Key Takeaways:

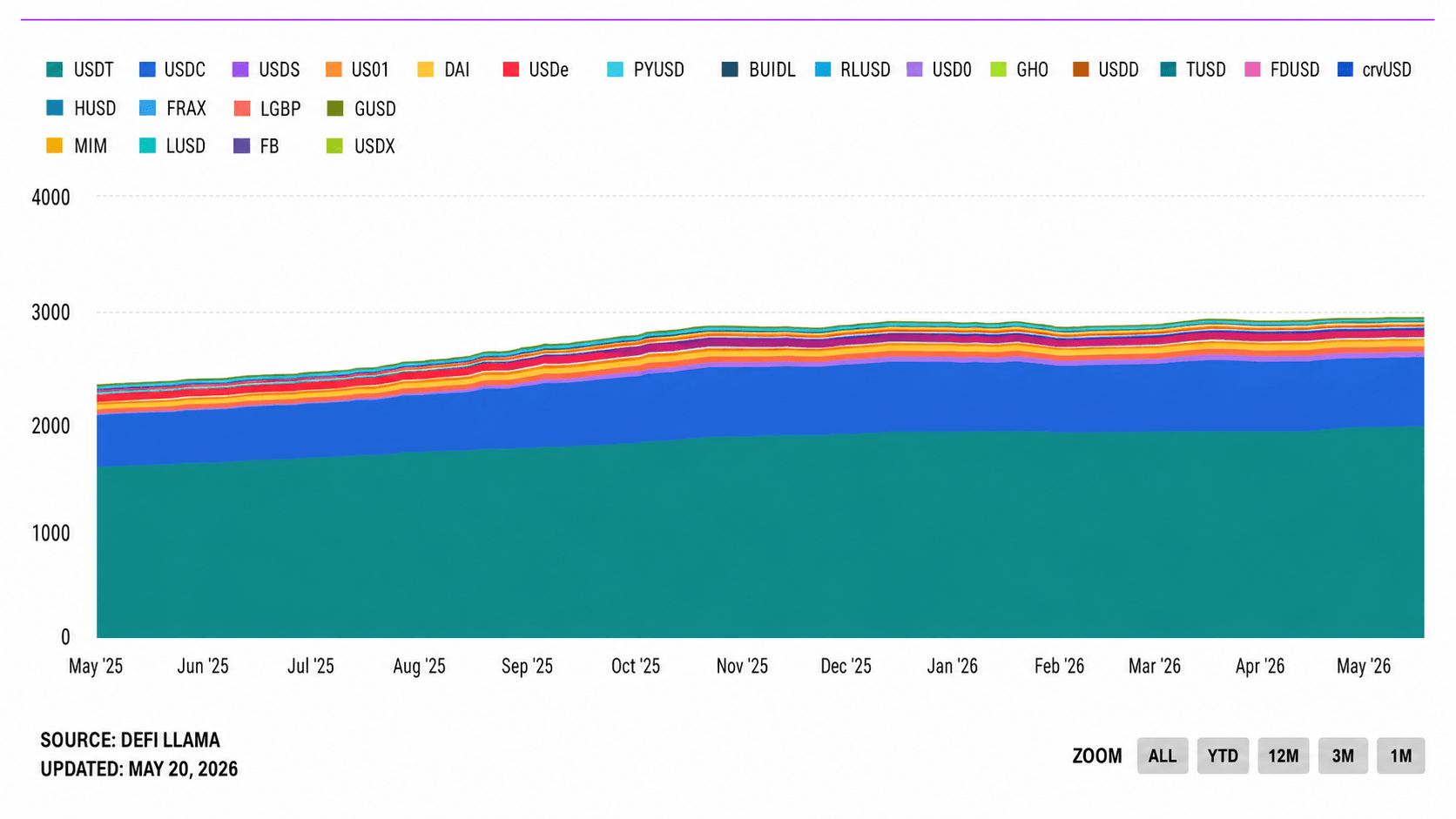

According to data, USDT’s net growth over the past month stands at roughly $900 million (0.3% of the total supply), as nearly every dollar entering the market is a Tether dollar replacing a redeemed USDC, USDe, or PYUSD position.

USDT’s circulating supply now sits at approximately $189.7 billion, giving it close to 60% of the total stablecoin market. When combined with USDC, the two incumbents account for roughly 93% of the entire category.

Tether’s monthly gain of over $5 billion does not appear to reflect new money entering the stablecoin sector but rather a rotation from competing products back into the perceived safety and liquidity of USDT.

Market share of different stablecoins per their total capitalization.

The sharpest pain is visible in relation to Ethena, as the synthetic dollar protocol’s USDe has declined 28% over the past month and is down approximately 34% year-to-date, with sustained outflows running since October 2025. Paypal’s PYUSD and Circle’s USDC have also posted declines over the same window, though neither at the same severity as USDe.

The dynamics reflect two converging forces. First, the regulatory environment in the U.S. has tilted toward Tether’s positioning: pending stablecoin legislation, primarily the GENIUS Act, which the Senate is working to finalize, has raised compliance questions for newer algorithmic and synthetic instruments, nudging institutional users toward more established issuers. Second, broader risk-off sentiment in the market has historically pushed capital toward the most liquid stablecoin, which remains USDT by a wide margin.

Bitcoin.com News reported on the stablecoin market crossing $320 billion last month, a milestone at the time accompanied by a slight dip in Tether’s dominance share. The latest data suggests that dip has since reversed, with Tether reasserting control even as total market growth stalls.

For decentralized finance ( DeFi) protocols that rely on USDe and PYUSD as collateral or liquidity layers, the continued compression of those supplies is likely to have downstream effects on borrowing rates and yield opportunities across lending markets.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。