Author: Gino Matos, CryptoSlate

Translated by: Deep Tide TechFlow

Deep Tide Introduction: Strategy has openly stated the possibility of selling currency to pay dividends, MARA sold 15,000 BTC to repay debts, and Sequans has repaid convertible bonds with Bitcoin for two consecutive quarters. The narrative of "never selling" Bitcoin is collapsing, as these companies are transforming Bitcoin from a "faith reserve" into a "liquidity tool." When the price of the currency drops, triggering more sell-offs, the sell-offs further depress the price, and the spiral begins.

Saylor Admits: Selling Currency Can Be More Cost-Effective Than Issuing New Shares

During the earnings call on May 5, CEO Phong Le of Strategy directly stated: "We will sell Bitcoin when it is beneficial for the company." Saylor added: Strategy may sell some Bitcoin to pay dividends, "to let the market adapt to this matter in advance."

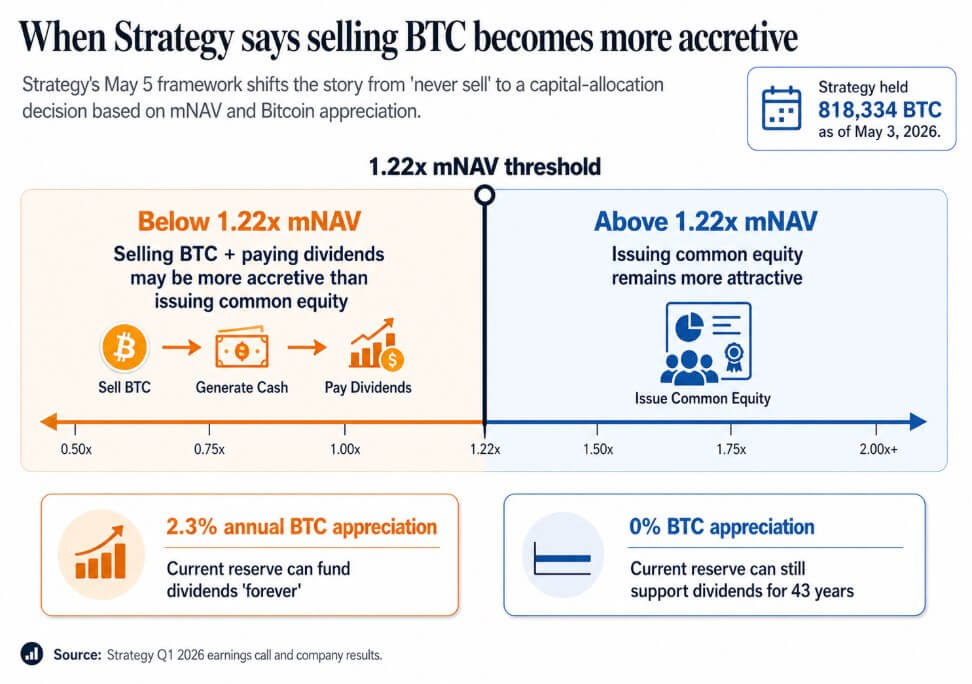

As of May 3, Strategy holds 818,334 BTC, having increased its holdings by 22% year-to-date, with a market cap of $64.14 billion.

This call formally established that selling BTC is officially included in the company's financial toolbox, backed by a quantitative framework.

Management provided a guideline—when mNAV (Market Value/Net Asset Value) is below 1.22 times, selling currency for dividends is more beneficial for shareholders than issuing new common stock. Saylor's algorithm is: as long as the annualized price increase of Bitcoin exceeds 2.3%, the existing Bitcoin reserves of Strategy can "always" pay dividends; even if the Bitcoin price increase is zero, the reserves are sufficient to issue dividends for 43 years.

Caption: Illustration of Strategy's 1.22 times mNAV threshold—when mNAV is below this line, selling currency for dividends is more beneficial to shareholders than issuing new stocks

The motto of "never selling" has given way to a model: buy when thickening during purchases, issue more when thickening during issuance, issue preferred shares when thickening during preferred share issuance, and sell currencies when thickening during sales. These companies are essentially leveraged treasury + credit vehicles.

Investors initially bought these stocks based on Bitcoin proxies established on scarcity and commitment to permanent holding. The 1.22 times mNAV threshold and 2.3% breakeven price increase are a more honest version, and also a more complex version.

When Bitcoin Becomes Working Capital

Sequans' first-quarter report is more straightforward. Revenue fell 24.8% year-on-year to $6.1 million, with an operating loss of $50.5 million. The realized net loss from selling Bitcoin in the first quarter reached $11.7 million, with the income from selling currency primarily used to repay convertible bonds and repurchase ADS.

As of March 31, Sequans held 1,514 BTC, of which 1,217 were used as collateral for $66.2 million in convertible bonds. By April 30, the holding fell to 1,114 BTC, with 817 Bitcoin backing $35.9 million in debt (due June 1).

This is exactly the same operation as in November 2025—at that time, Sequans sold 970 BTC, redeemed 50% of its convertible bonds, reducing its debt from $189 million to $94.5 million.

For two consecutive quarters, the same pattern: declining revenue, impending debt, and Bitcoin becomes operational liquidity. The BTC used as collateral was already tied to debt obligations before any proactive selling decision.

Similarly, MARA did the same thing in March on a larger scale—selling 15,133 BTC, converting approximately $1.1 billion to repurchase convertible notes, cutting 30% of its convertible bond balance in one go, locking in approximately $8.81 million in profit.

MARA packaged this operation as "balance sheet optimization," driven by debt structure and financing conditions. This has established a precedent: selling BTC can be an independent capital allocation decision, separate from Bitcoin faith, with the real question being—under what conditions is selling the highest return option.

Bull-Bear Divergence: Financing Conditions Determine Everything

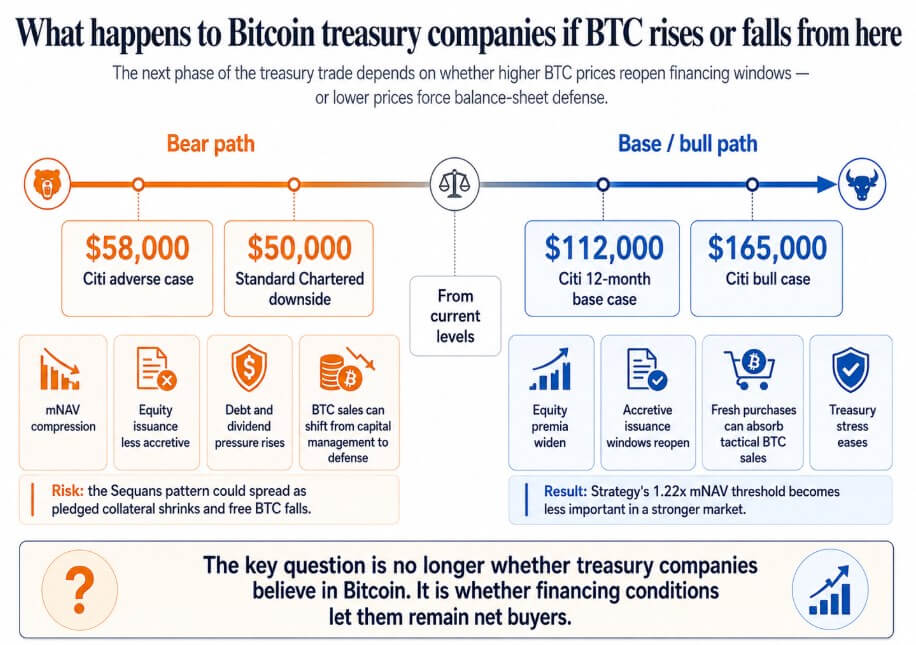

If Bitcoin rebounds to Citigroup's 12-month baseline expectation of $112,000 or the bullish scenario of $165,000, the equity premium of treasury companies will expand, the issuance window will reopen, and substantial new purchases will be sufficient to absorb tactical BTC sales.

Strategy's 1.22 times mNAV threshold will become a technical detail. Companies like Sequans that bear debt pressure during Bitcoin's weak phase can also resolve debt issues, entering the next cycle with unrestricted BTC.

If Bitcoin falls to Citigroup's unfavorable scenario of $58,000 (Standard Chartered has indicated a further path down to $50,000), companies trading at NAV or below will lose the thickening effect of issuing new stocks.

In this case, the obligations of preferred stock dividends continuously accumulate, with BTC sales shifting from capital management to balance sheet defense. Sequans’ model may spread to all "thin margin operations + BTC guaranteed borrowing" treasury companies—selling Bitcoin to repay debts, collateral shrinking, and reduced liquidity becoming the only option.

By that time, corporate Bitcoin buying will become a loop: falling currency prices trigger more selling, and more selling pressures down the price.

Caption: Two paths for Bitcoin treasury companies—facing balance sheet pressures in a bear market scenario ($50,000-$58,000) and easing financing pressures in a bull market scenario (above $112,000)

Corporate Bitcoin treasury trading is based on a commitment to "permanent currency holding," which allows investors to price these companies as Bitcoin proxies. Once selling is recognized as a publicly acknowledged tool in the model, investors must incorporate debt maturity dates, collateral requirements, dividend obligations, and management’s mNAV level where they would choose to sell currency rather than issue new shares into their pricing.

Saylor's 2.3% annualized break-even and 1.22 times mNAV threshold are more candid. In the next phase of corporate Bitcoin treasury trading, the weight of financing conditions will not be lower than that of Bitcoin faith.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。