Author: XinGPT

Micron surged today, one of the core reasons is that UBS raised Micron's rating valuation directly to a target price of $1635!

So I took a close look at UBS's report on the significant upgrade of Micron's rating today, the core is the change in valuation methods.

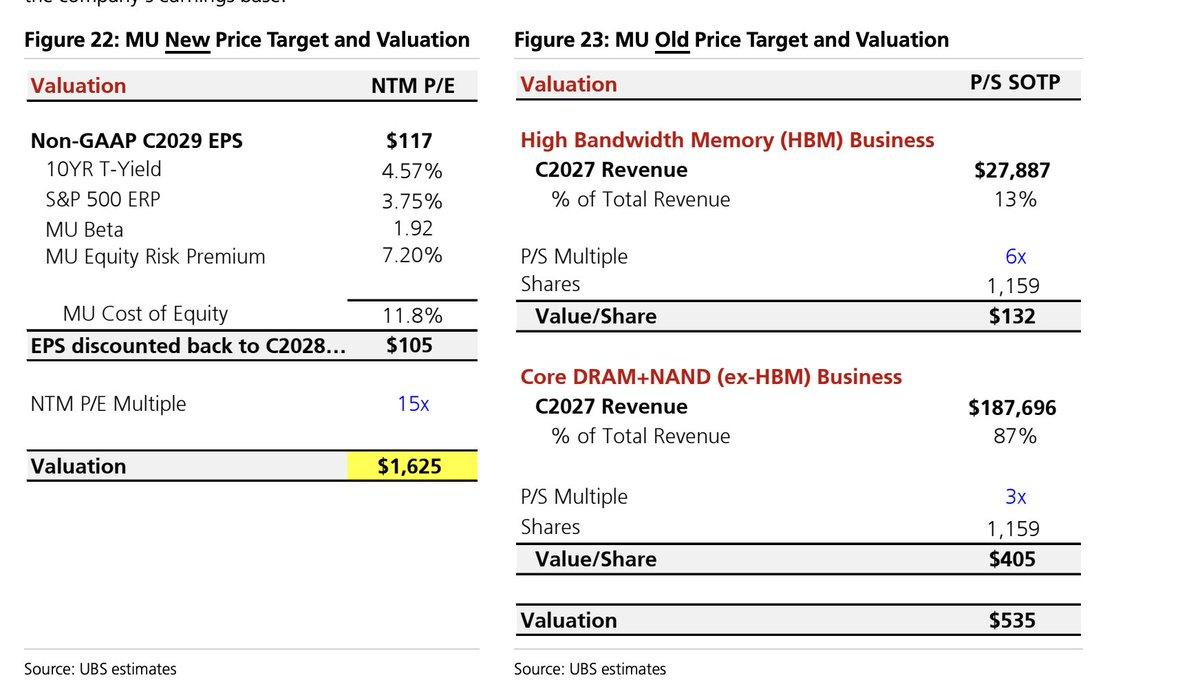

Previously, UBS valued Micron using the SoTP sum of parts approach, based on P/S multiples. It broke Micron into two segments: HBM business and core DRAM+NAND business.

- HBM benefits from AI server demand and grows faster, thus receives a higher multiple, with an estimated revenue of about $27.89 billion in 2027 and a 6x P/S valuation, corresponding to about $132 per share;

- Core DRAM+NAND is estimated at about $187.7 billion in revenue in 2027, with a 3x P/S valuation, corresponding to about $405 per share.

The sum of the two parts gives the original target price of $535. The implicit logic of this method is that Micron remains a strong cyclical storage company, but the HBM business is higher quality, hence different revenue multiples are assigned. (Figure 1)

Now UBS has switched to a holistic P/E valuation, raising the target price from $535 to $1,625. The new method uses about 15x NTM P/E, anchoring to an EPS of about $117 in 2029, and discounts this back to 2028 using an equity cost of about 12%.

UBS chose the EPS for 2029 because it believes that by then, the model will have included a round of mild storage downcycle. If Micron can still earn over $100 EPS at that time, it indicates that this is not merely peak earnings in the cycle, but closer to “cyclical earnings capability”. (Figure 2)

The core reason for the change in valuation method is LTAs, or long-term agreements.

UBS believes that this new round of enhanced LTAs not only locks in shipment volumes but also includes 3 to 5-year terms, fixed quantity commitments, and some fixed price mechanisms. It estimates that about 20% to 30% of the industry's DDR shipments in 2027 will be covered by such agreements, with Micron at about 20%, while hyperscalers have locked in about 60% to 70% of the industry Server DDR5 volume. As a result, Micron's revenue and profit visibility improve, and the peaks and troughs of DDR prices may be dampened by about half.

Therefore, UBS's judgment is that Micron is no longer just a company that profits from storage price cycles, but rather because of AI demand and long-term fixed price and quantity agreements, the stability of profits has been systematically elevated.

Thus, the valuation framework has shifted from “segment revenue multiples” to “overall earnings multiples”. The core change is from “individual HBM revaluation” to “overall revaluation of Micron”.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。