Produced by | MiaoTiao APP

Author | Ding Ping, HuXiao APP

Header image | Vision China

Wash is not the storm itself, but he may make the market realize that when the storm comes, the Federal Reserve is no longer in the same position as before.

In the past two years, tech giants like Nvidia, Microsoft, and Meta have continually broken market value records, and AI has almost redefined the entire market's risk appetite, raising the S&P and Nasdaq indices significantly.

However, if we break down this round of market movement, AI is actually just the story in the spotlight. The real support for US stock valuations is another more critical premise: long-term interest rates will eventually come down.

Only if this premise holds can the market dare to continue to pay high premiums for future earnings, dare to continuously discount the growth narrative of a few tech leaders to today, and dare to pursue on valuations of 30 times, 40 times, or even higher.

But now, this premise is becoming unstable.

The yield on the 30-year US Treasury bond continues to rise, recently breaking the 5% high. For a US stock market that is highly concentrated, boasts expensive valuations, and is extremely dependent on future earnings narratives, the longer the long-end rates stay high, the more fragile the valuation system becomes.

What’s more troubling is that this pressure may continue to grow.

On May 15, Powell, who had led the Federal Reserve for eight years, officially stepped down, and Kevin Wash became the next chairman. Compared to Powell, Wash may be more tolerant of market pressure, more insistent on reducing the balance sheet, and reduce the Federal Reserve's implicit support for the financial market.

Once long-end interest rates continue to rise, and the Federal Reserve no longer calms the market as quickly as before, the logic of prosperity that previously supported high US stock valuations may begin to lose its support.

The current fragility of US stocks

Is that long-end interest rates cannot be suppressed.

Recently, the market has been overly focused on whether the Federal Reserve will cut interest rates, ignoring one issue: that long-end interest rates no longer follow monetary policy.

Theoretically, central bank rate cuts directly lower short-term interest rates. If the market believes that future rates will remain low, long-end rates can decline accordingly. But an unexpected situation has occurred: even though the Federal Reserve hasn't raised rates, the 30-year Treasury yield continues to rise, peaking at 5.13% on May 15. This indicates that the market does not believe that the long-term risk in the US will decrease, thus requiring a higher risk premium.

This is precisely the most fragile point of US stocks at present.

The reason long-end interest rates remain high can be attributed to at least three reasons.

First, inflation has not fallen smoothly as the market expected.

Recent data shows that the US April CPI increased by 3.8% year-on-year, the highest in nearly three years, and the core CPI increase expanded to 2.8%. More tricky is that the risks of the US-Iran conflict have not truly resolved, and high oil prices continue to strengthen the market's concerns about imported inflation. As long as inflation expectations cannot be thoroughly suppressed, long-end interest rates will be hard to decline smoothly.

Second, the fiscal issues in the US are also undermining market confidence in long-term fiscal constraints.

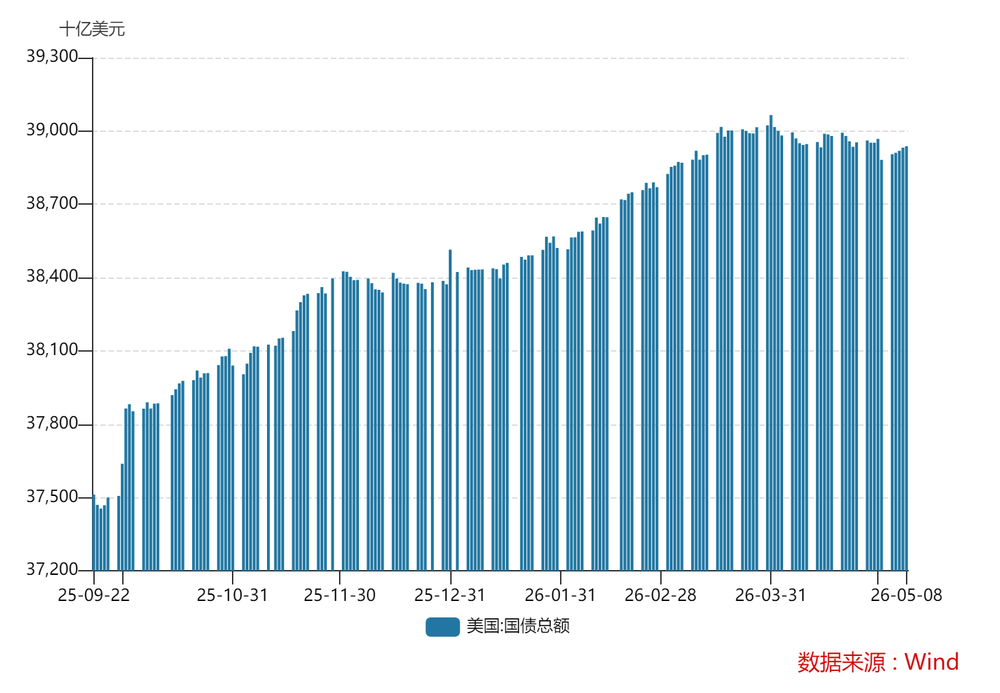

By October 2025, US national debt exceeded $38 trillion; in just five months, this figure surpassed $39 trillion. This is due to long-term fiscal deficits (high military and social welfare expenditures), and the US Treasury is issuing new bonds to repay old debts, which in turn bring higher interest expenses, making the US fall into a "Ponzi-like" fiscal debt situation where it relies on a continuously expanding debt scale to maintain the stability of the existing system.

Third, the supply and demand structure of US Treasuries is deteriorating.

On one side, the Treasury continues to increase bond issuance; on the other side, overseas investors are reducing their holdings, as the world moves towards de-dollarization, with foreign official entities decreasing their purchases of US Treasuries. The ratio of US Treasuries in global reserve assets is on a downward trend, currently at 24%. Supply is increasing, while demand is weakening, resulting in increasing difficulty in suppressing long-end rates.

When the aforementioned risks remain unresolved, US Treasuries can no longer be seen merely as safe assets, and investors will naturally demand a higher risk premium.

This poses particular danger to US stocks.

Because the current US stock market is not a generally undervalued market that slowly reveals its performance; rather, it is a highly concentrated market supported by a few leaders and is extremely sensitive to discount rates.

Once long-term rates remain high, the discounting of future cash flows will become significantly harsher, and the tolerance range for valuations will rapidly narrow. At that point, the companies to initially suffer the impact may not be the ones with the worst fundamentals, but rather those with the best fundamentals but whose valuations have already been pushed to the limits.

Bank of America’s Hartnett has also stated that if the 30-year Treasury yield breaks above 5%, market financing costs will rise, risk appetite will decline, and overvalued tech stocks will be the first to feel the impact.

October 2023 already demonstrated this once.

At that time, the 30-year Treasury yield briefly surpassed 5%, and the Nasdaq index corrected by about 10% over a few months. At that time, investors still believed that if financial conditions continued to worsen, the Federal Reserve would eventually send calming signals. But if expectations begin to loosen after Wash takes office, the market's response to the same long-end rate shock will be completely different.

Many people like to compare today with 2007, but in fact, the real takeaway is not that interest rates were also high then, but that the harm of high rates to the financial system is never instantaneous. It resembles a slow erosion: first pressuring financing, then valuations, then balance sheets, ultimately exposing the most fragile link in the system.

What truly collapsed in 2007 were real estate, subprime mortgages, and shadow banking; today, the more dangerous concerns are that high fiscal deficits are pushing long-term debt supply higher and higher, long-end rates cannot be brought down, banks face floating losses, commercial real estate tail risks, and the reliance of risk assets on liquidity will all gradually be pushed out.

Therefore, once long-end rates cannot come down, the valuation foundation of this AI bull market in US stocks will start to weaken.

This problem will become even more serious during the Wash era.

Why should the market be wary of Wash?

Because Wash tends to reduce the balance sheet, which will further increase the yield on the 30-year Treasury bond and amplify the fragility of US stocks.

How should this be understood?

Reducing the balance sheet means decreasing the scale of the Federal Reserve's balance sheet. The Federal Reserve previously bought a lot of Treasury bonds, mortgage-backed securities (MBS), and other assets to stimulate the economy; by buying these assets, it effectively injected a large amount of funds into the market. Reducing the balance sheet means letting these assets decrease, slowly withdrawing liquidity from the market.

We can also simply understand that the Treasury's new or maturing bonds will no longer be bought by the Federal Reserve, and they may even sell the Treasuries they hold.

As mentioned above, the current US Treasury is still increasing bond issuance, and overseas holdings are being reduced. If the Federal Reserve also reduces its balance sheet, then new bonds and maturing Treasuries can only flow into the market, with the market determining the interest rates, resulting in persistently rising Treasury yields. This will lead to an increasingly heavy interest burden for the Treasury, which is very dangerous for a system that relies on issuing new debt to replace old debt. Once interest costs become too high to sustain, a US debt crisis will arise.

Former Treasury Secretary Paulson has also warned that once US Treasuries start losing market buyers, the entire financial system's "risk-free anchor" will be shaken.

Given the serious consequences, why does Wash still lean towards reducing the balance sheet? This has to do with his background.

Wash served as a member of the Federal Reserve Board from 2006 to 2011, and this experience is key to assessing his policy inclinations. He fully experienced the last round of credit expansion before the financial crisis, the 2008 global financial crisis, and the initiation of zero interest rates and quantitative easing (QE).

He is not one to completely deny crisis intervention; on the contrary, during times of systemic risk, he supported the Federal Reserve acting as a lender of last resort and acknowledged the necessity of unconventional tools. However, he later grew increasingly skeptical about whether long-term QE should exist post-crisis.

From his perspective, the post-crisis US economy did not exhibit a recovery proportional to asset prices. The recovery of the real economy is not strong, productivity improvements are limited, but the prices of financial assets quickly rebounded driven by liquidity, even exceeding pre-crisis levels.

This led Wash to form a typical judgment that QE might be very good at elevating financial asset prices but may not be equally effective in repairing the real economy. Once the market begins to default to the assumption that "the Federal Reserve will inevitably support asset prices," the financial system will increasingly rely on liquidity, risk appetite will remain low for a long time, and asset bubbles and mismatches will become more serious.

Thus, in his logic, if the Federal Reserve maintains an oversized balance sheet for a long time and keeps term premiums low, the market will ultimately become increasingly unable to operate independently of central bank liquidity. He sees the balance sheet reduction not only as a withdrawal of liquidity but also as the Federal Reserve actively stepping back from its role as a "stabilizer of financial conditions."

This is also why Wash is more inclined to promote QT (quantitative tightening) than Powell.

Therefore, after Wash takes office, the high interest rate environment will be even more severe, and the Federal Reserve may not respond as quickly to calm the market as before. Once this expectation forms, the already fragile high valuation system of US stocks will face further amplified pressure.

The AI narrative also cannot digest high rates

Of course, the persistence of high yields on 30-year US Treasuries is not an absolute negative for US stocks.

If the US economy continues to strengthen unexpectedly, corporate earnings are continuously revised upward, especially if AI can indeed quickly translate into broad productivity gains, then even high long-term rates may not be unbearable for risk assets. Ultimately, what truly determines whether the market can digest high rates is economic growth itself.

In the past year, US stocks, especially tech stocks, have been able to continue rising in a high-interest environment largely due to such optimistic expectations: that AI will significantly enhance corporate earnings, boost productivity, and open up a new round of growth for the US economy.

However, the problem is that the AI narrative currently focuses more on a few leading companies and the capital market level, and has not been sufficiently proven to rapidly and broadly translate into fundamental improvements across the entire economy.

Taking Nvidia as an example, it has indeed created amazing capital returns and market imagination, but companies like this share common characteristics, such as high technological barriers, high profit concentration, and limited job absorption capacity (by fiscal year 2026, Nvidia's total global employee count is only about 42,000), meaning the spillover effects on the overall economy are not as strong as market sentiment suggests.

In other words, AI can quickly raise valuations for companies like Nvidia and Microsoft in a short period of time but may not be able to support broader employment, investment, and expansion of the real sector in the same short time frame.

Moreover, more realistically, the US currently faces issues related to insufficient electricity, infrastructure, and industrial support. The faster the AI industry expands, the more easily it can draw capital, energy, and talent away into the leading tech sectors, thereby worsening the already unbalanced allocation of resources towards the leading tech sectors.

This is not to say that AI is ineffective, but to emphasize that it has not yet accelerated enough to cover the valuation pressures brought on by high long-end rates.

In other words, the market thinks it is trading AI, but in reality, it is still trading another matter: low long-end rates and the Federal Reserve's support. As long as these two premises remain in place, high valuations can continue; once they begin to loosen, no matter how strong AI is, it simply delays reevaluation rather than cancels it.

Wash is not the source of risk, but he may be the one making it harder to reverse this situation.

In summary, though Wash will not actively create a crisis, he may lead the market to truly accept for the first time that the previous high valuation logic, which relied on low long-end rates and Federal Reserve support, is no longer as stable.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。