Author: FinTax

1 Background

In recent years, significant price fluctuations have brought gold, a traditional asset, back to the center of the market: In 2025, the annual increase in gold prices exceeded 50%, and in January of this year, it even broke the $5000/ounce mark, once approaching $5600/ounce. However, since March, with the ongoing geopolitical conflicts in the Middle East and shocks in energy prices, gold prices have plummeted, completely erasing all gains made this year, leading to the dramatic changes in the market that popularized the term "gold monkey market" on social media. Concurrently, there has been a rising narrative around "gold tokenization"—on the other side of the financial world, people are actively exploring more possibilities for gold on the blockchain.

On March 19, the World Gold Council announced plans to construct a new type of shared infrastructure for the digital gold market and proposed the concept of "Gold as a Service," which aims to develop a digital issuance management system connecting physical gold custody with gold-backed products, to provide a standardized system for the issuance, trading, and management of various digital gold assets. At the same time, tokenized gold assets such as PAXG and XAUt have evolved from concepts into scaled markets, with institutions accelerating their strategic layouts in related fields.

Gold tokenization provides a new way to express the value of traditional gold. Compared to physical gold and other gold products, tokenized gold has a lower investment threshold, supports 24/7 trading, and ensures investor rights through standardized custody, third-party audits, and redemption mechanisms, offering investors a secure and convenient alternative investment channel. Therefore, many voices believe that gold tokenization could be the next "dark horse" in the RWA sector.

Is gold tokenization a "dark horse" or just a "gimmick"? This question is worth pondering. To explore the answer, one cannot rely solely on narrative emotions but must return to three questions: What are the different product forms of gold that already exist, how does tokenization differ from physical gold, gold ETFs, etc., and does it have real functional increments? Has the market and regulatory framework for tokenized gold formed a transparent market sufficient to support investor trust? What unavoidable risks do projects planning to lay out tokenized gold and ordinary investors face?

2 Market Status of Tokenized Gold

2.1 Core Concept

Tokenized Gold refers to the digitization of ownership, beneficial rights, or other economic rights of physical gold through blockchain and smart contract technology, converting them into digital tokens on the chain. Typically, each token is anchored to a certain weight of physical gold, which is stored in a vault by a gold custodian. Since gold tokens reside on the chain, users can send them to others' wallet addresses or conduct on-chain transactions just like other cryptocurrencies.

The operational process of tokenized gold has several key components: (1) Custody: The project party purchases physical gold and stores it in a secure and insured vault, ensuring that digital tokens are backed by real-world assets; (2) Minting: The project party uses smart contracts on the blockchain to mint digital tokens, with the number of tokens minted matching the amount of gold in reserve; (3) Redemption: Some tokenized gold projects support physical redemption, where when users convert tokens into physical gold, the corresponding number of tokens is destroyed, keeping the token supply consistent with the gold reserves; (4) Reconciliation, auditing, and certification: To maintain trust in a decentralized system, the project party must hire an independent third-party audit agency for regular inventory checks and verifications; some projects also use oracle networks to provide proof of reserves.

For example, Tether Gold (XAUt) represents ownership of one ounce (31.1035 grams) of gold held in a Swiss vault and compliant with the London Bullion Market Association (LBMA) delivery standards (purity usually 99.9%). The operating entity, TG Commodities, purchases physical gold from the Swiss market and stores it, allowing investors to check the unique serial number, weight, and purity of specific gold bars through their blockchain address. There are two paths for redeeming funds: one is to redeem a complete physical gold bar, which requires users to hold a certain minimum amount of XAUt to initiate the request; the other is to exchange XAUt for US dollars or Tether (USDT) through compliant channels like Bitfinex.

2.2 Market Development Status

Currently, tokenized gold is dominated by mainstream products such as Tether Gold (XAUt) and PAX Gold (PAXG), which together account for the vast majority of market share. Meanwhile, there are also non-mainstream gold token products in the market like Kinesis Gold (KAU), Pleasing Gold (PGOLD), and Matrixdock Gold (XAUm), which have established advantages through differentiated competition, though they are relatively small in scale. Furthermore, the World Gold Council plans to launch a token called "Pooled Gold Interests" (PGI) in 2026, which adopts a trust rights model different from the physical collateral structures of mainstream tokens like XAUt and PAXG, further promoting market diversification under a duopoly competition landscape.

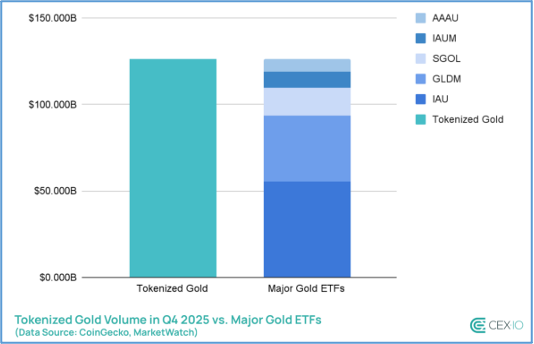

In terms of market size, according to statistics (source: Rwa.xyz), as of April 17, 2026, the total market capitalization of tokenized gold reached $5.27 billion. Research reports indicate (Cex.io) that the total trading volume of tokenized gold for the whole of 2025 is expected to reach $178 billion, with trading volume soaring to over $126 billion in the fourth quarter, far exceeding previous periods and even slightly higher than the total of the five largest gold ETFs. The investor base is also gradually expanding, with the number of tokenized gold holders increasing by over 115,000 people in the past year, a 14-fold growth compared to 2024.

Figure 1 Estimated Total Market Capitalization of Tokenized Gold

Figure 2 Total Trading Volume of Tokenized Gold for the Entire Year of 2025

In terms of application prospects, the continued entry of financial institutions is driving the expansion of the tokenized gold market. The implementation of tokenized gold also brings new business innovation space for traditional financial institutions and emerging crypto-financial platforms. ETP market makers, Flow Traders, have launched 24-hour over-the-counter liquidity services for tokenized assets, promoting efficient cross-platform trading of popular assets like tokenized gold; at the same time, the tokenization of Hang Seng Gold ETF and Hex Trust supporting HSBC to put gold assets on-chain… In the future, tokenized gold may become a foundational asset in building on-chain portfolios, thus opening a true new era of on-chain asset management.

3 What Makes Tokenized Gold Different: Comparison of Gold Investment Tools

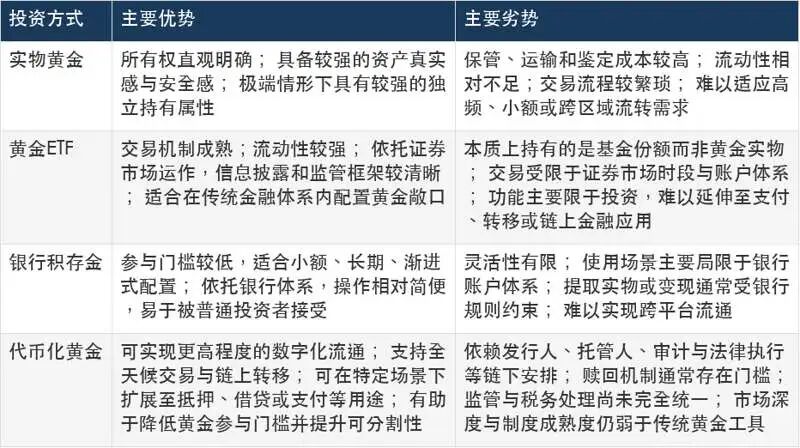

As a traditional safe-haven asset, gold plays an important role in investment portfolios. Aside from tokenized gold, the main ways investors gain exposure to gold include physical gold, gold ETFs, and bank accumulation gold. Physical gold exists in the form of bars, coins, or jewelry, being the most straightforward and traditional investment method, where investors directly purchase and hold physical gold, resulting in clear ownership and visible assets; gold ETFs, fully known as gold exchange-traded funds, are traded on stock exchanges, allowing investors to buy and sell ETF shares via securities accounts, with rights shares backed by physical gold, thereby indirectly acquiring returns from fluctuations in gold prices; accumulation gold refers to a type of gold investment product launched by commercial banks, where investors can accumulate gold shares by investing in terms of amounts or weights through regular investments or scattered purchases, and manage them through account forms. Different gold investment tools have varied ownership structures, trading methods, and usage scenarios, resulting in their respective advantages and disadvantages.

For the inconvenience of custodianship and high craftsmanship fees of physical gold investments, products like gold ETFs provide investors with more efficient trading tools but still face issues such as centralized settlements with multiple intermediaries, trading delays, and limited trading hours. Tokenized gold offers innovative solutions to these problems: first, it provides a digital token linked to physical gold, achieving similar investment functionalities as traditional products like gold ETFs, while also lowering the investment threshold through property rights segmentation; second, it frees investors from trading hour restrictions, supporting instantaneous and high-frequency trading scenarios, and generally has lower management fees than traditional products, theoretically allowing investors to experience better liquidity at a lower trading cost; third, it expands the sources of income for gold investment tools. Tokenized gold is expected to transcend gold's traditional functions as a diversified investment configuration and store of value, transforming into deployable capital, sparking new application scenarios such as gold pledging, lending, and more. Investors may profit not only from the price differences of gold trading but could also enjoy the returns brought by DeFi.

Different investment tools arise from diversified user needs, and it cannot be said that one form can completely replace another; however, it is undebatable that tokenization creates new possibilities for acquiring and trading gold. During the downtime of traditional products like gold futures and ETFs, tokenized gold serves a key price discovery function. As a historically valuable hard currency in the market, gold, under the innovative development of tokenization, has become easier to obtain and trade, holding unique value in enriching investor choices and promoting the integration of gold assets into the modern financial system.

Table 1 Comparison of Different Gold Investment Methods

2 Advantages and Disadvantages of Different Gold Investment Tools

4 Regulatory Landscape and Compliance Challenges of Tokenized Gold

4.1 Regulatory Models of Major Jurisdictions

The global regulatory policies for tokenized gold showcase a diverse pattern, with different countries and regions forming their own distinctive local policy models due to varying financial infrastructures, market environments, and regulatory features.

(1) United States: The U.S. has yet to issue specific regulatory documents governing tokenized gold. It is generally believed that if the issuance or sales arrangements of tokenized gold meet the identification criteria of investment contracts (i.e., the Howey Test), it is considered a security governed by the Federal Securities Law, including obligations for information disclosure and investor suitability management, under the oversight of the U.S. Securities and Exchange Commission (SEC). Additionally, tokenized gold may also be deemed a "commodity," thus falling under the jurisdiction of the U.S. Commodity Futures Trading Commission (CFTC).

(2) Europe: The development of tokenized gold in Europe is characterized by legislation, aiming to strike a balance between innovation and regulation. The European Union is promoting bills like DORA and MiCA to regulate token activities. Member states such as Luxembourg, Germany, and Switzerland have also set up pathways to provide special regulatory sandbox systems for RWA. However, how exactly tokenized gold is regulated still needs to be clarified based on the architectural arrangements and substantive nature of the tokenized gold projects.

(3) Hong Kong, China: If a tokenized gold project is classified as a "security token," it falls under the regulatory scope of the Securities and Futures Ordinance (SFO), requiring issuers to meet prospectus or private placement exemption requirements and implement customer due diligence and source of funds checks in accordance with the Anti-Money Laundering and Counter-Terrorist Financing Ordinance (AMLO). Additionally, any services related to issuance and trading must obtain a compliance license based on the virtual asset service provider licensing system.

4.2 Possible Compliance Challenges

As the wheels of technological innovation roll forward, complex compliance issues are gradually surfacing. First, the underlying assets provide the most basic credit for gold tokens. Whether the project structure and audit mechanisms are designed to effectively control underlying asset risks is a primary concern for project parties. This requires project parties to ensure clear ownership of physical gold, free from rights defects, and to pay attention to whether the gold being purchased has any encumbrances or pledges, with the source and quality of gold needing to be strictly verified and subject to regular third-party audits. Additionally, there should be sufficient, truthful, and timely disclosure of information, including details of the underlying assets, risk factors, and revenue mechanisms, to avoid regulatory penalties and class action lawsuits due to misrepresentation or concealment. Second, cross-border compliance and ongoing operations present challenges to the compliance capabilities of project parties. Given gold's global circulation properties, the locations of token issuance, custody, and investors may be in different countries or regions, subjecting them to multiple legal jurisdictions, which requires project parties to systematically outline the regulatory requirements and compliance obligations that their business activities may trigger and respond appropriately. Lastly, regarding taxation, the legal attributes and tax qualifications of tokenized gold remain ambiguous, while the nature of income generated from tokenized gold projects will significantly affect the applicable tax types and burdens. Additionally, from the asset side to the trading side, tokenized gold projects may trigger tax obligations at multiple stages and points, including issuance, income distribution, and secondary market trading, necessitating project parties and investors to engage in reasonable tax planning through timely updates on tax policies and seeking professional assistance.

5 Conclusion

Gold tokenization might be one of the most intriguing intersections between traditional finance and Web3 this year. Returning to the initial question, gold tokenization is neither a meaningless repackaging of old wine in new bottles nor an unconditional dark horse to bet on. On one hand, tokenized gold enhances the accessibility and liquidity of gold, possesses special value compared to traditional investment categories, and has already formed a certain scale market, presenting good development potential under the push of global policies and institutional layouts. On the other hand, we must also recognize that the foundational value of tokenized gold is still being solidified, with factors such as the safety of underlying assets, the quality of third-party audits, information disclosure and redemption mechanisms, and the global regulatory framework influencing whether it can secure a place in the fierce market competition. Nevertheless, the future of gold is being rewritten on the blockchain, and all of this is happening right now.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。