Author: Claude, Deep Tide TechFlow

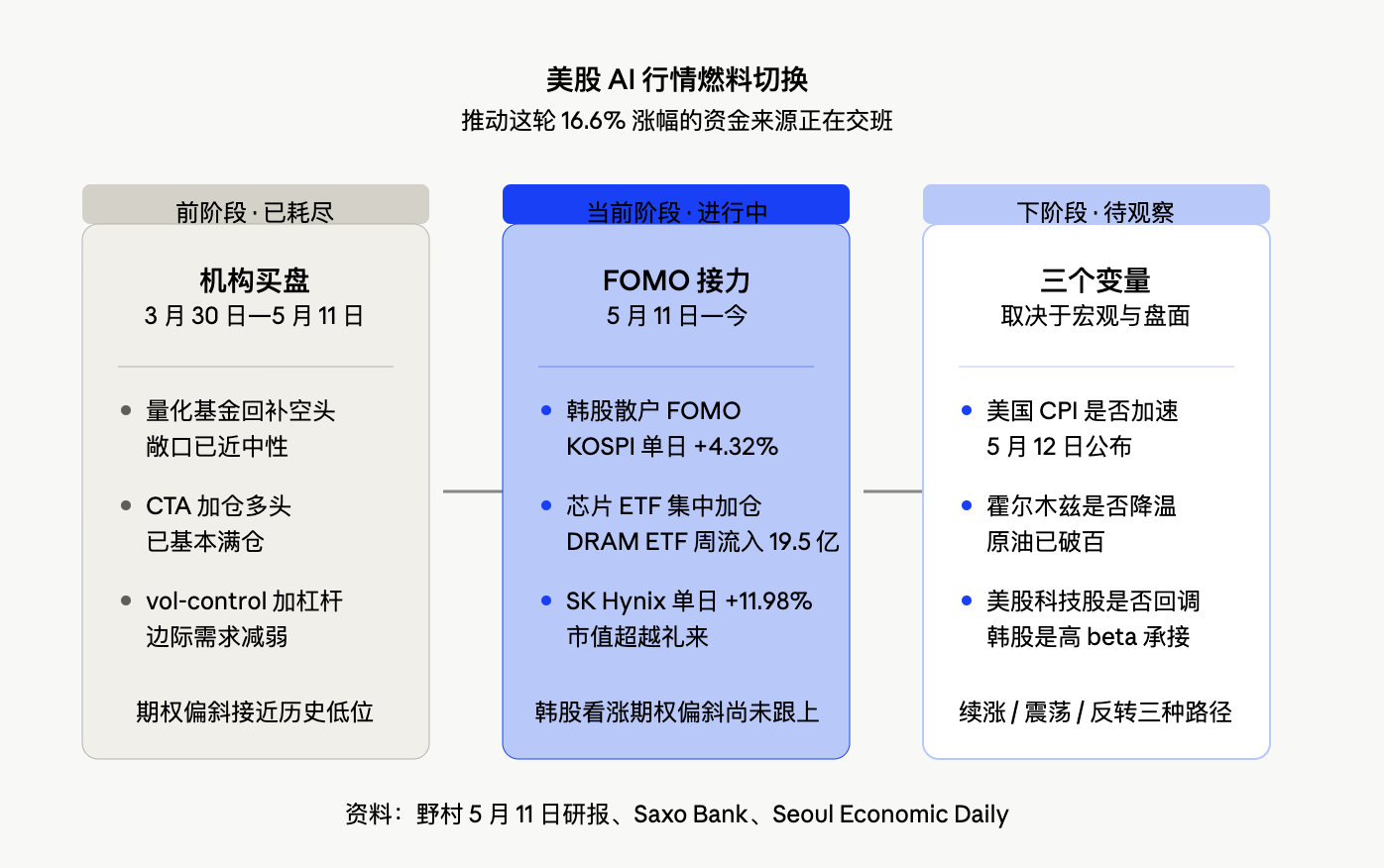

Deep Tide Overview: Nomura's research report released on May 11 throws out a key judgment: "At least in terms of US stocks, the AI market may be taking a breath." On the same day, KOSPI surged 4.32% to 7822.24 points, triggering a buy-sidecar during the day, with SK Hynix soaring 11.98%, its market value surpassing Eli Lilly for the first time to become the 14th largest globally. The report's judgment that "the next leg looks to the Korean FOMO" almost coincided with the surge in Korean stocks. The impetus for AI trading in US stocks is shifting from "shorts being squeezed" to "retail FOMO."

The AI market in US stocks has not ended. The S&P 500 has accumulated an increase of about 16.6% in 28 trading days, but where the money driving the index comes from and how much fuel there is left for pushing the prices up is undergoing subtle changes. Nomura's assessment is that the phase driven by short covering and institutional replenishment is nearing its end; if AI trading is to continue, a new wave of funds must take over. The Korean market used as a case study on the day of the report's release demonstrated this, with KOSPI crossing 7000, 7400, and 7800 points within a week, and retail investors falling into "hynix FOMO," with overseas funds concentrating on increasing positions in chip stocks through DRAM ETFs. The narrative is shifting from the Nasdaq to KOSPI.

Everything seems normal in US stocks, but the abnormal combination of "spot up/volatility up" has been triggered

The surface reading of AI trading in US stocks still appears enthusiastic. Saxo's options briefing on May 11 showed the VIX closing at 17.19, up 0.64% for the day. This reading is below historical averages, but the fact that the VIX is rising even as the index hits record highs is itself an abnormal signal. The CBOE SKEW index rose to 138.21 (+1.54%), and the VVIX, which measures VIX volatility, rose to 96.78 (+3.39%), indicating that institutional investors have not let go of their hedges even as the index reaches new highs.

Nomura’s report on May 11 described this combination as an "abnormal situation" for US tech stocks. The report pointed out that the Nasdaq is showing a combination of "spot up, volatility also up," with the VIX continuing to decline while the VXN (Nasdaq volatility) is rebounding significantly; the skew of US tech stock options (the difference between the implied volatility of 25-delta put options and that of 25-delta call options over one month) has quickly dropped close to historical lows, returning to levels seen around October 2025. This decline in skew indicates that the premium for put protection relative to call options has been suppressed, making market pricing for tech stocks' upside more crowded.

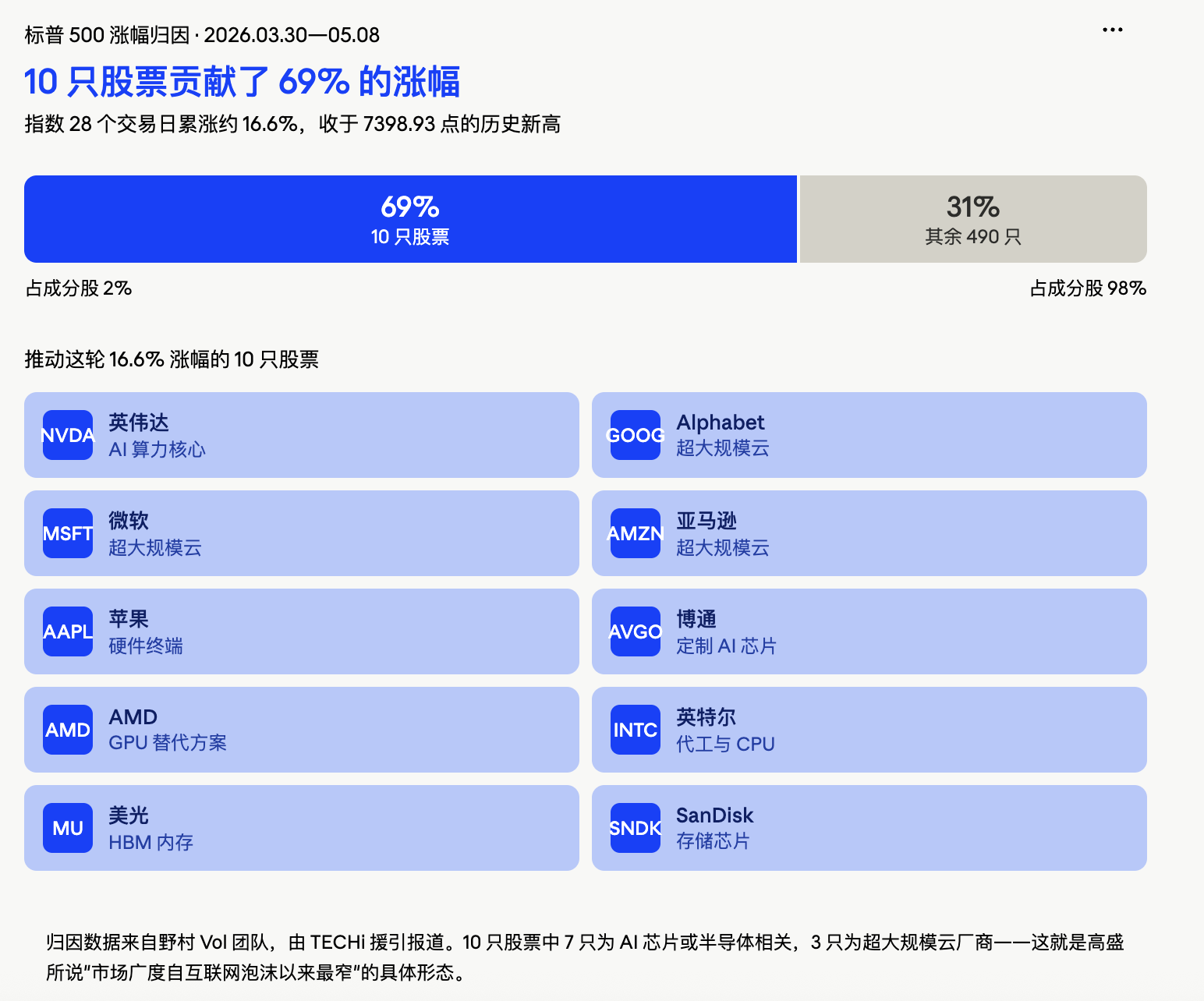

More attention should be paid to the structure of this rally. According to TECHi citing Nomura's Vol team’s contribution attribution chart, about 69% of the S&P 500’s 16% increase since March 30 was contributed by 10 stocks: Alphabet, Nvidia, Amazon, Broadcom, Intel, Micron, Apple, AMD, Microsoft, and SanDisk, while the remaining 490 constituent stocks only contributed 31%. Goldman Sachs' head of US stock strategy, Ben Snider, also pointed out that the current market breadth has shrunk to one of the narrowest levels since the dot-com bubble. "The big push on AI" and "Iran conflict" have been identified by Goldman as the two clearest risks to the stock market in the coming weeks.

Shorts have been fully squeezed, who will push the next leg?

The real killer judgment in Nomura's report is not the "abnormal combination" itself, but the dissection of the capital side: the stock exposure of quantitative funds has returned to near neutral. The previous forced buying to cover shorts has basically been completed. CTA (Commodity Trading Advisor) funds have largely returned to being fully long, and the marginal demand for volatility control strategies is also weakening.

In other words, the three main buy forces that have pushed AI stocks in recent weeks — shorts being squeezed, CTA increasing positions, and volatility falling driving vol-control leverages — are now nearing their limits. If AI stocks are to continue rising, they can no longer rely mainly on the force of "shorts being squeezed to buy."

It should be noted that Nomura's estimates of the positions of quant funds, CTAs, macro funds, etc., are based on model calculations, not measured positions. This means it is more suitable as a temperature gauge for marginal changes rather than an accurate position report. However, even so, the direction is clear: the algorithmic buying from the institutional end is nearing its limit, and further upward momentum must depend more on retail and emotion-driven funds.

Goldman's trading desk aligns closely with Nomura's judgments. Rich Privorotsky, head of Goldman's One-Delta trading desk, previously described the current rhythm as "semi-irrational chasing," and drew a parallel to 1999 when telecom equipment orders were surging, providing an "entity bottleneck narrative," similar to the logic of AI computational power scarcity today. Goldman's volatility trading desk has categorized the recent situation as "spot up, volatility up," which has restricted further accumulation space for systemic strategies.

This judgment means that the AI trading in US stocks hasn't collapsed, but the script of "continuing to push up by squeezing shorts" is nearing its end.

Korean stocks provide the answer: On the day Nomura’s report was released, KOSPI surged 4.32% triggering a buy-sidecar

Another judgment in Nomura's report is: If AI trading is to have another phase, the real continuation signal will depend on whether Korea shows FOMO again.

On the day the report was released, the Korean market responded with an extreme explosion. KOSPI closed at 7822.24 points, up 4.32% for the day, reaching 7899.32 points during the day, triggering a buy-side car. SK Hynix rose 11.98% to 1.888 million won, its market value surpassing Eli Lilly for the first time to become the 14th globally; Samsung Electronics rose 6.33% to 285,500 won, with the combined market value of the two companies exceeding 300 trillion won, accounting for nearly half of KOSPI's total market value. The combined market value of the Korean stock market and KOSDAQ surpassed 700 trillion won for the first time, just 8 trading days after breaking through 600 trillion won on October 27.

During trading on May 12, KOSPI further broke through 3900 points (i.e., the 7900 points level), setting a new historical high. However, same-day data revealed another side of FOMO: Among the 948 stocks in the KOSPI market, only 186 rose while 696 fell; about 30% of the constituents have cumulatively declined this year. The gains were entirely concentrated in the two semiconductor heavyweight stocks, Samsung and SK Hynix.

Retail FOMO has already formed a new market vocabulary. Korean financial media described the split mindset of retail investors using the term "hynix FOMO," with one side having "if only I had bought at 800,000 won" regret, and the other side experiencing anxiety about "should I jump in now" and "a correction is coming soon." A lot of discussions about "Samjeon-nix" (a combination of Samsung + Hynix) have emerged in the retail community. This is a typical retail-driven chase pattern, highly consistent with Nomura's definition of "FOMO signal."

The flow of overseas funds is even more illustrative. According to a report by the Seoul Economic Daily on May 10, iShares MSCI Korea ETF (EWY) saw a net outflow of $1.0145 billion during the period from May 1 to 7, which indicates that passive funds are withdrawing from the Korean market. However, at the same time, Roundhill Active DRAM ETF saw a net inflow of $1.9538 billion during the same period, with SK Hynix accounting for 25.94% and Samsung Electronics 21.62% of this ETF, totaling about 48%. Overseas funds are not selling Korea but are selling broad indices and buying chips, which is precise accumulation of the AI theme.

However, there is one detail worth staying vigilant about. Nomura noted in its May 11 report that KOSPI 200 also exhibited "spot up, volatility up," but the skew of call options did not rise, which does not appear to be a volatility expansion driven by demand for chasing call options. In other words, as of the point of the report's release, the Korean market had not yet entered the typical "fear of missing out, rushing to buy call options" state. Whether this signal will quickly reverse after KOSPI's surge on that day will be key to judging the sustainability of FOMO.

The Korean stock market is an extension of the US stock AI capital expenditure chain; how long the next leg can be sustained depends on the "pyramid top"

The FOMO in the Korean stock market is not an isolated event; it is essentially a high beta extension of the US stock AI capital expenditure story.

Data can directly anchor this transmission chain. According to estimates by Bridgewater, Alphabet, Amazon, Meta, and Microsoft are projected to invest about $650 billion in AI-related infrastructure by 2026. Goldman Sachs cited data indicating that the consensus for capital expenditures of the largest cloud infrastructure companies jumped by $130 billion in the last quarter, reaching $670 billion, which is over 90% of these companies' expected operating cash flow. Microsoft’s capital expenditure for the third fiscal quarter reached $31.9 billion, while Alphabet disclosed property and equipment purchases of $35.7 billion in Q1, and Meta raised its capital expenditure guidance for 2026 to a range of $125 billion to $145 billion.

This capital flows into data centers, GPUs, memory, networks, power systems, and cloud capacity. SK Hynix and Samsung are sitting at the core of this capital flow, with HBM4 memory and HBM high-bandwidth storage being snatched up by large cloud vendors. According to a report by Reuters, SK Hynix has recently received "unprecedented" order proposals from large tech companies, with some clients proactively expressing willingness to finance new production lines and ASML lithography machines. Chip production capacity is nearly exhausted. This is why the narrative of KOSPI's one-day 4.32% surge is completely self-consistent, as the Korean stock market is essentially the "second derivative" of the US stock AI story.

However, this linkage also means vulnerability. Once US tech stocks show a complete reversal, Korean stocks will be the high beta assets that bear the most direct selling pressure. Another risk path noted by Nomura is that rising inflation could force global central banks to take a more hawkish stance; this week’s (May 12) US CPI is a key event, and the current option market's premiums for this event remain low, indicating the market has not paid a high insurance premium for this risk.

There is also a variable macro backdrop: the Strait of Hormuz. WTI crude oil closed at $100.09 on May 8 (+4.89%), and Brent crude at $105.66 (+4.31%), with conflicts near the Strait of Hormuz escalating. Nomura’s judgment is that as long as the Strait remains obstructed and the US and Iran still disagree on ceasefire conditions, the AI-dominated market environment may last longer than expected. Energy price fluctuations will boost inflation expectations but will also make the market less willing to step away from "the AI story that can make money."

Putting the above clues together, the phase of US stocks' AI market driven by "squeezing shorts" is nearing its end; Korean FOMO has been ignited, with retail and overseas chip ETFs increasing positions synchronously, but the options skew has not caught up; how long the next leg can be sustained depends on whether US tech stocks pull back, whether US CPI signals accelerating inflation, and whether the Strait of Hormuz ultimately cools down. The judgment framework of Nomura's report has been repeatedly validated by market actions, Seoul is becoming the latest epicenter of this wave of AI trading.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。