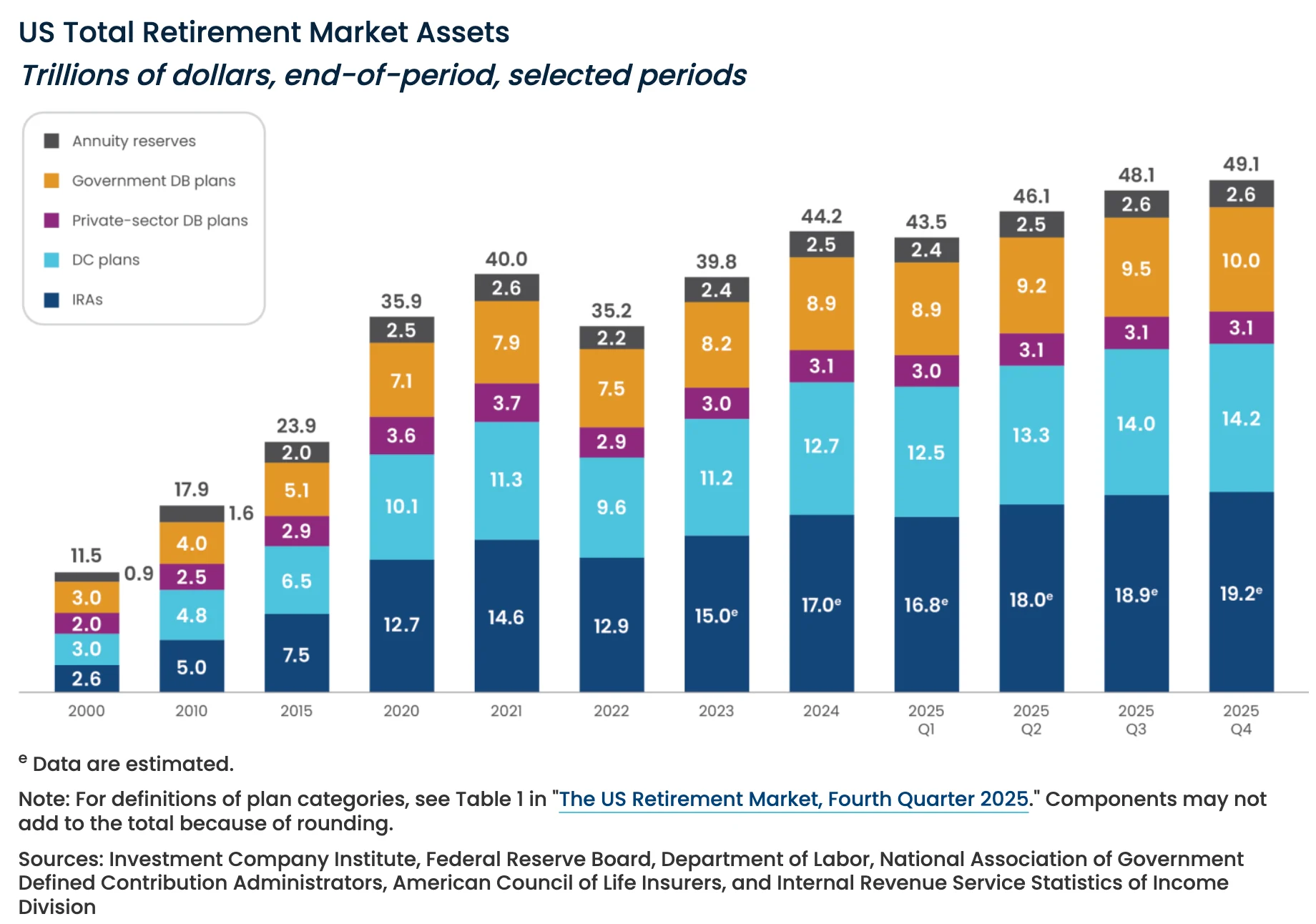

Within the American retirement system, a substantial number of 401(k), pensions, and long-term savings accounts employ passive index investment strategies. Funds typically allocate assets automatically according to index constituents and their market capitalization weights.

This strategy originated from the first index fund for ordinary investors launched by index fund pioneer John Bogle in 1976, with the core philosophy of "replicating the market rather than beating the market." With extremely low management fees and high diversification, it has become the preferred allocation method for pensions and 401(k) accounts. As of now, the total amount of American retirement assets has surpassed $49 trillion.

This means that once SpaceX is included in the index, all funds tracking these benchmarks will buy in proportionally without analyzing valuation, judging bubbles, or even caring if the company is profitable.

However, this game has sparked strong dissatisfaction within the pension system.

Recently, the American Federation of Teachers wrote to the SEC, urging stronger scrutiny of SpaceX's listing, warning that workers' lifelong savings could be controlled by a company that resembles a family business rather than a transparent public company.

Simultaneously, the three major public pension funds in the U.S., managing over $1 trillion (CalPERS, New York State, and New York City pension systems), jointly wrote to Musk, strongly opposing SpaceX's extreme governance structure, including super voting rights, a veto power over his own removal as CEO, and the right to be immune from lawsuits.

They pointed out that Musk simultaneously manages multiple companies, including SpaceX, Tesla, xAI, and Neuralink, creating immense risks due to divided attention. The letter calls for SpaceX to gradually shift towards a one share one vote system within seven years, establish a board with a majority of external shareholders, separate the roles of CEO and chairman, and eliminate Musk's self-veto power.

This modification of rules tailored for the super IPO on Wall Street is essentially tying the retirement savings of millions of Americans closely to Musk’s grand space dreams. After early investors enjoy hundredfold returns, the remaining "backstop" costs are being passed onto passive investors who are unable to make choices.

The largest "grandpa squeeze" game in history is officially kicking off in the name of indices.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。