The data center serves as the safety net, providing upward elasticity for the cryptocurrency business when the market heats up.

Written by: Prathik Desai

Translated by: Chopper, Foresight News

In the first quarter of 2026, Galaxy Digital's cryptocurrency asset holdings continued to be under pressure, but its operating business has begun to decouple from the cryptocurrency market cycle. The company believes that integrating the two is the correct strategy. In the first quarter, Bitcoin fell more than 20%, and Ethereum dropped about 30%, yet Galaxy's proprietary trading volume remained relatively stable. This is the first clear signal that its business is beginning to shake off the cyclical fluctuations of the cryptocurrency bull and bear markets.

Previously, when analyzing Galaxy's financial report, I suggested that the Helios data center business is expected to become a tool to hedge against the cryptocurrency cycle. At that time, this judgment was just a forward-looking prediction, relying on the project being completed on time and signed cash flow materializing.

Entering April, the first batch of data centers at Galaxy's Helios facility in Texas was officially delivered to CoreWeave, marking the company's transition towards a high-margin, low-cyclicality data center track. Although the current revenue from data centers is still small, starting in the second quarter of 2026, the company's overall financial performance may welcome a significant turning point.

This article will analyze why Galaxy chose to develop both businesses in synergy and how this will help it achieve stability that is difficult for other companies to attain.

First Failure of Cycle Linkage

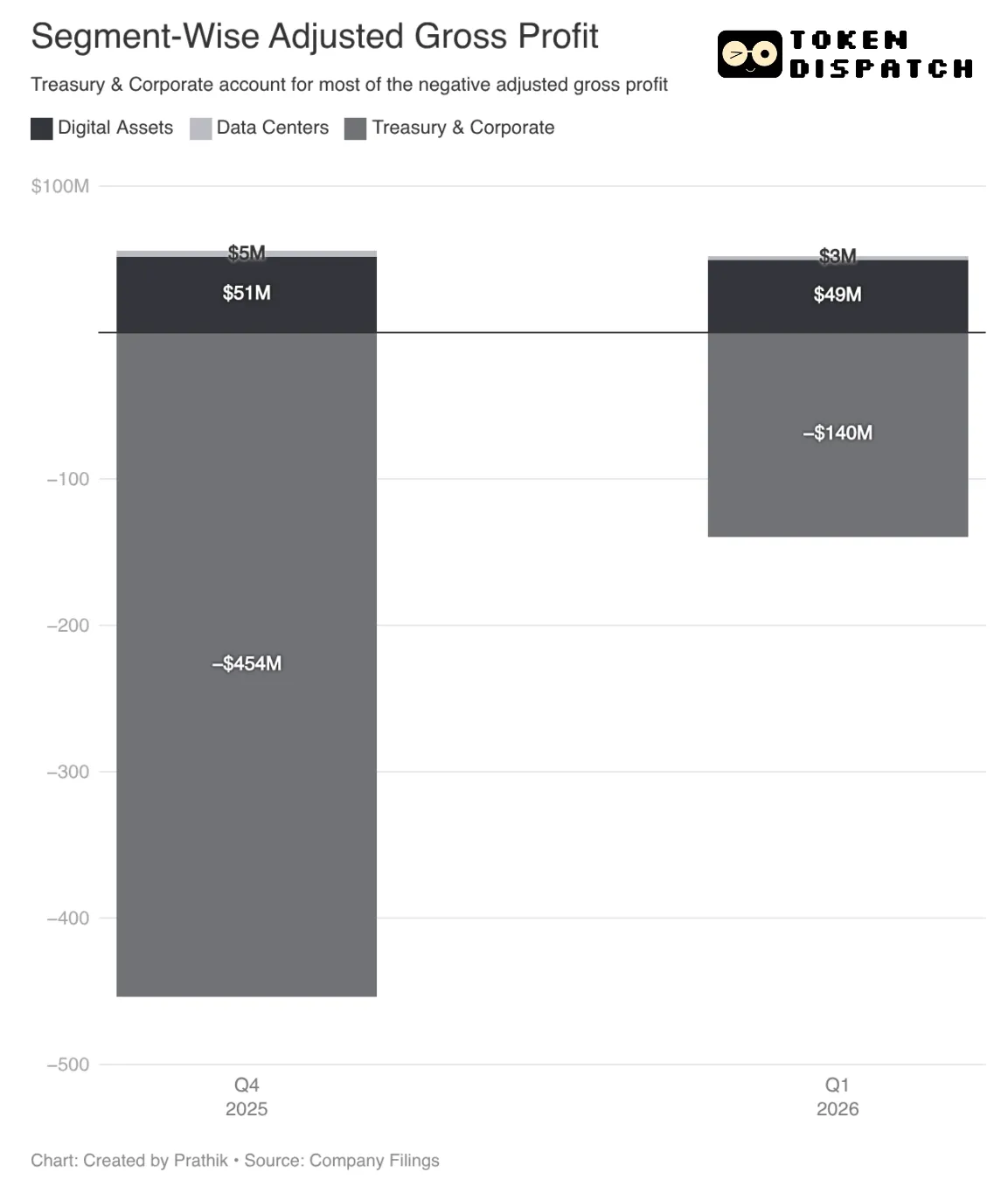

From the financial report, Galaxy remains a typical cryptocurrency company. In the first quarter of 2026, the adjusted EBITDA loss was $188 million, almost entirely stemming from an adjusted gross loss of $140 million in the financial and corporate sectors, mainly due to the valuation adjustment of cryptocurrency asset holdings. As of March 31, 2026, Galaxy's cryptocurrency asset holdings have shrunk to $667 million, down 27% from $920 million at the end of last year.

The cryptocurrency asset business segment covers cryptocurrency trading, lending, asset management, and infrastructure businesses, and this quarter still recorded an adjusted gross profit of $49 million, nearly flat compared to $51 million in the fourth quarter.

Declining cryptocurrency prices led to participant losses, sharply reducing trading volume and impacting Galaxy's business. This also reduced the scale of collateralized assets on which Galaxy relies to earn interest.

The company's proprietary trading business also confirms this trend: quarterly trading volume was basically flat, while the overall trading scale of the industry contracted by more than 25%.

In the face of a market downturn, where does Galaxy's operational resilience come from?

Solid Fundamental Base

Diversifying risks by expanding product lines and enriching customer structure is the core secret to Galaxy maintaining stability while peers are under pressure.

Over the past 18 months, the company has continually layered service fees and recurring revenue into its trading business. The asset management segment recorded a net inflow of $69 million, despite the valuation reassessment causing the management scale to fall from $11.4 billion to $8 billion. After the end of the first quarter, Galaxy secured a $75 million asset management order from a single client, marking one of the largest single mandates in its history.

Due to the drop in coin prices and the natural roll-over of loans maturing, the lending business contracted by 20%, but the company continues to add new clients.

In May, Galaxy will launch a fintech hedge fund focused on tokenized infrastructure, while also opening the GalaxyOne popular trading application to enterprises, allowing institutions to complete trading, custody, financing, pledging, and cryptocurrency research services all in one place. Both new businesses are expected to operate independently of Bitcoin price fluctuations, creating stable recurring revenue.

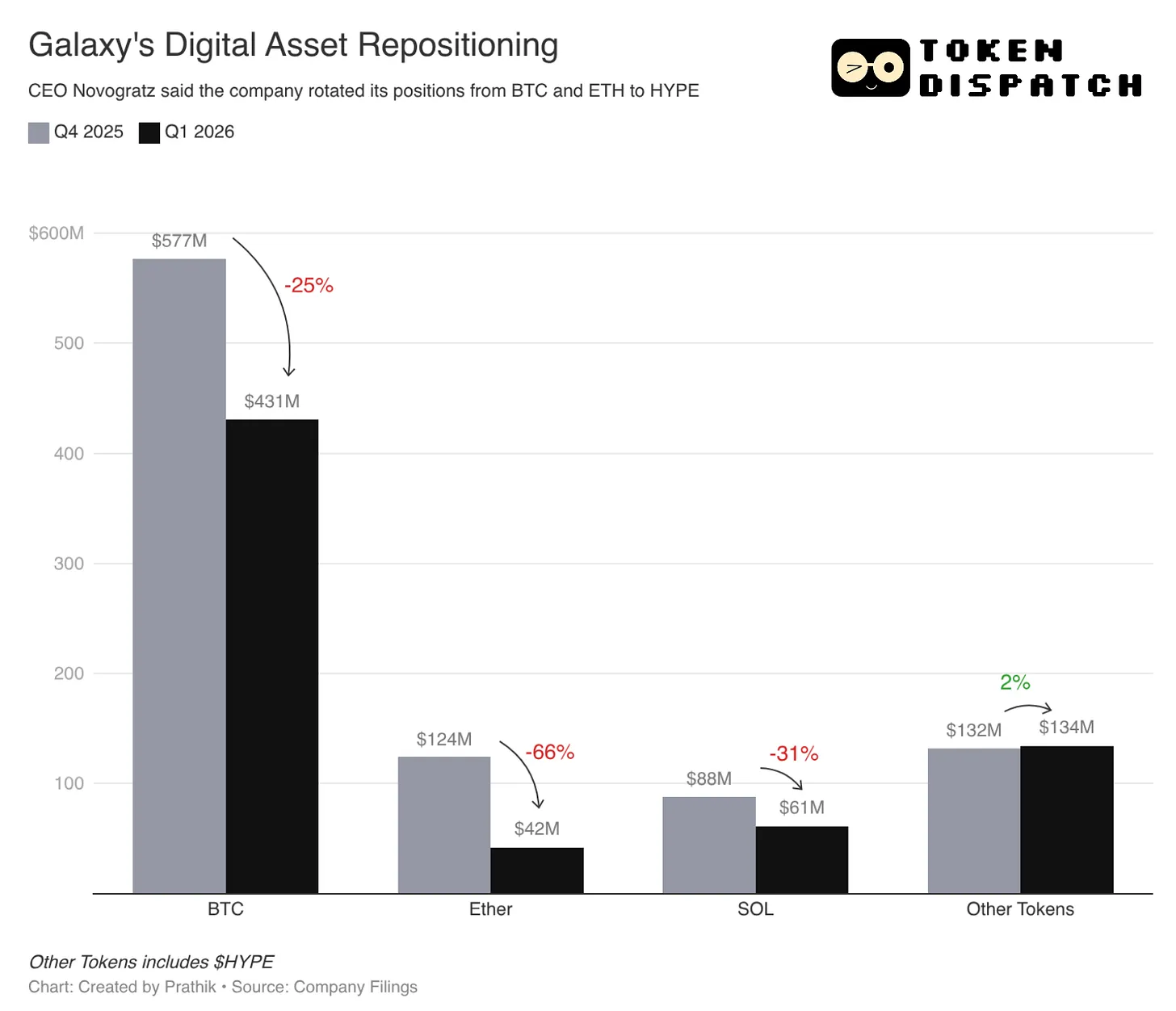

Another strategy is asset structure rebalancing. Galaxy has proactively reduced its Bitcoin exposure, reallocating a significant portion of its balance sheet to Hyperliquid, resulting in its overall portfolio outperforming the cryptocurrency market.

For investors and analysts, the biggest highlight is that the Texas data center has finally officially commenced operations.

Data Center: New Growth Engine Launched

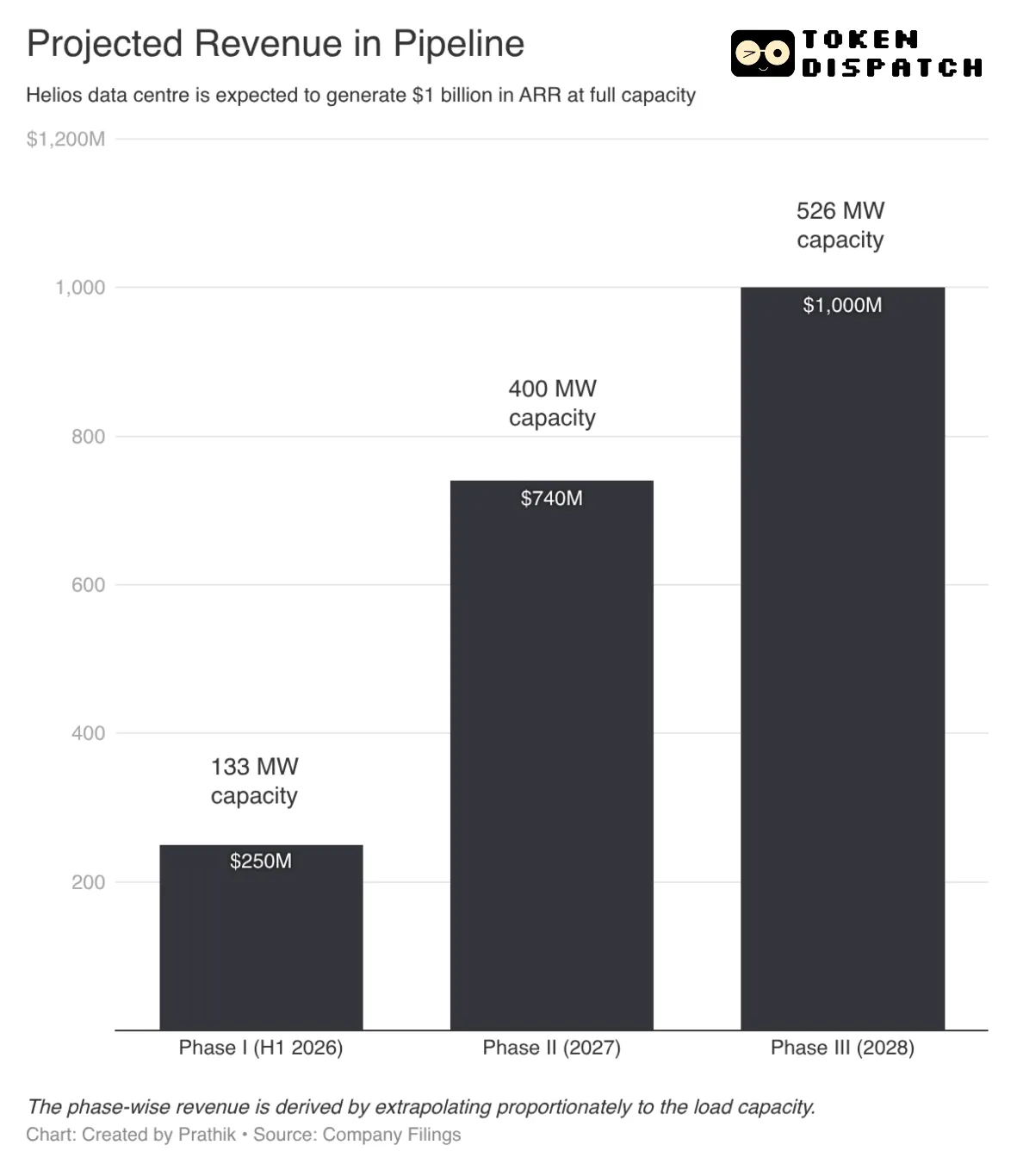

In the first quarter, Galaxy's Helios data center delivered its first batch of facilities to CoreWeave, and it is expected to achieve $1 billion in annualized revenue by 2028 after full load operations.

The originally planned Bitcoin mining park has now transformed into a mature AI data center, with power distribution, cooling, and network links all fully operational.

Currently, data center revenue is only $3 million, still small in scale, but the project strictly adheres to the commissioning timeline of 133 megawatts for the first phase. The three most notable features of this business are: high gross profit, low cyclicality, and long-term locked cash flow. Contracts last up to 15 years, with an EBITDA profit margin of nearly 90% on the leasing level. In the second half of 2026, once the first phase is fully operational, Helios alone is expected to contribute annualized revenue of $250 million, completely decoupled from cryptocurrency prices.

For reference, in this quarter, Galaxy's digital asset segment recorded an adjusted gross profit of $49 million, translating to an annualized revenue scale of about $200 million; while Helios Phase 1, with $250 million in annualized revenue and a 90% EBITDA profit margin, has surpassed the existing core cryptocurrency business.

In addition, Galaxy has obtained approval for an additional 830 megawatts of power capacity from the Texas Electric Reliability Council and is connecting with more potential tenants beyond CoreWeave for capacity expansion.

The company is unwilling to overly rely on a single business or client, and President Christopher Ferraro has also clearly favored a multi-tenant, multi-park expansion strategy.

However, how will it fund these multiple sites? Each site requires capital-intensive computing capabilities, cooling equipment, and other infrastructure.

In the Helios Phase 1 project, the end client behind CoreWeave is a trillion-dollar market capitalization investment-grade public company, and its high-quality creditworthiness directly optimizes Galaxy's future data center project financing conditions.

Galaxy Dual Business Model

Galaxy's two major business units have completely different funding needs, profitability curves, and performance visibility. On the surface, the synergy is limited, and outside observers commonly wonder why the company doesn't directly split and operate independently.

The company judges that both businesses still have cyclical linkages in the future and should not be simply separated.

Most people see Galaxy as an ordinary cryptocurrency company on the verge of spinning off its data center business. But they overlook the connection between its cryptocurrency trading and data center operations. When Galaxy's data center business achieves annual revenues of $1 billion with an EBITDA profit margin of 90%, it will be fully capable of operating its cryptocurrency infrastructure business steadily in a bear market.

The data center serves as a backstop, while the cryptocurrency business provides upward elasticity when the market recovers. This dual business model can lower the group's capital costs overall, hedge against each other, and reduce overall risk.

The core cryptocurrency business does not have to bear the downturn cycle alone, it only needs to cover variable costs to stabilize the fundamentals, as seen in the first quarter of this year; the demand for data centers comes from technology giants locking in computing power resources, which is itself unrelated to token market conditions. With a cryptocurrency business that generates stable cash flow, Galaxy also possesses stronger capabilities to self-finance new projects, and the speed of expanding new parks far exceeds that of independent data center startups.

Currently, the cyclical signs displayed in just one quarter are still preliminary observations. To establish a long-term trend, continuous verification will be needed over the next two to three quarters.

However, it is undeniable that the structural direction Galaxy is building is correct. The data center provides high gross profits, long-term locking, and predictable cash flows; the trading segment undertakes low gross profits, high turnover, and strong cyclical cryptocurrency business.

As Novogratz stated, if this performance continues for another three quarters, he will definitely celebrate.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。