Author: Claude, Deep Tide TechFlow

Introduction by Deep Tide: As the Nasdaq continuously hits historical highs and Nvidia's market value approaches $5.3 trillion, Michael Burry, who became famous for shorting subprime mortgages during the 2008 financial crisis, the prototype character of the movie "The Big Short," is now betting in the opposite direction.

He not only maintains his bearish bets on Nvidia and Palantir but has also expanded his short positions to semiconductor ETFs and Nasdaq ETFs, while buying traditional software stocks that have been suppressed by the AI narrative, constructing a complete "AI bubble repricing" portfolio.

The Nasdaq index reached a new historical high this week, closing at approximately 26,247 points on May 8, with the S&P 500 also hitting a record on the same day. The Philadelphia Semiconductor Index has accumulated an increase of about 55% since the second quarter, and Nvidia's stock price is nearing its historical high of $217.80, with a market value exceeding $5.2 trillion. The technology stock frenzy driven by AI is currently at its hottest stage.

However, at the most euphoric moment in the market, an investor known for betting against the trend is significantly increasing his stakes in another direction.

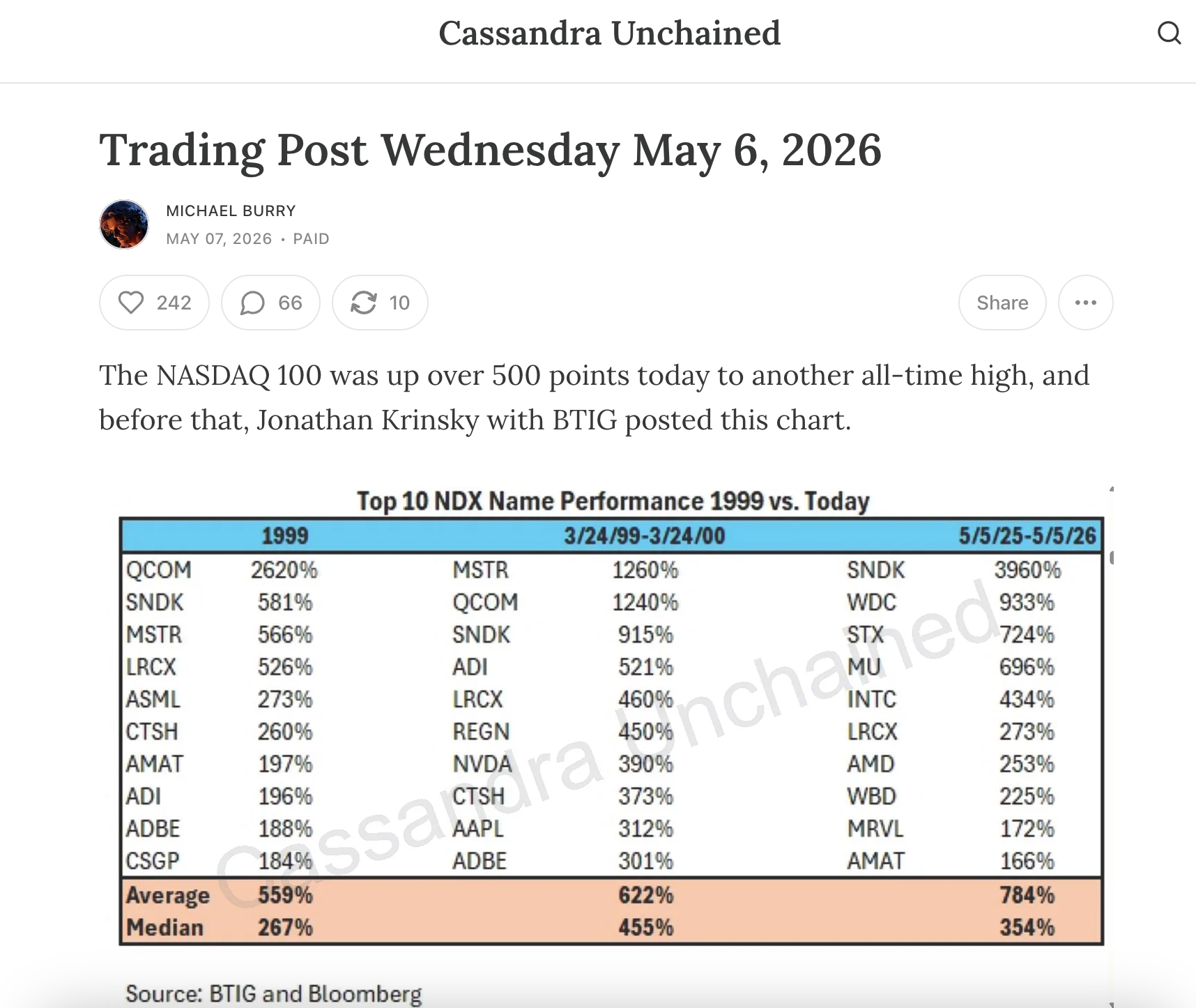

According to Foreign Policy Journal on May 7, hedge fund manager Michael Burry, who predicted the 2008 subprime crisis and was adapted into the movie "The Big Short," revealed his latest portfolio adjustments this week in his Substack column "Cassandra Unchained":

He not only maintains his put options on Nvidia and Palantir but has also added direct short positions on Palantir and expanded his bearish bets on Semiconductor ETFs (SOXX), Nasdaq 100 ETFs (QQQ), and Oracle.

At the same time, he began buying a batch of traditional software companies marginalized by the AI wave, such as Adobe, Autodesk, Salesforce, and Veeva Systems, reasoning that the stock price declines of these companies stem from panic selling rather than fundamental deterioration.

Thus, a complete big short hedge portfolio has emerged, with the core logic being shorting AI beneficiaries and going long on AI victims.

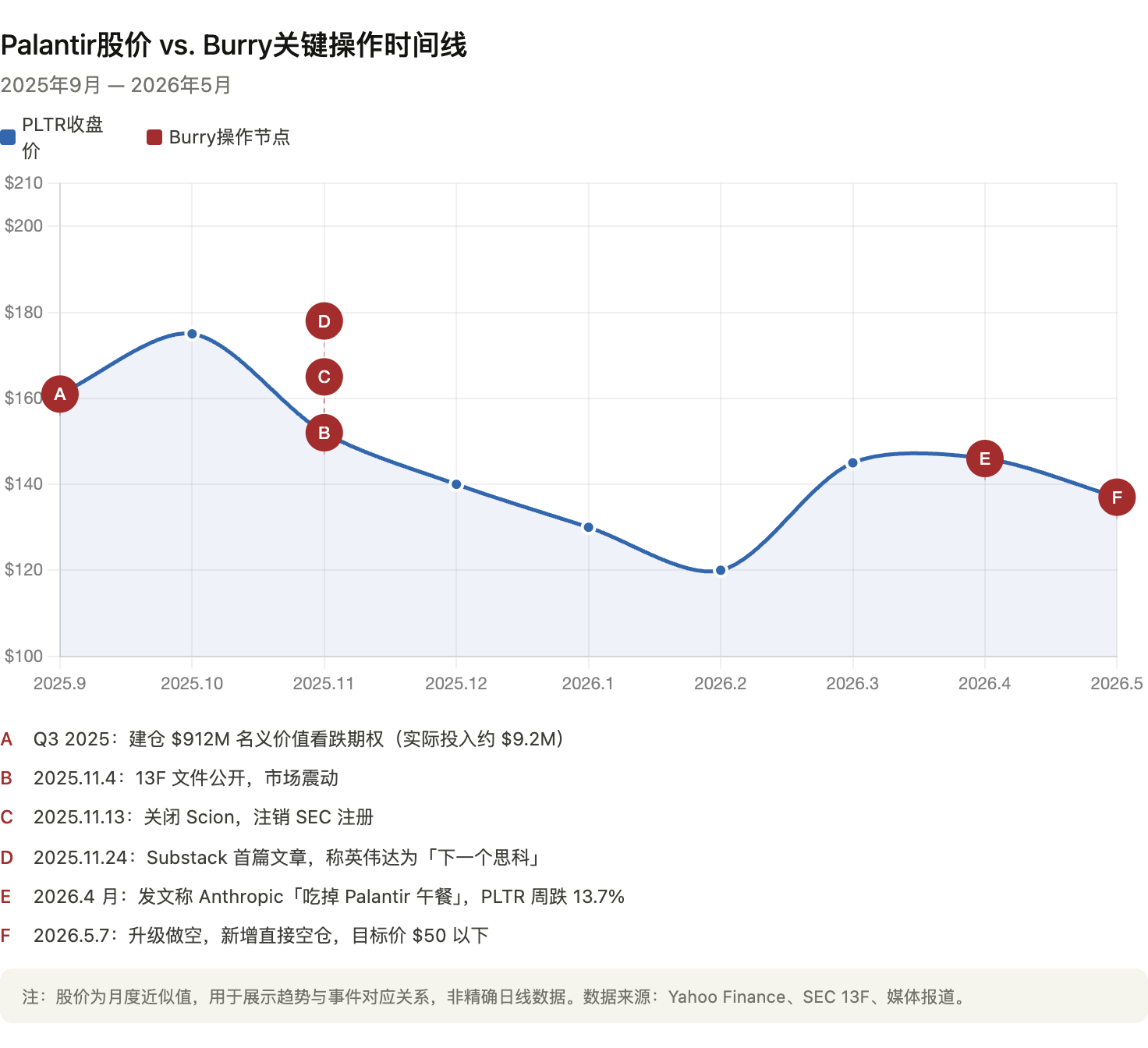

Starting from the $1.1 billion bet in November last year

Burry's shorting of the AI sector began in the third quarter of 2025.

At that time, the 13F filing of his hedge fund Scion Asset Management indicated that he purchased approximately $912 million in notional value of put options on Palantir and approximately $187 million in notional value of put options on Nvidia. This news caused market tremors when it was announced last November, leading to downward pressure on the stock prices of Palantir and Nvidia.

However, Burry later clarified on the X platform that his actual investment was about $9.2 million, not the $912 million widely reported by the media—the latter being the notional value of the options contracts, a difference of nearly a hundredfold. This detail is crucial: the notional values in the 13F filing are often misread as actual invested funds, thus exaggerating the scale of the trades.

Shortly after the news broke, Burry announced the closure of Scion Asset Management and withdrew his SEC registration, ending his career managing external funds.

He then transitioned to being a personal investor and opened a column on Substack under the name "Cassandra Unchained" (Cassandra is a prophet in Greek mythology who predicts the truth but is not believed), continuously publishing market analysis.

Palantir shorting has become effective, Burry says "not down enough"

From the trading results, Burry's wager on Palantir is currently profitable. Palantir's stock price has fallen from around $161 when he entered to around $137 now, a cumulative drop of about 34% from its 52-week high of $207. Although the company just released an impressive first-quarter report for 2026 (with revenue up 85% year-on-year), the stock price dropped after the report was published.

Burry has not taken profits. According to his Substack, he currently holds put options expiring in December 2026 with a strike price of $100 and put options expiring in June 2027 with a strike price of $50, indicating he expects Palantir to fall more than 60% from current levels within the next year. He clearly stated in the post that Palantir's reasonable valuation is only "in the single digits to the lower double digits."

In April of this year, Burry wrote on Substack that Anthropic is "eating Palantir's lunch", pointing out that this AI safety company's revenue growth has exceeded an annualized level of $30 billion, and its easier-to-use, lower-cost AI integration tools are replacing Palantir's complex enterprise deployment solutions. Following this post, Palantir's stock price fell 13.7% within a week, after which Burry deleted the post. Wedbush analyst Dan Ives dismissed this view as a "fabricated narrative," and Palantir CEO Alex Karp had previously publicly expressed that he could not understand Burry's shorting stance.

Nvidia shorting is still at a loss, but Burry insists "AI is a bubble"

Compared to the success with Palantir, Burry’s position on Nvidia is quite different.

Nvidia's stock price closed at about $215 on May 8, nearing its historical high of $217.80, with a market value of about $5.3 trillion. Reports indicate that Burry holds Nvidia put options with a strike price of $110, expiring in December 2027, which are currently deeply in the red. However, he has not reduced his position; instead, he has continued to increase it in recent portfolio adjustments.

Burry’s core logic for shorting Nvidia is "overbuilding AI infrastructure." In his first Substack article in November last year, he compared the current AI investment frenzy to the dot-com bubble of the late 1990s, likening Nvidia to Cisco at that time. Cisco's stock price soared by 3,800% from 1995 to 2000, becoming the highest market capitalization company globally, only to crash more than 80% during the dot-com bust.

Burry’s main arguments include: mega-scale customers like Microsoft, Google, Meta, Amazon, and Oracle are extending the depreciation periods of GPUs to beautify their financial reports; he estimates that between 2026 and 2028, these accounting maneuvers will collectively underreport about $176 billion in depreciation expenses, artificially inflating the profits of the entire industry. Additionally, he believes that the current massive capital expenditure on AI infrastructure is based on overly optimistic demand forecasts, similar to the telecom companies' frenzied laying of fiber optic cables around the year 2000.

This viewpoint triggered a direct counterattack from Nvidia. According to CNBC, Nvidia privately distributed a seven-page memo to Wall Street sell-side analysts, responding point by point to Burry's accusations, specifically mentioning Burry's posts on X as sources needing rebuttal. Nvidia stated in the memo that its customers set GPU depreciation periods at four to six years based on actual usable life, and early products (like the A100 released in 2020) still maintain high utilization rates. Burry responded, "I am not saying Nvidia is Enron," but insists on his analysis.

Going long on software stocks pressured by AI: A complete bubble hedge portfolio

What is perhaps most noteworthy in Burry's portfolio adjustments is not the shorting itself but his long positions.

Recently, he has bought stocks from Adobe, Autodesk, Salesforce, Veeva Systems, and MSCI. The common feature of these companies is that their business fundamentals remain strong, but their stock prices have dropped significantly due to the narrative that they are "being disrupted by AI" and forced selling by private credit funds.

Adobe's stock is currently down about 30% from its 52-week high, and Autodesk has dropped about 22% this year, with both companies' forward P/E ratios returning to levels seen in 2018-2019.

Burry explained on Substack that he "does not believe that the technical pressure from private credit and software debt is sufficient to have a long-term impact on these stocks." In other words, he thinks the market has overpunished companies labeled as "AI losers" and overly favored companies labeled as "AI winners"—and he is betting on a correction of this mispricing.

Viewing both the short and long sides together, Burry is constructing a typical long-short hedge portfolio: If the AI bubble narrative bursts, overvalued beneficiary stocks like Nvidia and Palantir will be the first to suffer, while the traditional software stocks that have been mistakenly sold off may see a valuation recovery. Even if the overall market declines, this structure could still achieve positive returns.

Burry candidly wrote in the letter to investors he sent upon closing Scion: "My judgment of the value of securities has long been out of sync with the market." This sentence is both a reflection and a consistent declaration of his.

At the peak of the AI frenzy, he chose to stand on the opposite side of the crowd.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。