As the focus on AI relaxes, overlooked assets such as healthcare, European defense, and Asian financial stocks come back into view.

Written by: Zhao Ying

Source: Wall Street Insights

With momentum trading experiencing the largest consecutive drawdown since 2022, the market's heavy focus on AI themes is facing reevaluation. Louis Miller, head of Goldman Sachs' global custom stock basket business, believes that investors are showing a stronger willingness to diversify, and the contours of "post-war trading" are gradually becoming clearer.

The two and a half days of momentum selling that began last Friday marked a turning point in market sentiment. Miller noted that beyond core AI assets, oversold consumer sectors, overlooked healthcare, and financial and defense sectors benefiting from the interest rate environment and geopolitical easing are becoming new focal points for capital.

At the same time, the continued high interest rate environment has introduced new risks. Miller warned that if U.S. Treasury yields do not fall back to "pre-war" levels, low-quality stock baskets could face more than a 20% relative downside, and the fragility of unprofitable tech stocks should not be overlooked.

Momentum trading suffers significant setback, diversification window opens

According to data from Goldman Sachs' FICC and equities departments, the momentum drawdown that started last Friday is the largest consecutive momentum decline since 2022. Miller characterizes this as a signal of investors' "increased willingness to diversify," rather than a mere technical adjustment.

Throughout the "wartime" phase, Goldman Sachs' bottleneck basket (GSCBBOTL) has been the preferred alternative beyond core AI assets. Miller indicated that the market's definition of AI is extending beyond semiconductors and hyperscale cloud providers to a broader range of sectors, with investors beginning to seek AI exposure outside the U.S.

Asian AI trades have performed strongly this year, but last week's momentum selling created rare buying opportunities in some themes. Goldman Sachs' Asian AI bottleneck basket (GSXABOTL) experienced a correction of about 3% in the past week. Miller believes that this basket focuses on the most strained supply segments of AI infrastructure, which possess high allocation value.

In a high interest rate environment, low-quality stock risks become prominent

Miller clearly indicates that if interest rates remain elevated for a prolonged period, certain overvalued sectors will face significant pressure. Goldman Sachs' low-quality stock basket (GSXULOWQ) consolidates multiple theme baskets with low-quality characteristics, covering unprofitable tech stocks, low-profit small-cap stocks, and companies sensitive to high-yield debt.

Data shows that despite a significant rise in U.S. 10-year Treasury yields, the performance of GSXULOWQ has been relatively resilient. However, Miller warns that if yields do not fall back to pre-war levels, this basket could face a relative downside of more than 20%.

In the selection of interest rate-sensitive hedging tools, Goldman Sachs’ unprofitable tech basket (GSX1NPTC) has remained one of the most popular options. However, Miller prefers the newly launched unprofitable non-tech basket (GSCBNOPS), which excludes names driven strongly by market sentiment such as space, satellites, and quantum computing, making it a more precise short for interest rate sensitivity.

Healthcare: Compounding assets with low correlation to AI

The healthcare sector has long underperformed cyclical stocks, lacking major catalysts, and has faded from market focus. However, Miller believes that this sector is a compounding asset negatively correlated with AI trends—performing steadily during AI sell-offs and is also a beneficiary of AI applications (such as drug development and hospital capital expenditures).

Goldman Sachs data shows that the excess correlation of various subsectors of U.S. healthcare to AI is generally negative. Specifically, Miller is optimistic about the biotech sector, as the upcoming pharmaceutical patent cliff will drive M&A activity, making Goldman Sachs' biotech strategic M&A basket attractive in this context. The life sciences tools sector is expected to benefit from the recovery of end markets, while the growth in biopharmaceuticals will drive the overall pharmaceutical supply chain upward.

Financial stocks outside the U.S.: Dual beneficiaries of interest rates and post-war cycles

Miller states that interest rate-sensitive financial stocks will benefit from both the high interest rate environment and the cyclical recovery following the end of the war. Although U.S. financial stocks may not face short-term performance issues, given the uncertainties surrounding midterm elections this year, he currently favors financial exposure outside the U.S.

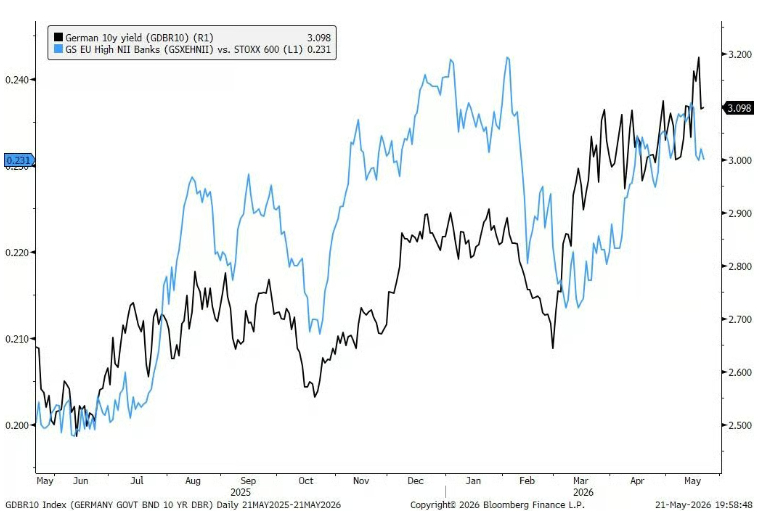

In Europe, Goldman Sachs' high net interest income basket (GSXEHNII) focuses on banks with the most profitable leverage to interest rates. The Greek bank basket (GSXEGRBK) also meets high net interest income standards and additionally possesses robust loan growth and valuation advantages compared to European peers.

In Asia, Japanese bank trades (GSXAJMEB) have a logical configuration ahead of next month's Bank of Japan meeting, with the latest statements from the Bank of Japan leaning towards continued rate hikes.

European defense: Reentry opportunities after valuation reset

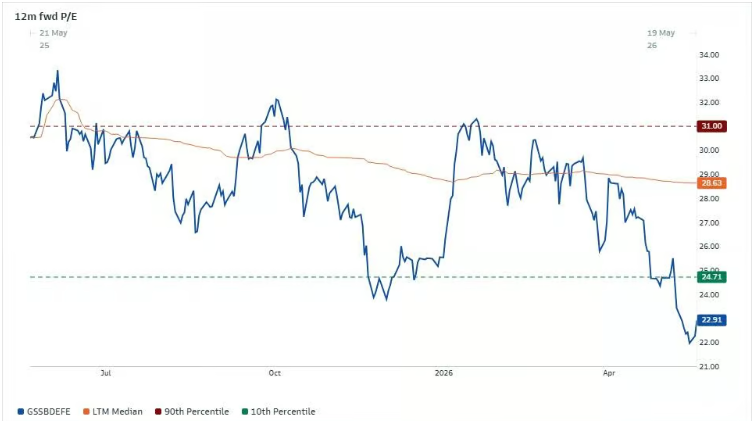

Global defense spending continues to rise, and the European Satory defense exhibition and NATO summit in June and July will bring intense catalysts. Miller points out that after significant valuation compression and position clearing since the beginning of the year, European defense trades (GSSBDEFE) are returning, with at least a 10% repair space remaining between their year-to-date price performance and earnings adjustments per share.

From a valuation perspective, if the European defense sector returns to last year's median valuation multiple, it implies over 20% upside potential (current P/E ratio is about 23 times versus last year's 29 times). Miller notes that although the market generally believes European defense is less high-tech compared to the U.S. and Asia, small and mid-cap sectors can gain a purer "new defense" exposure through Goldman Sachs' new defense basket (GSXENDEF).

U.S. defense trades (GSXUDFNS) have also seen a decrease in valuations, with prior sell-offs primarily driven by beta, and post-war inventory replenishment expected to lead to upward revisions in earnings expectations.

Three major "post-war scenario" trades: Options structure captures binary inflection points

Miller has also designed three specific trades for the "post-war" scenario.

The first is low momentum squeeze trades. Currently, U.S. momentum and AI trades are highly synonymous; if substantial downgrade catalysts occur, there may be a short squeeze on low momentum baskets (GSXULMOM). In the consumer sector, Miller recommends expressing upside exposure through options: the cost of a July 2026 call spread option for the consumer discretionary basket (GSXUCOND) at 110/120% is 1.07%, with a maximum payout ratio of 9.3 times; the 108/118% call spread option for the low-end consumer basket (GSXULOWD) costs 1.28%, with a maximum payout ratio of 7.8 times.

The second is a dual binary option on gold against oil. In a post-war scenario, gold miners and buyers are naturally shorting oil, and potential sovereign wealth fund custody arrangements may suppress the dollar. The cost of a September 2026 dual binary option—gold ETF (GLD) above 107.5% and oil prices between $75 and $90—is currently about 12%.

The third is a stock-bond dual hedge. Miller points out that a decline in AI enthusiasm could drag down the overall market, as AI has contributed approximately 6 percentage points to the S&P 500 index returns over the past six months. Goldman Sachs' volatility structured team believes that the combination scenario of the end of war combined with cooling AI enthusiasm may result in a 3% decline in the S&P 500 index and a 30 basis point decline in 10-year yields. The corresponding September 2026 dual binary option—S&P 500 below 97% and 10-year SOFR below the forward rate by 30 basis points—costs 8.0%. Miller also specifically noted that current market attention is focused on inflation risks, which means that the cost of hedging growth risks is relatively cheap.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。