Since the end of 2022, when ChatGPT sparked a wave of artificial intelligence, the market's investment logic in AI has always revolved around the "Magnificent-7," especially those "super-scale enterprises" that dominate cloud computing infrastructure. However, the emergence of China's DeepSeek in early 2025, along with the ensuing fierce debate around the effectiveness of AI capital expenditures, is subtly changing this landscape. Investors are beginning to realize that the real "gold rush" may not only be found among these giants, but deeper within the industry chain that provides them with "shovels" and "tools."

From Doubts About "Arms Race" to Performance Validation

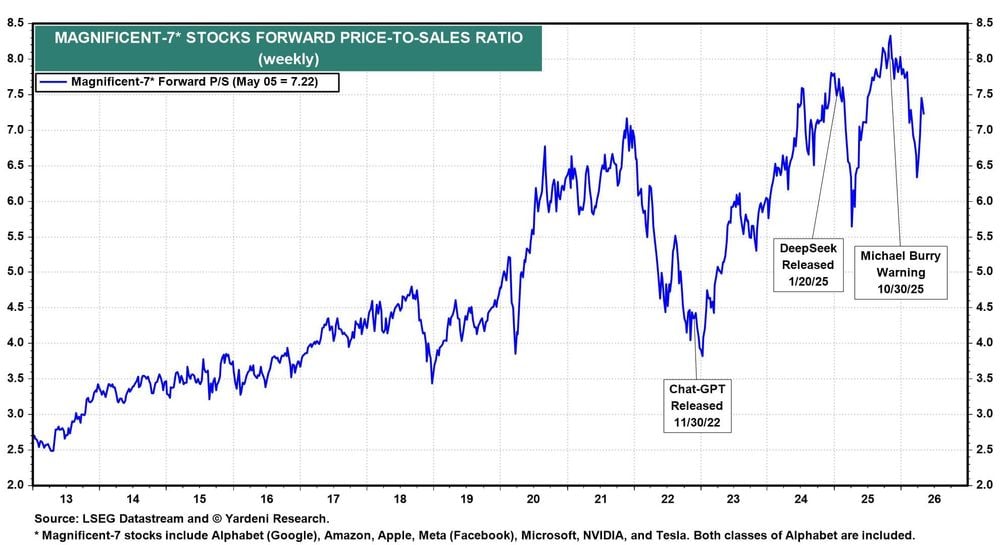

In the second half of last year, the market was engulfed by concerns over AI investment returns. Notable investor Michael Burry publicly warned that the vast AI capital expenditures of super-scale enterprises might not generate the expected profits due to various reasons, intensifying market fears of an AI bubble. At that time, the stock prices of the "Magnificent-7" were under pressure, and market sentiment turned cautious.

However, the earnings season in April this year provided a strong counterargument. The cloud computing business revenue of super-scale enterprises continued to exceed expectations, and the robust demand for "computational power" seemed to validate all previous massive investments. During my observations in the industry, I noted that market sentiment often turns after key data is announced. This time was no exception; the "hard data" of performance quickly quelled discussions about whether capital expenditures were excessive.

The "Certainty" Dividend of Capital Expenditure: The Explosion of the Semiconductor Industry Chain

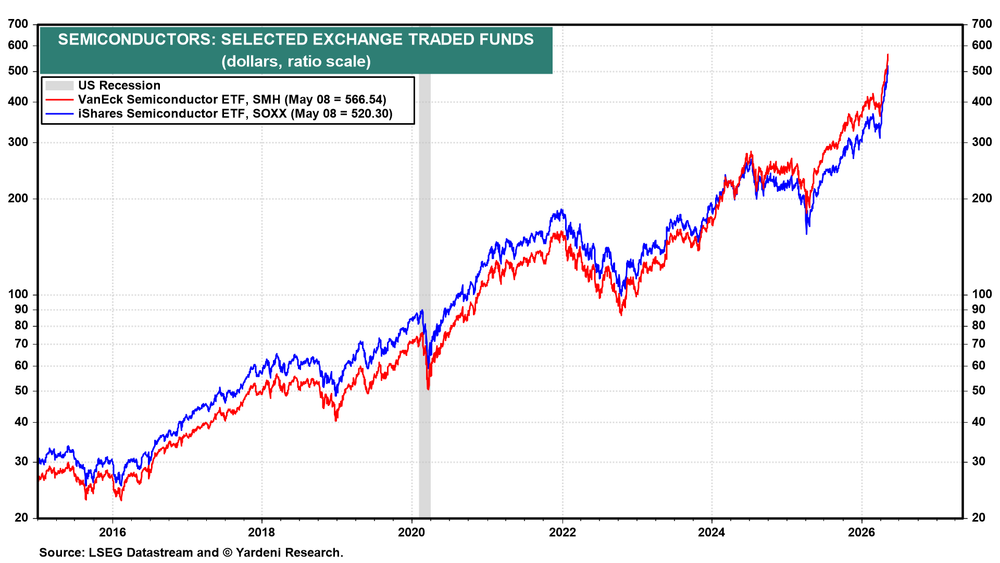

Although discussions about whether AI capital expenditures can ultimately lead to huge profits for super-scale enterprises are ongoing, a more certain logic has emerged: regardless of who the ultimate winner of AI applications is, this enormous capital expenditure will first convert into strong demand for semiconductors and AI-related components.

This judgment directly drove semiconductor-related ETFs to reach historical highs in April. From a professional perspective, this is a typical "shovel sellers" logic—when a gold rush occurs, those selling shovels often reap rewards first and most definitely.

Memory Chips: The Real Bottleneck of AI Training

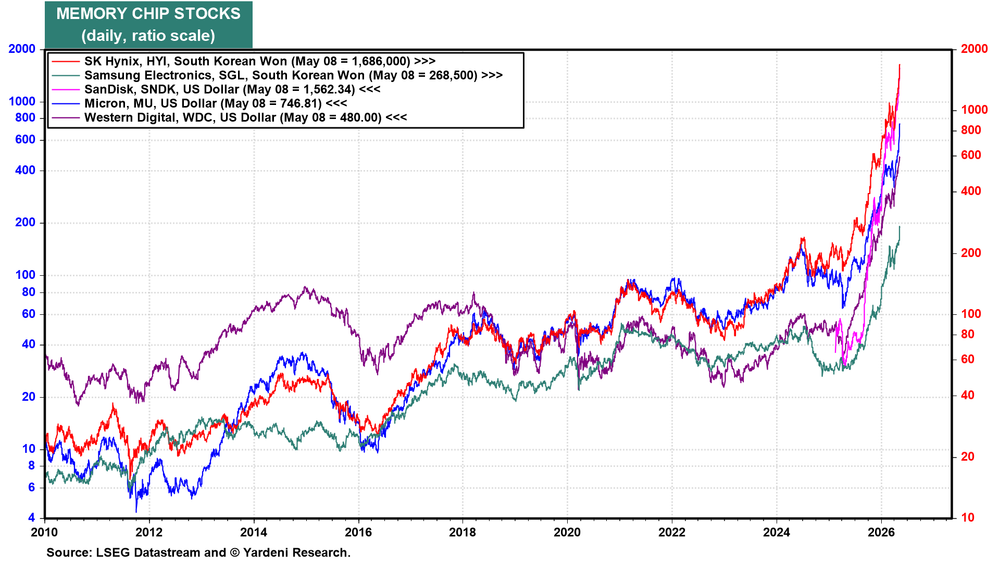

In this round of semiconductor rise, memory chip companies have stood out prominently. Storage giants in the U.S. and South Korea—SK Hynix, Samsung, SanDisk, Micron Technology, and Western Digital—have all seen significant stock price increases. I pointed out in March that high bandwidth memory (HBM) is the real "bottleneck" in the AI training process. As long as AI's demand for computational power continues to outstrip supply, the growth momentum of these companies is unlikely to be shaken.

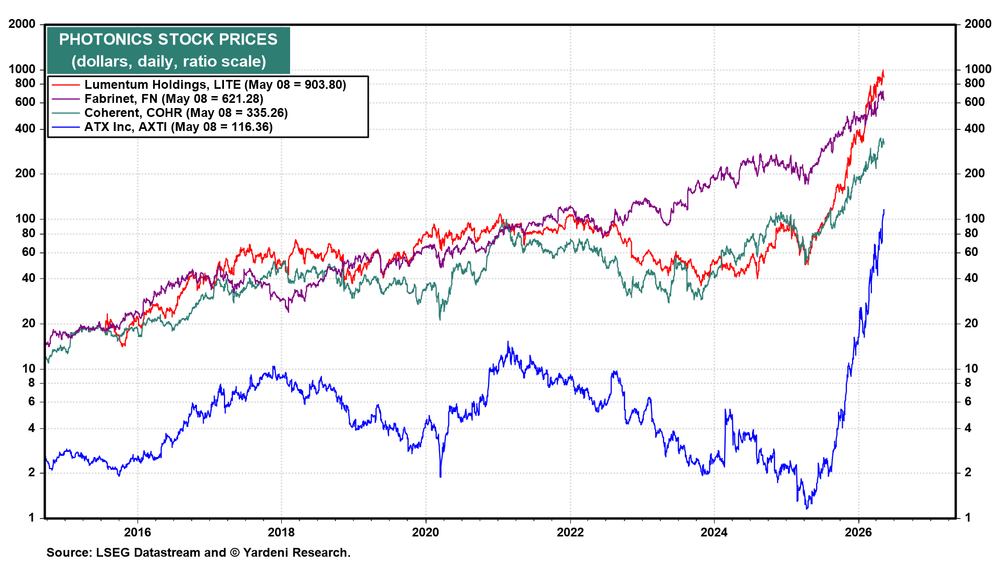

Photonics and the Wider Semiconductor Ecosystem

In addition to memory chips, photonics companies have also performed impressively. Optical interconnect technology plays a crucial role in high-speed data transmission within AI data centers, and its importance is being revalued by the market.

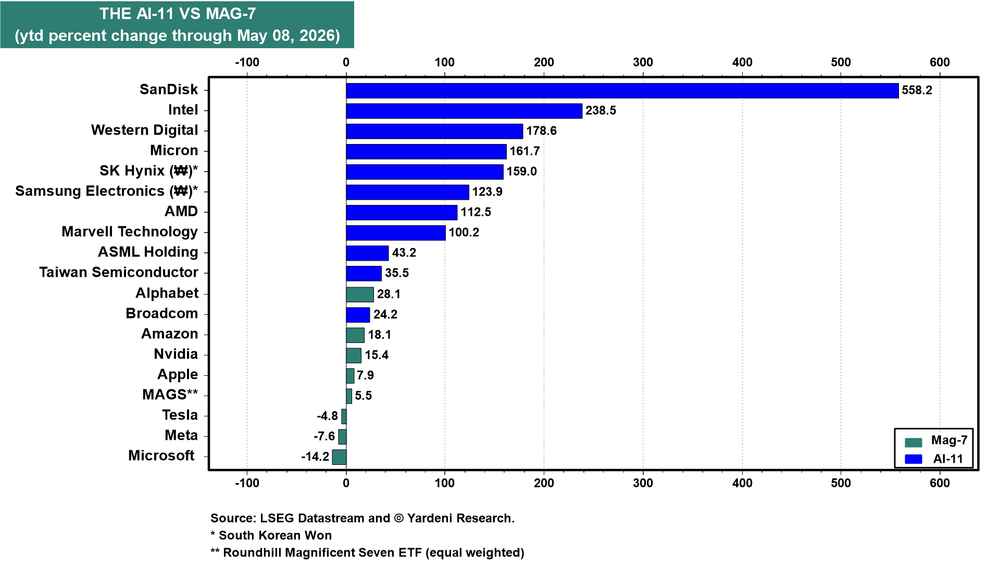

Investors have clearly concluded: the opportunity for AI investment is by no means limited to the "Magnificent-7." As of this year, among the "AI-11" semiconductor stocks we track, nearly every one has outperformed the members of the "Magnificent-7," except for Broadcom.

Insight into the "AI-11" Supply Chain: Where Every Dollar Goes

Understanding the next opportunity in AI investment hinges on seeing how capital flows through this supply chain. Below are the core links of the "AI-11" I have outlined:

1. Foundry and Lithography (TSMC, ASML)

TSMC provides foundry services for all leading logic chips and is the undisputed cornerstone of the industry. ASML monopolizes extreme ultraviolet lithography (EUV) equipment, an indispensable "checkpoint" for manufacturing cutting-edge chips.

2. Logic and Custom Chips (AMD, Broadcom, Intel)

AMD is rapidly gaining market share in the field of AI inference. Broadcom is a core partner for customization of ASIC chips for super-scale enterprises, dominating in the networking chip domain. Marvell complements the landscape of custom chips, networking, and optical connections. Intel is telling its "revival story" about its foundry business and benefiting from AI server cycles' demand for CPUs.

3. Memory Chips (Micron, SK Hynix, Samsung)

These three giants supply the real "hard currency" in AI training—high bandwidth memory. SK Hynix currently leads the global HBM market.

4. Enterprise-grade NAND and Storage (SanDisk, Western Digital)

SanDisk has become a pure beneficiary of enterprise-grade NAND flash memory and solid-state drives (SSDs). Western Digital provides large-capacity hard disk drives (HDDs) as a supplement.

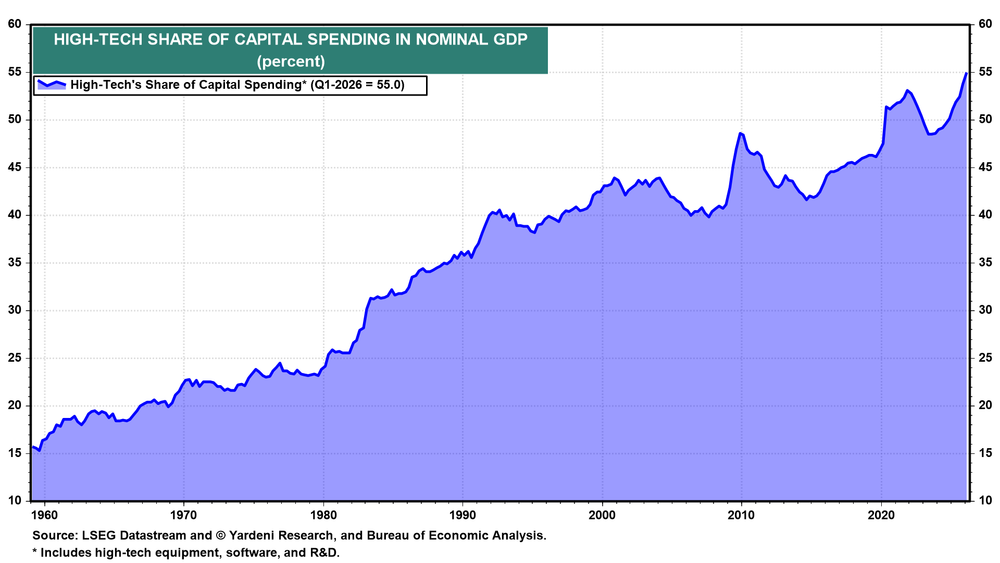

Every dollar of capital expenditure on AI infrastructure by super-scale enterprises must pass through this complete supply chain before reaching the server racks. This explains why the high-tech sector now occupies a record level of 55% of U.S. corporate capital expenditures.

The Dominance of the "Magnificent-7" Persists, but Marginal Growth is Shifting

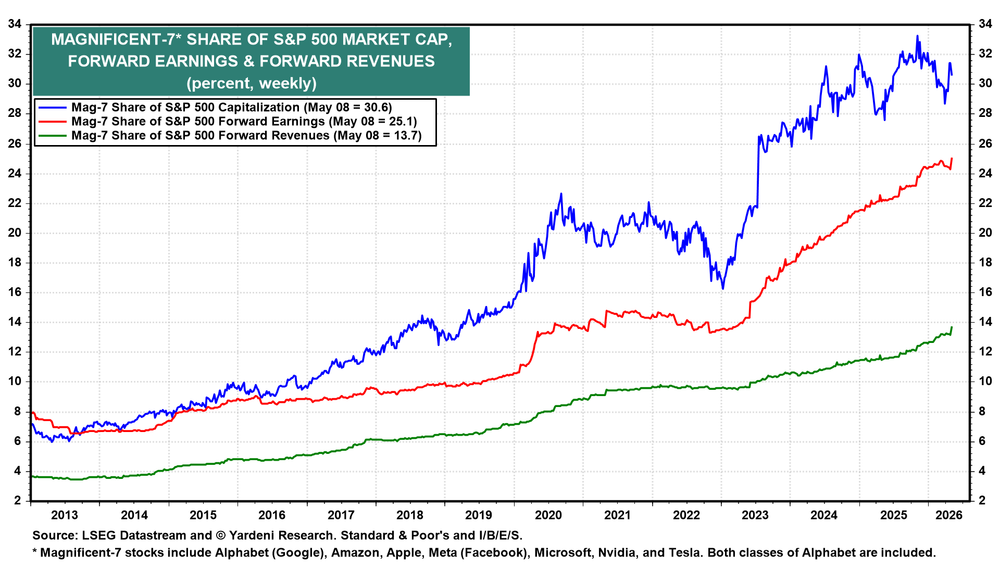

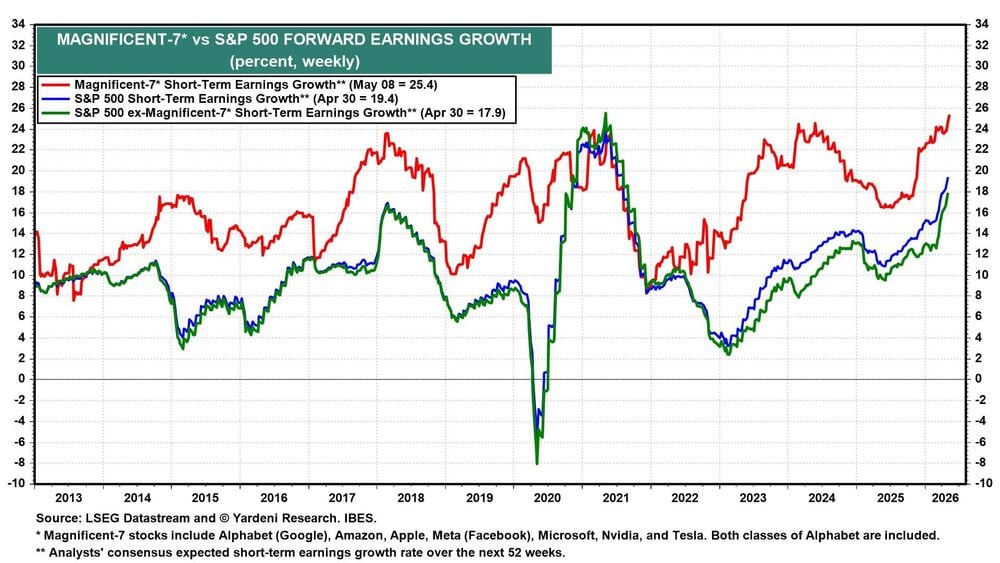

It is undeniable that the "Magnificent-7" still dominate the S&P 500 index. Together, they account for 30.6% of the index's market capitalization, 25.1% of forward earnings, and 13.7% of forward revenues. The strong fundamentals represented by this label still exist.

However, marginal changes are occurring. The current forward earnings growth rate for the "Magnificent-7" is 25.4%, while the S&P 500 index excluding the "Magnificent-7" (the "S&P 493") stands at 17.9%. This gap has significantly narrowed compared to a year ago. The "S&P 493" is catching up in this growth race. The premium once granted to the "Magnificent-7" due to the scarcity of earnings growth is becoming less significant as growth begins to spread more broadly.

I believe the market has adequately priced the dominance of the "Magnificent-7." The marginal funds that investors focus on are shifting towards fields that can extend the AI narrative beyond the initial seven companies.

Conclusion: From "Betting on Winners" to "Investing in Certainty"

Looking back at the evolution of the AI investment logic, we can clearly see a main thread: transitioning from the initial "betting on which giant will win" to "investing in the most certain links of the industry chain." The certainty of AI capital expenditures has brought unprecedented prosperity to the semiconductor supply chain. For investors, understanding this shift from the "demand side" to the "supply side" may be key to grasping AI investment opportunities in the coming years. Of course, any investment decision needs to consider one's own risk tolerance, as market uncertainties always exist, but understanding industry logic is the first step towards making informed decisions.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。