BlackRock's BUIDL has become an indispensable asset in the field of digital assets. However, its largest buyers are not traditional institutions, but DeFi.

Written by: Henry Kim, Ryan Yoon

Translated and organized by: BitpushNews

Core Summary

- The on-chain significance of BUIDL is not that BlackRock issued a token, but that Ethena, Ondo, Frax, and Spark use BUIDL as a building block for their dollar products, transforming an institutional fund into a fundamental asset within the DeFi supply chain.

- The choice of BUIDL by protocols is not for yield, but because it satisfies three conditions simultaneously: clear legal claims, on-chain composability, and existing compliance. No other asset can provide all three at once.

- The supply chain does not stop at layer one. As BUIDL is processed into USDtb and further transformed into dollar products specific to ecosystems, the demand for underlying assets rises with the emergence of each new ecosystem.

- BUIDL reveals a brand new channel for tokenized asset distribution. Its clients are not discovered through traditional sales channels but through DeFi protocols—a customer group that does not exist in traditional finance. Without recognizing this channel, the next BUIDL will not appear.

From Institutional Products to Protocol Infrastructure

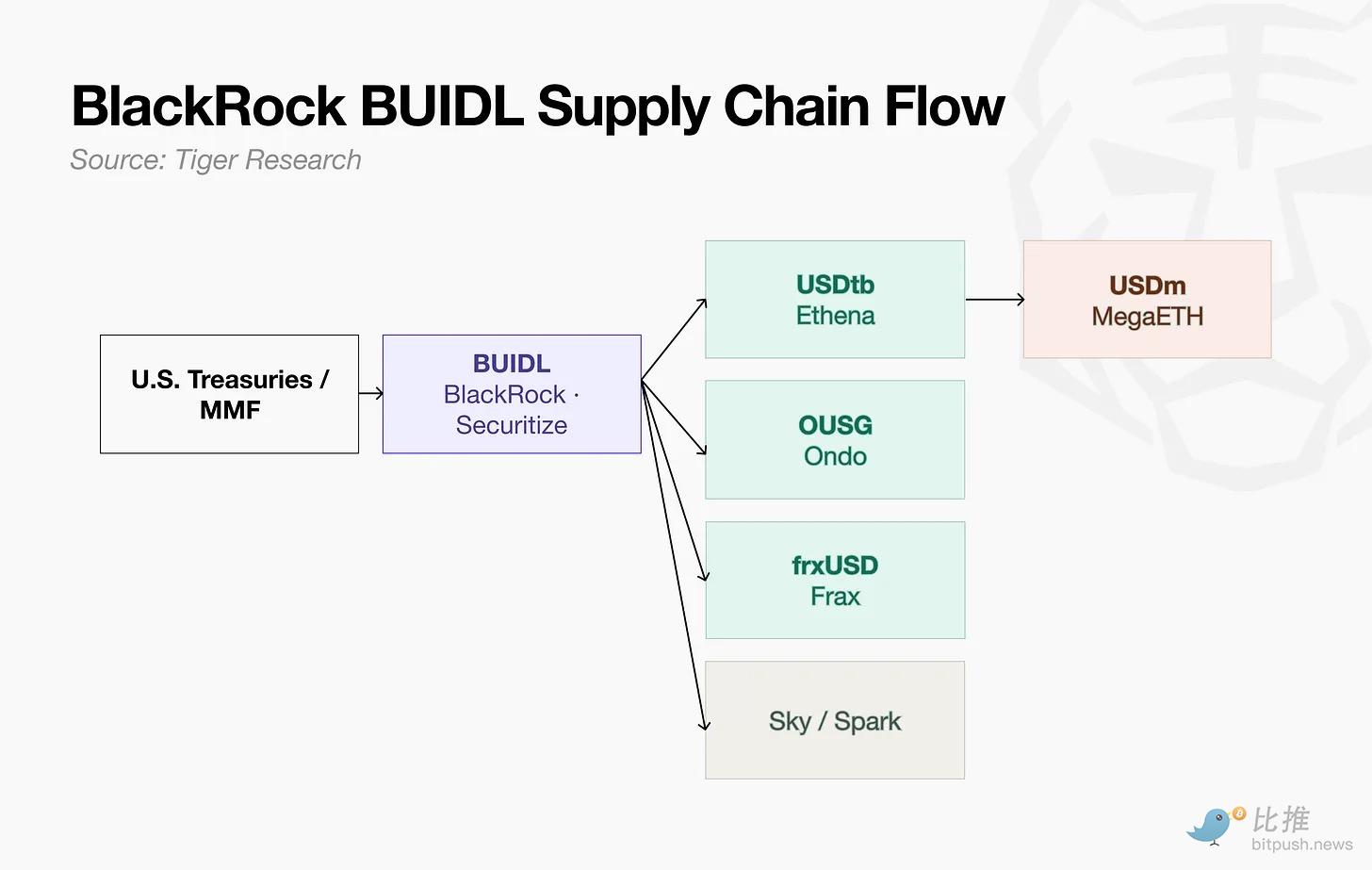

BUIDL was initially designed for institutions: providing exposure to cash and U.S. Treasury bonds, limited to accredited investors, with a minimum subscription amount of $5 million.

However, the first movers were DeFi protocols, not traditional institutions. They purchased not merely for yield, but for the following three reasons:

- Legal Clarity: Issued under Rule 506(c), investor rights are protected under U.S. securities law. Protocols can clearly explain asset properties and redemption processes in legal terms.

- Lower Compliance Costs: After the GENIUS Act, reserve design became very complex. BUIDL already meets institutional-grade collateral standards. The compliance burden is shifted, eliminating the need to build from scratch. This advantage has become increasingly evident as regulations tighten.

- On-Chain Composability: Can be used as protocol reserves, exchange collateral, or underlying for ecosystem dollar products.

As there were no other assets that met all three conditions at the time, BUIDL became the default underlying asset.

How DeFi Protocols Use BUIDL

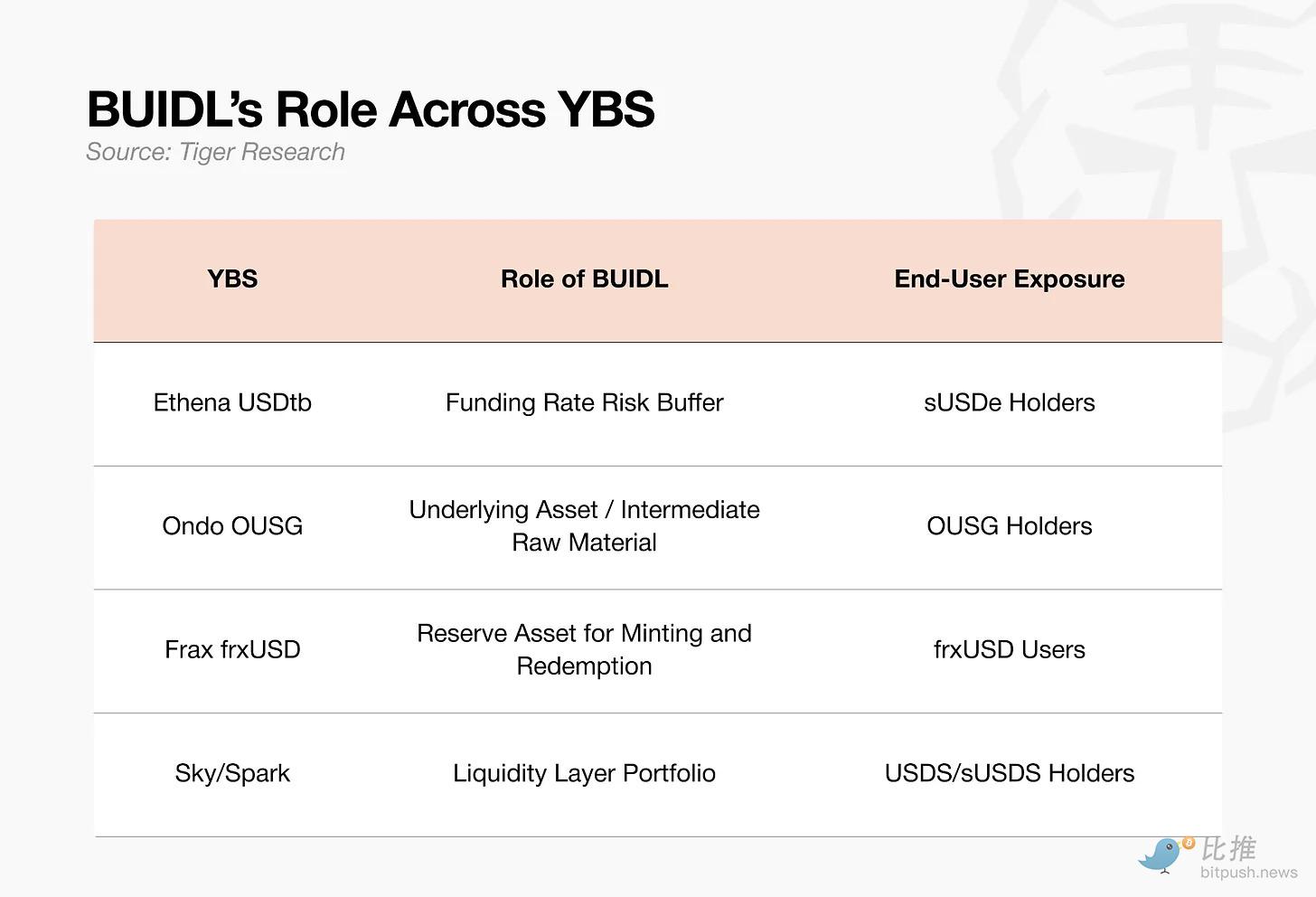

The key is not the mere fact that protocols hold BUIDL, but the specific roles that BUIDL plays within the framework of each protocol.

2.1. Ethena (USDtb): Funding Rate Buffer

Ethena's flagship product is the synthetic dollar USDe and its staked version sUSDe.

The revenue sources for USDe include:

- Staking rewards from collateral assets

- Funding rates from perpetual contracts (through Delta neutral strategies)

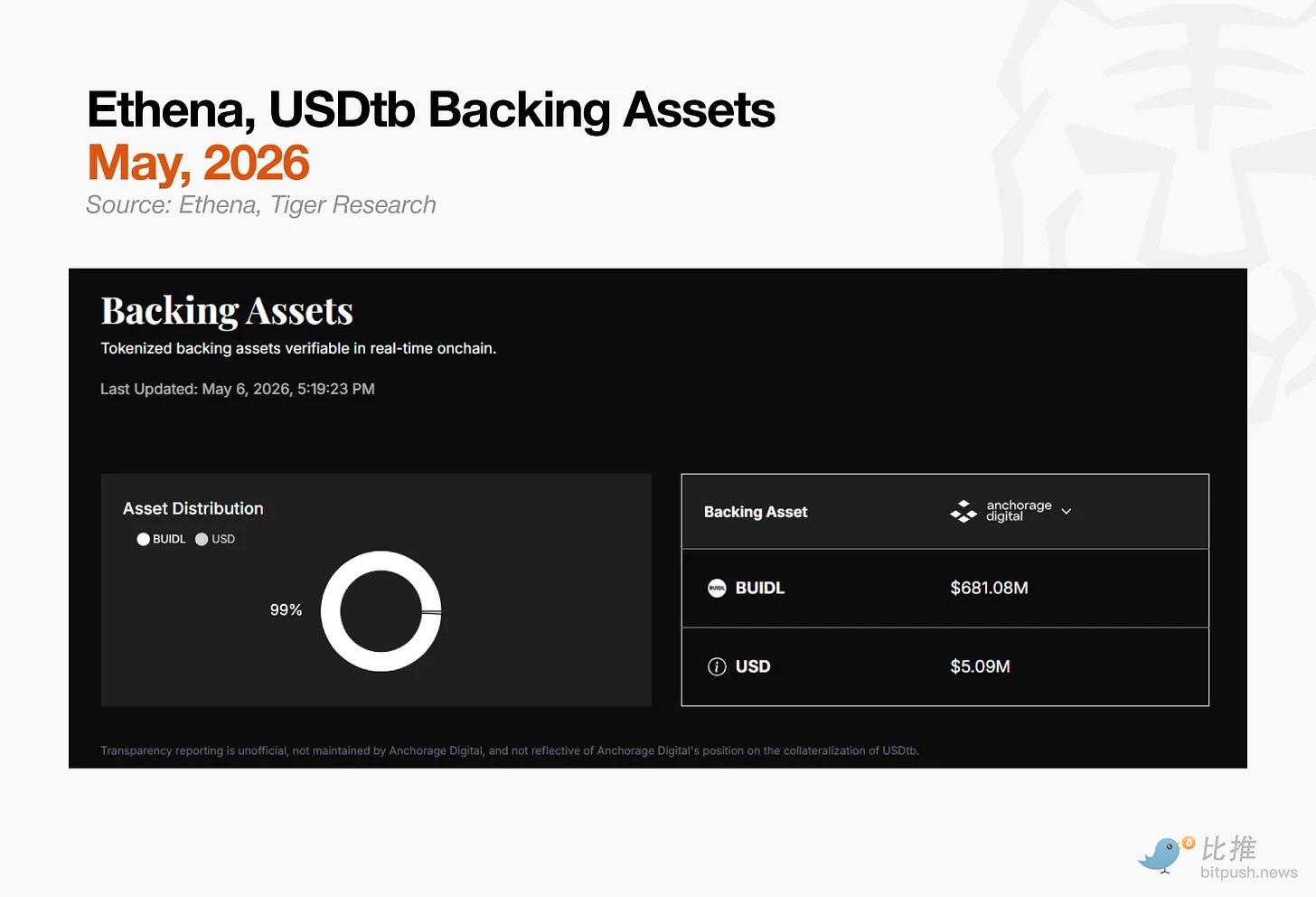

The second revenue source—funding rates—comes from Delta neutral strategies. USDe holds short futures positions equal to the size of the collateral to offset price risks. When long demand dominates, longs pay funding fees to shorts. Ethena, as the short side, directly collects this income.

Risks arise when funding rates turn negative. In a bear market, short demand may exceed long positions, causing the short side to pay funding fees. For Ethena, revenue turns into costs. If this situation persists, the insurance fund may be depleted, and the dollar peg of USDe will face pressure.

Ethena needs an asset capable of absorbing this pressure. USDtb fills this role, with its core reserves being BUIDL and USDC. The goal is not to enhance yields but to provide a defensive buffer, ensuring Ethena maintains structural stability during periods of negative funding rates.

2.2. Ondo (OUSG): BUIDL as Intermediate Input

OUSG (Ondo U.S. Treasury Fund) is a tokenized fund that brings institutional-level U.S. Treasury exposure onto the chain. Direct access to institutional money market funds like BlackRock BUIDL or Franklin Templeton FOBXX typically requires millions of dollars and accredited investor status. OUSG lowers this threshold, acting as an on-chain intermediary that makes these assets available to DeFi users.

BUIDL is a core component of OUSG's reserve composition, alongside Franklin Templeton's FOBXX and WisdomTree's WTGXX. OUSG repackages institutional assets that retail investors cannot access directly into a chain-based intermediate product.

2.3. Frax (frxUSD): Minting and Redeeming Reserves

frxUSD is a new type of dollar stablecoin designed by the Frax Protocol, aiming to maintain a stable value of 1 dollar like USDC or USDT. Its uniqueness lies in its reserve structure.

Existing stablecoins typically keep their reserves in cash or Treasuries held in offline bank accounts. Frax uses BUIDL (a tokenized Treasury on-chain) instead. Its mechanism is a direct 1:1 exchange: deposit BUIDL to mint frxUSD, return frxUSD to redeem BUIDL.

The end users do not directly interact with this structure. They use frxUSD as a stablecoin for payments or DeFi, while BUIDL operates in the background, supporting each minting and redeeming process.

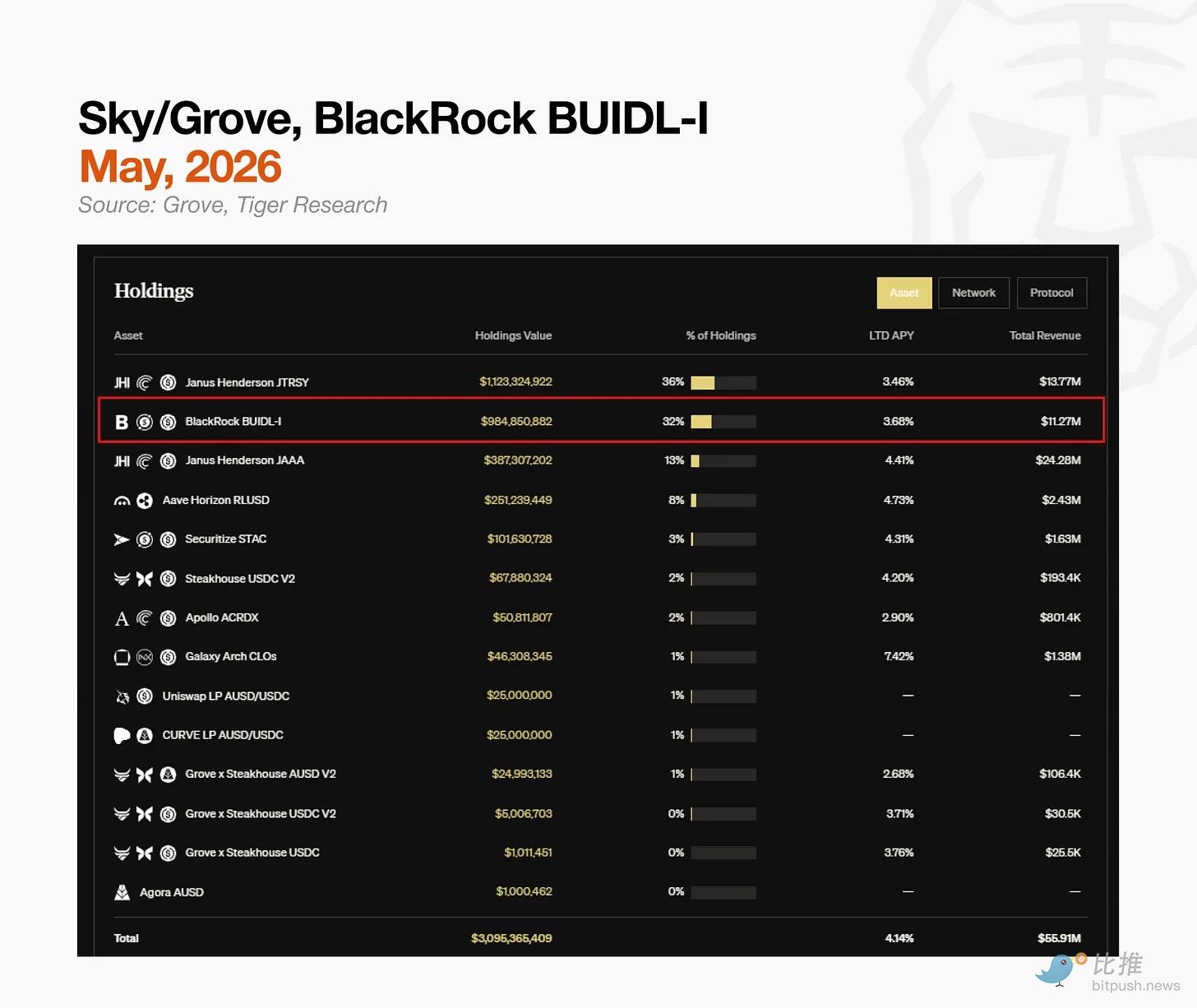

2.4. Spark's Tokenized Grand Prix (TGP) Allocation and the Common Thread with BUIDL

Spark's Tokenized Grand Prix (TGP) allocated $500 million of its $1 billion quota to BUIDL, with the rest allocated to Superstate's USTB and Centrifuge's JTRSY. Spark did not select a single reserve asset but built a portfolio.

Traditional asset management companies similarly mix Treasuries, money market funds, and credit instruments. The difference is that this portfolio operates on-chain, redeployed through DeFi tracks as collateral and liquidity.

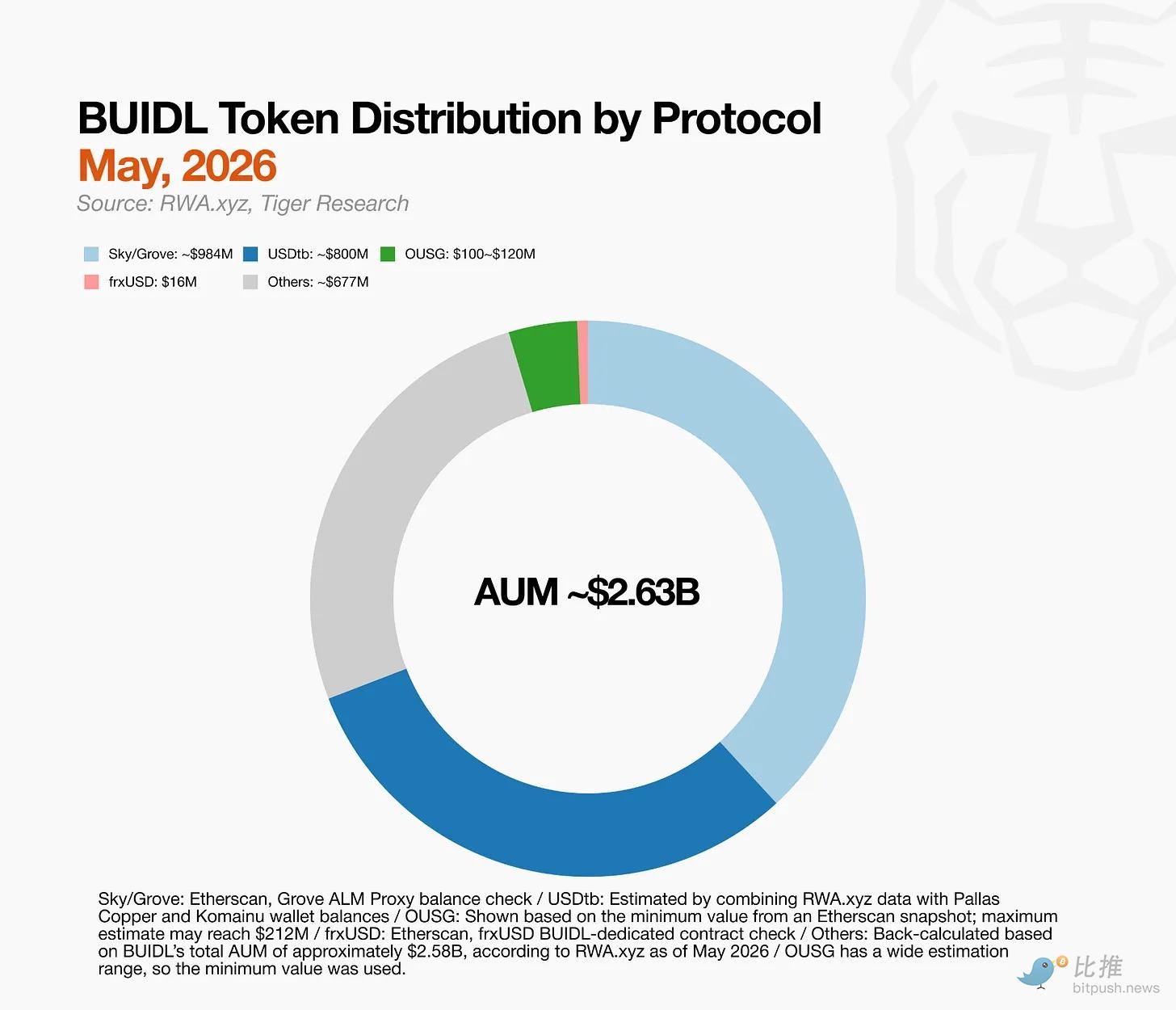

In the above four cases, BUIDL plays different roles: reserve asset, intermediate input, minting and redeeming support, and portfolio component. But there is one common pattern: in any case, BUIDL is not the final product. Protocols purchase BUIDL to fill their own systems, and this demand structure is already operating at scale.

Reprocessing of BUIDL: Composite Demand Structure

As mentioned earlier, various protocols have directly adopted BUIDL as a reserve asset. But the chain does not stop there. Products built on BUIDL are becoming reserves for new products, expanding the layer of derivative structures.

MegaETH's USDm is the clearest example. USDm is an ecosystem-specific stablecoin developed in collaboration with Ethena. Its reserve is USDtb, and the reserve of USDtb is BUIDL. As the demand for USDm within MegaETH grows, so does the demand for BUIDL.

Each new ecosystem entering this structure adds "clients" rather than "competitors." Speed of adoption is also an important differentiating factor in on-chain finance. Building an equivalent derivative structure in traditional finance requires months of regulatory review, legal contract signing, and custodial arrangements. On-chain, this process is significantly compressed. Within a regulatory framework, the scope of qualifying underlying assets is virtually unlimited.

In summary, BUIDL is unlocking composite demand by anchoring the continuously expanding on-chain structure in a foundation of secure real-world assets.

What Comes After BUIDL?

BlackRock built an institutional fund; Ethena, Ondo, Frax, and Spark adopted it as a foundational asset; MegaETH layered ecosystem-specific dollars on top of it. All this happened in less than two years since BUIDL's launch in March 2024.

This speed is driven not just by BlackRock's brand. Legal clarity, on-chain composability, and regulatory compliance: BUIDL was the only asset that could provide all three at that time. This first-mover advantage is tremendous, and it generates a compounding effect as more DeFi protocols integrate BUIDL into their reserves.

For the teams designing the next tokenized asset, the question is how to enter this market. Most take one of two paths: either assume that tokenization itself will generate demand, or replicate the distribution model of traditional finance through sales teams, broker networks, and existing channels.

BUIDL took a third route. DeFi protocols, including Ethena, Ondo, Frax, and Spark, were the first adopters. Exchanges and institutions such as Deribit, Binance, and OKX followed suit. BUIDL found a client segment that does not exist in traditional finance.

These clients purchase assets and build their own products on them, which then become the foundation for the next protocol. They are not clients acquired through sales but customers attracted through "design." Without recognizing this customer group, the next BUIDL will not materialize.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。