You might think you are buying Nvidia or Tesla, but you may only be buying a "price promise."

Written by: Conflux

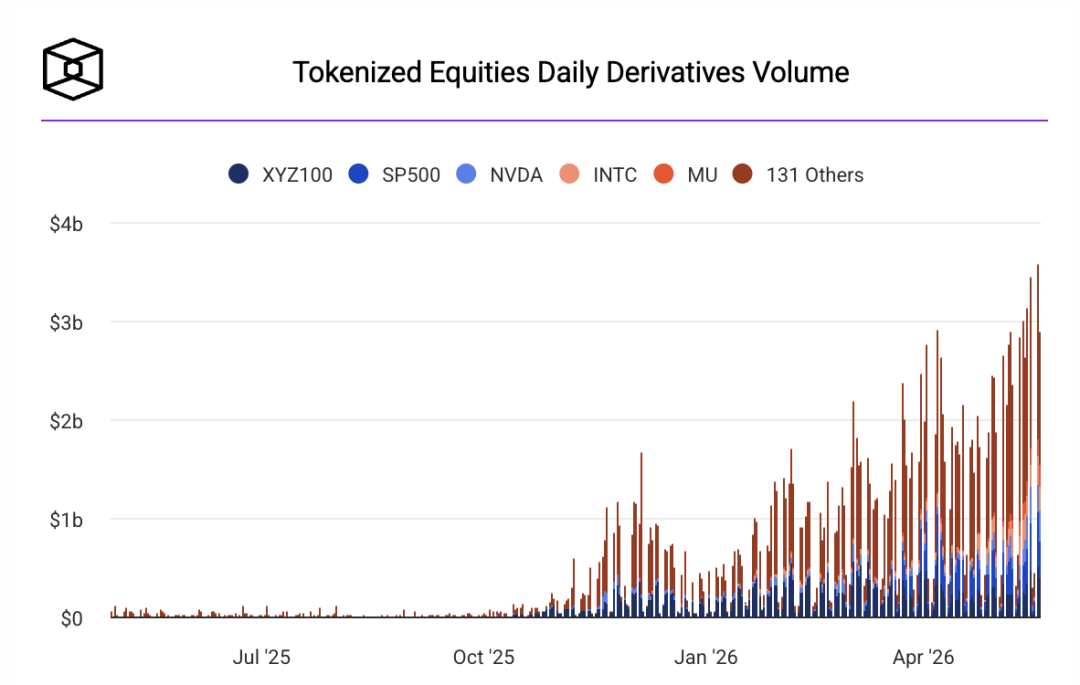

On May 18, the daily trading volume of tokenized stocks surged to $3.57 billion, setting a historic high.

This number was quickly shared.

However, more critically: You might think you are buying Nvidia or Tesla, but you may only be buying a "price promise."

The true sense of "US stocks on-chain"—complete ownership, voting rights, and dividend rights of stocks entering the on-chain system—has only just begun to be seriously promoted by Wall Street.

These two things are not the same.

In the past two years: The on-chain world has solved "how to buy"

In the past two years, on-chain finance has indeed gotten one thing right: making it easier for users to gain exposure to asset prices.

Users can:

- Trade US stock-like Tokens 7 × 24 hours

- Settle using stablecoins

- Achieve lower barriers to obtaining price fluctuation returns on US stock assets

But these changes are all focused on the same level: the trading method has been restructured, but the asset rights have not been restructured.

What you gain is "price exposure," not "asset ownership."

The real question lies in the rights layer—what legal rights correspond to the Token you hold on-chain?

This is the most important and easily overlooked issue behind today’s $3.57 billion.

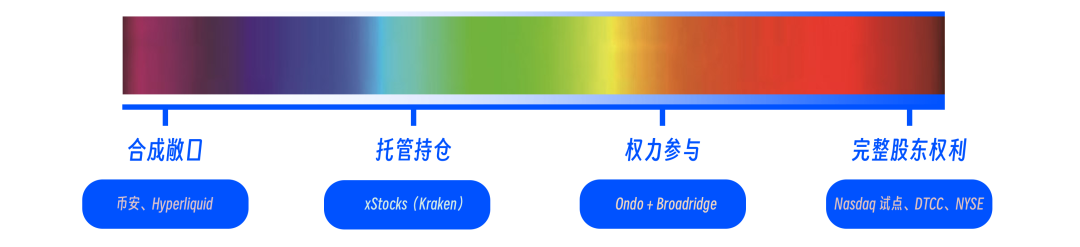

The spectrum structure of tokenized stocks

"Tokenized stocks" are not a single product but a gradually progressive structural spectrum. From left to right, the rights gradually become complete, but compliance and institutional costs also gradually rise.

First layer: Synthetic price exposure (shadow assets)

This layer is the most mainstream form currently. The Token you hold is essentially just a price tracking tool.

The underlying typically maintains price anchoring through delta hedging, market maker risk management, partial collateralization with real stocks, and over-the-counter contracts.

But the key point is that what you receive is not an asset but a price result. The risk does not lie in the stock but in the platform's credit.

Second layer: Custodial holding structure (limited rights mapping)

This layer begins to show real stock custody.

Typically achieved through SPV or custodial structures, allowing for 1:1 asset holdings while attempting to isolate user assets. Compared to the first layer, this is a qualitative change:

- The underlying asset genuinely exists

- The structure is closer to "asset mapping"

But the problem still exists; you are still not a shareholder.

Voting rights and governance rights usually do not rest in the hands of the users. Dividends are also often "redistributed" through on-chain mechanisms rather than executed by the traditional securities system.

Essentially, this is an economic rights mapping, not a legal rights mapping.

Third layer: Rights interface layer (proxy voting begins to appear)

This layer begins to touch on "rights."

Some projects begin to connect with traditional financial infrastructures (such as Ondo and financial services giant Broadridge's collaboration), enabling on-chain users to:

- View company governance information

- Receive shareholder documents

- Express opinions on voting matters

It seems closer to "shareholders," but the key difference is: you are participating in the process, not owning legal voting rights. The actual voting rights may still be executed by an intermediate structure.

The essence of this layer is that rights become visible but not executable.

Fourth layer: Settlement layer tokenization (pilot phase)

This layer is the true meaning of "complete stock on-chain." Core features include:

- Dividends, distributions, and voting are executed at a unified settlement layer

- On-chain records gradually align with legal registrations

- Clearing is completed by regulated financial infrastructures

Driving this layer are no longer crypto-native projects but clearing houses, exchange systems, traditional brokerages, and investment bank networks.

What they are doing is not issuing Tokens but rather: rewriting the underlying settlement system of the securities market.

Why is this completely different from FTX?

Many people might compare this round with FTX's tokenized stock attempt in 2021.

But the essence is completely different.

In 2021, FTX did something similar. They launched about 55 tokenized versions of stocks on the Solana chain, covering Tesla, Google, Nvidia, and others. The products supported fragmented trading and could also be used as collateral.

But it had two fatal flaws: no real shareholder rights and no SEC securities registration. Thus, it was essentially more like a "on-chain price mapping product," rather than a truly foundational securities infrastructure.

And the key to this round of change is: the participants have changed. Now entering the system are DTCC, the New York Stock Exchange, Nasdaq, Morgan Stanley, and the SEC. What they are doing is very clear—digitizing the underlying infrastructure of the securities market.

Real change: from "trading on-chain" to "rights on-chain"

In the past two years, the on-chain world has solved "how to trade asset prices"; now it begins to face: "how to define asset rights themselves."

The difficulty of this step does not lie in technology but in institutions, including:

- How shareholder identities are mapped

- How voting rights are executed

- How dividends are automated

- How cross-border regulations are coordinated

The question has shifted from "Can it be done?" to whether the existing financial order will be rewritten.

Three core questions in the end

If we compress the entire tokenized stock system to its core, there are only three questions left:

First, can an on-chain address become a legal shareholder identity?

Second, can dividends, voting, and distributions be automatically executed on-chain and recognized by law?

Third, can the cross-border regulatory and clearing systems operate in sync with the on-chain system?

Conclusion

$3.57 billion is neither the endpoint nor the climax.

It is more like a signal—previous tokenized stocks merely changed the "trading method."

What is beginning to happen now is a deeper structural migration. The "rights system" of the global securities market is being reassembled and is attempting to be remapped on-chain.

If this process continues to advance, the change will not only be whether you can buy Nvidia but how the global capital market is defined.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。