Elon Musk nurtures AI with satellites.

Written by: Bao Yilong

Source: Wall Street Journal

Core Summary

1. Starlink is a true cash cow. In 2025, the Connectivity segment (led by Starlink) is expected to generate $11.39 billion in revenue, up 50% year-over-year; operating profit is $4.42 billion, with a profit margin of 39%; the segment's Adjusted EBITDA will reach $7.17 billion, with an EBITDA margin of 63%. As of March 2026, the global user base surpassed 10.3 million, covering 164 countries.

2. xAI represents the greatest uncertainty. The xAI, which integrated into SpaceX in February 2026, recorded an operating loss of $6.36 billion for the whole year of 2025, accounting for the vast majority of the company's overall losses; Q1 2026 capital expenditures reached $7.7 billion for the quarter (three times year-over-year), with an annualized consumption exceeding $30 billion.

3. The financial structure is highly imbalanced. In 2025, the company incurred a consolidated net loss of $4.94 billion, and in Q1 2026, the net loss was $4.28 billion, with quarterly losses almost equal to last year's total. Anthropic signed a computing power procurement agreement worth $1.25 billion per month (approximately $40 billion total), but either party can cancel the contract with 90 days notice.

4. Musk has absolute control. Through Class B shares (10 votes per share), Musk will maintain 85.1% of the combined voting power after the IPO, and the company is classified as a Controlled Company, exempting it from certain Nasdaq governance requirements, making it virtually impossible for retail investors to influence company decisions.

5. The Space segment is facing strategic transformation pains. The launch business achieved over 80% global market share in 2025, but R&D expenditures for Starship have totaled over $15 billion. The Space segment incurred an operating loss of $660 million in 2025, with R&D expenditures of $3 billion, both significantly higher than the previous year. Starship is expected to conduct its first commercial flight in the second half of 2026, serving as the core infrastructure for the next stage of expansion for the company's three main businesses.

6. Valuation controversies are significant. The target valuation of $17.5 trillion corresponds to a 9.4 times price-to-sales ratio for 2025 revenue, while renowned valuation scholar Aswath Damodaran's discounted cash flow analysis yields a valuation of about $12.2 trillion, 30% lower than the IPO price. However, market enthusiasm is high, and this IPO is expected to become the largest IPO in US stock market history.

Overall Judgment

SpaceX's prospectus essentially tells the story of a trilemma: the company possesses the world's strongest space infrastructure (launching + satellite internet), the fastest-growing satellite internet (Starlink), and an expensive and uncertain AI transformation (xAI).

The three are not naturally integrated, but rather the result of Musk’s forceful merger through an all-stock acquisition.

From a financial perspective, Starlink's profitability is beyond doubt, with a 63% segment EBITDA margin, ranking among the top in global tech companies.

However, this lighthouse is obscured by the black hole of xAI. In 2025, the AI segment burned through $12.7 billion in capital expenditures, consuming most of the company's cash flow, and Q1 2026 saw a net cash outflow of nearly $9 billion.

Investors buying into SpaceX are essentially betting on an unfalsifiable vision: orbital AI computing power, Starship commercialization, and Musk's personal charisma, not merely the real profitability of satellite internet.

The biggest issue with this IPO may not be valuation, but rather information asymmetry:

- The draft prospectus disclosed that data center construction costs were significantly below the industry benchmark, but specific numbers were removed in the final version;

- A $1.25 billion monthly deal with Anthropic carries a 90-day cancellation clause and cannot be regarded as guaranteed revenue.

When core competitive advantage data is actively deleted and the largest client contract can be terminated with 90 days' notice, what are investors really paying for? This is the question that IPO investors need answered most.

The Eve of the Largest IPO in History

On May 20, 2026, Space Exploration Technologies Corp. submitted its S-1 prospectus to the U.S. Securities and Exchange Commission (SEC), under the ticker SPCX, planning to list on Nasdaq.

This 280-page document presents the financial picture of this private company, which has rejected going public for 24 years, to the public for the first time.

At the reported target valuation of $17.5 trillion, SpaceX would surpass Saudi Aramco's $17 trillion valuation in 2019, becoming one of the largest stock issuances in human history.

The underwriter list includes almost all top Wall Street institutions: Goldman Sachs leading, followed by Morgan Stanley, Bank of America, Citigroup, and JPMorgan, with a total of 20 joint bookrunners, opening subscription channels to retail platforms like Robinhood and Fidelity.

The roadshow is scheduled to start on June 4, with pricing on June 11 and listing on June 12. Musk has arranged a precise countdown for this cosmic IPO. But investors must first penetrate that 280 pages of text to answer a core question: what exactly is this company?

SpaceX categorizes its business into three segments: Space / Connectivity / AI.

This structure itself signals that this is no longer just a rocket company, nor merely a satellite internet company—it is trying to become a vertically integrated empire spanning space, communication, and artificial intelligence.

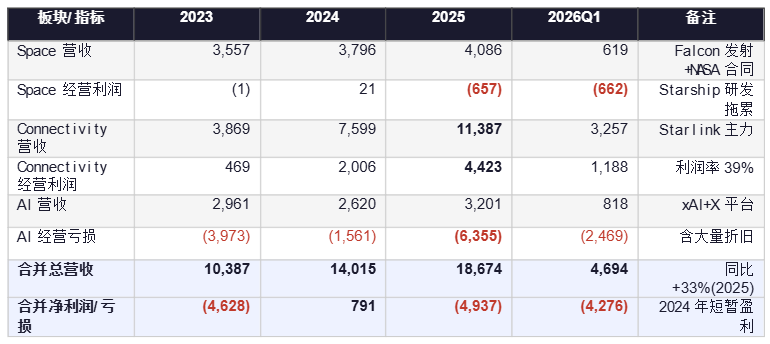

【Chart 1: Revenue and Operating Profit of Three Segments (2023–2026Q1, million USD)】

Source: SpaceX S-1 prospectus, May 20, 2026. AI segment data is compiled from the historical financial data of xAI and the X platform starting from 2023.

Source: SpaceX S-1 prospectus, May 20, 2026. AI segment data is compiled from the historical financial data of xAI and the X platform starting from 2023.

From the three-year data, a clear storyline emerges: in 2023, the company was mired in losses (including Twitter impairment), in 2024, prior to integrating xAI, it achieved profitability, while in Q1 2026, it incurred a quarterly loss of $4.3 billion, almost equivalent to the entire loss for 2025. The rapidly expanding AI business is pushing the company onto a distinctly different financial track.

Starlink: How Much Can This Money-Making Machine Print?

Starlink is the clearest and most convincing asset in SpaceX's prospectus.

In 2025, the Connectivity segment (primarily Starlink) achieved $11.39 billion in revenue, up 50% year-over-year; operating profit reached $4.42 billion, a 120% increase year-over-year; the segment's EBITDA soared to $7.17 billion, with an EBITDA margin of 63%, exceeding most internet platforms.

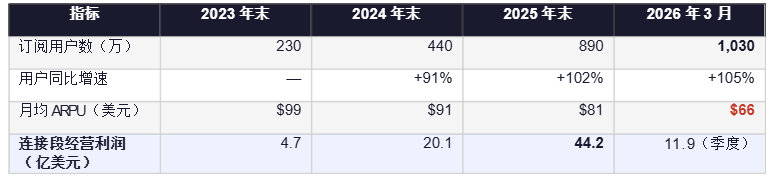

User growth has also been rapid: 2.3 million by the end of 2023, 4.4 million by the end of 2024, 8.9 million by the end of 2025, and by March 31, 2026, surpassed 10.3 million, with a year-over-year growth rate of 105%. The service covers 164 countries and regions, reaching a potential user base of 3.3 billion.

【Chart 2: Starlink User Numbers and Monthly Average ARPU Trends (2023–2026Q1)】

Source: SpaceX S-1 prospectus. ARPU is the average revenue per user per subscription service line per month.

Source: SpaceX S-1 prospectus. ARPU is the average revenue per user per subscription service line per month.

However, one number is worth noting: monthly average ARPU has continuously declined from $99 in 2023 to $66 in Q1 2026, a 33% decrease over three years.

This decline is driven by the dilution brought by Starlink's international expansion, as users from low- to middle-income countries possess less purchasing power, and lower-priced packages inevitably press down the average price. The company explains this is a strategic choice, compensating for single-user revenue declines through greater user numbers.

This logic currently holds: user numbers have increased 4.5 times, offsetting the decline in ARPU, and total revenue still maintains a 50% growth rate. However, whether the ARPU decline has reached its bottom is a core variable in Starlink's long-term model. The prospectus does not provide expectations for the bottom.

Another key catalyst is the next-generation V3 satellites. Deployment is expected to start in the second half of 2026 via Starship, with a single satellite capacity of 1 Tbps, 20 times that of the existing V2 Mini satellites.

By then, network quality will experience a qualitative leap, potentially supporting higher pricing tiers. This is the most crucial technological upgrade point in Starlink's long-term story.

xAI: The Most Expensive AI Bet in History

On February 2, 2026, SpaceX completed an all-stock acquisition of xAI.

This transaction transformed Musk from a rocket builder into an AI developer and shifted SpaceX from a satellite internet company with predictable profits to a cash-burning machine entrenched in the AI arms race.

xAI's core is the Grok large model and the X social platform.

Grok has iterated to version Grok-4.3, achieving frontier levels on the GPQA Diamond scientific reasoning benchmark; the X platform has approximately 550 million monthly active users, with about 117 million using Grok's AI features and around 6.3 million paying users.

The problem lies in scale and costs.

To train and reason with Grok, SpaceX has built supercomputing clusters codenamed Colossus and Colossus II in Texas.

The former consists of about 100,000 H100 chips, while the latter features around 220,000 GB200/GB300 chips, with a total computing power of about 1 GW (gigawatt). This is one of the largest single AI computing clusters on Earth today.

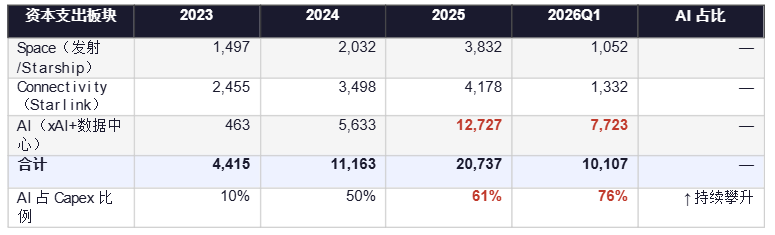

【Chart 3: Breakdown of Capital Expenditure Structure (2023–2026Q1, million USD)】

Source: SpaceX S-1 prospectus. AI capital expenditure in Q1 2026 reached $7.7 billion, nearly threefold year-over-year growth.

Source: SpaceX S-1 prospectus. AI capital expenditure in Q1 2026 reached $7.7 billion, nearly threefold year-over-year growth.

The data speaks volumes: out of $10.7 billion in capital expenditures in Q1 2026, $7.7 billion flowed to AI, accounting for 76%. Most of the money earned by Starlink has gone into the black hole of computing power.

Currently, xAI's largest external customer is Anthropic.

The two signed an agreement in May 2026, where Anthropic committed to paying SpaceX $1.25 billion per month for access to Colossus/Colossus II, with a total contract value of about $40 billion, valid until May 2029.

This is currently one of xAI's biggest sources of revenue, supporting the AI segment's revenue expectations for 2026.

However, an investigation by The Information revealed a critical risk: either party to the agreement can give a 90-day notice to cancel, which is an extremely unusual contract term. A $40 billion contract could evaporate within 90 days.

An additional narrative for xAI is orbital AI computing power. Musk envisions using solar energy to operate AI computing power in orbit at a cost lower than that on the ground.

Yet, the S-1 prospectus explicitly states: we have not, and no one else has, previously operated or attempted to operate orbital AI compute.

While the company promotes a disruptive vision, it is simultaneously constructing massive gas turbine-powered data centers on the ground.

What’s more striking is that the draft prospectus once revealed that the construction cost of SpaceX's data centers was only $2.7 million per megawatt (industry benchmark is about $12.3 million per megawatt), but this number was removed in the final version, leaving only the wording "considerably lower than industry benchmarks."

This means potential investors cannot verify the company's core claim of cost competitiveness.

Space: The Growth Bottleneck of a Monopoly

Among the three segments, the Space segment is the most underestimated and misunderstood.

It contributes about 22% of the company's revenue in 2025, but because of Starship's high annual development expenses of $3 billion, this segment incurred an operating loss of $660 million in 2025.

The launch monopoly of Falcon 9 is beyond question.

In 2025, SpaceX completed 165 orbital launches, capturing over 80% of the global market share, with a success rate of over 99%, including 122 internal Starlink launches and 43 for external commercial/government clients.

Major competitors Blue Origin and ULA collectively hold less than 20% market share.

However, the ceiling in the space launch market is becoming apparent: in 2025, the Space segment's revenue grew only 7.6% year-over-year, far below Connectivity's 50%. External launch orders amounted to 43, a slight decline from 45 in 2024. The launch services business is already fairly mature, and true incremental revenue comes from Starship commercialization.

The milestone of Starship is the foundation of all of SpaceX's commercial logic.

Only with Starship achieving large-scale reusable launches can the deployment of the V3 satellites (60 per launch) occur, accelerating the coverage expansion of Starlink; SpaceX can also realize its long-term vision of orbital AI computing power satellites.

As of the prospectus disclosure, Starship has completed 11 flight tests, and the company expects commercialization to begin in the second half of 2026—this is the most crucial near-term catalyst for this IPO.

Behind 85% Voting Power: The Governance Logic of the Musk Empire

The SpaceX prospectus reveals a meticulously designed dual-class stock structure: Class A shares carry 1 vote per share (issued in this IPO), while Class B shares carry 10 votes per share (held by Musk).

Before the IPO, Musk held approximately 5.6 billion Class B shares (93.6% of Class B), and combined with his holdings of Class A shares, his combined voting power reaches 85.1%—surpassing the control ratio of any founder of a major publicly-listed company in the U.S.

WSJ reports that this structure makes it nearly impossible for investors to oust Musk. The company will list on Nasdaq as a Controlled Company, exempting it from governance rules requiring a majority of independent directors. Musk concurrently serves as CEO, CTO, and chairman of the board.

What’s also noteworthy is Musk's compensation package design: Musk's cash salary in 2025 is only $54,000, but he holds a set of stock options with extremely aggressive terms.

Among them, the condition for exercising 1 billion Class B shares is the establishment of a permanent colony on Mars with a population of 1 million and a company market value of $7.5 trillion. The existence of such stock packages makes future potential dilution challenging to predict.

Meanwhile, the prospectus also reveals large-scale related party transactions between SpaceX and Musk's other companies for the first time: in 2025, the company purchased $131 million worth of Cybertrucks and $506 million of Megapacks from Tesla; xAI had previously paid Tesla various fees totaling $731 million.

Tesla is mentioned 87 times in the prospectus—this number indicates the degree of internal connections within Musk's empire.

Is $17.5 Trillion Worth It? Divergence Between Market and Academia

At a valuation of $17.5 trillion, SpaceX's price-to-sales ratio is about 9.4 times (corresponding to $18.67 billion in revenue for 2025).

By comparison, mainstream cloud computing businesses like Amazon AWS and Microsoft Azure have price-to-sales ratios of about 12-15 times, but they are already mature, profitable businesses.

Renowned valuation scholar and NYU finance professor Aswath Damodaran's discounted cash flow analysis arrives at a valuation of about $12.2 trillion, which is about 30% lower than the target IPO valuation.

Damodaran believes the current valuation is entirely based on trust in Musk himself.

However, the market clearly disagrees. Public information shows that SpaceX's valuation in the private secondary market has been adjusted upward many times over the past year, and the IPO book is attracting significant institutional demand.

The phenomenon known as FOMO premium (fear of missing out premium) is driving pricing logic—not because DCF analysis suggests one should buy, but because no one dares to say they don't own SpaceX.

It's noteworthy that data from the past 10 years does support caution: PitchBook research analyst Franco Granda points out that historically, extremely large IPOs generally underperform the market post-listing.

But SpaceX's uniqueness lies in its status as the only strong player in two markets, being both the monopolist in launch services and the leader in satellite internet. This scarcity itself warrants a premium.

Three Forward-Looking Signals

Based on the prospectus and external information, investors need to track the following three key signals:

- The commercialization timeline for Starship: The first orbital payload delivery in the second half of 2026 is the most critical point for validating the company's narrative logic. Any delays will push back the V3 satellite deployment plan and the orbital AI computing timeline, necessitating a reassessment of growth expectations across the company's three business segments.

- Renewal or replacement of the Anthropic contract: The $1.25 billion/month deal expires in May 2029 and has a 90-day cancellation clause. If Anthropic shifts to self-built computing power before the contract expiration (a common trend in the industry), revenue forecasts for the xAI segment will face significant pressure.

- Confirmation of the bottom for Starlink ARPU: Monthly average ARPU has dropped from $99 to $66. If it further declines below $50 within 2026, it would indicate that the international dilution effect outweighs the compensation from scale growth, putting profitability of the Connectivity segment under pressure.

Conclusion: Are You Buying The Company or Musk?

SpaceX's prospectus ultimately presents a paradox: Starlink is currently one of the fastest-growing and most profitable broadband services known in human history.

However, xAI is a capital-consuming gamble akin to constructing a nuclear power plant, and its core customer contracts can be canceled within 90 days, with core competitive advantage data actively deleted from the prospectus.

Traditional financial analysis frameworks fail here.

Valuation analysts say $12.2 trillion, but the market gives $17.5 trillion, and some even claim $20 trillion. This is not a financial issue, this is a faith issue—do you believe Musk can simultaneously achieve Starship commercialization, global satellite direct connection to mobile phones, orbital AI computing power, and Mars colonization?

Historically, every great tech company IPO has its skeptics claiming valuations are too high, and many end up regretting not buying.

SpaceX's challenge is not whether it can succeed, but rather: when you enter at a price of $17.5 trillion, how much do you need it to succeed to avoid losses? That answer is not provided in the prospectus.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。