Pressure at the level of centralized exchanges will only cause liquidity to emerge from elsewhere.

Written by: Thejaswini M A

Translated by: Luffy, Foresight News

When someone deliberately prevents you from seeing something, you instantly become curious and can't help but want to understand it. Barbra Streisand once tried to remove photos of her mansion from the internet. Before the lawsuit, only 6 people had downloaded this photo; after the legal storm, nearly 500,000 people viewed and spread it. This is the famous Streisand Effect and one of the most consistently proven principles in the history of information dissemination.

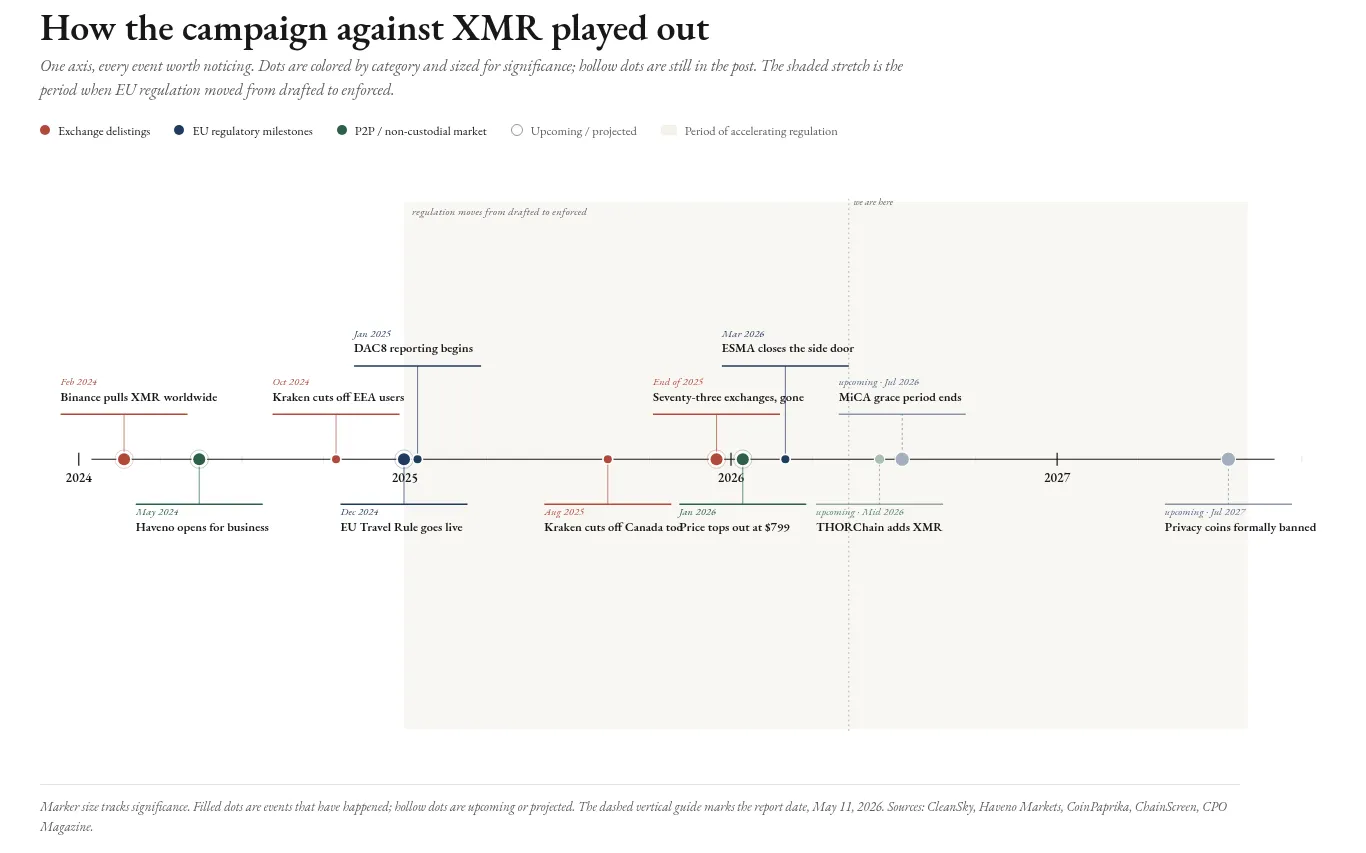

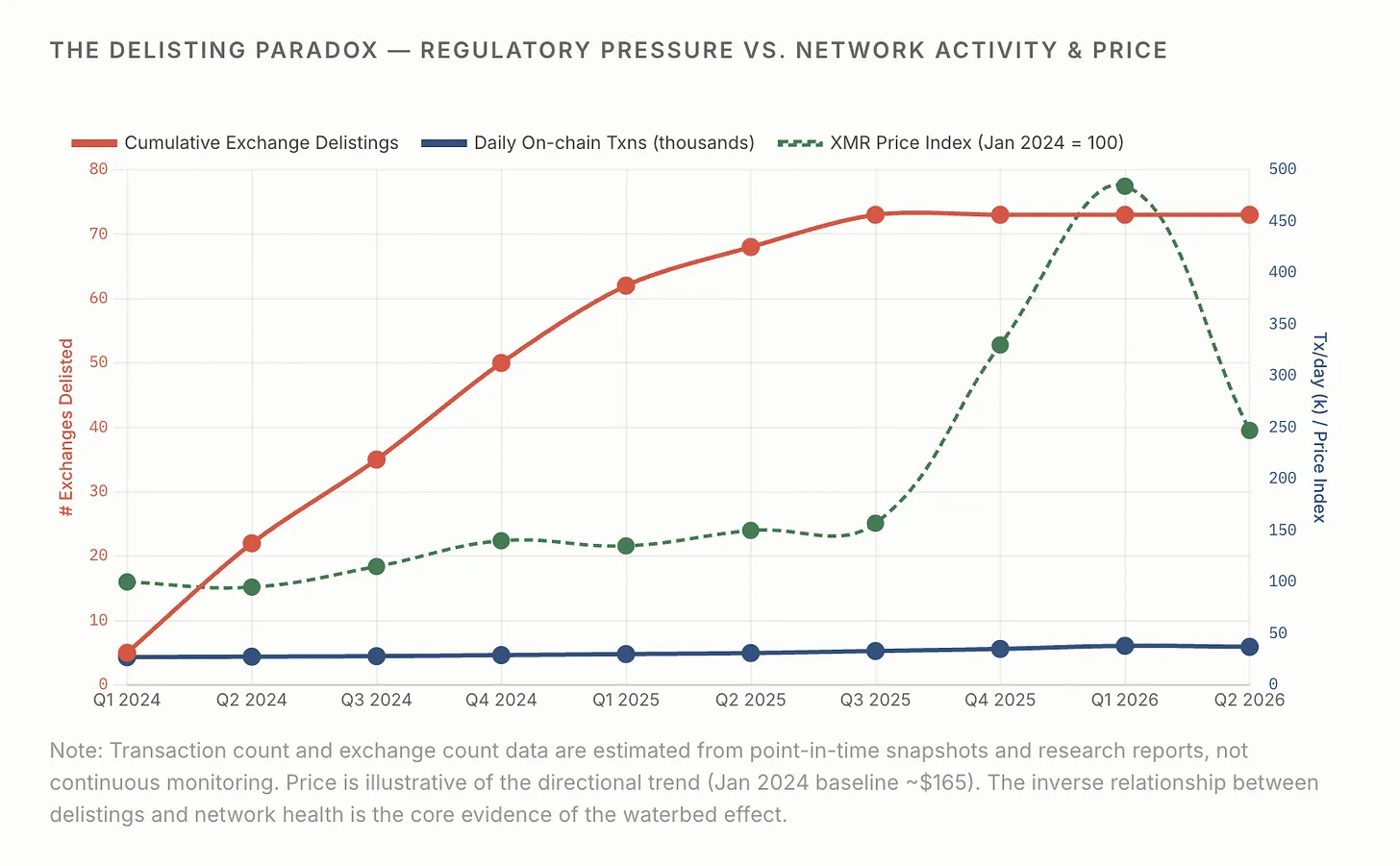

European regulators have continuously pressured major exchanges to delist Monero for two years, and 73 exchanges have complied. However, in January 2026, Monero hit a price high not seen in eight years. I didn't predict this outcome either; any logically consistent regulatory theory could not explain this anomalous trend.

According to conventional logic, when cryptocurrencies are delisted from mainstream exchanges, liquidity dries up, prices drop instantly, and the projects gradually fade from view, becoming footnotes in an industry unable to withstand regulatory pressure. This logic is deeply ingrained, and exchanges even use delisting as a bargaining chip to intervene in project governance, causing major projects to be wary of it.

On January 14, 2026, Monero reached an all-time high. I am not saying that regulators should have consulted Wikipedia in advance, but they certainly overlooked the most basic common sense principles.

The EU's Markets in Crypto-Assets Regulation (MiCA), Travel Rule, and DAC8 Anti-Money Laundering Bill are all based on the same set of regulatory logic: by imposing control on centralized exchanges where cryptocurrencies connect with traditional finance, the underlying cryptocurrencies can lose their space to survive. This rule works for most coins, but Monero is the exception.

Let's start with the underlying principles.

Monero is a cryptocurrency that defaults to transaction privacy. All on-chain transactions of Bitcoin are completely public and traceable; any address, transfer amount, and fund flow are fully visible. In contrast, Monero hides the sender and amount through ring signatures, stealth addresses, and a mechanism called RingCT.

The on-chain forensics agency Chainalysis has publicly admitted that it cannot extract valid traceable data from Monero's private transactions. The inability to trace by regulators is the core reason for Monero's delisting. Ironically, the large-scale delisting itself has become a form of strength certification: Monero's privacy technology is mature enough that regulators are powerless to monitor it and can only choose to cut off ordinary users' trading access.

Now let's look at the actual results brought by the large-scale delisting.

The decentralized non-custodial peer-to-peer trading platform Haveno was specifically designed for XMR trading and launched in May 2024. By May 10, 2026, the platform had completed a total of 24,018 transactions, with a total transaction volume of 921,585 XMR, which equates to approximately $374 million at average prices. Haveno did not exist before the regulatory delisting wave; its birth was precisely to fill the market gap left by the exit of compliant exchanges.

During the delisting regulation period, the total on-chain trading volume of Monero increased by about 30%-35%. At the beginning of 2024, the average daily transactions were only 25,000 to 30,000, while by the beginning of 2026, it had risen to 35,000 to 40,000 transactions, with a monthly transaction volume of about 800,000. The overall network ecology remained robust and positive, resembling more an active migration of asset settlement channels rather than a decline of the project.

On the day after Monero set its historical high on January 14, Felix Protocol launched the XMR/USDC perpetual contract market on Hyperliquid, without the need for community governance voting, exchange approval, or regulatory permission. On the launch day, the total open interest for XMR futures across the network reached a record of $275 million, with the coin price rising 6% in one day and trading volume surging 13%.

As of May 2026, the open interest for XMR on the Hyperliquid platform reached $36.37 million, surpassing Binance and BitMEX before delisting, making it the largest Monero trading market in the world. It is a decentralized exchange that does not require KYC or regulatory license constraints.

This is a typical waterbed effect: when you press down hard in one place, the pressure will rebound out from another. The regulatory delisting of Monero became the most vivid example. Regulators attempted to ban Monero by pressuring centralized exchanges, but the market merely completed the spontaneous transfer of trading grounds.

Regulatory efforts to forcibly cut off custodial trading channels inadvertently stimulated the growth of a non-custodial crypto ecosystem. The development of Haveno, atomic swaps, and peer-to-peer trading markets to their current scale is essentially an inevitable result driven by market demand. The regulatory pressure initially intended to stifle the Monero market ended up establishing a solid and long-term underlying infrastructure for it, a wonderful accident.

Before the wave of delisting regulations, regulatory agencies still had a certain degree of control, allowing them to monitor the order books of compliant exchanges, rely on fiat deposit channels for KYC tracing, and utilize exchange data to analyze fund flows. After the forced delisting, these monitoring tools instantly became ineffective. Fiat exchange channels turned to peer-to-peer trading under the Tor network, price discovery functions shifted to the unpermissioned decentralized exchange ecosystem, and regulators completely lost their tracking visibility.

Article 79 of the EU's Anti-Money Laundering Regulation (AMLR) explicitly prohibits anonymous cryptocurrency accounts and will take effect on July 10, 2027; the transitional period for MiCA regulations will also end in July 2026. Existing signs indicate that every round of regulatory implementation and enforcement escalation will not only fail to curb Monero but will also accelerate its infrastructure migration process. Every user expelled from compliant custodial exchanges will deeply root themselves in the non-custodial peer-to-peer ecology. By the time the comprehensive ban lands in 2027, this non-custodial ecology will have already undergone three years of accumulation, with foundations increasingly solidified.

Regarding the claim that "Monero no longer needs exchanges," it is necessary to clarify objectively.

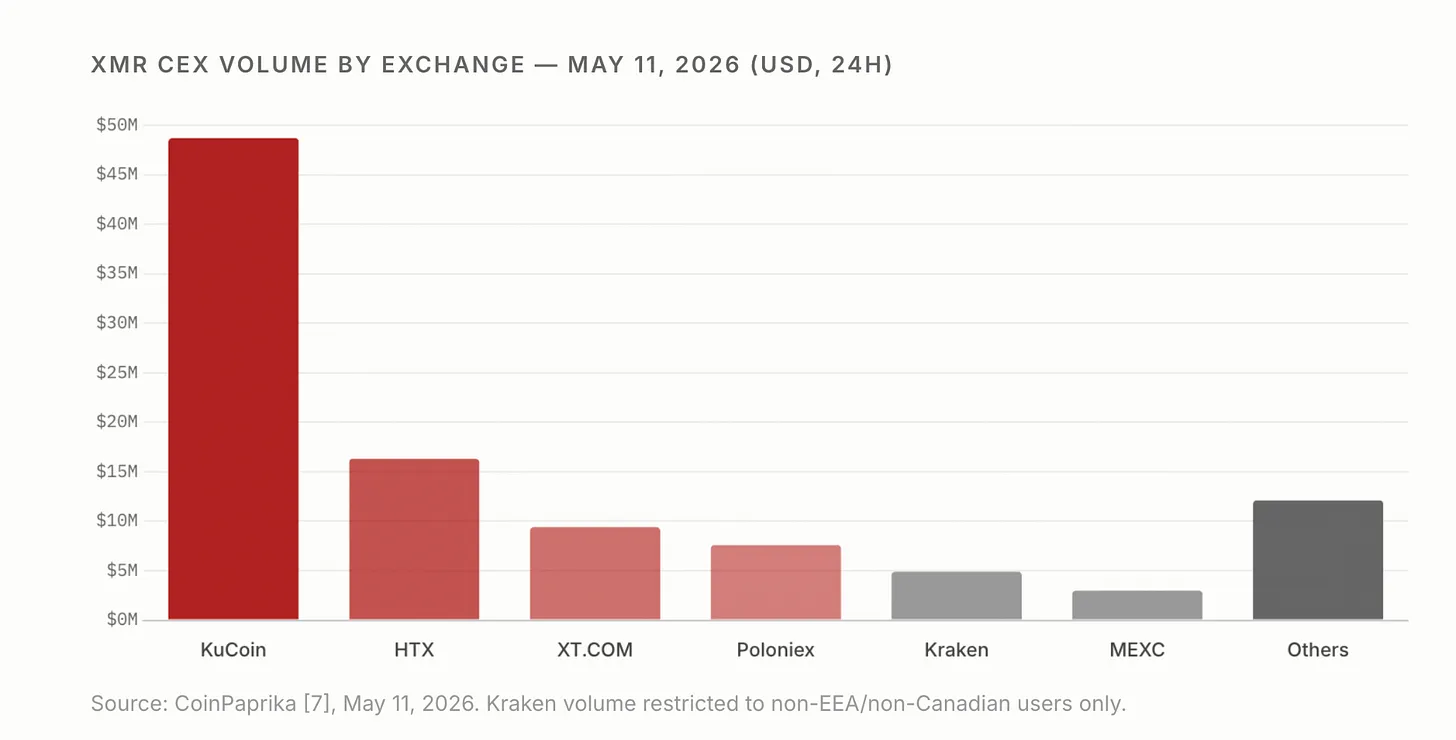

It has been proven that Monero no longer relies on compliant spot exchanges in Europe. However, it still needs the core functions that exchanges provide: price discovery, fiat exchange, large liquidity absorption, and cross-market arbitrage. These functions have simply been redirected: peer-to-peer trading is handled by Haveno and Bisq; conversion between Bitcoin and XMR relies on atomic swaps; custodial trading traffic has shifted to offshore exchange KuCoin (which accounted for over 50% of centralized exchange XMR trading volume as of May 2026); derivatives trading has settled in decentralized perpetual contract platforms. The official FAQs and resource pages of Monero still list exchanges as one of the mainstream purchasing channels.

A more rigorous statement is that Monero has proven that even detached from the European compliant exchange system, it can still survive and even set new historical highs. But this does not mean that exchanges have lost their value to it. The historical highest price set in January 2026 confirms the resilience of the project, rather than an unlimited liquidity or the existence of all structural risks has disappeared.

In the coming year, two core developments will determine the direction of Monero's future.

First, the FCMP++ upgrade. As of May 2026, this upgrade has entered the second round of testnet stress testing, with a security audit by Trail of Bits scheduled from May 11 to 22. The full-chain member proof technology will replace the current ring signature mechanism: originally, transactions were hidden among 16 interference addresses, but after the upgrade, they can be concealed among 150 million on-chain transaction outputs. If the audit passes smoothly, it will eliminate the last significant technical barrier to Monero's privacy declaration.

Second, THORChain plans to integrate XMR, expected to be launched between June and July 2026, depending on the progress of the second round of audit. After the integration, direct cross-chain exchanges of XMR will be possible without KYC and non-custodial. Currently, most non-custodial trading of Monero still requires intermediating through Bitcoin, while THORChain can open decentralized exchange channels between XMR and Ethereum, stablecoins, completely eliminating reliance on intermediary coins and further weakening the discourse power of traditional exchanges.

Of course, neither of these developments can be guaranteed. The audit may uncover security vulnerabilities, and technical integration may be delayed; proof-of-work networks always face risks of hash rate centralization; the EU's anti-money laundering ban may trigger more offshore exchanges to delist XMR; liquidity dispersed among DEX, peer-to-peer markets, and offshore CEX may also lead to increased bid-ask spreads and worsened large trade slippage.

Ironically, the EU has unintentionally become the most efficient free marketing department for Monero. After a round of stringent regulation, it not only completely loses the ability to monitor the market but also adds governance challenges. Logically, Monero should be charging the EU for consulting fees, yet regulatory agencies are likely to continue holding meetings to discuss new rounds of regulatory details.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。