Article Translation: Block Unicorn

The company earned billions of dollars in interest income by holding U.S. Treasury reserves as collateral for its stablecoin, paying fees to other platforms for distributing and settling USDC across the payment system. For every dollar Circle earns, it pays about 60 cents to its USDC partners. As long as the profit margin is large enough, it can afford this expense. However, with the arrival of low-interest rates, this USDC issuer has lost too much profit. For most of its development, Circle had only one product: USDC.

In its recently released Q1 2026 financial report, the USDC issuer announced several initiatives aimed at enhancing the value within its operational scope. These include a $222 million presale for its native Layer-1 token ARC, with a fully diluted valuation of $3 billion; launching artificial intelligence agent infrastructure; and expanding its Circle payment network to enable banks to facilitate stablecoin payments by circumventing the volatility of digital assets. The achievements that Circle has made over the past few quarters will change this situation.

In summary, these initiatives mark Circle's attempt to transition from a single-layer company to a full-stack financial platform capable of operating and extracting value at multiple layers of the payment stack.

Today, I will evaluate whether Circle can utilize vertical integration to offset the shrinking revenue business as this revenue has been continually shrinking with each rate cut by the Federal Reserve.

The Disappearing Buoy

In Q1 2026, Circle's total revenue was $694 million, a 20% year-over-year increase. This growth was entirely due to the expansion of the circulating stablecoin supply, with no improvements in USDC itself. The circulating stablecoin supply grew from $235 billion in March 2025 to $315 billion in March 2026, an increase of over 30%. During the same period, USDC's market share fell by 62 basis points.

Circle faces a bigger problem. The era of low interest rates has arrived, with the Federal Reserve rate dropping from 4.5% a year ago to the current 3.75%.

Although the average circulation of USDC increased by 39% year-over-year as of Q1 2026, Circle's reserve income grew only 17% year-over-year to $653 million. This is because the average reserve yield fell by 66 basis points from 4.16% in Q1 2025 to 3.50% in Q1 2026, significantly offsetting the aforementioned growth.

This is not a one-time phenomenon. Over the past four quarters, the gap between Circle's reserve income growth rate and USDC supply growth rate has continued to narrow.

Circle's primary source of income has not grown proportionally with its circulating stablecoin supply.

The company also faces issues of value loss.

The 60-Cent Awakening

This means that the cost of holding and distributing each dollar of USDC on the platform exceeds 60 cents. Of the $405 million in USDC, Circle paid Coinbase $330 million (about 80%) in Q1 2026 as distribution costs. In this quarter's $653 million in reserve income, Circle paid partners $405 million as distribution and transaction costs.

In an industry where new players continuously expand and integrate across various layers of the tech stack, this represents a significant loss of money.

At this moment, various signs indicate that Circle should face reality. The continuous decline in interest rates is leading to a reduction in its reserve income; high distribution costs are causing constant value loss; and Circle's core business remains an alternative metric for yield, decreasing in value with every rate cut by the Federal Reserve. Under President Donald Trump's leadership, market expectations for a dovish stance from the Federal Reserve are becoming increasingly stronger.

What is Circle's countermeasure? The answer is: through vertical integration, capturing more value throughout the business chain and reducing dependence on interest income.

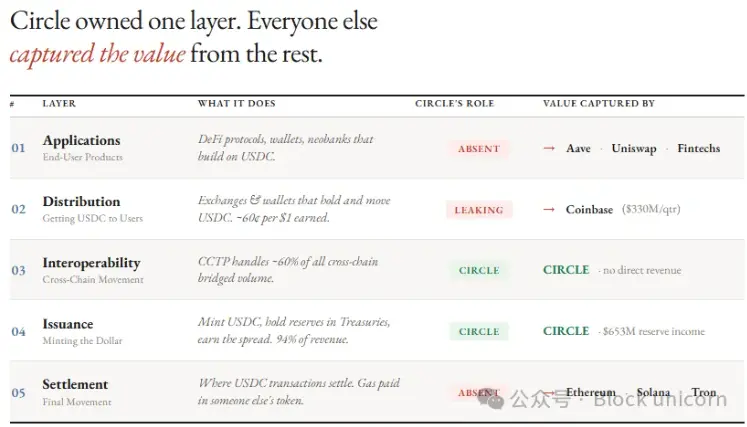

To understand what Circle is building, consider what it currently possesses.

As the USDC issuer, Circle has been observing how others have captured value at every layer above the foundational layer of the stablecoin stack — the issuance layer.

At the issuance layer, Circle issues USDC and EURC, holds U.S. Treasury reserves via BlackRock's Circle Reserve Fund, manages a 1:1 pegged exchange rate, and handles issuance and redemption through Circle Mint. 94% of its total revenue comes from U.S. Treasury reserve income.

Subsequently, Circle expanded its business to the interoperability layer through its Cross-Chain Transfer Protocol (CCTP), which transfers USDC across blockchains and handles about 60% of cross-chain bridge transaction volume. While this mechanism is responsible for routing USDC between chains, CCTP itself operates on chains owned by others. Therefore, Circle cannot gain significant direct income from this.

All other layers in the stack belong to others.

The settlement system runs on Ethereum, Solana, and Tron. Every USDC transaction incurs gas fees paid in other tokens (ETH, SOL, TRX), and Circle has no control over congestion, fees, or governance on these chains.

Distribution channels mainly rely on Coinbase, exchanges, and wallets. Circle needs to pay revenue sharing, incentive program fees, and integration costs to get USDC into users' hands.

Third-party institutions, such as decentralized finance (DeFi) protocols, fintech companies, neo-banks, and prediction markets, build applications and products using USDC. This means that end customers, whether retail or institutional, do not need to transact directly with Circle.

This structure results in Circle only making 40 cents for every dollar it earns.

Controlling the Tech Stack

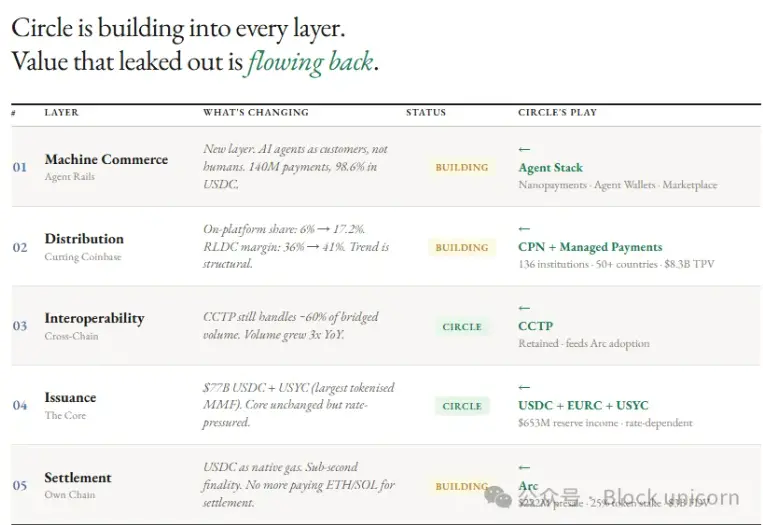

On May 11, Circle announced three investment plans aimed at vertically integrating different tiers of its business that it previously did not own.

The first is settlements.Circle owns the native Layer-1 blockchain Arc, which aims to capture fees currently generated by the transfer of USDC across blockchains such as Ethereum, Solana, and Tron.

EVM-compatible Arc provides sub-second finality and uses USDC as its native gas fee token, with transaction fees around $0.001. To make its chain more attractive to institutional users, Circle offers configurable privacy protection and quantum-resistant architecture. In contrast, universal public chains like Ethereum and Solana are completely transparent and cannot provide privacy for sensitive transactions such as institutional payments.

Circle raised $222 million through the ARC token presale, with a valuation of $3 billion. This round of financing was led by a16z with a $75 million investment, with other investors including BlackRock, Apollo Global Management, Intercontinental Exchange (parent company of the New York Stock Exchange), Standard Chartered Bank, ARK Invest, SBI Group, IDG Capital, Bullish, and Haun Ventures.

The second is distribution.Circle Payments Network (CPN) helps USDC issuers reduce dependence on Coinbase.

CPN connects financial institutions directly to Circle's network, allowing them to mint, redeem, and route USDC without going through exchanges. The network has 136 registered institutions (up 36% quarter-over-quarter), with an annual transaction volume of $8.3 billion (up 17% quarter-over-quarter), providing fiat payment services in over 50 countries.

Thus, the proportion of USDC based on Circle's own infrastructure has nearly tripled, growing from about 6% a year ago to 17.2%. Even with a decline in reserve yield, the RLDC profit margin (revenue minus distribution and transaction costs as a percentage of revenue) has steadily increased from 38% in Q2 2025 to 41% in Q1 2026.

Circle has not yet commercialized CPN but prioritizes user growth over fees. However, once it is commercialized, every increase in CPN usage will generate usage-based revenue for Circle without relying on interest.

Circle has built a complete agent economy through products such as Agent Wallets, Nanopayments (supporting gas-free USDC transfers as low as $0.000001), Agent Marketplace (where agents can discover and pay for services), and Circle CLI (to accelerate agent onboarding and wallet configuration).

The third layer is the application layer.Through this third layer, Circle charges small fees on large transactions executed by AI agents, capturing ongoing value across the entire agent economy.

How big is the market opportunity for agent payments? Last month, Circle's marketing head Peter Schroeder announced that among the 140 million transactions completed by AI agents in nine months, USDC accounted for 98.6%.

Stack Competition

Circle's expansion into the payment system is not easy. Payment giant Stripe started at the top and gradually moved in with a series of transactions and product launches. The acquisition of Bridge gave Stripe control over the authorization, hosting, forex, and issuing layers. By launching Tempo, Stripe entered the settlement layer. Today, Stripe controls all seven layers of payments, serving 5 million merchants.

Tether uses Plasma, incubated by the USDT issuer, as its settlement chain. However, Tether's regulatory scrutiny is still less stringent than USDC's.

Stripe dominates the consumer transaction space, while Tether leads in emerging market dollar transactions and cryptocurrency trading. Therefore, Circle is positioning itself in the field of institutional settlements and machine trading, where regulatory credibility and programmable infrastructure may be more important than the checkout integrations dominated by Stripe.

CRCL's Counteroffensive

Despite Circle raising $222 million for the ARC token pre-sale aimed at institutional investors, the initial development funds for ARC actually come from CRCL's shareholders. Ironically, the greatest resistance Circle faces may be how to deal with internal resistance.

What does it mean for a public company if the value of the Arc token increases? I pointed out this issue last November.

“The nature of a native token will raise some controversy in the open market. Why would the market recognize or value a native token that captures the value created by Arc and CPN rather than allowing that value to flow back into Circle's income statement? Why should Circle's surplus be used to fund a cost center that is not expected to return profits to shareholders? Existing shareholders will never tolerate this. Public market investors buy CRCL for its reserve income. They are unlikely to passively watch a new asset absorb the capital appreciation of their infrastructure investment.”

How will Circle solve this issue? Is standalone listing for Arc reasonable? We won’t know the answer until the first quarter after Arc launches on its mainnet.

Currently, Circle's long-term goal is to capture as much value as possible by continually expanding its influence across these layers. Each time USDC settles on Arc, Circle earns a settlement fee. When institutions transact via CPN, Circle retains distribution profits. Finally, when agents transact through Nanopayments on Arc, Circle also hopes to be able to charge fees at that layer.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。