Author: Jason

Translation: Deep Tide TechFlow

Deep Tide Introduction: RoboStrategy ($BOT) just went public and has faced constant controversy; some say it is a "liquidity exit scam", while others feel it resembles a venture capital fund. Essentially, it replicates Saylor's MSTR flywheel: issuing shares at a premium to buy private equity in robots, where each issuance not only avoids dilution but actually increases NAV. Heavily invested in Figure AI and Apptronik, which are top targets that cannot obtain shares, on the eve of AI capabilities spilling into the physical world, this could be the only pure robot exposure retail investors can access.

The newly public $BOT (RoboStrategy) has sparked various interpretations—some say it is a liquidity exit scam, others think it resembles the next $DRAM, and some compare it to Fundrise's $VCX. My view is different:

As the name suggests, $BOT closely replicates Microstrategy ($MSTR) strategy. If you are optimistic about the robotics sector in the coming years, this is a worthwhile asset to allocate. It is not just a venture capital fund or an industry ETF; there are structural differences.

Strategy Flywheel Review

Each share of Strategy $MSTR represents the BTC holdings of the company.

Saylor issues shares at a NAV premium (1.5x - 3x mNAV premium).

Because of the premium, the selling price of new shares is higher than the value of underlying assets, and the cash obtained is used to buy more BTC (thickening effect).

Due to the premium issuance, the NAV per share increases, corresponding with "per share BTC" rising simultaneously.

But why would there be a NAV premium?

Are investors foolish enough to pay more than the value of the underlying asset for a company?

The simple answer: reflexive speculation + access scarcity

Most institutional allocation tools cannot directly buy BTC on balance sheets, making MSTR an excellent proxy exposure.

Saylor's narrative and brand trust—the market believes he can continuously obtain funding to sustain the flywheel.

The reflexivity of each share of BTC thickening. As long as the mNAV remains above 1x, each issuance of shares is thickening rather than dilutive because, despite the increased share count, the BTC per share is still rising.

Leverage and convertible bonds: MSTR’s proxy characteristic causes extremely high volatility due to BTC. They issue a large number of convertible bonds to buy BTC. The convertible bond market is eager to buy such bonds because it gets a bond + a bullish option on MSTR stock price increase, with very low interest rates. Saylor secured near-zero-cost loans to buy BTC.

Mapping to $BOT

The underlying assets of RoboStrategy are not BTC, but private equity in robots. Roth recently announced a $2 billion equity financing limit for $BOT, acting as an ATM mechanism. Shares can be issued at a premium to Roth, increasing $BOT’s NAV while funds are effectively allocated to top robotic companies.

Currently, RoboStrategy's portfolio heavily invests in Figure AI, Apptronik, and Dyna, all leading robotics companies in the United States. From first principles, these companies have no reason not to perform well in the next 3-5 years. Human labor is the largest TAM globally, with demand for more labor clearly exhibiting exponential growth, especially against the backdrop of western industrial and manufacturing domestic capacity. An obvious but underrated connection is that robots are the biggest beneficiaries of advancements in AI capabilities; embodied intelligence is the next logical frontier for expanding demand and materializing digital intelligence from cutting-edge labs. RoboStrategy is the only widely accessible tool for pure private exposure to robotics.

Bullish Mechanisms

Access scarcity: Retail investors cannot access these shares. Robotics is even earlier than AI labs, the rounds are more selective, and even institutional allocators find it hard to gain entry. The RoboStrategy team has a top track record in securing allocation and conducting due diligence investments.

NAV mechanisms: Robotics equity represents operational execution such as product launches, contract signings, AI improvements, and valuation increases through financing rounds. BTC resembles a pure commodity. Multiple engines drive NAV growth here, thus pushing up $BOT’s price.

Meme properties: The stock code is $BOT. If memecoins and certain memestocks have proven anything, it’s that the code itself carries traffic.

Reflexivity: If RoboStrategy continues to grow into a giant allocator in the robotics sector, it will reflexively amplify its own value—becoming the best exposure tool in the robotics space while remaining open to the public.

Balancing the Bearish Mechanisms

NAV subjectivity: If robotics don't rise unilaterally, and a down round occurs, it will compress $BOT’s NAV, especially if it’s a large position in the portfolio.

Liquidity events killing access premium: When Figure or Apptronik go public, that part of the NAV turns into publicly traded shares, compressing the corresponding packaging premium. This assumes that no new positions are added on the private equity side, but Figure or Apptronik should not IPO in the short term.

No convertible bond market or leverage: $BOT does not have the convertible bond-fueled leverage cycle that MSTR has, but I expect more actions in this regard.

SpaceX stealing the best robot proxy position: SpaceX’s IPO is coming soon, and Optimus/humanoid robots are a significant part of Musk's pitch. If the narrative momentum shifts to SpaceXAI, other players will lose steam. However, SpaceX is a conglomerate rather than a pure play, with open market valuations implying over $1 trillion. It could also have the opposite effect, bringing several positive revaluations to private robotics companies.

2027 is the Year of Robots and World Models

Jim Fan, Director of Robotics at Nvidia, summarized two weeks ago that a "Great Parallel" is occurring in the robotics field:

Large language models (LLM) are reaching their conclusion.

Robots will replicate the exact development path of LLM, accelerating robots towards the same conclusion.

Now is not the time to nitpick Figure AI's livestream or sing the blues about robots not being ready; everything is happening, and the pace will be faster than most expect.

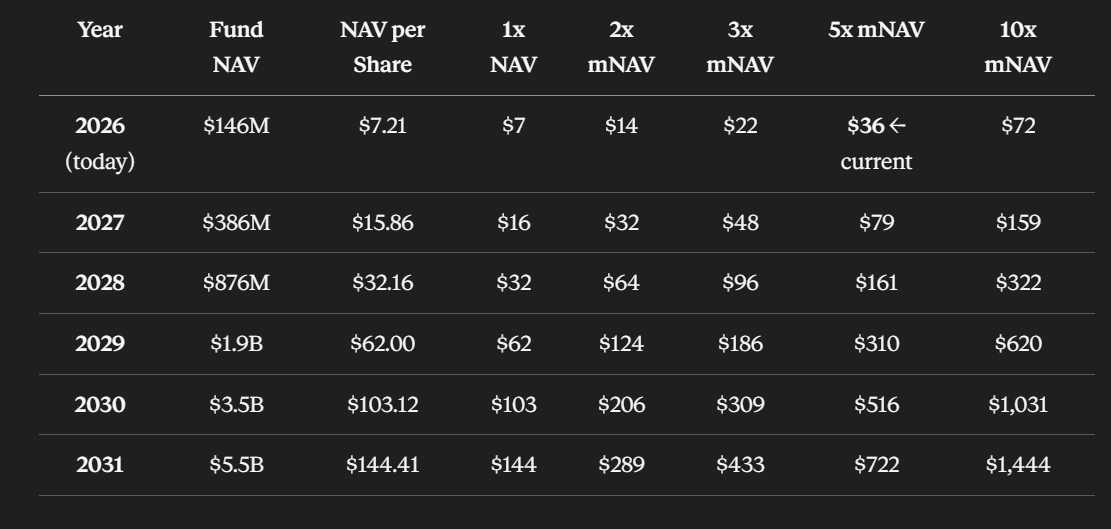

If we apply a simple but simplified growth valuation model to top US robotics companies, referencing Anthropic or OpenAI's trajectories, combined with different mNAVs, we arrive at the following prices:

Figure caption: Claude created this model; even a conservative 2x mNAV scenario suggests the price will rise about 8 times from the current price within five years.

At this moment, RoboStrategy is the best public tool for long-term bets in this sector.

Disclaimer: This is clearly not financial advice.

Disclosure: I hold $BOT.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。