All things can be priced.

Written by: Prathik Desai

Translated by: Luffy, Foresight News

Last week, Hyperliquid's HIP-3 market launched perpetual contracts ahead of SpaceX's IPO. The opening price was set at $150 per share, corresponding to an implied company valuation of $1.78 trillion, below its IPO target valuation of $2 trillion. Within just a few hours, market traders pushed the contract price up to $216, with the implied valuation of the company exceeding $2.5 trillion. The next day, the stock price hit $230 at one point.

At this decentralized exchange, ordinary retail investors completed the valuation pricing for Musk's rocket company; by this time, the company's stock had not yet officially listed, and the market's given valuation was already 25% higher than its IPO target.

Two days later, Polymarket partnered with the Nasdaq private market sector to launch prediction contracts regarding milestones in the development of non-public companies. Now, users can bet on various events for unlisted enterprises, including the timing of IPOs and valuations.

Viewed individually, these non-public company perpetual contracts and event contracts have limited influence. But together, the market can continuously value SpaceX and assess its listing probability. However, what is the true reference value of this pricing before the company’s stock is offered to the public?

In this article, I will break down how the cryptocurrency industry has built a parallel valuation system for non-listed companies, and what impact this system will have on related enterprises.

In the 1980s, various places in the United States emerged known as "speculator shops." On the surface, they appeared to be newly-formed stock brokerage firms. They were also equipped with automatic ticker tape machines displaying real-time stock prices and counters for customers to place orders; but in reality, they were not legal.

Nasdaq still defines “speculator shops” as illegal brokerage institutions that accept client trade orders but do not actually execute settlements.

At that time, the American working class could participate in stock betting here with extremely low margins, with the betting threshold requiring only $1. The operators of these places acted as the counterparty for all trades. If a customer was bullish on the American Steel Company's stock price and won the bet, the operator would pay out a bonus; if the stock price fell, the margin would belong to the operator. The entire process did not involve actual stock circulation and there was no equity settlement.

Regulators and mainstream financial institutions had a deep disdain for these places. Regulatory agencies believed they undermined public trust in financial markets, and various states in America gradually enacted laws to eliminate them. In 1921, New York’s “Martin Act” completely ended the “speculator shops.”

But rather ironically, the once condemned “speculator shops,” viewed as “gambling dens” and eradicated, ended up nurturing the public's enthusiasm for investing in stocks. Between 1900 and 1922, American public stock ownership soared, with initial market demand driven by gambling schemes.

Despite being non-compliant, illegal betting firms remained popular due to their total separation of equity ownership and price speculations.

A century later, the cryptocurrency industry replicated this logic, creating a brand new valuation channel for leading global private companies. But the two differ immensely in legality and transparency: traditional betting firms are completely opaque, with prices manipulated by operators, and trading partners fixed as the venue itself, only settling in cash with no traceable records; once the operator goes bankrupt, customer funds would also be lost.

On the other hand, on-chain perpetual contracts operate under completely different rules. Every transaction on Hyperliquid is recorded on the blockchain, funding rates are publicly accessible, and settlement processes are automated and verifiable. Anyone can immediately check the number of open contracts, liquidation price ranges, and counterparty risk exposure.

Like the past "speculator shops," this pricing system in the crypto world also detaches equity ownership from pricing, but replaces opaque operations with on-chain transparency.

All things can be priced

After Polymarket established cooperation with the Nasdaq private market, it launched various event contracts that cover companies like OpenAI, SpaceX, and Kraken, with transaction focuses including IPO timelines, valuation thresholds, secondary market trading dynamics, and more.

The pricing logic behind these contracts fundamentally differs from the “speculator shops” of the 19th century. Today, traditional financial institutions are actively participating and collaborating with crypto infrastructures. The ultimate settlement of Polymarket event contracts depends on actual transaction records from directed acquisitions and standardized secondary auction data initiated by companies.

For example, if a contract bets on "OpenAI's valuation surpassing $1 trillion at IPO," the final settlement will be based on real inter-institution transaction records. This also marks the first time regulated secondary market data service providers have granted exclusive pricing data for use in crypto predictive protocols.

Event contracts are merely the tip of the iceberg; they are just a part of the complete parallel valuation system that the cryptocurrency industry has built for non-listed companies. Different tools within this system can price the same enterprise from various dimensions.

Event contracts primarily assess the probability and timing of a company’s IPO; while pre-IPO perpetual contracts can continuously reflect market valuation sentiment before a company officially lists. Market makers like Trade.xyz and Ventuals have launched perpetual contracts for non-public companies such as SpaceX and Anthropic on Hyperliquid, supporting uninterrupted trading 24/7.

These contracts can instantly update company valuations, whereas in traditional models, official valuations of non-public companies are usually only updated quarterly or adjusted after financing rounds.

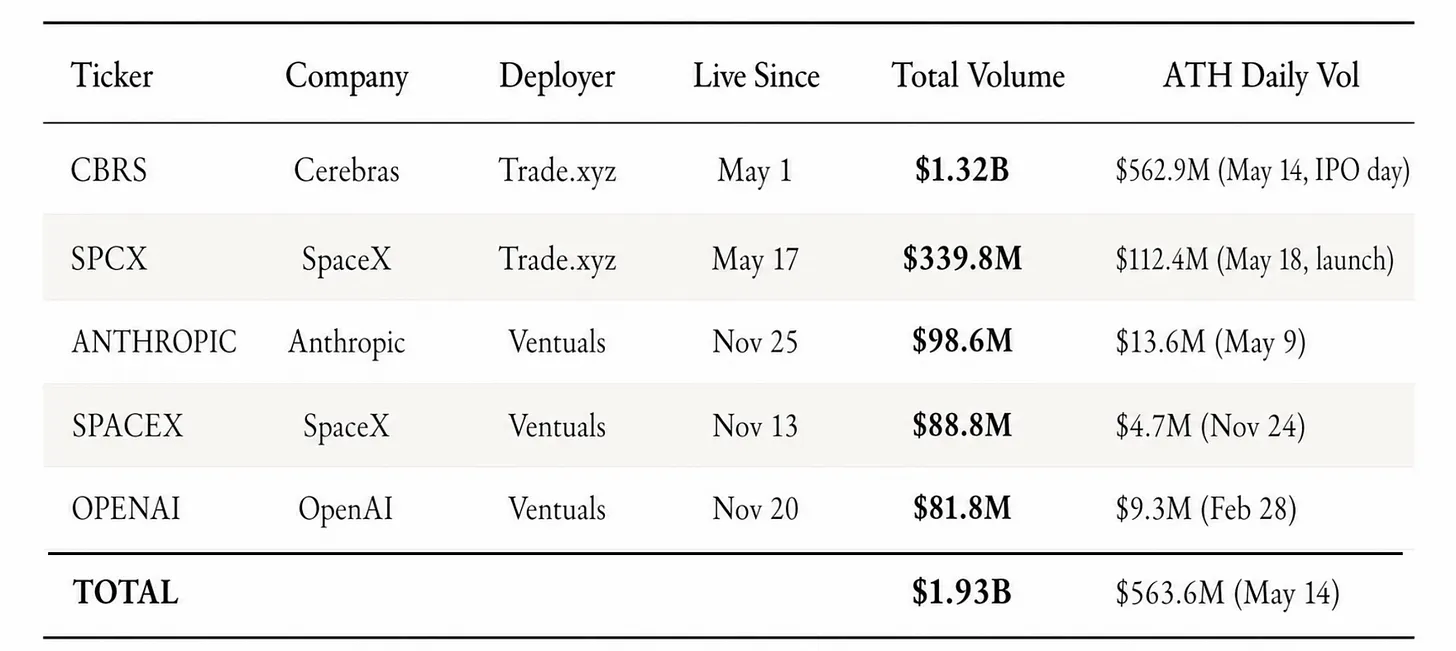

In the past six months, the cumulative transaction value for just five companies: Anthropic, SpaceX, OpenAI, and Cerebras on the Hyperliquid platform reached $1.9 billion, with over $1.6 billion in transactions in May 2026 alone.

In addition to synthetic asset pricing, this system also has a third type of product form.

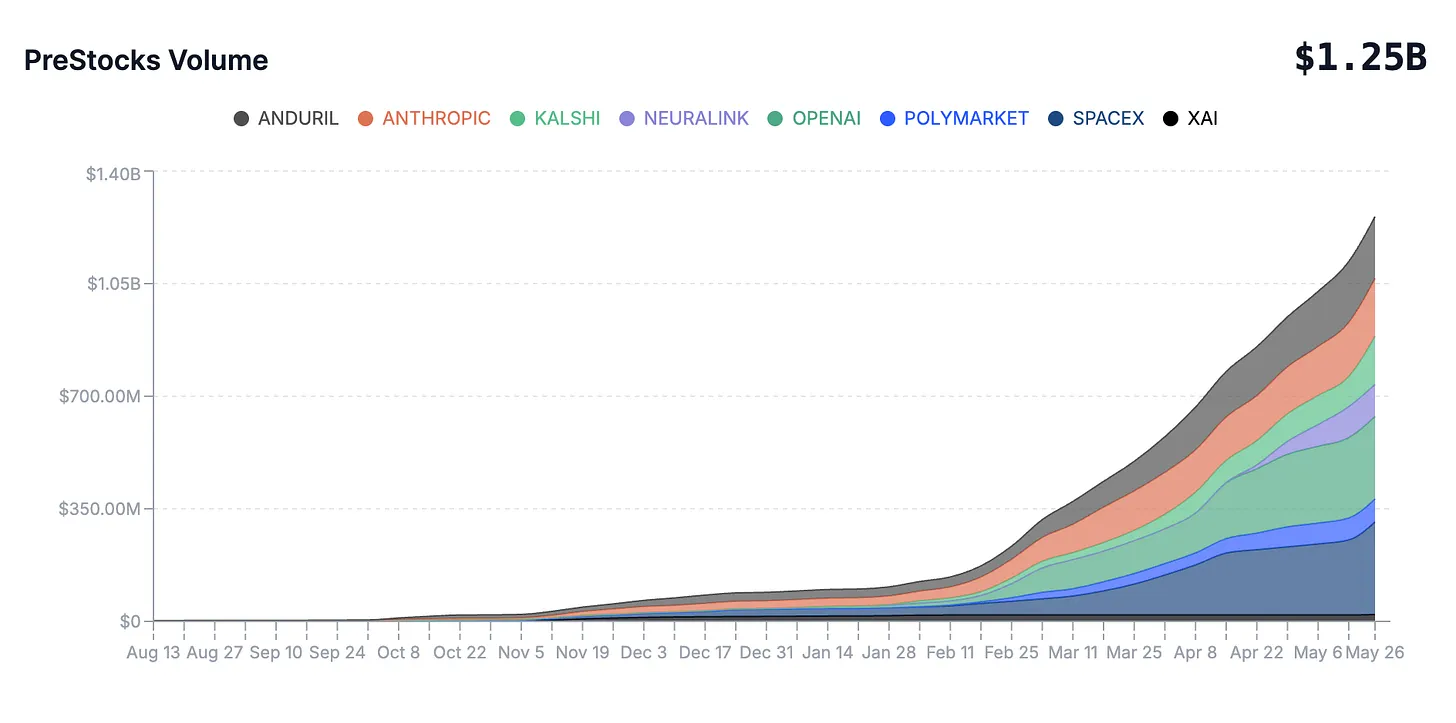

Based on the Solana public chain and invested in by Republic Capital, the PreStocks platform tokenizes the equity of non-listed companies through special purpose vehicles (SPVs), with targets including SpaceX, OpenAI, Anthropic, and more. The mainstream Solana wallet Phantom has integrated PreStocks functionality, allowing tens of millions of users to trade these equity tokens conveniently.

Unlike perpetual contracts and prediction markets, these tokens aim to allow users to gain real economic benefits corresponding to actual equity rather than merely gambling on price fluctuations.

The market demand for these assets is very robust.

From October 2025 to the end of April 2026, tokens related to Anthropic on the PreStocks platform surged by 733%, with their implied company valuation exceeding $1 trillion. Consequently, Anthropic became the third non-listed company to achieve a trillion-dollar valuation on-chain, following OpenAI and SpaceX.

During the same period, the valuation provided by the strictly regulated traditional secondary trading platform Forge Global for Anthropic was also close to $1 trillion. The convergence of valuations for the same unlisted company from a blockchain token platform and a traditional compliant equity market is noteworthy.

As of now, PreStocks has completed a cumulative total of 3.67 million transactions, with a total transaction value exceeding $1.25 billion, of which 93% of transactions occurred in 2026.

Platform data shows that more than 20,000 users currently hold token assets of non-listed companies like Anduril, Neuralink, Kalshi, and Polymarket, with a total holding value exceeding $25 million.

What is the reference value of such pricing results? Data proves that their signaling effect is quite significant.

Earlier this month, Trade.xyz launched pre-IPO perpetual contracts for Cerebras Systems. One hour before the NASDAQ opened, the price of this on-chain contract was approximately $340; the NASDAQ opening price for this stock was around $350, while the IPO issuance price was set at $185. The discrepancy between the Hyperliquid contract price and the final opening price was only 3%, while the valuation error on traditional secondary platforms reached as high as 35%.

Today, event contracts, perpetual contracts, and equity tokens issued through special purpose entities collectively form a multidimensional, comprehensive pricing system spontaneously arising from the market. Previously, such a mature pricing model only served public companies.

However, trading these types of assets also incurs related costs: Perpetual contracts have funding rates; when market bullish and bearish forces are imbalanced, one side must continuously pay the other (or vice versa). For traders who are long-term bullish and waiting for a company’s IPO, if the listing time remains uncertain, the accumulated funding rate over several weeks can become a significant expense.

Equity tokens relying on special purpose vehicles incur platform fees and also come with counterparty risks due to underlying entities. Prediction market contracts may lock user funds until event settlement.

Different products also align with different types of participants: short-term speculators are willing to bear funding rates to profit from quick price fluctuations; long-term investors with confidence in business development prefer lower-cost prediction contracts. Ultimately, the comprehensive price formed by multiple tools also reflects the diverse expectations of market participants.

Only pricing, no ownership involvement

This valuation system has a core characteristic: pricing is completely separated from equity ownership.

Users trading contracts related to the timing of OpenAI's IPO cannot enjoy profit dividends from the company; traders going long on SpaceX’s pre-IPO perpetual contracts on Hyperliquid also do not have voting rights in the enterprise.

Since equity cannot be obtained, why does the market still need such pricing tools for non-listed companies?

The patterns formed by combining event contracts, perpetual contracts, and equity tokens resemble credit default swaps (CDS) from the early 21st century in essence. Investors can express judgments on a company's credit status through credit default swaps without issuing loans to the company. Such products establish a parallel pricing system for credit risk, with market liquidity and price responsiveness often surpassing the underlying bond markets.

PreStocks tried to go further. The platform claimed that tokens issued through special purpose entities would allow holders to acquire corresponding rights through indirect shareholding. However, Anthropic officially refuted this by stating that equity transfers without board approval would not be acknowledged by the company. Following this news, related tokens experienced a one-day drop from around $1,400 to $812.

However, the market quickly repaired itself. Two weeks after the sharp decline, the token price rebounded to around $1,050. Although the legal rights issue had shaken market sentiment, participants reassessed the risk and reset their valuations.

This also reflects the differing situations of two types of traders:

An investor who bought Anthropic tokens on PreStocks at $122 in October 2025, despite facing legal turmoil, still saw a paper gain of 7 times by the end of May. However, such assets relying on special purpose vehicles generally face issues of insufficient on-chain liquidity and could encounter risks of legal statements from the company at any future moment.

If the same investor chose to trade Anthropic perpetual contracts on Hyperliquid, although they could not gain several times returns, the platform’s liquidity is fuller, allowing for opening and closing positions at any time; all position records are traceable on-chain and are not subject to the counterparty risks brought by restrictions on equity transfers.

It is evident that the market for non-listed companies is beginning to recognize the value of these new trading tools. They fill market gaps, enabling the public to express judgments on enterprises without formal transaction channels, and these products precisely address that pain point. Of course, it does not equate to direct holding of company equity.

The rationale behind the pricing system for non-listed companies

According to Polymarket, there are currently nearly 1,600 unicorn companies globally, with a total valuation exceeding $5 trillion. Companies like OpenAI and Anthropic have strong brands, scalable revenues, and massive user bases; their characteristics are no different from public companies, aside from lacking public shareholders.

Through various promotional channels, non-listed companies like SpaceX and OpenAI are already well-known to the public, and almost everyone has their judgments on their future. However, for a long time, ordinary investors could not participate in valuation and trading, leading to a significant gap between market opinions and trading channels. The comprehensive valuation system created by the cryptocurrency industry aims to fill this void.

Currently, the market still cannot achieve direct trading of non-listed company shares and instead relies on indirect equity holding vehicles, probability bets, sentiment trading, continuous valuation, and other methods for pricing.

The significance of the non-listed company pricing system has long surpassed the prediction markets and pre-IPO perpetual contracts themselves. It confirms a trend: when an asset class possesses a complete pricing ecosystem, even if traditional market systems have not followed suit, new trading models will form early.

Similar cases have already emerged. Last year, Hyperliquid launched silver perpetual contracts, and within just one month, the transaction volume for these contracts accounted for 2% of total global silver trading volume. It is noteworthy that silver has been traded on the Chicago Mercantile Exchange (COMEX) for decades, with mature institutional infrastructure, abundant liquidity, yet also faced barriers like intermediaries, high margin thresholds, fixed trading hours, and account access restrictions. Hyperliquid eliminated all friction points, allowing traders to freely price silver.

Robinhood is also developing similar models; its platform has now integrated stocks, options, crypto assets, and prediction markets. When users see Kalshi election-related contracts next to their positions in Nvidia, the prices of different targets can corroborate each other, returning a more complete market logic. The value of a single product is limited; a combined ecosystem can yield greater benefits.

This infrastructure does not develop in isolation. The potential of asset tokenization has already been proven: Kraken's xStocks product has tokenized shares of over 100 publicly traded companies, with a cumulative transaction volume reaching $25 billion and over 80,000 on-chain holders. Each token is verified 1:1 by real stocks held in custody by regulated institutions.

The success of xStocks demonstrates the feasibility of large-scale tokenization of listed company assets. If this model can be replicated in the non-listed company realm while addressing corporate authorization issues and compliantly advancing asset tokenization before IPOs, the popularity of such pricing tools will further increase.

The richer the variety of tools for pricing, the more the market comprehensive prices can reflect the information and consensus mastered by all participants. This is also the core value of the non-listed company valuation system: prediction contracts, pre-IPO perpetual contracts, special purpose entity tokens, and traditional secondary markets each interpret enterprises from different dimensions, and the combination yields effects similar to the public trading markets for listed companies.

Traditional markets establish qualified investor systems based on the logic that non-listed company situations are complex and risks are higher, with ordinary investors lacking the ability to assess. However, today, the public tracks companies like SpaceX year-round through social media and informational content, and well before they formally submit IPO prospectuses (S-1 documents), they have already participated in pricing using various tools. This old logic is no longer tenable.

When regulators shut down “speculator shops,” they only saw the speculative attributes but overlooked the real market demand behind it. People long to trade assets they cannot hold and express their judgments. Even if the venues are shut down, the demand never disappears; it merely shifts from "speculator shops" to legitimate brokers, futures markets, and now extends to blockchain.

Currently, $5 trillion worth of non-listed company assets are isolated behind qualified investor thresholds, with valuations only periodically updated by insiders and venture capital firms. Yet the dynamics and reputations of these companies are already public; establishing a mature parallel pricing system is an inevitable trend.

PreStocks attempts to bind pricing to equity ownership; Hyperliquid and Polymarket cannot provide equity, but they create high-leverage channels without access thresholds, releasing price signals.

In the future, such tools may completely change the market pricing logic for leading IPO candidates before they officially list. During the window from when a company submits its prospectus to its official listing, market sentiment and various information continuously ferment, and this system can capture changes in real-time, effectively narrowing the deviation between the estimated price in the prospectus and the final opening price.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。