Author: Claude, Deep Tide TechFlow

Deep Tide Introduction: On-chain data shows that Wintermute and Auros Global significantly withdrew liquidity from mainstream cryptocurrencies such as BTC and ETH from Hyperliquid on May 18, totaling nearly $100 million.

Auros has fully closed its positions and withdrawn funds to Binance, while Wintermute's liquidity in BTC+ETH has sharply decreased by about 90%. This withdrawal occurred just three days after CME and ICE jointly pressured U.S. regulators to review Hyperliquid; the actions of market makers could be an early indicator of a regulatory storm.

Hyperliquid is undergoing a rare liquidity withdrawal event.

According to monitoring data from the on-chain intelligence platform Hyperinsight, on May 18, the two major market makers Wintermute and Auros Global drastically reduced the liquidity supply of mainstream cryptocurrencies within hours, withdrawing a total of about $100 million. Multiple independent on-chain analysis accounts have cross-verified this data through address tracing, and no significant contradictions have emerged.

The timing of this action is intriguing. Just three days prior, Bloomberg reported that CME Group and the Intercontinental Exchange (ICE) were jointly lobbying the Commodity Futures Trading Commission (CFTC) and U.S. Congress members for stricter regulation of Hyperliquid. The rapid withdrawal of the two major market makers may be a routine compliance risk management action, or a precursor to a regulatory storm, and the market is closely watching.

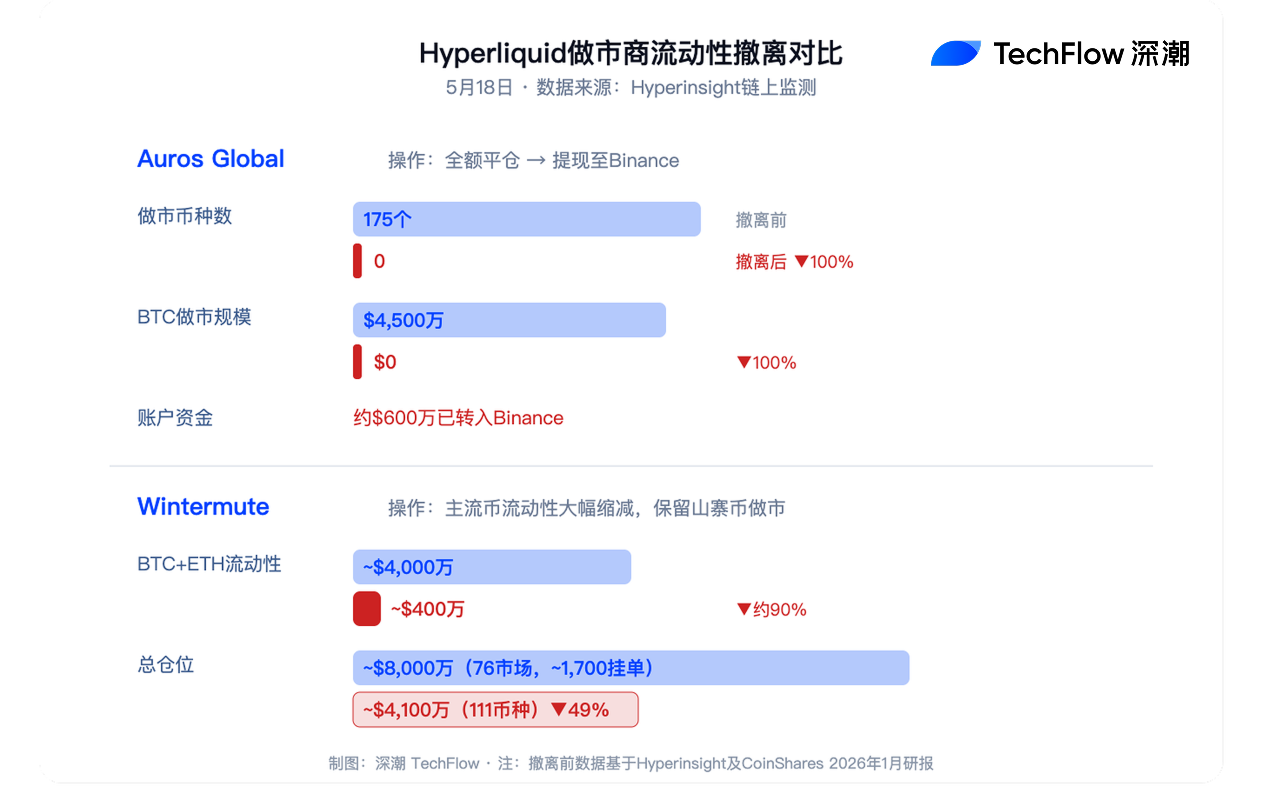

Auros fully closes positions and withdraws to Binance, Wintermute's mainstream cryptocurrency depth drops by 90%

Hyperinsight on-chain data shows that the withdrawal paths of the two market makers are drastically different but synchronized in timing.

Auros Global (some on-chain tags show as Oros Global) provided liquidity for 175 cryptocurrencies on Hyperliquid before withdrawing, with BTC alone having a market-making scale of about $45 million. As of the morning of May 18, Auros had fully closed positions, with about $6 million withdrawn to Binance; the holdings and withdrawal records of the related addresses can be publicly accessed on HypurrScan.

Wintermute's operations are somewhat more restrained but similarly aggressive. Its liquidity for BTC and ETH dropped from about $40 million to about $4 million, a decrease of about 90%; overall positions decreased from nearly $80 million to $41 million. Wintermute still maintains orders for 111 cryptocurrencies, but the order book depth for mainstream cryptocurrencies has significantly thinned.

The two addresses are as follows:

0xecb63caa47c7c4e77f60f1ce858cf28dc2b82b00

0x023a3d058020fb76cca98f01b3c48c8938a22355

For Hyperliquid, which relies on on-chain order book matching, the simultaneous withdrawal of the two market makers means the widening of the bid-ask spread for core trading pairs like BTC and ETH, increased slippage, and a significant rise in the execution cost of large trades.

CME and ICE united pressure three days ago, directly targeting Hyperliquid's perpetual oil contracts

The time window for the market makers' withdrawal aligns closely with an escalating regulatory game.

On May 15, according to Bloomberg, CME Group and ICE issued warnings to the CFTC and U.S. Congress members, stating that Hyperliquid's anonymous trading environment could distort the global oil price benchmark and provide channels for market manipulation and sanction evasion. The two exchanges requested that Hyperliquid register with the CFTC, meaning the platform would need to implement customer identification procedures and transaction monitoring mechanisms, which directly conflicts with its current anonymous trading model.

According to CoinDesk, the core concerns of CME and ICE focus on Hyperliquid's HIP-3 market. This mechanism allows users to gain synthetic exposure to stocks and commodities through on-chain contracts. In March this year, the perpetual contract tracking WTI crude oil on Hyperliquid set a record of over $1.2 billion in 24-hour trading volume during a spike in traditional market oil prices, directly touching the nerves of traditional exchanges over pricing power.

The Hyperliquid Policy Center subsequently released a statement saying these concerns are "groundless," emphasizing that the on-chain transparency of public chains actually provides more effective tools for regulatory enforcement. According to U.Today, this advocacy group has met with the CFTC seeking to establish a legal framework that allows U.S. users to participate in compliance.

However, the calculation logic of market makers differs from the public relations statements of the protocol parties. Both Wintermute and Auros Global are regulatory-bound institutional entities, and when compliance uncertainty rises, reducing exposure is standard risk management response. During the flash crash in October 2025, Wintermute desk strategist Jasper De Maere told Decrypt that when the reliability of hedging tools cannot be guaranteed, the only thing market makers can do is withdraw.

Cerebras PreIPO's out-of-the-box effect accelerates Wall Street's awareness

One of the catalysts for escalating regulatory pressure is that Hyperliquid's "out-of-the-box" speed in traditional financial markets far exceeds expectations.

On May 14, AI chip company Cerebras Systems went public on Nasdaq, with an IPO price of $185 per share and an opening price of $350, a nearly 90% increase, making it the largest U.S. tech IPO since Uber in 2019. In the weeks leading up to the listing, Hyperliquid's PreIPO perpetual contracts had already begun pricing CBRS, with more than $280 million in trading volume on the day of the listing.

BitMEX co-founder Arthur Hayes posted on X platform that he estimated the opening price of CBRS through Hyperliquid's gray market contracts. According to U.Today, the daily trading volume of Cerebras' PreIPO contracts on Hyperliquid once exceeded $230 million, while Nasdaq's official pre-market trading was only about $30 million. Professional traders shared screenshots on social media quoting charts from the on-chain DEX instead of traditional trading terminals.

This phenomenon made Wall Street realize that Hyperliquid is no longer just a derivatives exchange native to crypto; it is intruding into the core territory of traditional finance. As of May 2026, Hyperliquid controls 53% of the fee revenue in the on-chain derivatives space, with open contracts reaching $2.45 billion.

How the liquidity gap evolves in the short term depends on regulatory pace

Currently, Wintermute still maintains some market-making activities on Hyperliquid (111 cryptocurrencies), but the liquidity of mainstream cryptocurrencies is far below previous levels. According to an analysis by 0xLoris on GitHub in January 2026, Wintermute previously maintained an aggregate nominal value of about $199 million in orders across 76 markets on Hyperliquid. The current withdrawal indicates that this figure has significantly shrunk.

For traders, what needs to be focused on in the short term is the changes in the bid-ask spread of BTC and ETH perpetual contracts and the slippage of large orders. The on-chain order book structure of Hyperliquid means that market makers' withdrawals will reflect more directly in the trading experience than centralized exchanges.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。