Author: Nic Carter

Translated by: Deep Tide TechFlow

Deep Tide Overview: U.S. military special forces made $400,000 using confidential information on Polymarket, which is just the latest scandal. Nic Carter points out that prediction markets are trapped in a vicious cycle: they rely on insider trading to produce accurate prices, but this makes retail investors feel that the market is manipulated and causes them to withdraw. This contradiction determines whether prediction markets can survive long-term.

As I wrote in February of this year, there is a serious insider trading problem in prediction markets, and it is not accidental. This leads to a significant failure pattern:

The social value of prediction markets comes from incentivizing insiders to leak confidential information with money, but this over time destroys retail investors' confidence in the market.

Two days ago, the largest scandal thus far broke out: the U.S. Department of Justice charged Special Forces Sergeant Gannon Ken Van Dyke with improper trading using confidential information. Before the Maduro raid, he made $400,000 on Polymarket. He is not an ordinary soldier but a senior Green Beret responsible for special operations planning and execution.

Simply put, while many people call for leniency because insider trading among congressional members is widespread (and legal), he should still go to prison. His actions could leak raid information to Venezuelans through trading activities, which is problematic both ethically and legally. While the Venezuelans may not have noticed, the government cannot accept such a precedent: elite combat personnel leaking details of upcoming operations for personal gain through market activities. I sympathize with Van Dyke, but he indeed violated the law and the confidentiality he swore to uphold.

This is just the latest in a series of real or suspected insider trading scandals occurring in prediction markets. Previously, Israel arrested two reservists for trading using military confidential intelligence on Polymarket. Markets regarding the timing of the Iran war, ceasefire agreements, Khamenei's assassination, and Biden's pardons are also under suspicion, but no one has been arrested yet. Kalshi and Polymarket have also flagged and suspended accounts trading on markets involving their own interests, such as three congressional candidates betting on their own election markets.

You might think that as more people realize that trading with confidential information is illegal not only in the securities market but also in prediction markets, these issues will disappear. But I believe the problem is deeper than that.

The premise of prediction markets is that they are informationally efficient because they reward informed insiders.

In other words, prediction markets are "good" because they aggregate a large number of uninformed retail investors, and these retail investors create economic incentives for insiders to disclose private information. (This concept—that retail investors create incentives for informed insiders to participate—has been well-documented in financial literature, and a recent paper has extended it to prediction markets.) Then, prediction markets can reliably claim they have social utility because they indeed provide better and timelier signals than other platforms (experts, polls, etc.). Kalshi and Polymarket both understand this but are reluctant to admit it explicitly. However, they do hint at it in their marketing!

Kalshi's CEO Tarek Mansour stated on the Sourcery podcast that "there is no insider trading in commodity markets. In fact, it is all insider trading," which is… an extremely creative interpretation of the law. He added:

I believe there are some parts of non-public information that traders cannot trade on, but I think we are restricting it a bit too much right now.

Kalshi has used slogans like "trade anything" and "everyone is an expert in something," both of which imply that ordinary people can monetize privileged information on the platform if they happen to possess it.

Polymarket's CEO Shayne Coplan had this dialogue with CBS last year:

Anderson Cooper: But prediction markets indeed rely on certain people having insider information.

Shayne Coplan: Uh-huh. Yes. I think it's a good thing for people to have an advantage in the market. Obviously, you need to manage it, you need to be very clear and strict about boundaries, like in ethical aspects, we have spent a lot of time on that. But this is somewhat unavoidable, and there are many benefits to be gained from it. You know, people will adapt.

Shayne also said that prediction markets are "the most accurate thing humanity currently has, until someone creates some sort of super crystal ball." Some of that accuracy comes from insiders.

Robinhood's CEO Vlad Tenev (working with Kalshi) said:

Prediction markets actually allow you to get news faster, in some cases even before it happens. I think it does have tremendous economic value.

Economist Robin Hanson, seen by many as the father of prediction markets, directly embraced this viewpoint and wrote a lengthy defense of insider trading in prediction markets. In 2024, he said:

If the purpose of the (predictions) market is to obtain accurate price information, then you certainly want to allow insiders to trade, even if it may deter others from betting because they feel it’s unfair, because that makes prices more accurate. That should be the priority.

I must point out that both Kalshi and Polymarket have anti-insider trading policies. Kalshi is regulated by the CFTC, which has always explicitly prohibited trading based on Material Non-Public Information (MNPI) and conducts market monitoring. When I wrote a blog in February, I noted that Polymarket had not explicitly sanctioned insider trading, but in March, they updated their rulebook to include detailed prohibitions against the following types of trading:

- Trading based on stolen confidential information (if you're a soldier, the operational plans do not belong to you but to the government)

- Trading based on information illegally passed to you by insiders

- Trading on any contract where you can influence the outcome

The focus of this section is not to blame Kalshi or Polymarket or their leadership for implying that traders have informational advantages. I think their policies (after the March 2026 update) are clear enough. Instead, I want to point out the fundamental contradiction troubling these markets:

Prediction markets rely on informed traders to produce accurate prices, but they also depend on uninformed traders to create economic incentives to attract informed trading flow. This creates a tension:

- If insider trading is tolerated too much, uninformed traders may exit due to feeling it’s unfair

- If insider trading is restricted too strictly, markets may exclude their most valuable source of information

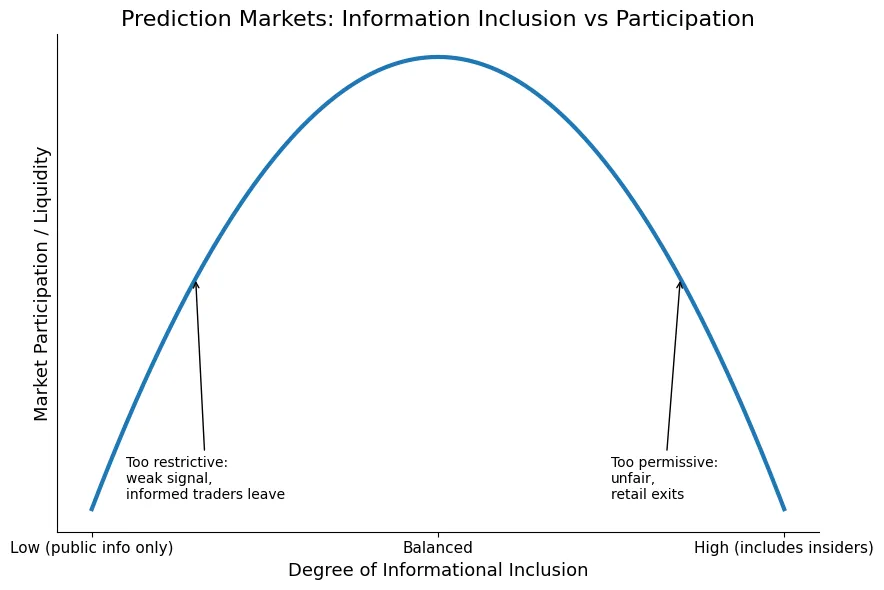

Thus, there is a trade-off between informational efficiency and perceived fairness. This is a visual representation of the same idea:

Chart: Trade-off curve between informational efficiency and perceived fairness

So we ultimately face several different failure modes:

Too many sharks, and they eat all the fish

If insider trading standards are too lax, the market becomes highly informationally efficient, but retail investors will clearly feel that the market is "manipulated," as they are always betting against insiders. Consequently, retail investors leave, and market liquidity decreases. This is the failure mode I previously discussed. This is where we currently stand, but I believe we will rebound in another direction.

No sharks, no advantage

This is at the other end of the spectrum. Insider trading is strictly regulated on the platform, with real-time market monitoring and strong regulatory reporting, thus driving informed trading flow away. The social value information produced by these markets is consequently reduced, merely becoming sentiment aggregators rather than generating "news before it happens." Consequently, the platform cannot effectively market itself.

The existential question is whether there is a golden midpoint: maximizing liquidity, where retail investors feel the market is "fair enough," while informed trading flow can still be rewarded for their information gathering. The chart suggests it might exist, but reality is messier.

My prediction from February still holds. As I said at that time:

Serious risks still exist: insider trading scandals will make retail traders feel the market is manipulated, leading them to abandon the platform. I predict there will be a series of insider trading events this year, convincing platforms to significantly strengthen market surveillance, and causing Polymarket in particular to move away from anonymous models.

I anticipate Polymarket will completely remove the ability to trade without KYC (which is currently the case on non-U.S. platforms) and strengthen the marking of suspicious trades on the platform. There will be numerous criminal cases regarding stolen insider information, but the temptation will still exist. While the platforms won’t admit it, there is indeed an "socially optimal" amount of insider trading. But can they optimally calibrate it? Will regulators allow them to do so?

Notably, not all informed traders are insiders. You can make yourself informed by collecting public information and trading based on that. However, there is indeed a portion of informed traders who are insiders misusing information.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。