Author: Deep Tide TechFlow

On May 8, AI cloud computing provider CoreWeave (CRWV) plunged 11.4% in a single day, closing at $114.15. This marks another "performance day drop" for the company since its IPO in March last year. However, unlike previous instances, this drop was compounded by a more tension-filled contrast: Duan Yongping, widely known in the Chinese community as a disciple of Buffett, had just established a position in CoreWeave in the fourth quarter of 2025, with a stake of about $20 million. Based on the position and the average price in the fourth quarter, the timing of the acquisition is close to the year’s lowest range for CoreWeave in December 2025.

CoreWeave is currently one of the most polarizing AI assets in the U.S. stock market. On one side is an order reserve approaching $100 billion, along with the narrative of "selling shovels," deeply tied to Nvidia; on the other side is the financial reality of widening losses despite scaling up and continual cashing out by insiders. The Q1 financial report acts like a prism, clearly reflecting this divergence.

Q1 Financial Report: Revenue Doubles but Losses Widen, Q2 Guidance Pierces Valuation

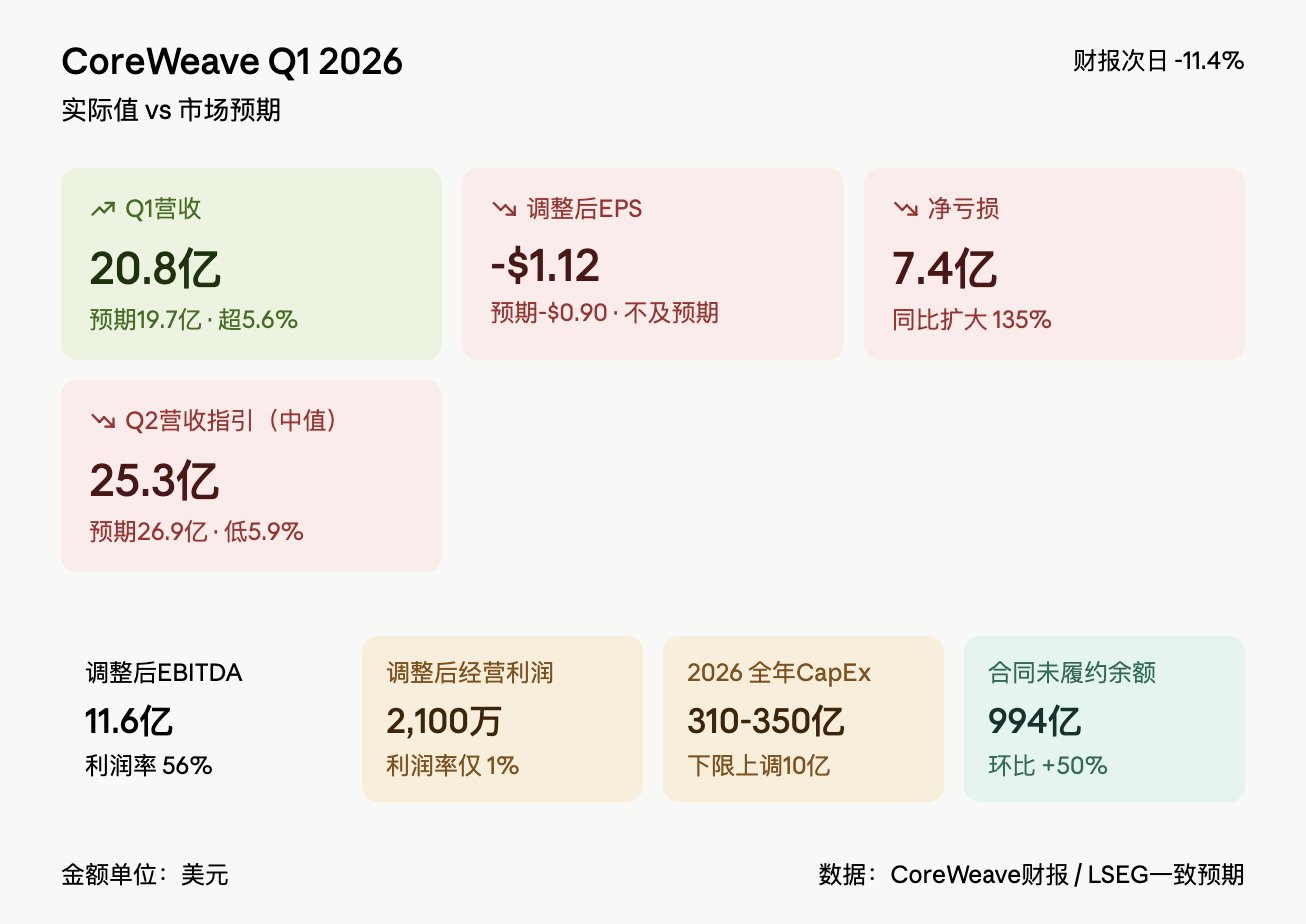

CoreWeave's Q1 revenue reached $2.08 billion, a 112% year-over-year increase and a 32% quarter-over-quarter rise, exceeding the LSEG market expectation of $1.97 billion. However, the adjusted loss per share was $1.12, worse than the expected loss of $0.90; the net loss widened to $740 million, more than doubling from $315 million in the same period last year.

The real trigger for the sell-off was the forward guidance. The company provided a revenue range for Q2 of $2.45 billion to $2.6 billion, with a midpoint of $2.53 billion, significantly lower than the market expectation of $2.69 billion. Meanwhile, the lower limit for the full-year capital expenditure in 2026 was raised from $30 billion to $31 billion, with CFO Nitin Agrawal attributing this to rising component prices.

The fragility of the profit structure is exposed. Q1 adjusted EBITDA reached $1.16 billion (profit margin 56%), which seems impressive; however, the adjusted operating profit was only $21 million, with the operating profit margin shrinking to 1%. This is due to a year-over-year surge in technology and infrastructure costs by 127% to $1.27 billion, and sales and marketing expenses skyrocketing more than six-fold to $69 million. While revenue is rising, costs are increasing even faster.

CEO Michael Intrator emphasized during the earnings call: "We have reached hyperscale." He disclosed that the company currently has 10 clients committed to spending more than $1 billion, a significant improvement over 62% of revenue dependency on a single client, Microsoft, in 2024. Intrator also expects CoreWeave's annualized revenue to exceed $30 billion by the end of 2027.

Bullish Narrative: $100 Billion Orders, Deeply Tied to Nvidia

The core supporting the bullish logic is the order reserve. As of the end of Q1, CoreWeave's remaining contract balance (RPO) reached $99.4 billion, net increasing by approximately $33 billion quarter-over-quarter and almost quadrupling year-over-year. Intrator stated that new contracts signed in Q1 exceeded $40 billion.

The client list is also reshaping market perceptions. In Q1, CoreWeave added Anthropic as a client, providing computing power support for its Claude series models; signed a $2.1 billion AI cloud agreement with Meta; and trading company Jane Street committed approximately $6 billion in orders, completing a separate $1 billion equity investment. Nvidia again purchased $2 billion worth of Class A common stock from CoreWeave this quarter; the world's largest GPU supplier, also a major investor and important customer of CoreWeave, has been described as Nvidia's "favorite child".

In terms of financing structure, CoreWeave completed an $8.5 billion investment-grade HPC (high-performance computing) secured delayed draw term loan (DDTL) in Q1, priced below 6%, described by management as "first of its kind." Year-to-date, the company has raised over $20 billion in debt and equity financing, with the weighted average cost of debt decreasing by approximately 80 basis points. S&P Global Ratings raised CoreWeave's credit outlook from "stable" to "positive" at the same time.

Bearish Logic: The Bigger the Scale, the Less Profitable; Debt Snowball Grows Larger

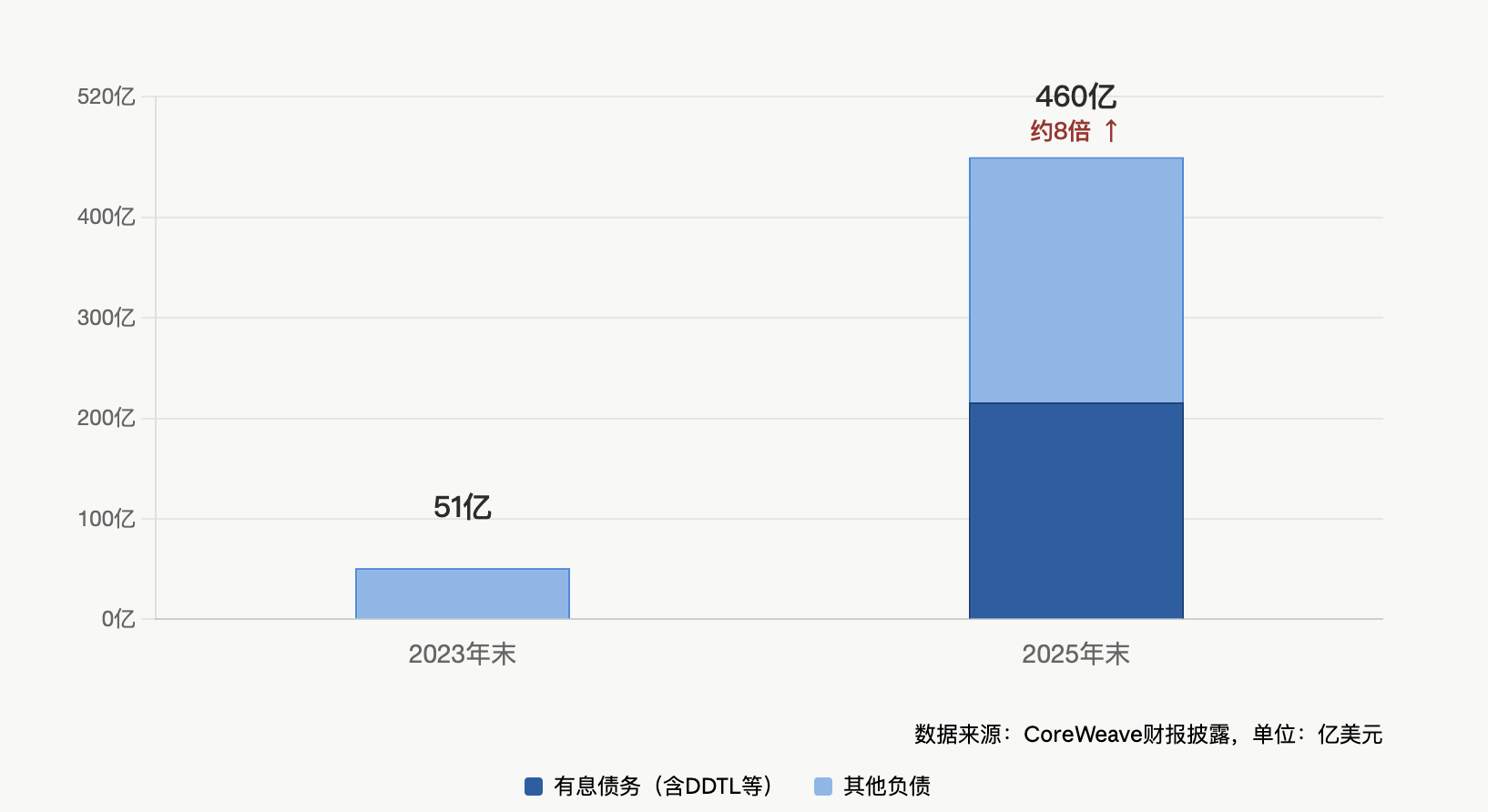

However, another set of numbers in the financial report is causing anxiety. Q1 capital expenditures reached $6.8 billion, and the company expects Q2 capital expenditures to further rise to between $7 billion and $9 billion. Q2 interest expense guidance is $650 million to $730 million, reflecting the rapid expansion of debt scale.

The total debt amount is staggering. By the end of Q1, CoreWeave's total debt was approximately $25 billion. This number is significantly higher than the leverage level of traditional cloud service providers relative to the company's current annual revenue scale. Morgan Stanley data indicates that CoreWeave's total debt financing for the entire year of 2025 could reach about $11.8 billion, far exceeding the $1.5 billion in equity financing during the same period, with the core expansion tool being the DDTL, using order contracts as collateral to finance GPU procurement through a "sign first, finance later" model.

The most pointed criticism comes from the quality of profits. Despite management's repeated emphasis on a 56% EBITDA profit margin, the adjusted operating profit margin was only 1%, with the "true" gross margin after deducting technology and infrastructure costs at about 4%, compressing both quarter-over-quarter and against market expectations. Intrator attributed this to a stage effect of scale expansion, stating that as the company rapidly expands from a 1 gigawatt operational scale, the dilution effect on profit margin due to new capacity is immense. He promised this is the "low point for profit margins," and that they will gradually rebound in future quarters.

However, the market is currently unwilling to pay for this promise. Analysts from Morgan Stanley and Jefferies have given positive ratings, but CoreWeave has faced short-term pullbacks after each previous financial report, and this time the drop is deeper than in prior reports.

Insiders Continue to Sell, forming a Mirror Image with Duan Yongping's Bottom Fishing

Before and after the financial report was released, insiders at CoreWeave did not stop selling. CEO Mike Intrator sold 307,693 shares at the end of April; co-founders Brian Venturo and Chen Goldberg both have records of selling; the institutional shareholder Magnetar Financial had previously sold over $300 million worth of shares. The latest disclosures show that a major shareholder recently sold about 1.2 million shares.

This stands in sharp contrast to Duan Yongping's accumulation actions in the fourth quarter. According to the 13F document disclosed by H&H International Investment in February 2026, Duan Yongping first established a position of 299,900 shares in CoreWeave during the fourth quarter of 2025, at a time when the company's stock price had retreated over 65% from its peak, and concerns about its debt structure reached a climax.

It is noteworthy that CoreWeave constitutes only 0.12% of Duan Yongping's total holdings in H&H, indicating a "light position trial." During the same period, Duan Yongping increased his position in Nvidia by over 1,110% and established new positions in Credo Technology (high-speed interconnect) and Tempus AI (AI healthcare), with these three new AI positions collectively accounting for less than 0.3%. This signifies that Duan Yongping's real bet is on Nvidia itself, with CoreWeave more like a small extension layout in the downstream AI computing power supply chain.

The Key Question Now: Turning Point or Trap?

Intrator posed an emotionally charged rhetorical question during the Q&A session of the earnings call: "I have always felt that everyone is staring at the stock price tree and missing the entire forest."

This captures the current standoff between bulls and bears. The forest that bulls see is the nearly $100 billion in contract reserves, a diversified client base, the triple tie to Nvidia, and the upgraded credit rating; the tree that bears see is the 1% operating profit margin, widening net losses, aggressive capital expenditures, and continually selling insiders.

CoreWeave's stock price is still up nearly 80% since the beginning of the year and has increased over 200% since its IPO. However, when a stock's bullish premise is based on forward narratives while bears rely on current numbers, every financial report becomes a battleground for these two narratives. Duan Yongping previously stated in an interview with Fang Sanwen: "AI is a huge revolution brought about by a qualitative change in computing power, which may exceed the influence of the internet and the industrial revolution. Currently, the AI bubble is obvious, and 90% of companies may be eliminated, but those that survive will become the next generation of giants." His 0.12% light position itself acknowledges the uncertainty of this gamble.

The next testing point is already clear: the Q2 financial report. If the operating profit margin does not rebound as promised by management, the credibility of the "forest" narrative will face genuine pressure testing.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。