Author: Kuri, Shenchao TechFlow

Every time someone makes a lot of money in the US stock market, the onlookers always do the same thing first: they check his holding report to find the next stock to buy.

Recently, the report that has been checked the most belongs to a 24-year-old German named Leopold Aschenbrenner.

In March of this year, domestic media reported extensively about him, with similar headlines; for example, the genius fired by OpenAI wrote a 165-page paper predicting AI trends, started a hedge fund, and manages 5.5 billion dollars...

But a label is just a label. What truly draws people's attention to this fund is that it does not buy Nvidia, does not buy OpenAI, and does not buy any companies that make AI models. It only buys things that AI cannot survive without, such as power generation, chip manufacturing, optical communication, data centers...

In his own words from the paper, the bottleneck of AI is not in the algorithms, but in electricity and computing power. The entire fund is betting that this statement is correct.

Investment bloggers on social media call him the “poster child of the US stock market in the AI era,” or the AI version of stock god Warren Buffett. This title has resurfaced recently because the degree to which he is betting correctly has become a bit absurd.

According to data released by the copy trading platform Autopilot on May 1, a simulated portfolio mirroring his holdings has risen by 61% in two months. Based on this calculation, the scale of his fund has approached 9 billion dollars.

Where is the money coming from? Mainly from two heavily invested stocks. Bloom Energy, a fuel cell company providing off-grid power to AI data centers, has seen its stock price rise by 239% since the beginning of the year.

According to the holding report made public at the end of last year, he holds 875 million dollars in stock and options of this company, which has now inflated to nearly 3 billion.

Then there’s Intel. The same holding report shows that in Q1 of 2025, he bought 20 million Intel call options, when Intel’s stock price was around 20 dollars, and mainstream judgments on Wall Street believed Intel was not doing well.

Last week, Intel soared to 113 dollars, reaching a historic high not seen in 25 years. Within a year, it nearly quintupled; the return on his options is even more outrageous than on stocks.

I can understand the impulse of onlookers. The American investment website Motley Fool published four articles in one day dissecting his holdings, and the overseas Reddit investment board is discussing whether to copy his homework. Everyone is trying to find the next Intel in his holdings report.

But you must know that holdings reports typically have a 45-day delay. By the time you see what he bought, the market has already moved halfway.

More crucially, even if you knew his holdings in real time, you still couldn’t replicate the reasons why he continuously bet correctly.

The circle is the greatest Alpha

Firstly, the most mystical aspect about Leopold Aschenbrenner is his paper on AI written in 2024, which almost predicted the current direction of AI development and investment trends.

The core argument can actually be summarized in one sentence: the training computing power for AI models increases by about half an order of magnitude each year, and at this rate, general artificial intelligence (AGI) capable of human-like abilities will appear around 2027.

But to maintain this growth rate, the key limiting factors are not on the algorithmic level, but in electricity, chip production capacity, and physical space. The electricity consumption of a single training cluster will jump from megawatt-level to gigawatt-level, nearing the output of a large nuclear power plant.

This is the underlying logic of his entire fund. The speed of AI development is determined by physical bottlenecks, so you should invest in the bottlenecks themselves.

This judgment sounds like a conclusion derived from extensive research done by a clever person in a study. However, I believe it is the circle that enabled him to form this judgment.

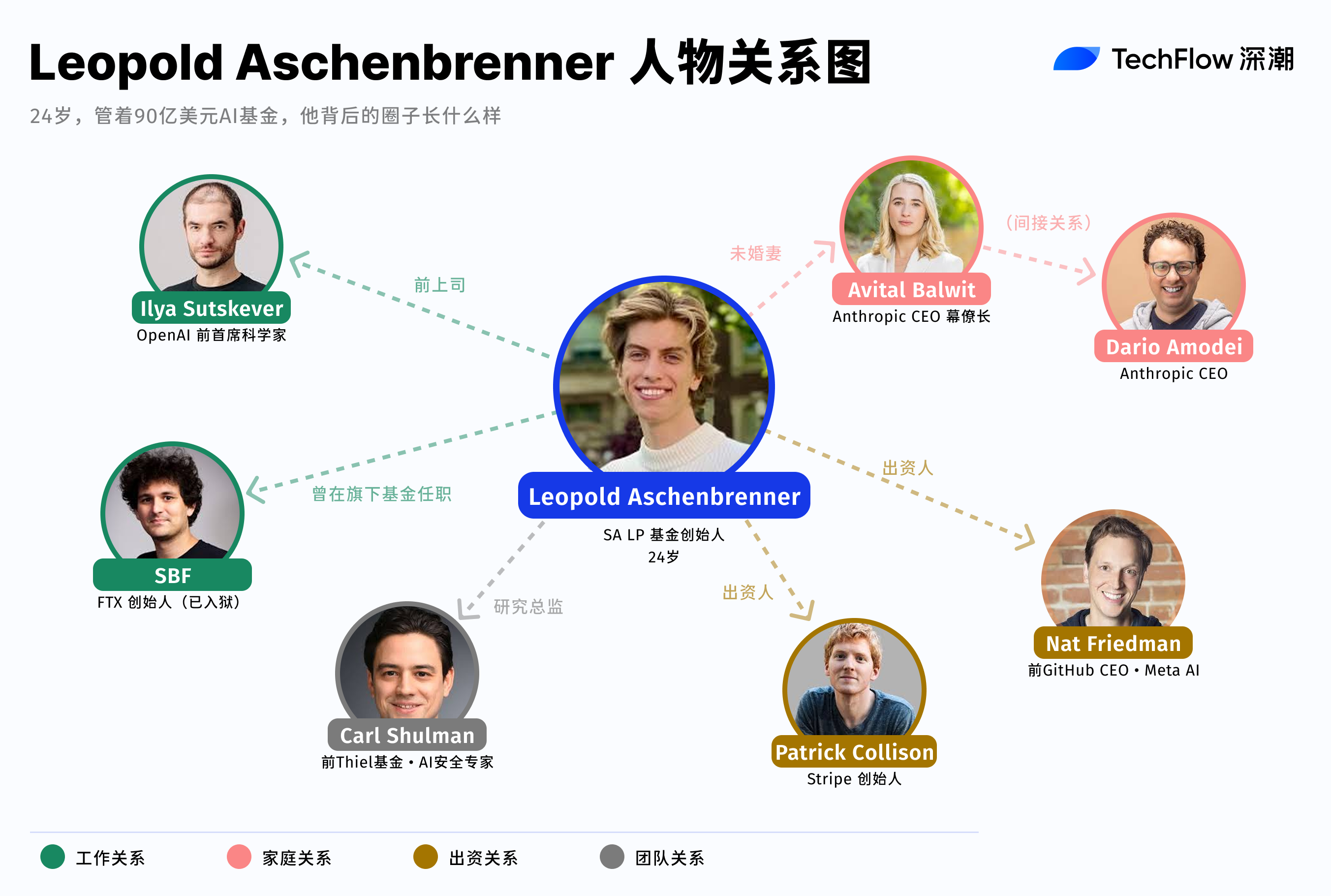

Before writing his paper, he worked for a year in OpenAI’s Superalignment team. This team specializes in studying how to control AI that is smarter than humans and reports directly to chief scientist Ilya Sutskever.

During that year, he witnessed internal training programs, actual power consumption, and the specific power and chip requirements of the next generation of models. When he made the judgment about "gigawatt-level electricity consumption" in his paper, his basis may have been the internal roadmap in the lab.

In April 2024, he was fired by OpenAI; the catalyst was an internal memorandum he wrote to the OpenAI board, warning that the company's safety measures were insufficient and posed a risk of infiltration by foreign intelligence agencies.

This memorandum caused tension between management and the board, and OpenAI subsequently fired him on the grounds of "leaking information."

Two months later, the paper was published. This paper is less of an independent study and more of a public version of his internal understanding at OpenAI.

AI papers solve the problem of "what direction to look." But in investing, knowing the direction is far from enough.

AI needs more electricity; this judgment has been voiced by many analysts since 2024. What is truly valuable is timing and position, such as whether you dare to throw 20 million call options into Intel when the stock price is 20 dollars.

This confidence does not just come from believing in the grand trend of AI, but from knowing specifically which company is signing large power procurement contracts, which data center is expanding, and what the scale of demand is.

And the fund founded by Leopold Aschenbrenner, Situational Awareness, has investors who just happen to sit in the front row of these decisions.

The LPs of this fund include the two founders of Stripe, whose company handles payment flows for half of the tech companies in Silicon Valley and can directly perceive the acceleration of infrastructure spending;

and another investor is former GitHub CEO and current Meta AI product head Nat Friedman, who is involved in decision-making for power procurement every day.

What they bring to the fund is not just initial capital, but a continuously updated information pipeline.

Additionally, the research director in his fund is also a key role in this chain. Carl Shulman, an old veteran in the field of AI safety, previously worked at Peter Thiel's hedge fund Clarium Capital, responsible for converting the insights from the AI circle into executable trading strategies.

His holdings also include an easily overlooked corner of crypto.

The holding report at the end of last year showed that he established positions in CleanSpark and Bitfarms, both of which are Bitcoin mining companies that are transforming their BTC mining facilities into AI computing centers.

Crypto mines naturally possess large-scale power access and cooling systems, which are precisely the most scarce resources for AI data centers.

Interestingly, he is not unfamiliar with the crypto industry. In 2022, he worked for nine months at the Future Fund, a charity fund founded by SBF, leaving just before FTX collapsed.

Whether this experience directly influenced his judgment of mining companies is unknown to outsiders. But it can be confirmed that he is one of the very few people who has deeply interacted with both the crypto industry and cutting-edge AI laboratories. This intersection itself is also a rare recognition position and potential networking link.

Another detail is that his fiancée Avital Balwit is the chief of staff of Anthropic’s CEO Dario Amodei. Anthropic is the parent company of Claude and is also OpenAI’s most direct competitor.

He has worked at OpenAI, and his fiancée is next to Anthropic's CEO. The two companies at the forefront of the AGI race see him having practical experience at one and daily contact at the other.

Last year, Fortune magazine interviewed more than a dozen insiders who have interacted with him, and the conclusion was that he excels at "packaging ideas brewing in Silicon Valley labs into narratives."

I feel this description is too polite. What he does is more straightforward, which is to bet on the public market using the knowledge obtained from his private circle. The published AI papers are the declassified versions, while his investment fund is the complete version.

A positive feedback loop that outsiders cannot access

Looking back, Leopold Aschenbrenner's fund has chosen a rather uncommon structure.

Most funds in the AI field take the venture capital route, investing in early-stage companies and betting on who can become the next OpenAI. He did not take this path. According to Fortune, he explicitly rejected the VC model when founding the fund, reasoning that the impact of AGI is too significant, and only in the most liquid public markets can investment judgments be fully expressed.

This choice itself reveals a consensus in his circle: the biggest investment opportunities in the AI era may lie within those old companies that already have physical infrastructure.

It could be a fuel cell company with ready access to power, a semiconductor giant with wafer fabrication lines, or a Bitcoin mining enterprise with mining facilities and cooling systems. These companies have been publicly listed for many years and have good liquidity, but most analysts are still pricing them based on old valuation frameworks, not seriously incorporating the variable of "AI infrastructure necessity" into their models.

This is his arbitrage space.

People in the circle already know the pace and scale of the expansion of AI infrastructure while the public market is still pricing using old logic. The spread in between is the source of profit.

This information advantage has another characteristic: it reinforces itself.

The better the fund's returns, the more central industry people are willing to become LPs. The more LPs, the denser the decision-making layer information the fund can access. The denser the information, the higher the accuracy of the bets. This is a positive feedback loop, and for outsiders, the threshold to enter this loop will only get higher.

Of course, this loop also has a fragile side. The highly concentrated holdings, combined with significant leverage, mean the entire fund is highly dependent on a single narrative. As long as the premise of "AI infrastructure continues to expand" remains valid, everything will go smoothly.

But if the pace of AI development slows or energy bottlenecks are circumvented by some technological breakthrough, the speed of the retreat of concentrated positions will far exceed that of building positions. He is betting not just on direction, but on rhythm. Once the rhythm is mismatched, the consensus in the circle may become a collective blind spot instead.

Returning to the initial question.

Everyone is studying his holdings, trying to replicate his operations. But behind stock god-level returns are structural conditions.

The papers are public, the holding reports are public, and his investment logic is also stated clearly in podcasts and interviews. But even if you fully understand each of his judgments, you still cannot replicate the position he was in when he made these judgments.

Positions can be traced back, returns can be envied, but the source of cognition cannot be shared. This is probably the most valuable form of asymmetry in this era.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。