Caitho Securities believes that the market's reaction to war has shifted from "emotion-driven" to "economically transmitted", with the stock market increasingly focusing on fiscal expansion, inflation expectations, oil price fluctuations, and monetary policies as real economic variables.

Written by: Li Jia

Source: Wall Street Journal

As the guns erupt, fortunes are made. Just as the market is hotly discussing whether the Middle East conflict will drag down the global economy, the S&P 500 and Nasdaq indexes both reached new highs. What does war really mean for the U.S. stock market?

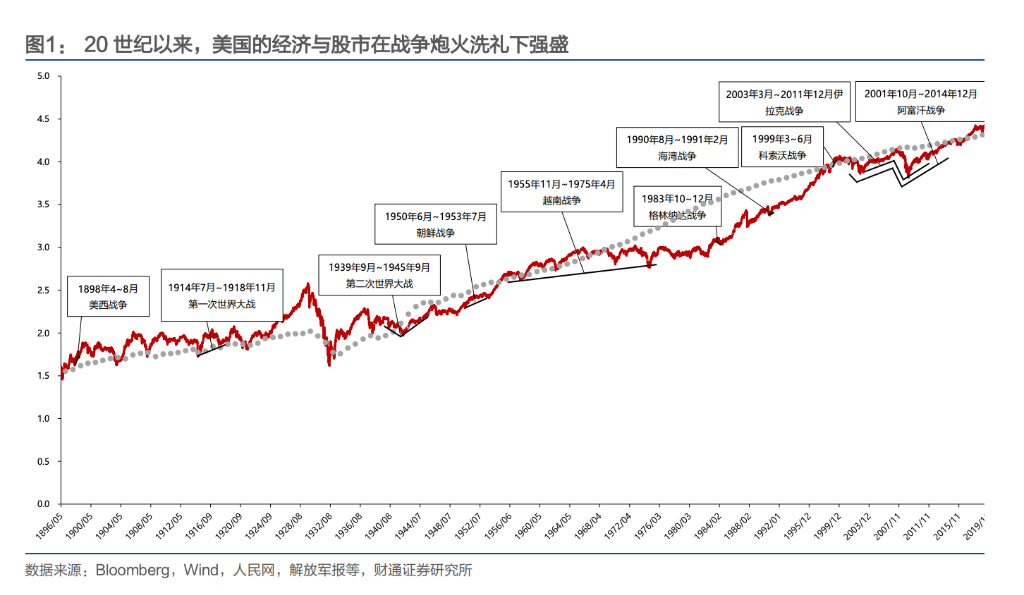

Caitho Securities report provides a straightforward answer: War and the long bull market in the U.S. stock market are not in opposition but are more akin to a symbiotic relationship. The historical performance of the Dow Jones Index confirms this point—an increase of 28% during the Spanish-American War, an increase of 26% during the Korean War, an over 80% rise during the 19-year Vietnam War, and the Afghanistan War traversing the period around the 2008 financial crisis almost doubled the index.

Since becoming the world's largest economy in the late 19th century, the U.S. has generally obtained substantial gains from each war except for the Vietnam War. From capturing Spanish colonies during the Spanish-American War, to profiting massively in both World Wars, and moving to smaller-scale conflicts around oil resources after the Gulf War, the U.S. has transformed from a "participant" in wars to a "initiator" of wars.

The response path of the U.S. stock market amid gunfire is also clear: Before and during World War II, wars primarily impacted the market through emotional shocks; since the Korean War, this direct effect has gradually weakened, with wars transmitting more through economic channels such as inflation, oil prices, and fiscal deficits to the stock market.

The Vietnam War is the only war that resulted in the U.S. "losing money" and profoundly changed its war logic. The subsequent conflicts initiated by the U.S. almost universally feature three characteristics: short duration, limited scope, and centered around oil—and all have ultimately achieved their objectives.

From "picking up the pieces" to proactively instigating, U.S. war strategy has undergone three turnarounds

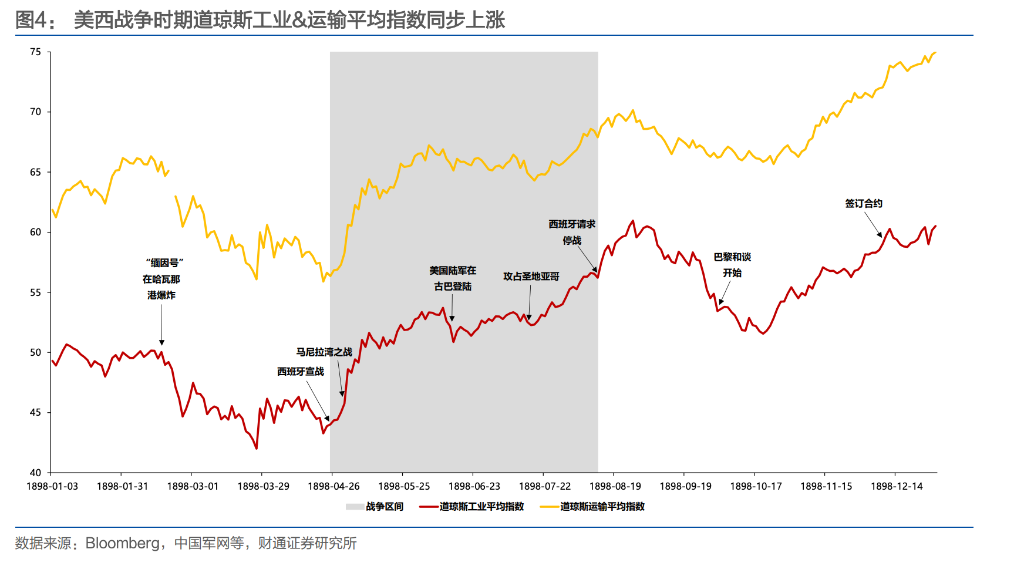

The Spanish-American War in 1898 was the first significant war actively instigated by the U.S. At that time, domestic monopolistic consortiums were in urgent need of new markets, investment sites, and raw material sources, making the remnants of the Spanish colonial empire the best target. After the war, the U.S. gained control of Cuba and acquired the Philippines, Guam, and Puerto Rico. The Dow Jones Industrial Index rose by 28% during the three-month war, in sync with battlefield victories.

When World War I broke out, the U.S. initially maintained neutrality. During the market closure in July 1914, investors realized that the U.S. would become the largest beneficiary of the European conflict—homeland far from the battlefield could continue to produce and export munitions to Europe. By 1917, U.S. banks, including Morgan, had provided $10 billion to the British and French governments for weapon purchases. Although the stock index fell nearly 10% after officially entering the war in April 1917, the industrial index had risen approximately 107% from its 1914 low by March 1917.

World War II was the critical battle that established U.S. global dominance. In the early stage of the war in September 1939, the U.S. stock market briefly declined due to the "excess profits tax" suppressing corporate profit expectations—the Congress imposed a maximum tax rate of 95% on profits exceeding $5,000, severely suppressing the DDM numerator. It was not until the Battle of Coral Sea in May 1942 and the Battle of Midway turned the tide of war that investors keenly sensed the war's direction, leading the U.S. stock market to rebound ahead of schedule. The industrial index rose 82% in the latter half of the war, with the transportation index rising 127% and the utility index increasing 203%.

The Korean War marked the U.S.'s first "non-winning" war. While arms demand propelled the weak post-World War II economy, U.S. troops failed to achieve their set goals. Nevertheless, the Dow Jones Industrial Index still rose 26% throughout the period, with the transportation index soaring 86%.

The Vietnam War became a watershed, being the only war in which the U.S. lost without gaining benefits.

The U.S. defense budget soared from $49.6 billion in 1961 to $81.9 billion in 1968 (accounting for 43.3% of the federal budget), with the fiscal deficit rising from $3.7 billion to $25 billion, and inflation rising from 1.5% to 4.7%. The U.S. GDP's share of the world's total output fell from 34% to under 30%. After the war, U.S. war strategies underwent a complete turnaround: no longer engaging in large-scale ground wars, but shifting to short-duration, low-casualty "proxy-style" conflicts centered around airstrikes.

Subsequent conflicts, including the Gulf War, Kosovo War, Afghanistan War, and Iraq War, were invariably initiated by the U.S., leveraging local conflicts or black swan events, primarily located in the Middle East and Balkan regions, with core objectives revolving around oil resource control and arms demand.

Ways war transmits to the stock market have changed: from emotion-driven to economy-driven

Before and during World War II, wartime events often directly influenced investor sentiment. During the Spanish-American War, victories at the Battle of Manila Bay and the Battle of Santiago Bay pushed indexes to rise about 10% within ten days; in both World Wars, news of U.S. participation often triggered panic sell-offs.

However, since the Korean War, this direct influence has gradually diminished. From November 1950 to February 1951, as U.S. and Korean forces suffered setbacks, the U.S. stock market continued to rise—because the economy, which had stagnated post-World War II, resumed during the Korean War: U.S. GDP growth in 1950 was about 8.7%, maintaining above 8% in 1951. The fiscal expansion brought on by war instead became a catalyst for economic recovery.

During the Vietnam War, this shift was even more pronounced. The Battle of the Ia Drang Valley in November 1965 (the first large-scale battle of the Vietnam War for U.S. forces) did not significantly impact the stock market; the "Tet Offensive" launched by North Vietnam in early 1968 also failed to prevent the U.S. stock market from hitting new highs. The true drivers of the market were the credit tightening by the Federal Reserve in response to Vietnam War expenditures in 1966, as well as the economic recessions of 1969-1970 and 1973-1975. War sentiment had ceded ground to macro policies and corporate profits.

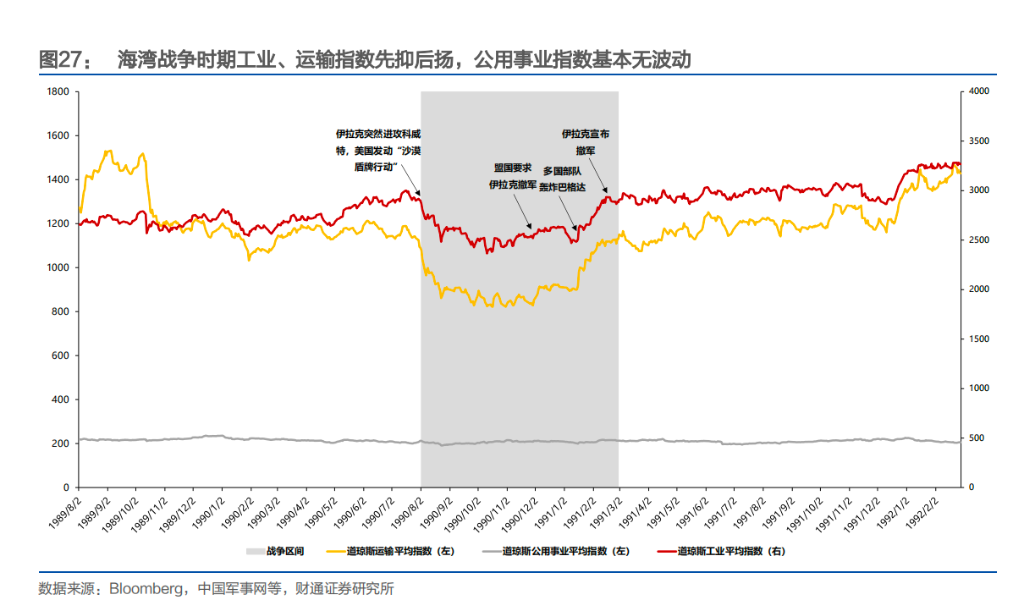

The Gulf War provided the clearest case of "economic transmission." After Iraq attacked Kuwait in August 1990, oil prices surged, with the market expecting a U.S. economic recession, leading to a bottoming out of S&P 500 valuations. After multinational forces bombed Baghdad in January 1991, oil prices fell back to pre-war levels, with the stock market rebounding in tandem. During the war, the Dow and oil prices almost perfectly operated in reverse—what the market traded was the balance between inflation and growth.

The Afghanistan War in 2001 and Iraq War in 2003 further validated this pattern. The most symbolic moment was the killing of Osama bin Laden in May 2011—this should have been the most breakthrough moment in the Afghanistan War, yet the next day the Dow only fell by 0.02%, and the S&P 500 fell by 0.18%. The market almost completely ignored this news.

In summary, the U.S. stock market's response to war has followed a clear evolutionary path: from "emotion-driven" to "economically transmitted." Early wars directly jolted the market through news of victories and defeats, while since the Korean War, the stock market has increasingly focused on real economic variables like fiscal expansion, inflation expectations, oil price fluctuations, and monetary policy.

War itself is no longer a reason for market fluctuations; rather, how war affects growth and costs has become the true object of market pricing.

Which industries profit from war? The answer is changing

During World War II, coal was the lifeblood of war, with anthracite's share rising from 43.8% pre-war to 48.9%, and the industry cumulatively rising 415%.

In the Korean War, oil took over as the new protagonist, with crude oil extraction and processing leading in price increases, continuing to rise from mid-1950 to the first half of 1952. During the Vietnam War, the collapse of the Bretton Woods system forced the dollar to devalue, allowing OPEC to raise prices to make up for losses, with the oil extraction industry exploding during the dollar crisis from late 1970 to early 1973, with a rise of as much as 1378% throughout the war.

The Kosovo War continued this pattern, with the raw materials and energy sectors experiencing the best returns.

The Gulf War is the only counterexample—transmission paths shifted to an indirect model of "oil prices → economic expectations," leading to short-term advantages in consumer staples and healthcare sectors, while energy, raw materials, and industrial sectors lagged.

A noteworthy trend is that as the U.S. economy has grown larger, the military-industrial complex has shifted from a growth engine to a fundamental economic base. The marginal contribution of individual wars to the overall economy has steadily declined, with market drivers increasingly yielding to macro variables like inflation, interest rates, and fiscal deficits.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。