Barclay's latest analysis shows that the Federal Reserve's baseline scenario still anticipates an interest rate cut in March 2027, but the conditions are extremely stringent, with only a 35% probability.

Written by: Zhao Ying

Source: Wall Street Journal

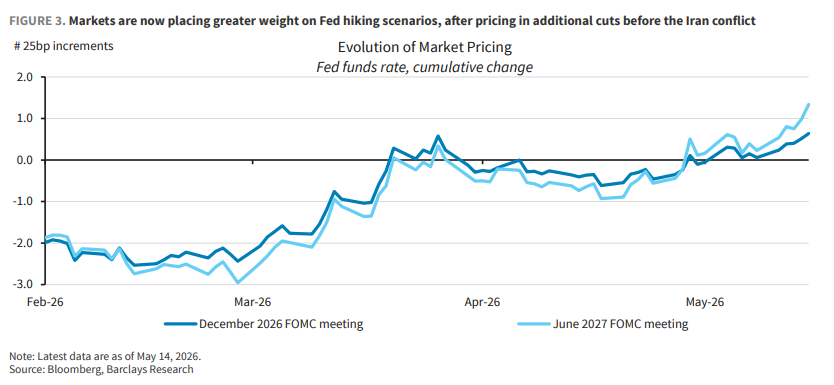

The Federal Reserve does not expect to raise interest rates this year as its baseline scenario, but it is no longer just a tail risk. The blockade of the Strait of Hormuz is raising pressures on commodity prices, and AI-related capital expenditures are squeezing some global supply chains; the market has begun to reprice the "hawkish turn": by the December 2026 FOMC meeting, the probability of an interest rate hike has exceeded 60%, and by March 2027, one rate hike has been fully priced in.

According to Wind Trading Desk, Barclays FICC economist Jonathan Millar and others noted in their Fed commentary on May 18 that the key judgment is: "While our baseline scenario does not anticipate a rate hike before the end of 2027, the upside risks to the policy rate have intensified." The three paths that could trigger a rate hike are also clear: a sustained disanchoring of long-term inflation expectations; core inflation remaining persistently high after the tariff shocks fade; and demand outpacing supply, especially as the AI investment cycle and wealth effect release ahead of productivity improvements.

The baseline path remains moderate: the Federal Reserve will hold rates steady until 2026, with the next step being a 25 basis point cut in March 2027. This judgment relies on two premises: a relatively swift end to the disturbances in the Strait of Hormuz and a retreat of tariff transmission and energy-related price pressures; simultaneously, a slowdown in consumer spending would cool overall demand.

However, the probability distribution has become quite "hawkish." In the subjective scenario, the probability of a 25 basis point cut in 2027 is 35%; holding rates steady until the end of 2027 is 30%; the rate hike scenario is 25%, with an increase of about 50-100 basis points; and the probability of a recession triggering significant rate cuts is 10%. In other words, the most likely deviation is not an immediate interest rate hike, but a delay in interest rate cuts.

The market no longer sees rate hikes as a tail risk

The changes in the interest rate market are very direct. Before the Iranian conflict, the market was still digesting more rate cuts; afterwards, pricing rapidly shifted towards the risk of rate hikes.

The underlying variable is not a single oil price shock. ISM manufacturing and services purchasing price indexes, as well as the New York Fed’s global supply chain pressure index, all indicate rising cost pressures; at the same time, the U.S. labor market has not significantly deteriorated, with the unemployment rate remaining in a low range and the three-month average non-farm employment giving a "relatively stable" impression.

This is tricky for the Federal Reserve. If it is just a one-time increase in price levels, policy can "see through" it; but if the shock lasts long enough, inflation expectations, wages, and corporate pricing behavior will start to follow, and the issue will shift from a supply shock to inflation inertia.

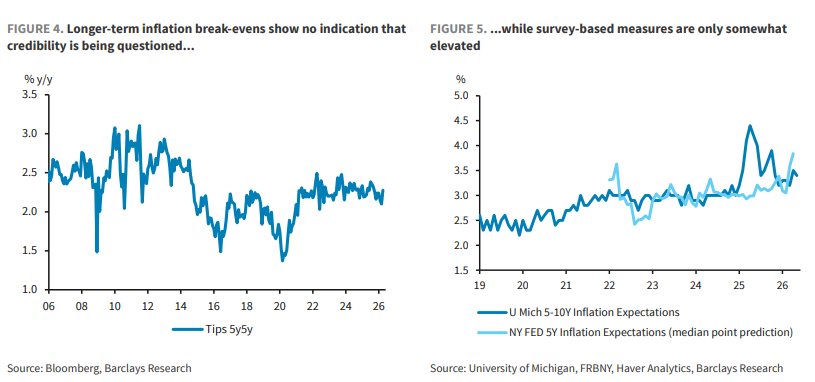

The shortest path to rate hikes: long-term inflation expectations becoming unanchored

The most direct trigger condition is the beginning of loosening long-term inflation expectations.

What needs to be monitored is not one or two months of CPI, but the market-based inflation expectations for 5-10 years, especially the 5y5y inflation breakeven rate. If these indicators continue to rise, and the trend is chaotic and disconnects from short-term inflation changes, the Federal Reserve will view it as a signal of damaged credibility regarding the 2% inflation target. If long-term inflation expectations in surveys from sources like the University of Michigan and the New York Fed rise in sync, this judgment will be reinforced.

We are not at that point yet. The long-term inflation breakeven rate has not shown that the Federal Reserve's credibility is in question, and the long-term inflation expectations from survey measures are only somewhat elevated. The real risk lies in the disturbances in the Strait of Hormuz and commodity shocks dragging on for too long and too greatly, leading the market to question whether the Federal Reserve is still willing to pay the costs of growth and employment for the 2% target.

If such signs appear, policy communication will likely shift hawkishly first. The Federal Reserve will not wait for all data to confirm before alerting the market.

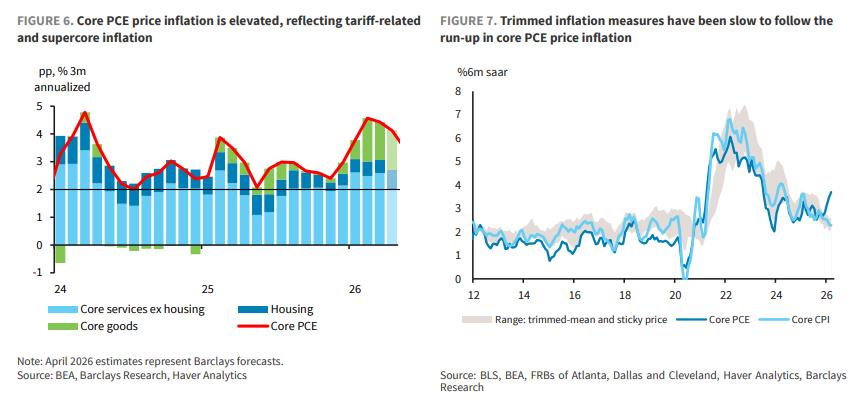

After tariffs retreat, if core PCE doesn't come down, it could be problematic

The second path is slower but more realistic: core inflation repeatedly exceeding expectations.

The key threshold given in the framework is that the core PCE rises approximately 0.18% month-on-month, which is roughly consistent with the 2% target monthly rate. If core PCE remains high above this level, while tariff-related pressures are expected to have begun to dissipate, the Federal Reserve's room for continued observation will be compressed.

Several finer points are more important: core goods have not shown the expected anti-inflationary behavior; the core services excluding housing, known as "super core," have limited cooling; global supply chain pressures are rising again; the trimmed mean or median inflation indicators are beginning to strengthen, indicating pressure is no longer concentrated in a few items.

The key word for this path is "sustained." Single-month data is insufficient; even several months may not suffice; but if it persists for several quarters, the Federal Reserve will have a hard time explaining it as a temporary disturbance.

There is also a fork here: if inflation is high while demand is strong, the policy inclination will shift toward tightening; if demand has already clearly weakened while inflation remains high, the dual objectives of the Federal Reserve will conflict. However, after the inflation shock of 2021-2022, the threshold for not prioritizing price stability is quite high.

AI may boost demand first, rather than immediately lowering inflation

The third path is less related to the Middle Eastern conflict, largely stemming from domestic demand in the United States.

The AI investment cycle is accelerating. Private domestic final purchasers have not yet significantly slowed down, and AI-related investments have accelerated again this year, with financial conditions leaning towards supporting growth under the Federal Reserve’s model. If the capital expenditures and stock market wealth effects brought by AI release ahead of productivity and cost efficiency, the result may not be a decline in inflation, but a surge in demand first.

This is different from the technology narrative during Greenspan's era. At that time, productivity gains were hard to recognize in real-time; supply improvements occurred first, and demand reactions lagged; this time, the potential productivity gains from AI are fully anticipated by the market and reflected in financial conditions and spending behavior.

The data also has two sides. Non-farm business sector productivity grew nearly 3% over the four quarters ending in Q1 2026, about twice the pre-pandemic rate; however, the San Francisco Fed’s adjusted indicator suggests this growth rate may be overestimated by about 1.5 percentage points. In other words, the apparent supply improvement may not be sufficient to sustain the demand that has already been anticipated.

The Federal Reserve will use several traditional signals to assess whether the economy is overheated: growth exceeding trend, unemployment rate dropping below the 4.0%-4.3% NAIRU range, wages accelerating again, and increases outpacing real productivity. Currently, evidence of wage acceleration is not strong, but this clue needs to be monitored.

The baseline remains a rate cut in 2027, but the premises are very demanding

The baseline scenario has not changed: holding steady for a long time, with a 25 basis point cut in March 2027. The logic is that by then, energy, tariff, and supply chain-related price pressures will have subsided, allowing core PCE to slow significantly, giving the Federal Reserve room to approach the long-term neutral rate.

This path is very sensitive to the duration of the disturbances in the Strait of Hormuz. If the disturbances are brief, and tariff transmission gradually fades, the cut window can still open; if disturbances prolong, core inflation and inflation expectations will first close the window.

Consumption is equally critical. Real disposable income for families has clearly slowed over the past year, mainly due to the deceleration of job growth; if labor supply growth continues to slow, consumer spending should also cool down accordingly. If this assumption fails, with AI capital expenditures and wealth effects continuing to support demand, the Federal Reserve will face a more challenging judgment: whether current policy is tight enough.

Thus, the Federal Reserve's risk in 2026 is not simply a switch from "rate cuts" to "rate hikes." More accurately stated, the path to rate cuts is being squeezed simultaneously by supply shocks, core inflation stickiness, and the spillover demand from AI. Rate hikes still require more robust data triggers, but they have already returned to the policy table.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。