Bitcoin fell to $60,000 this year, and with the massive liquidity of dollars and renminbi waiting to be released, returning to $126,000 is an inevitable trend.

Written by: Arthur Hayes, Co-founder of BitMEX

Translated by: Saoirse, Foresight News

The initial signs of the bull market gently soothed my emotions, a charming sense of hope enveloping me. I eagerly pressed the buy button, well aware that speculative fervor would push my portfolio to new heights — at least until the excited crowd in the market wakes up from their intoxicating fantasies and curbs their optimism about a bright future, before the market's gravitational pull reasserts itself and dominates financial trends.

This round, the future depicted by various market promoters is one where AI Agents flourish everywhere, creating seemingly endless economic wealth. New tech giants in China and the US become the controllers of the new era, building the underlying framework on which AI relies for survival. They dominate the tech industry in prosperous areas of San Francisco and Hangzhou, absorbing all available capital in the market, attempting to create a utopian world in this realm — at least for corporate shareholders and the ruling system. And as capital becomes increasingly scarce, they will pressure the current political arena to increase the issuance of dollars and renminbi, further consolidating their discourse power in the industry.

Crowding to build an AI utopia is not the only wave of fervor at this time. There is another group, keen on constructing a global war machine. Why should the international order, led by the United States, be the only one to create chaos and conflicts? Major powers need top-tier military capacity to eliminate hostile forces because no one can expect the unpredictable leaders of other countries to come to the aid of so-called allies. Thus, each country will justifiably choose to print money to arm themselves, conscripting youth to the battlefield, to pursue a so-called glorious war whose reasons remain unclear.

Meanwhile, we have all become the losers of the era: there is a severe lack of investment in the production of necessities, while the obsession with bonds and stock assets under the imperial system grows. Once geopolitical conflicts sever global trade routes, the dollar savings held will be difficult to value. Outsourcing the production of necessities entirely may inevitably lead to famine and social unrest. The lower class will eventually take to the streets to defend their rights, exposing the hypocrisy of arrogant politicians.

In the eyes of politicians and their linked bankers, there are three irrefutable reasons supporting the reckless printing of money by central banks and commercial banks. The catalyst for accelerating credit issuance is the currently simmering conflict between the US and Iran. This dispute is merely a tragic drama of death and destruction once again enacted by those in power due to governance ideological differences, while also clearly affirming: AI and drones will dominate the future of warfare, and no country can merely rely on an internationally ordered framework led by the US to ensure stable circulation of global commodities.

In the AI arena, there is a high degree of consensus between China and the US: the high ground in AI development must be seized within their own territories, or they will fall into a long-term strategic passivity. Therefore, AI hegemony is directly linked to national security. For other countries, to stabilize the acquisition of food and energy under any circumstance, they must redundantly construct transportation networks and other infrastructure, while stockpiling fertilizers, grain, and energy supplies, instead of mindlessly increasing their holdings of US debt and stock assets.

Before the 2028 US presidential election, a convergence of multiple era issues will foster a political consensus on loose monetary issuance, allowing for an uncontrolled expansion of legal currency credit. And this round of crypto bull market officially kicked off after the US airstrikes on Iran on February 28.

I hope this text can awaken the bullish belief within you, breaking free to soar toward a profitable future. Meanwhile, many of the impoverished masses around the world are suffering from obstructed circulation of necessities due to war, enduring hunger in the shadows ignored by mainstream media.

AI Optimism Wave

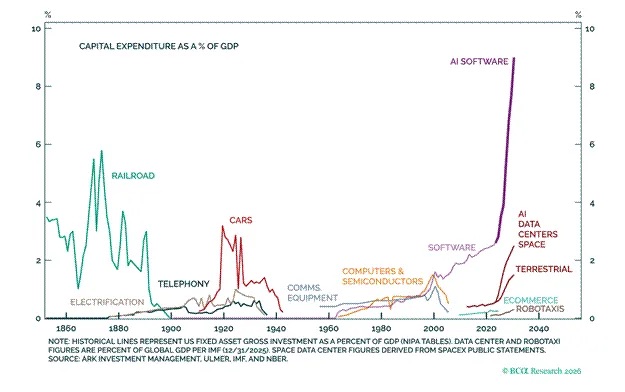

The global capital expenditure on AI model and Agent training and inference has reached an unprecedented scale in human civilization history. Many believe that this AI industry investment will create social value far exceeding any previous technological revolution. I agree, but human nature is often overly enthusiastic. There are no eternal extremes or perfection in the world, and people always tend to overdraw expectations, overinvest, and repeat constructions for an AI-led future.

Advocates of AI use nationalism to endorse massive industrial investment, covering up the inefficiency and waste of capital under the guise of national strategy. Patriotism should not be measured by a price tag. Leaders of both China and the US firmly believe that AI and technological hegemony are core lifelines to maintain their ruling structures. Technologists in both countries are also eager to amplify narratives of opposition, exaggerating threats from competitors in the AI field.

Objectively, both leaders have witnessed how the large-scale application of AI and drones can sway the outcomes of wars, and they fully accept this industrial competition logic. Therefore, both countries will prioritize the development of leading AI industries as top objectives in economic and military domains. This means that even if monetary policymakers are concerned that large-scale expansion of dollar and renminbi credit might trigger inflation, they cannot voice opposition. Central banks and commercial banks must unconditionally provide the capital needed for the tech industry.

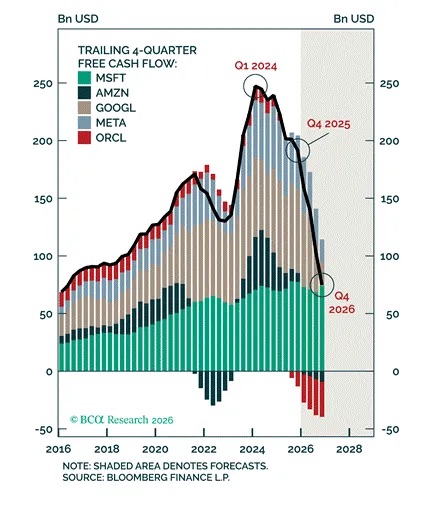

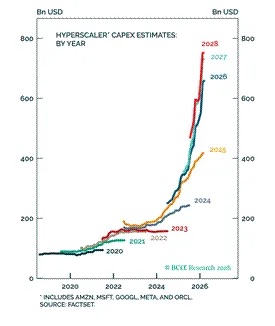

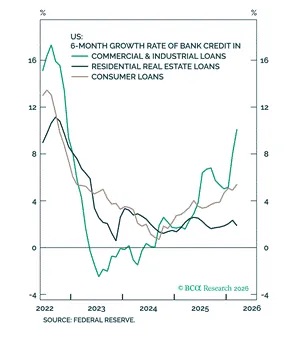

Currently, the AI capital expenditure in the US largely comes from the operational cash flows of leading profitable tech companies.

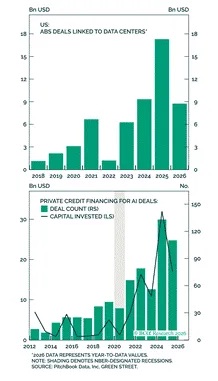

However, the scale of current and future industrial investments has long needed to rely on credit channels to expand funding supply.

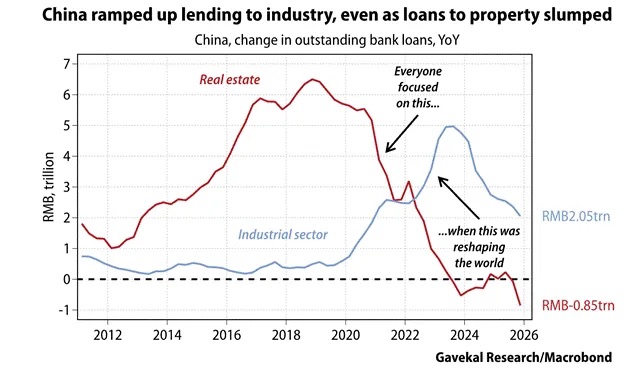

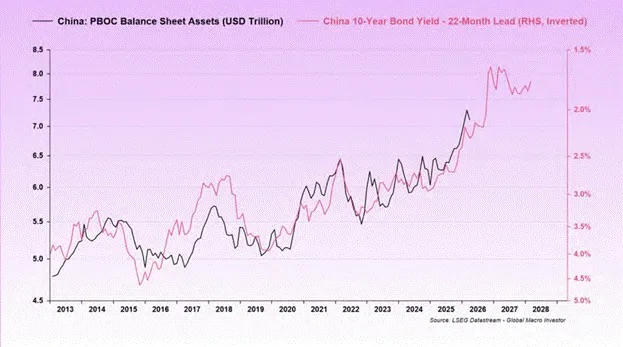

In China, policies have forced banks to reduce credit issuance in the real estate sector, shifting toward the tech industry.

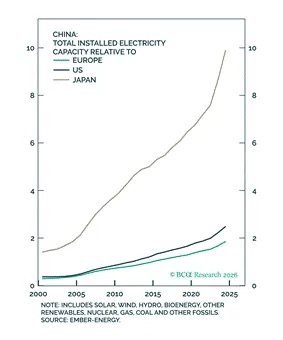

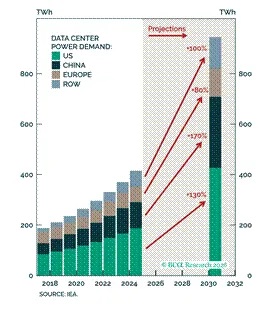

Besides capital investments related to data centers, both China and the US are also continuously ramping up power generation capacity.

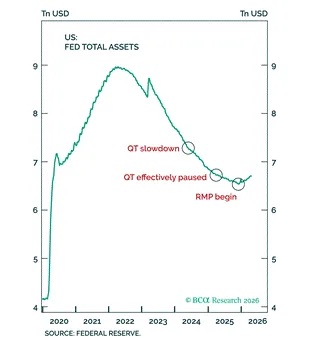

This is no longer just about commercial banks lending to AI or data center projects out of some patriotic mission. The Federal Reserve and the People's Bank of China are both increasing the issuance of legal currency and broadly relaxing the liquidity environment of financial markets.

The political demand to seize the AI track, combined with the financial demand to print money and support industrial development through credit, has created an excellent upward environment for cryptocurrencies. In the future, the total amount of legal currency will continue to increase, and as AI and power infrastructure capital expenditure surges each year, the rate of currency expansion will continue to accelerate.

As the cost of individual AI computing power continues to decline, the model complexity and the volume of tasks that AI Agents can handle will continue to increase, leading to exponential growth in computing power consumption, which is at the core of the paradox known as the "Mansfield Paradox." Additionally, there is the Red Queen effect — a company investing heavily to iterate its AI model will soon be surpassed by competitors’ technological upgrades, causing the initial investment to rapidly depreciate.

This forces the industry into an endless cycle of capital involution, as companies must continuously increase spending to develop cutting-edge models to crush competitors, ultimately resulting in hundreds of billions or even trillions in investments facing imminent devaluation. Due to these factors, unless an unexpected external market black swan occurs, the expansion momentum of AI capital expenditure will be unceasing.

When will this industrial frenzy come to an end?

I believe two things will nearly happen simultaneously, completely reversing the market’s perception of the necessity of trillion-level AI investment: first, a large IPO or super merger in the tech or AI sector will appear, with a scale unprecedented and an unstable financial logic that exceeds the market’s absorption capacity, shattering the atmosphere of industry fervor. At that time, people will start to reconsider whether the huge investment in developing AI is truly worth it. Once questioning becomes consensus, the industry bubble will burst.

Second, the campaign rhetoric of the Democratic challenger in the 2028 US election. Large-scale AI infrastructure will raise the costs of raw materials and labor, especially electricity prices, which are unpopular among American voters in many regions. Moreover, 90% of ordinary Americans do not hold substantial stocks and cannot share in the dividends of increasing stock prices of AI and related companies.

Therefore, a campaign platform that focuses on curbing the chaotic expansion of AI, returning to human values, and suppressing the inflation effect of infrastructure will easily gain public support. Even if the Democrats ultimately lose, it does not matter; such mainstream public opinion will lead capital institutions to begin to anticipate: in the future, the government may introduce policies to limit AI credit issuance and strengthen industry regulation, suppressing profit expectations for related companies.

But for now, the liquidity in the dollar and renminbi markets will continue to be loose, and both Bitcoin and the entire crypto industry will continue to benefit.

Countries Seeking Self-Preservation

Trump rashly airstriked Iran, completely disregarding the impact of the war on the global economy. Perhaps he was not without consideration, but this year’s optimistic expectation of a quick victory in this military action is evidently seriously detached from reality.

The US boasts rich energy and arable land resources; even if prices rise, local citizens will not face the risk of famine — the real crisis will only occur when politicians prioritize military spending over livelihood subsidies. However, citizens in Europe, Africa, and much of Asia are not so lucky.

The elite class in these countries previously misjudged the situation, naively believing that the US would take into account the plight of countries suffering from food and energy shortages and would not recklessly initiate conflicts in the Middle East that would disrupt commodity circulation.

Countries have previously over-relied on the US-led order, choosing to increase their holdings of dollar financial assets while neglecting the need to establish their own energy transport channels and trade routes. They also failed to stockpile essential goods in advance for emergencies.

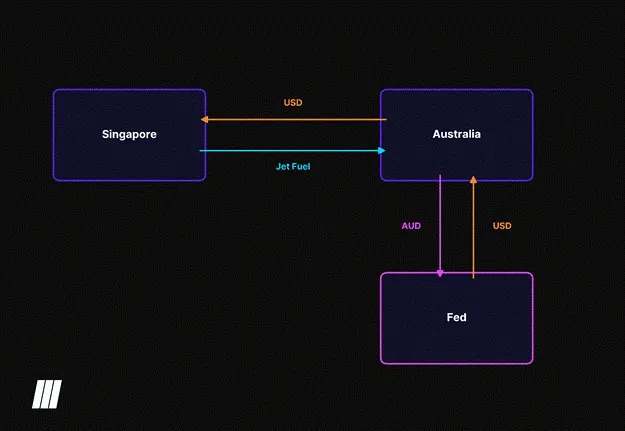

Marco Papic of BCA Research summarized this profoundly: this poses a huge hidden danger for other countries around the globe, as the entire world’s infrastructure layout has long been deeply tied to the US's geopolitical hegemony logic. Looking globally: Germany's air defense system is unable to cope with the threat from Russia, rooted in its reliance on US defense; many countries in the Gulf Cooperation Council have almost no alternative energy transport infrastructure and can only rely on shipping through the Strait of Hormuz, which is rooted in the US order framework; global manufacturing is highly concentrated in China, still designed around the US global structure; Australia's aviation fuel needs to be imported from South Korea, constrained by the US-led supply chain; Canada's infrastructure system heavily relies on US market demand, which also stems from the US hegemony structure.

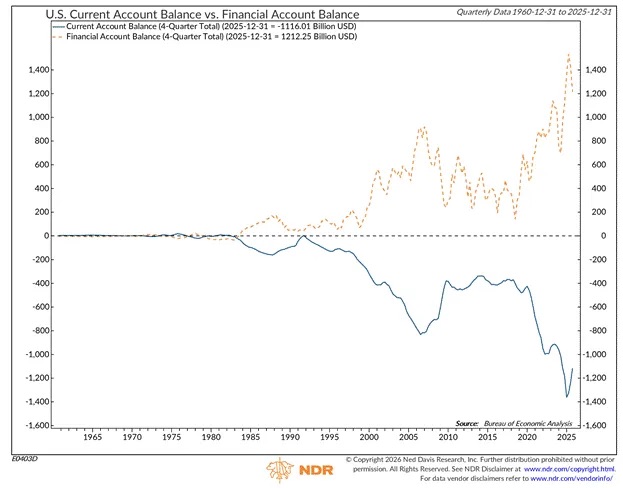

Global energy, defense, shipping, and manufacturing infrastructure have inherently been adapted to US geopolitical hegemony since their planning stages. This is reflected not only in the US’s long-term maintenance of a massive current account deficit — relying on an imperial economic structure that indiscriminately absorbs imported goods from around the world; but also in the global consensus to rely on the US's enormous defense expenditures to sustain an overall geopolitical macro layout. In short, the current global order is led by the US, and the US will go to war to defend this order at all costs.

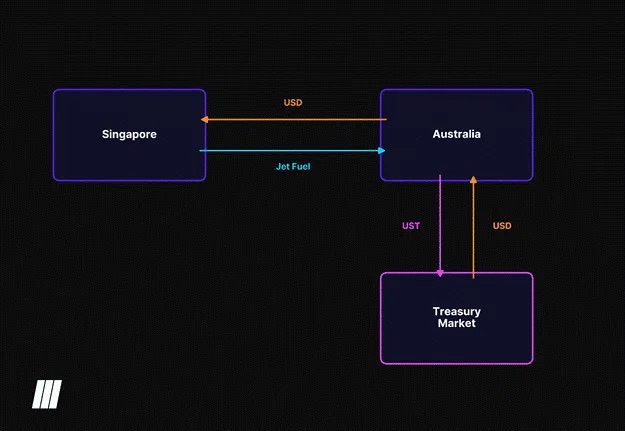

Bangladesh may face famine due to disrupted fertilizer exports from the Gulf and reduced grain production; Australia can only rush to Singapore for emergency procurement due to interruptions in fuel imports from China; Europeans are forced to give up low-priced Russian and Qatari oil and gas resources, instead purchasing high-priced American refined oil and liquefied natural gas.

All of this implies a complete restructuring of national sovereignty investment logic. When a war that is unrelated and unacknowledged by one’s self can sever food and energy supplies, holding US debt and S&P 500 index funds loses all significance. To compensate for strategic shortfalls, in the future, countries will marginally reduce their dollar assets and redirect capital towards infrastructure construction, defense layouts, and stockpiling essential goods.

The US hegemonic system relies on overseas capital's financial contributions to balance its own revenues and expenditures. Once foreign capital holds massive dollar assets and begins to sell off, it will directly impact the US financial market. The US has long relied on foreign capital to cover its huge current account deficits, and if the sell-off becomes uncontrolled, it could easily trigger a severe financial crisis.

The US Treasury Secretary and monetary policymakers are well aware of this, and currently, there are two major policy tools available to ease the crisis: expanding the scope of dollar swap limits and adjusting bank regulatory rules to compel financial institutions to increase their holdings of US debt.

If allied countries need funding for essential goods and infrastructure construction, the Federal Reserve or the Treasury can provide financing through dollar swap limits without directly selling off dollar assets and impacting the market, effectively using existing assets as collateral for liquidity borrowing. The UAE has previously applied for dollar swap limits for this reason. The landing of such credit tools will essentially further expand the total circulation of dollars.

The Passive Australia: Forced to Sell US Debt for Aviation Fuel

The Smart Australia: Borrowing Dollars from the Federal Reserve for Aviation Fuel Procurement

If the US market needs to hedge against ongoing sell-off pressure from various countries, it can also adjust bank regulatory rules to allow banks to increase their holdings of more US debt and stock assets under the same capital requirements. Optimizing leverage ratio regulatory rules is a step in that direction.

The global convention of allocating trade surplus reserves into dollar assets began with the US-Saudi petrodollar agreement in the 1970s, reaching its peak after the Asian financial crisis of 1997-1998. However, nowadays, holding dollar assets can no longer guarantee stable access to essential materials such as fertilizers and oil.

Countries need to focus on building domestic production capacity or cooperate with neighboring countries to establish supply chains to ensure the supply of basic materials. The era of just-in-time logistics, finely tuned for globalization, has already come to an end, and the era of strategic reserves for emergencies has officially arrived. This will become a long-term structural trend lasting for decades.

This also means that in the future, US monetary policy must maintain a liquidity environment more relaxed than normal to hedge against the market gap brought about by other countries reducing dollar assets and shifting toward physical infrastructure and material reserves.

Continuation of High Interest Rates and High Inflation

Wars inherently possess inflationary attributes, and the US-Iran conflict is no exception. Investments in AI infrastructure, global strategic reserves, and infrastructure booms have all become reasonable excuses for central banks and commercial banks to expand credit issuance. Politicians, due to practical needs and subjective considerations, tacitly approve and even support reckless money printing.

This is also the core reason why Bitcoin's performance has continued to lead gold, US tech stocks, and other mainstream risk assets since the outbreak of the war on February 28.

Post-war Bitcoin (gold), NASDAQ 100 index (magenta), US investment-grade tech ETF (white), gold (orange) performance

Bitcoin fell to $60,000 this year and, bolstered by massive liquidity of dollars and renminbi waiting to be released, returning to $126,000 is an inevitable trend.

Many skeptics are still unwilling to participate in this Bitcoin rebound, simply because its performance has significantly lagged behind tech stocks and gold over the past two years. Many even question whether Bitcoin still has value as a hedge against excessive currency issuance. But the market will ultimately witness that its sensitivity to the expansion of fiat currency liquidity is irreplaceable.

I predict that once Bitcoin breaks through $90,000, the pace of its rise will accelerate suddenly, entering an explosive stage; by then, a large number of options sellers will be forced to close positions due to price breaching the exercise price, further driving up the market. I cannot predict how high Bitcoin will eventually rise; unless a disruptive change occurs in the market, I will keep the Mansfield investment portfolio filled with risk exposure.

As the US midterm elections in November approach, the confrontation in the political arena regarding the AI industry and inflation issues will intensify, possibly causing a small pullback in the bull market. But looking deeper, the negative impact of high oil prices on Trump is far less than the outside world imagines.

California already has notable flaws in its energy policy and higher than average oil prices, making it difficult for the Republican Party to gain victory there; meanwhile, a $100 oil price and the reconstruction of energy industries in the Middle East and Venezuela would benefit the oil and gas-producing regions that support Trump.

Polling forecasts suggest that the Democrats have a 50% chance of gaining control of both the House and Senate, but even amid the US-Iran war, Trump still has plenty of time to court moderate voters and win public opinion. As long as citizens’ real income steadily rises, broad support can be gained. Opening up oil and gas extraction and developing the energy industry could push the S&P 500 index toward the 10,000-point threshold.

Now is the time to position in niche potential cryptocurrencies. In addition to our already heavy positions in Hyperliquid (HYPE) and Zcash (ZEC), I currently see the most potential in NEAR.

In my next article, I will elaborate on the logic: the privacy narrative combined with the NEAR smart intent ecosystem will bring positive cash flow to the protocol, completely reversing the long-standing sluggishness of the token’s trend and leading to a significant increase as it quickly pushes towards historical highs.

In the bull market, simply close your eyes and hold firmly. There will always be opportunities to sell and exit in the future, but that is not the time now. Go with the flow and seize the market dividend.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。