Written by: Alice French, Bloomberg

Translated by: Saoirse, Foresight News

In the tight-knit financial circles of Tokyo, few can spark as much controversy as Michael Lerch.

To some, he is the white knight—this mysterious American investor who rescues struggling Japanese companies from the brink of bankruptcy. But to others, he is the greedy hyena: a profit-driven hedge fund manager who capitalizes on vulnerable businesses in crisis.

In the entire Japanese capital market, Lerch is synonymous with death spiral financing. This is a lucrative yet controversial financing model. His boutique investment fund Evo is the largest buyer of float warrants in Japan. These niche financing instruments are aimed primarily at small listed companies with tight cash flows. The contracts can quickly inject cash into businesses to maintain operations but can also lead to massive equity dilution, which is why this model has a pejorative nickname.

(Note: Float warrants, commonly known as death spiral financing tools, have exercise prices that dynamically adjust downward with stock prices, creating a vicious cycle of continuous equity dilution and stock price declines. The rampant misuse in the Japanese market stems from a lack of financing channels for local small-cap low-quality firms, new listing market value regulations forcing survival, loose regulatory constraints, and dominant institutions monopolizing financing supply, forcing companies to accept high-risk contracts to maintain listing qualifications.)

After graduating from Princeton University, Lerch came to Japan in the 1990s. For many years thereafter, he remained largely hidden from public view, building his financial empire through arbitrage trading. However, everything changed last year: the originally struggling hotel operating company Metaplanet suddenly gained fame after investing over $2 billion in Bitcoin, nearly all of which came from warrant financing provided by Evo.

This frenzied accumulation of cryptocurrency drove up Metaplanet's stock price, attracting retail investors, large institutional giants, and even the Trump family to participate, vividly showcasing the impressive profitability of Lerch's business model.

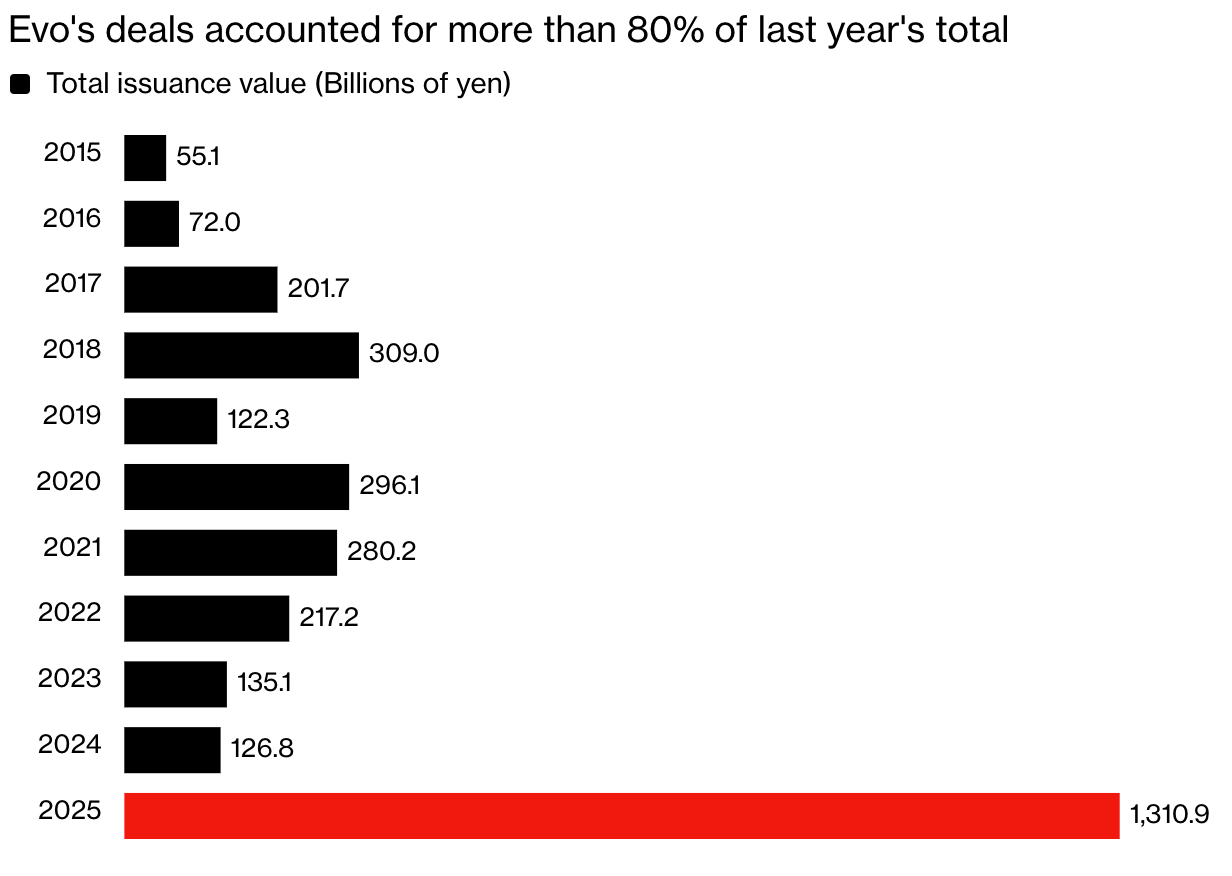

According to data from Japan's I-N Information Systems, a series of transactions between Evo and Metaplanet made 2025 the highest year for float warrant issuance in Japanese history. Last year, Lerch's fund reached a total of over 1 trillion yen (equivalent to $6.3 billion) in such financial transactions in Japan, accounting for more than 80% of the total scale across the market.

Japan's float warrant issuance reaches historical new high

Evo's transactions accounted for over 80% of last year's market total

Note: The statistical value includes initial issue price and maximum fundraising amount

Data Source: I-N Information Systems, Bloomberg

This surge continued into 2026. According to disclosures on the fund's website, Evo has signed equity financing agreements with at least 10 Japanese companies this year.

The skyrocketing demand for Lerch's financing services has also brought to light the issue of float warrant abuse in Japan. Coinciding with the Japanese government's upgrade of tax-exempt investment plans, a record number of retail investors flooded into the stock market, increasing potential risks. Such warrants can result in new shares being massively issued cheap to third parties, continuously diluting the holdings of small and medium shareholders.

Sadakazu Osaki, chief researcher at Nomura Research Institute and a senior expert in the Japanese stock capital market, stated: "These warrants are the last resort for poorly performing companies to finance. This spiral trading can cause equity dilution and suppress stock prices; once ordinary retail investors get sucked into it, they will face substantial risks."

Evo's remarkable performance last year also brought the long-hidden Lerch into the public eye. Throughout his career, he has acted discreetly, only giving one interview to Bloomberg in 2015. Last December, he made headlines again when a London court ruled that his company Evolution Capital Management in Nevada had to pay over $5 million in disputed bonuses to a disgruntled former trader.

This report is based on interviews with over 20 of Lerch's former employees, client partners, and industry insiders familiar with his business (most requested anonymity to protect their privacy), as well as data from Japanese listed company financial reports, court filings from London, and other judicial materials. All the information together reveals the truth: with highly advantageous cooperation terms and a firm, decisive style, this previously obscure fund has jumped to become a sought-after financing institution for Tokyo companies.

Lerch, who now resides year-round in a mansion by Lake Tahoe in Nevada, and his Evolution Financial Group both declined to comment on this report. The attorney representing Evolution Capital in the London case also did not respond to interview requests.

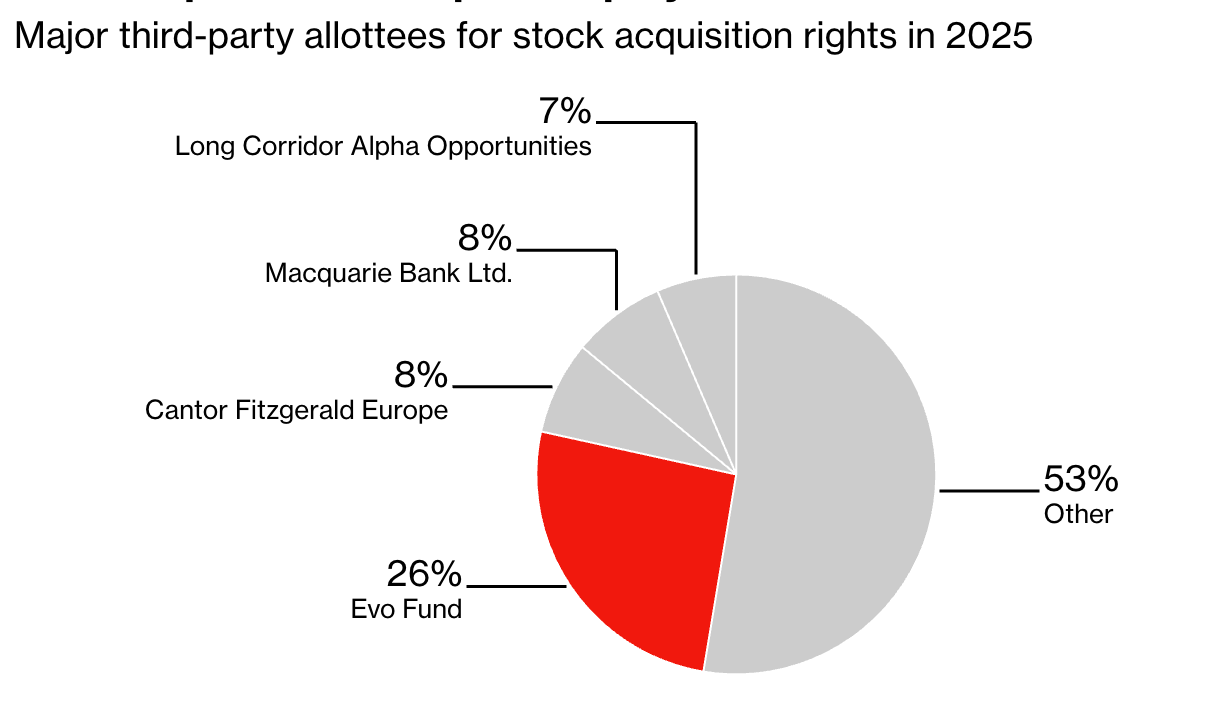

Evo is Japan's most popular warrant financing partner

Primary third-party recipients of stock warrants in 2025

Note: Based on issuance number statistics; due to rounding, the total percentage may not equal 100

Source: I-N Information Systems

In 1994, Lerch began his career in Japan. In the latter half of that year, he joined Barings Bank working on options trading, and just months later, the fraudulent operations of "rogue trader" Nick Leeson directly led to the bank's collapse.

From 1996 onwards, Lerch worked at Merrill Lynch, Crédit Agricole, and Lehman Brothers, sharpening his trading skills, and founded Evolution Financial Group in Tokyo in 2002. Evo is the first fund under the group, funded by himself and friends and family.

Andrew Jackson, who came to Japan in 1997, served as a trader at Jefferies' Tokyo branch in the mid-21st century and is currently the director of Japan stock strategy at Ortus Advisors, recalled: "At that time, there were investment opportunities everywhere in Japan, and Evo made a fortune. The market was loosely regulated, and all connections in the industry were built through bar meetings; the Japanese capital market at that time was like a wild jungle."

Jackson stated that he had numerous business dealings with Evolution Group back then. This institution thrived on the massive buy-sell spreads in the Japanese stock market and gained a reputation within the brokerage circles.

Now around 55, Lerch has expanded the Evolution Group into a cross-regional family office with businesses covering Los Angeles, Hong Kong, and a location on Hawaii's North Shore. According to court documents in London, the entire group has approximately 55 employees worldwide.

Those familiar with him say that his outstanding networking ability is key to his business expansion. To outsiders, Lerch is intelligent and shrewd, with a slightly eccentric personality: in the conservative Japanese business world, he favors brightly colored suits and thick-framed glasses, making him quite noticeable. In a YouTube video from 2023, he walks through the office wearing a bright yellow sweater, paired with matching glasses and a heavy pendant necklace, as part of a promotional video for the Japan-U.S. Young Leaders Exchange Program that the group participated in.

This is a screenshot of Michael Lerch from a YouTube video in 2023

During his university years, Lerch was an American football player, and his prestigious school background helped elevate his status in Tokyo. In the group's early days, he prioritized hiring Ivy League graduates and incorporated "tiger" elements into many business names as a tribute to the mascot of his alma mater, Princeton University.

Over the years, Lerch has leveraged his connections to secure several major deals:

- In 2010, Evolution Capital Management acquired the now-defunct professional basketball team Tokyo Apache;

- In the following year, Evolution Japan Securities acquired the electronic warrant business from Goldman Sachs Japan and subsequently divested this business to Japan's Caica Digital Company seven years later;

- In 2022, the group announced the sale of its self-developed electronic trading platform Tora (meaning "tiger" in Japanese) for $325 million to the London Stock Exchange Group.

However, Lerch's path to success has not been smooth. According to court documents submitted by the plaintiff in the London bonus dispute case, following the outbreak of the 2008 global financial crisis, his multi-strategy hedge fund launched in 2004 was forced to liquidate under the pressure of heavy investor redemptions. At its peak, this fund managed approximately $1 billion.

Evo's financing business focuses on float warrants while also offering convertible bonds and other financing tools, with the entire business rooted in Lerch's decades of arbitrage experience. The fund's Japanese website claims its advantage lies in tailoring to companies' personalized needs and making flexible and efficient investment decisions.

Since the early 21st century, following Japan's recovery from the collapse of the asset bubble, float warrants have become routine tools in the Japanese equity capital market. These warrants grant holders the right to purchase company stocks in the future, with exercise prices changing over time as agreed by both parties, usually based on the previous trading day's closing stock price.

They are quite similar to the direct issuance model of stocks in the U.S. market, serving as a fast and low-cost financing channel for those unable to secure bank or institutional credit.

When the exercise price is below the market price of the stock, the warrant holder will exercise the warrant for shares and then sell the stock to profit from the spread.

Osaki of Nomura Research Institute stated: "Some believe that this model has significant risks, but Evo's logic is very simple: when all institutions are unwilling to lend to a business, it is the only lifeline."

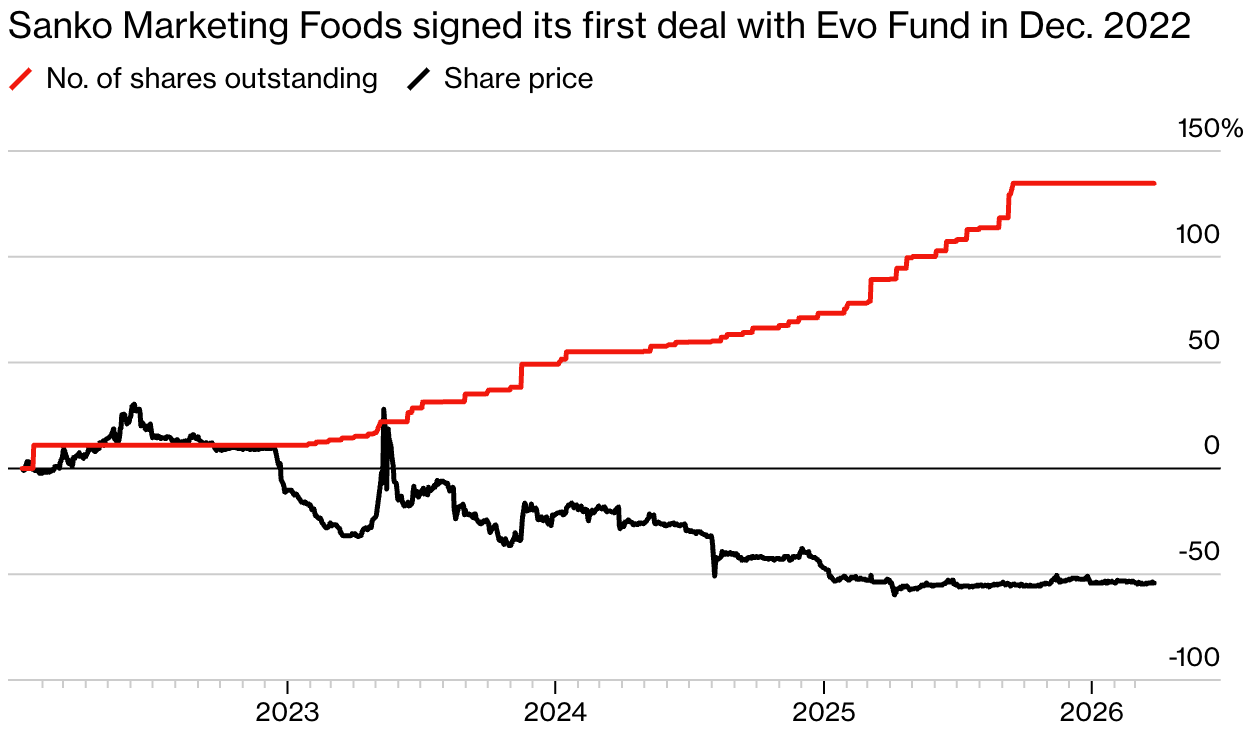

Yoshihiro Nagasawa, president of the seafood restaurant group Sanko Foods, feels this keenly: "Without Evo, we might have already shut down operations."

A seafood restaurant in Tokyo operated by Sanko Foods. Source: Sanko Foods

During the pandemic, Sanko Foods closed many stores and fell into a financial crisis, nearly facing delisting in early 2020. Around 2022, personnel from Evo proactively visited Sanko Foods' stall at Numazu Fish Market, located about 100 kilometers south of Tokyo, to promote their financing services. Shortly after, Yoshihiro Nagasawa met with Lerch and reached a financing cooperation agreement with Evo.

In an interview at a Tokyo izakaya, Yoshihiro Nagasawa candidly admitted: "It's undeniable that these warrants did suppress our stock price, also causing short-term losses for existing shareholders. But this funding saved the company, and it was all worth it. I am very grateful to Evo."

Evo's financing actions suppressed Sanko Foods' stock price

Sanko Foods signed its first transaction with Evo Fund in December 2022

Note: The data has been standardized based on percentage changes as of January 4, 2022

Source: Bloomberg; Sanko Foods disclosed

In stark contrast is Shin'go Kameida, president of the investment firm Manwei Investment Co., Ltd. He stated that after the company collaborated with Evo in 2023, its corporate reputation is still in recovery.

"That financing severely damaged the company's image," Shin'go Kameida admitted, stating that the company was in financial difficulty at the time and did not actively seek Evo financing but had no other options and signed a fixed exercise price warrant agreement without understanding the terms' risks.

Before partnering with Evo, the company's stock price was already on a downward track. Evo frequently exercised warrants at prices below market rates, further suppressing stock prices and provoking strong dissatisfaction among existing shareholders. "Evo's contract design ensured that they would make a profit from the start."

Evo's website claims that the fund can provide clients with flexible solutions, offering comprehensive support throughout the financing process while continuously engaging in proactive communication and collaboration with Japanese companies.

Shin'go Kameida, CEO of investment firm Manwei Investment Co., Ltd.

Simon Gerovich, president of Metaplanet, stated that Evo's highly competitive cooperation terms make it Japan's top-notch warrant financing partner. After many of its hotels closed due to the pandemic, Metaplanet entered into a float warrant agreement with Evo at the beginning of 2025 to raise funds for large-scale Bitcoin purchases.

"In terms of cooperation conditions, no institution can match Evo," Gerovich noted, explaining that other potential investors usually take 8%–10% of the exercise price as a risk premium, whereas Evo promises not to charge any discount fees when exercising.

Simultaneously, Evo's high exercise efficiency allows Metaplanet to rapidly raise funds. Evo also signed a borrowing agreement with Gerovich's investment company (the major shareholder of Metaplanet) to complete position hedging before each transaction, further accelerating the warrant exercise pace.

Last year, Gerovich publicly thanked Lerch for his support of Metaplanet on social media.

Industry insiders who have worked at Evo revealed that the fund's ability to offer favorable conditions relies on its mature warrant arbitrage capabilities. The team's traders have high risk control tolerance, while Lerch often uncovers and recruits talents at various social events in Tokyo.

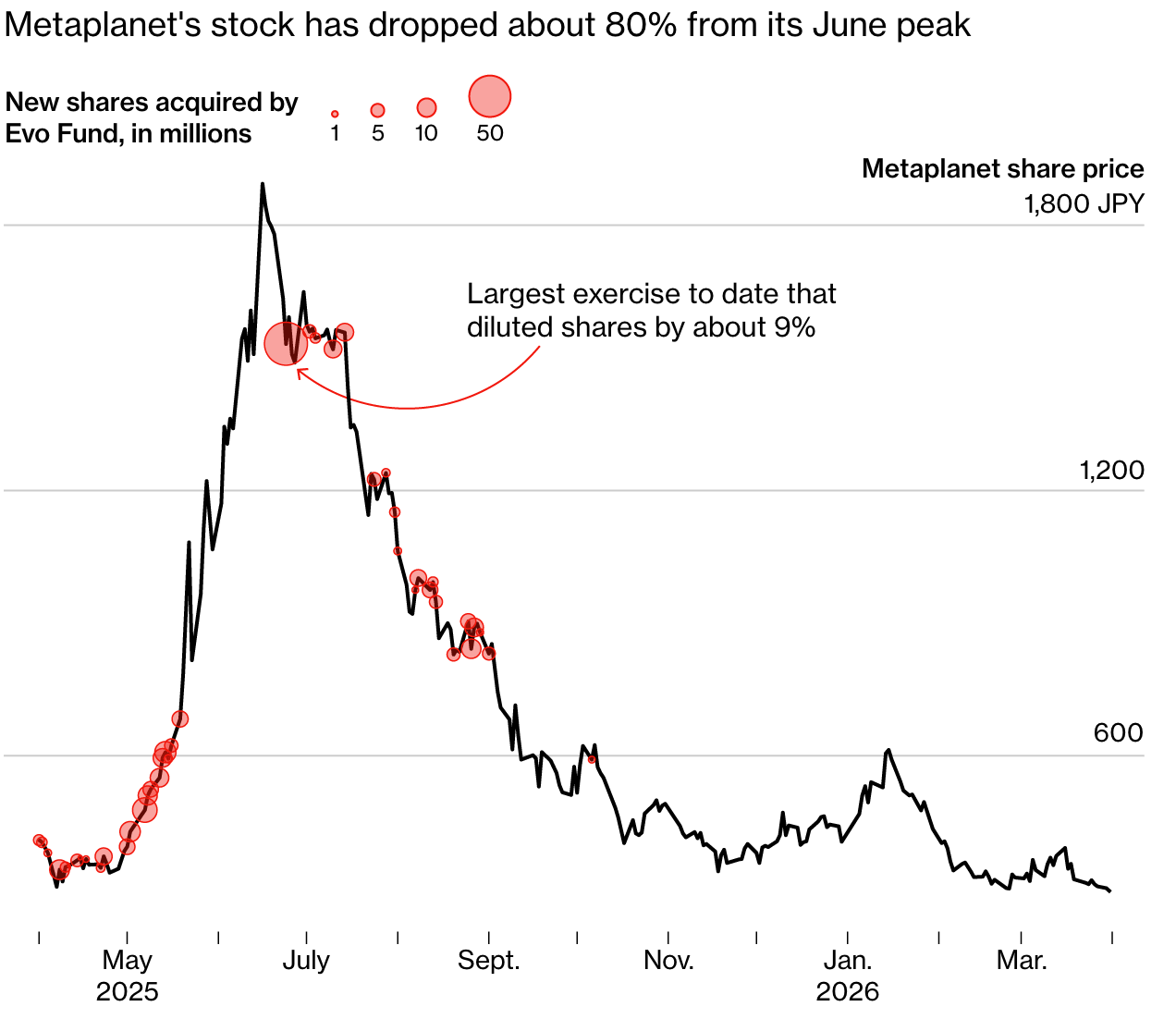

Evo's large scale exercise transactions with Metaplanet vividly illustrate the profit potential in this model. According to Metaplanet's regulatory announcements and Bloomberg's calculated data: On June 24, 2025, Evo acquired 54 million shares of Metaplanet at nearly 10% below the closing price. Within just a week, the fund sold 16% of those shares, earning 2.2 billion yen.

Gerovich stated: "Evo does make substantial profits, but this is a win-win situation." Metaplanet raised over 290 billion yen through warrants in 2025 and currently holds more than 40,000 Bitcoins.

As Metaplanet continues to raise funds and accumulate Bitcoins, Evo's exercise transactions continually dilute the equity of existing shareholders, many of whom hold shares through Japan's tax-exempt financial accounts. Just during the exercise on June 24, the total equity of Metaplanet expanded by approximately 9%.

Gerovich explained: "Under this business model, all shareholders' equity will be diluted, but no one minds, because this dilution is benign—our Bitcoin assets are continually appreciating."

After rising more than 2000% in the early stages, Metaplanet's stock price has plummeted about 80% since its peak in mid-June. Starting in October 2025, Metaplanet sought other financing channels, and Evo no longer exercised warrants on it.

Even as Metaplanet's stock price plummets, Evo continues to exercise MS (mobile exercise price) warrants

Metaplanet's stock price has dropped about 80% from the peak in June

Source: Metaplanet submitted documents; Bloomberg

The Japan Exchange Group (operator of the Tokyo Stock Exchange) declined to comment specifically on Evo's business. Their official statement said that float warrants issued to third parties are regular equity financing tools for listed companies.

The exchanges also acknowledged that there are concerns that such tools could harm shareholder rights through equity dilution and stock price declines, and they have implemented regulatory constraints, such as setting monthly exercise limits. Listed companies can also mitigate the shock of equity dilution by setting minimum exercise prices and lock-up reduction clauses.

However, Lerch has always acted firmly and uncompromisingly, making many Japanese companies wary of collaborating with him.

Alexey Shitov, who served as a senior executive at Evolution Group in the 2010s and took over the Goldman Sachs warrant business, stated: "Evo is known in the industry for being aggressive. Since Evolution Group took over the business, clients' perceptions of us have noticeably changed."

Regulatory punishment records show that in early 2016, Evo Investment Advisors, a Cayman subsidiary under the Evolution Group, was fined 9.2 million yen by the Japanese Financial Supervisory Authority for manipulating the stock price of a Tokyo-listed company. The Japanese Financial Supervisory Authority's Securities Trading Monitoring Commission did not provide additional comments on this matter.

In 2024, Evolution Japan Securities filed a lawsuit against robotics manufacturer Kuramoto Co. in Tokyo court, seeking 71 million yen in damages for breach of warrant contracts by issuing warrants to other third parties.

Kuramoto's president, Komine Mamoru, stated: "Evo actively approached us for cooperation, but we ultimately declined their warrant proposal. Even after the contract was terminated, they still filed a lawsuit." The case is still under review, and Kuramoto has already recognized this litigation as an anticipated loss in its February financial report.

Several partners and former employees who requested to remain anonymous revealed that Lerch can easily become forceful and irritable under pressure, having shown instances of unexpectedly firing traders and losing control of emotions during business communications.

Last year's labor dispute in London also exposed his stubborn and uncompromising style. The court ruled that Evolution Capital Management had unjustly withheld bonuses from former employee Robert Gagliardi, who had generated most of the company's revenue during his tenure. The group had previously argued that the employee was involved in a U.S. market investigation that damaged the company's reputation. Text messages disclosed in the case files showed Lerch even insulted this employee.

Setting aside various controversies, Evo's rise reflects the common predicaments faced by Japan's micro-cap listed companies: over 60% of listed companies in Japan are small and micro-cap stocks. As the Tokyo Stock Exchange raises market cap listing requirements, many companies urgently need to raise funds; how to balance the demand for rapid fundraising with the rights of retail shareholders has become a thorny issue.

Associate Professor Yao Zhihua of Kitakyushu City University believes that float warrants are a lifeline for poorly performing companies; without them, it is challenging to attract investment. The market has mixed reviews of this tool, but the high-profile collaboration between Evo and Metaplanet will undoubtedly drive overall market demand for such financing contracts.

For Shin'go Kameida, president of Manwei Investment Co., Ltd., the risks of harming shareholder interests far outweigh the cooperative benefits, and he is unwilling to partner with Evo again. In March of this year, during the company's new round of warrant financing, he chose to partner with Hong Kong hedge fund Long Corridor Asset Management, stating that the new contract would prioritize the protection of existing shareholders' interests.

Shin'go Kameida revealed that Evo still sends financing invitations, but he consistently refuses. "In the eyes of different people, Lerch is both a savior and a scavenging vulture. Such financing deals are always a double-edged sword."

(This article was co-written by: Jonathan Browning, Bailey Lipschultz, Finbarr Flynn, Wu Jin)

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。