Author: Lucas Shin

Translation: Deep Tide TechFlow

Deep Tide Overview: The market views Circle as an interest rate-sensitive money market fund, yet the supply of USDC still grew by 72% when interest rates declined. More overlooked is the wave of AI agency commerce: McKinsey predicts that the scale of agency transactions will reach $3-5 trillion by 2030, while 99.6% of the $106 million transaction volume of the HTTP payment standard x402 is settled in USDC. This represents a structural opportunity for stablecoin demand, not merely a bet on interest rates.

Conclusion:

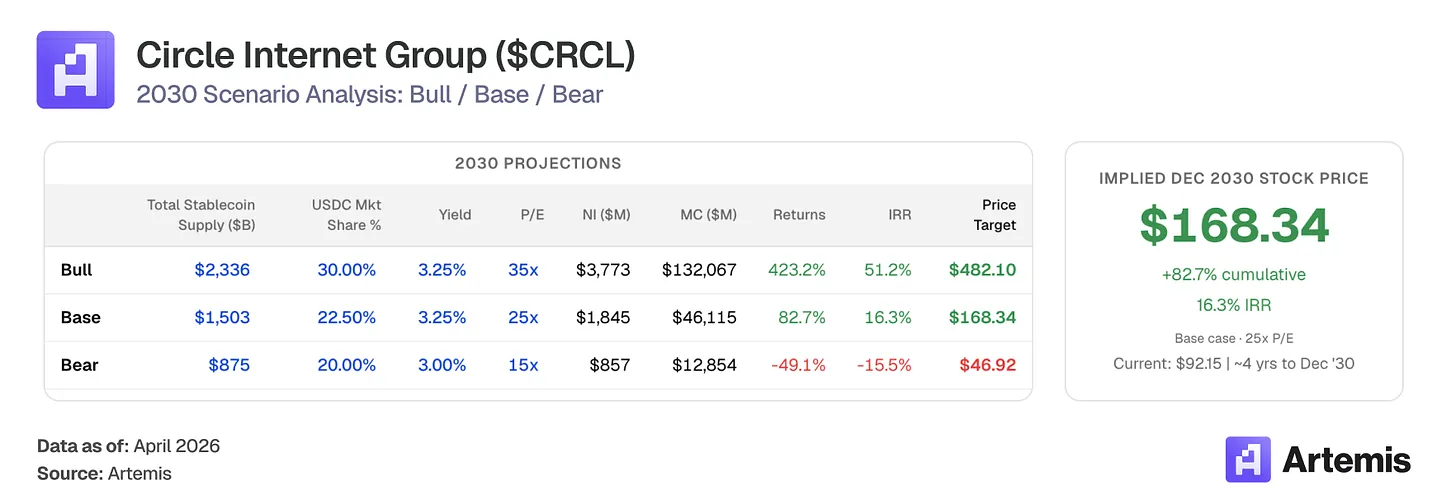

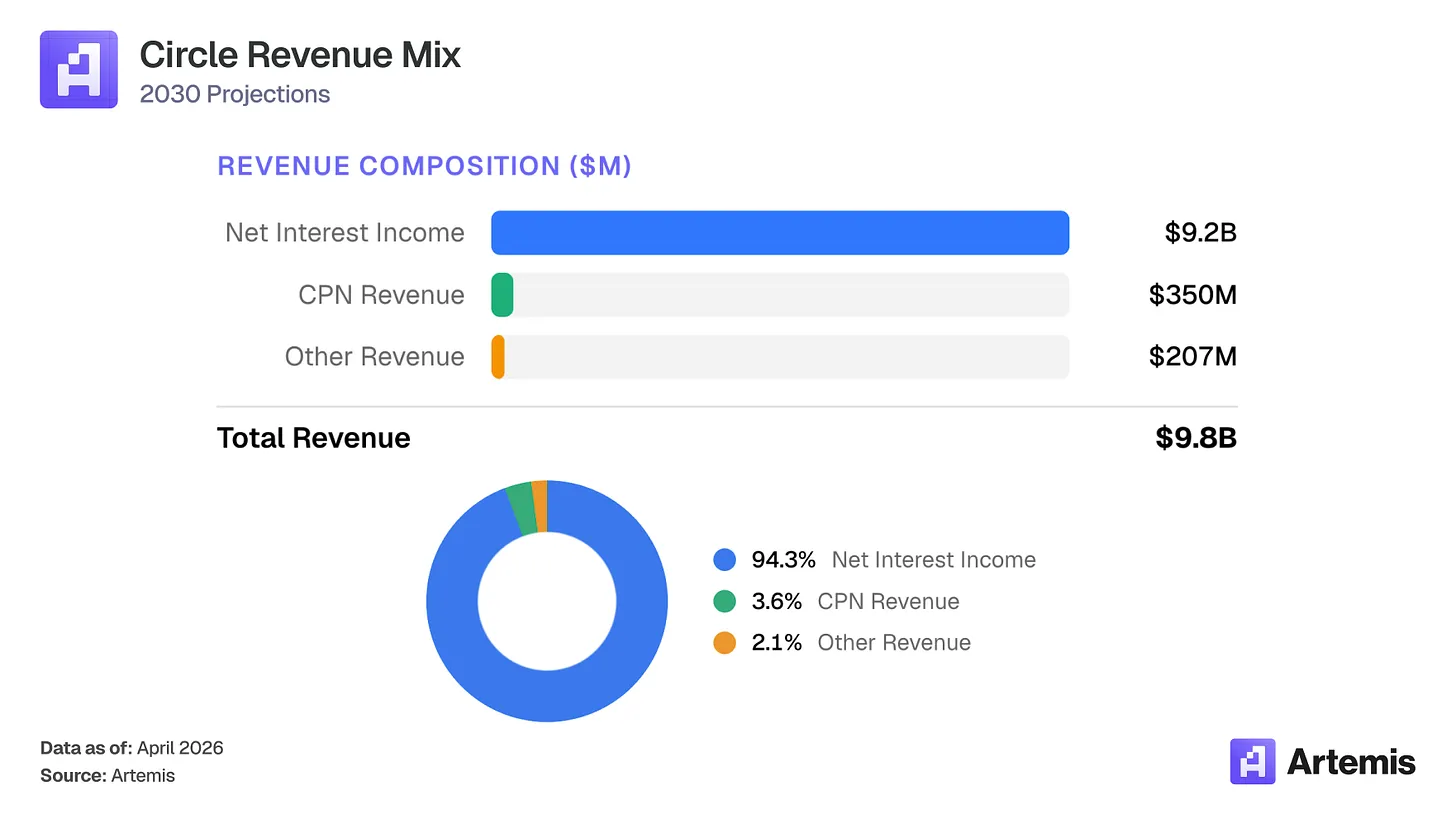

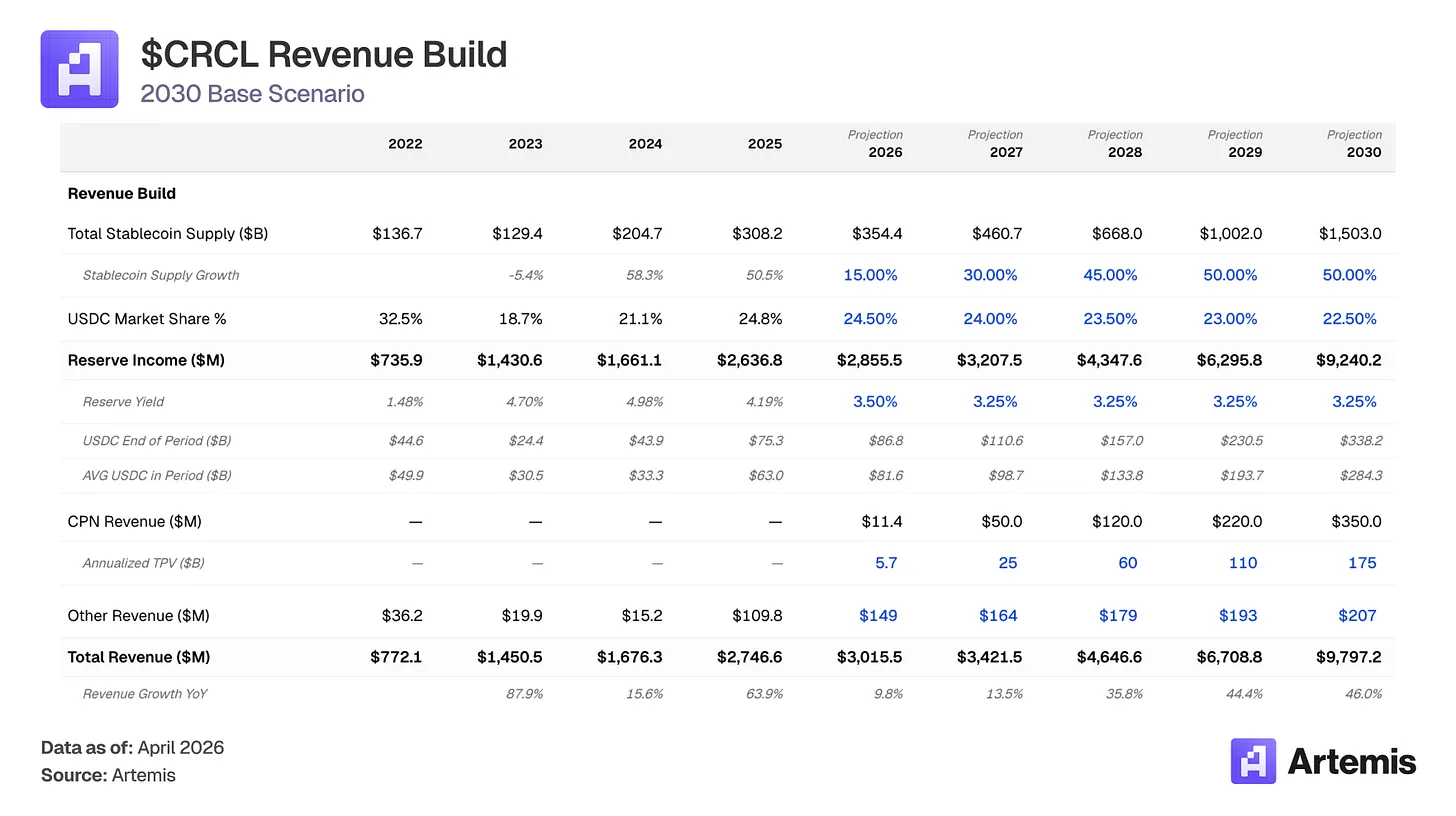

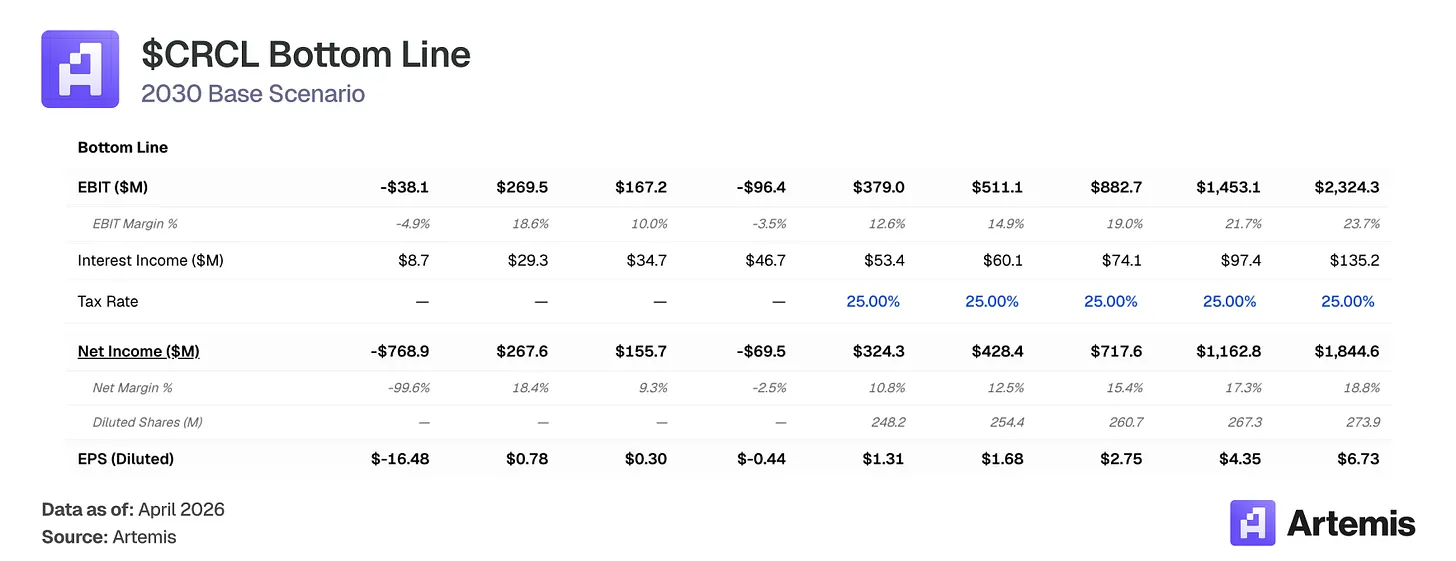

The market prices Circle as an interest rate-sensitive money market fund—betting on the Federal Reserve's fund rates sitting on the blockchain track. We believe this framework misprices the business. The supply of USDC is expected to increase by 72% to $75.3 billion by 2025, even if the Federal Reserve cuts rates by 75 basis points in the second half of the year, indicating that USDC demand is driven by genuine utility adoption rather than pure yield-seeking behavior. Our base case predicts that by 2030, the total market for stablecoins will reach about $1.5 trillion, with an average supply of USDC at $284 billion. Even with a projected compression in reserve yield, we expect Circle's reserve income to grow to $9.2 billion by 2030 (about 3.5 times the approximately $2.6 billion in 2025), as the growth in supply outweighs the compression in interest rates. Combined with the Circle Payment Network (CPN) expanding to $350 million in revenue, with distribution costs decreasing from 60% to 55%, our base case predicts total revenue of $9.8 billion and net income of about $1.8 billion by 2030.

Several tailwinds are supporting this trajectory: the GENIUS Act creates a favorable federal stablecoin framework for compliant issuers; Circle's payment network gains early traction with 55 financial institutions registered, processing an annualized transaction volume of $5.7 billion, providing transaction-based revenue streams that diversify interest rate sensitivity; the adoption of stablecoins expands in B2B payments, cross-border settlements, and DeFi. Our base case yields a predicted EPS of $6.73 by 2030, implying a target price of about $168 with a 25x terminal P/E ratio, representing an 83% upside relative to current levels.

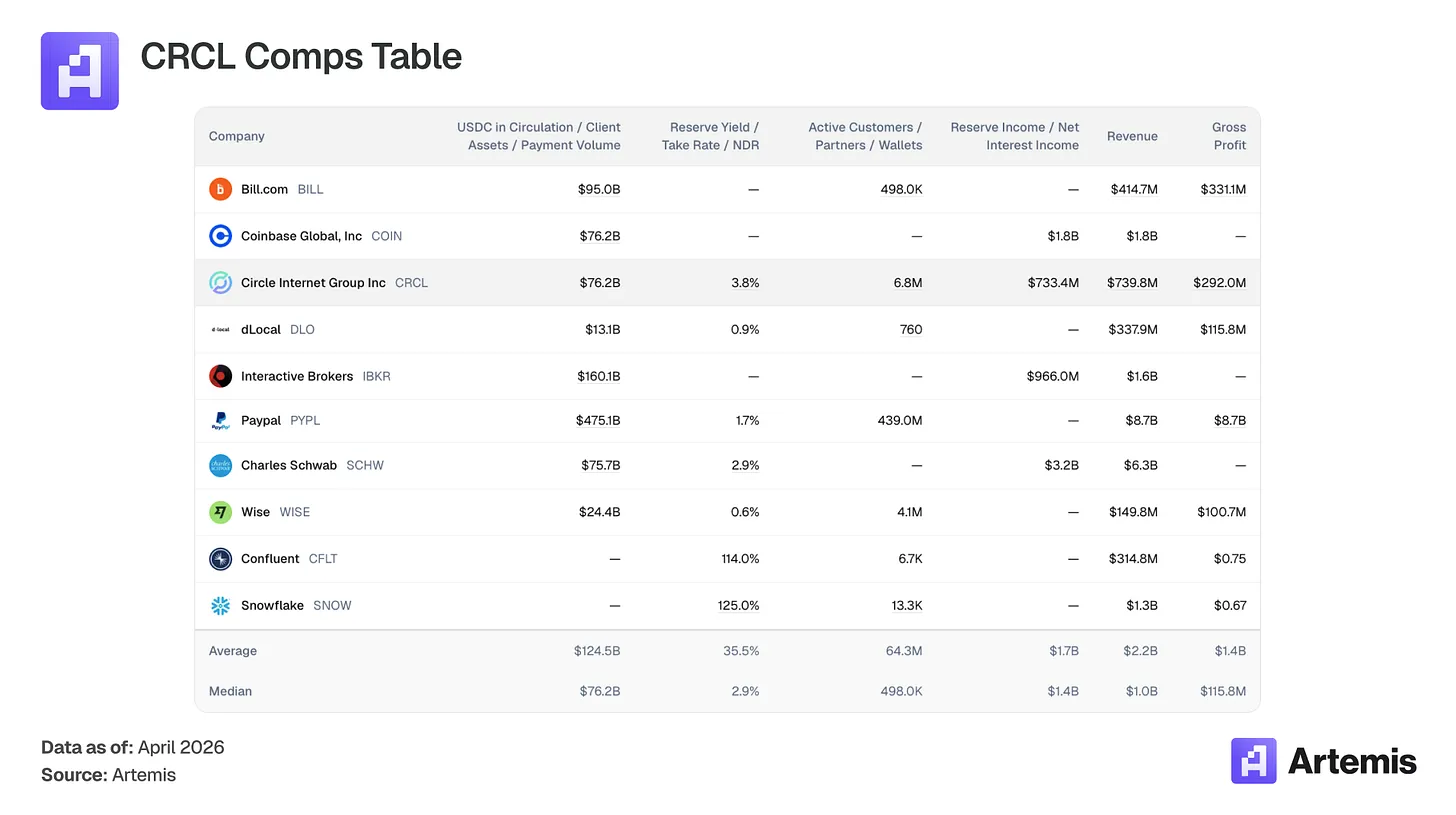

Comparable Company Table:

There are no direct publicly traded comparable companies to stablecoin issuers through reserve float monetization. Our comparable set includes companies that share key attributes with Circle's business: revenue models based on float (Charles Schwab, Interactive Brokers), digital payment infrastructure (PayPal, Wise, dLocal, Bill.com), crypto-native platforms (Coinbase), and high-growth infrastructure with usage-based economics (Snowflake, Confluent).

What does Circle do?

Circle is the issuer of USDC, a dollar-pegged stablecoin that is 1:1 tied to the US dollar. When users deposit dollars, USDC is minted; when they redeem, it is destroyed. The reserve (approximately 43% reverse repos, 43% Treasury bills, and 14% bank deposits, managed by Bank of New York Mellon and through BlackRock's USDXX fund) generates the yield that constitutes Circle's primary income.

Key cost structure details: Coinbase, as the primary distribution partner for USDC, earns 100% of the reserve income from USDC held on its platform, and 50% from USDC outside the platform. By 2025, Coinbase will generate $1.35 billion, comprising 51% of Circle's total reserve income. Including non-Coinbase distributions (12.7%), total distribution costs consume approximately 61% of reserve income, leaving a gross margin of 39%. We forecast distribution costs to decrease from 60% to 55% by 2030, as non-Coinbase distribution grows, with new financial institutions, banks, and custodial partners negotiating more favorable deals than what Circle currently has with Coinbase. This drives gross margins from 39% to 54%.

Apart from reserve income, Circle's most important growth lever is the Circle Payment Network (CPN), a cross-border B2B settlement network built on USDC. Launched in May 2025, CPN has registered 55 financial institutions, processing an annualized transaction volume of $5.7 billion, with a pipeline of 500 financial institutions. We expect CPN to expand to $175 billion in transaction processing volume by 2030, generating $350 million in transaction-based revenue at a rate of 0.2% (consistent with a blended cross-border fee rate of 20 bps). This revenue is insensitive to interest rates, allowing Circle to diversify away from pure reserve yield dependence. Additional revenue lines (referred to as "other income" in our model) include CCTP (47-50% of cross-chain bridge transaction volume) and Arc settlement infrastructure, which we estimate to yield a combined $207 million by 2030.

Argument #1: Supply Growth Outweighs Rate Compression

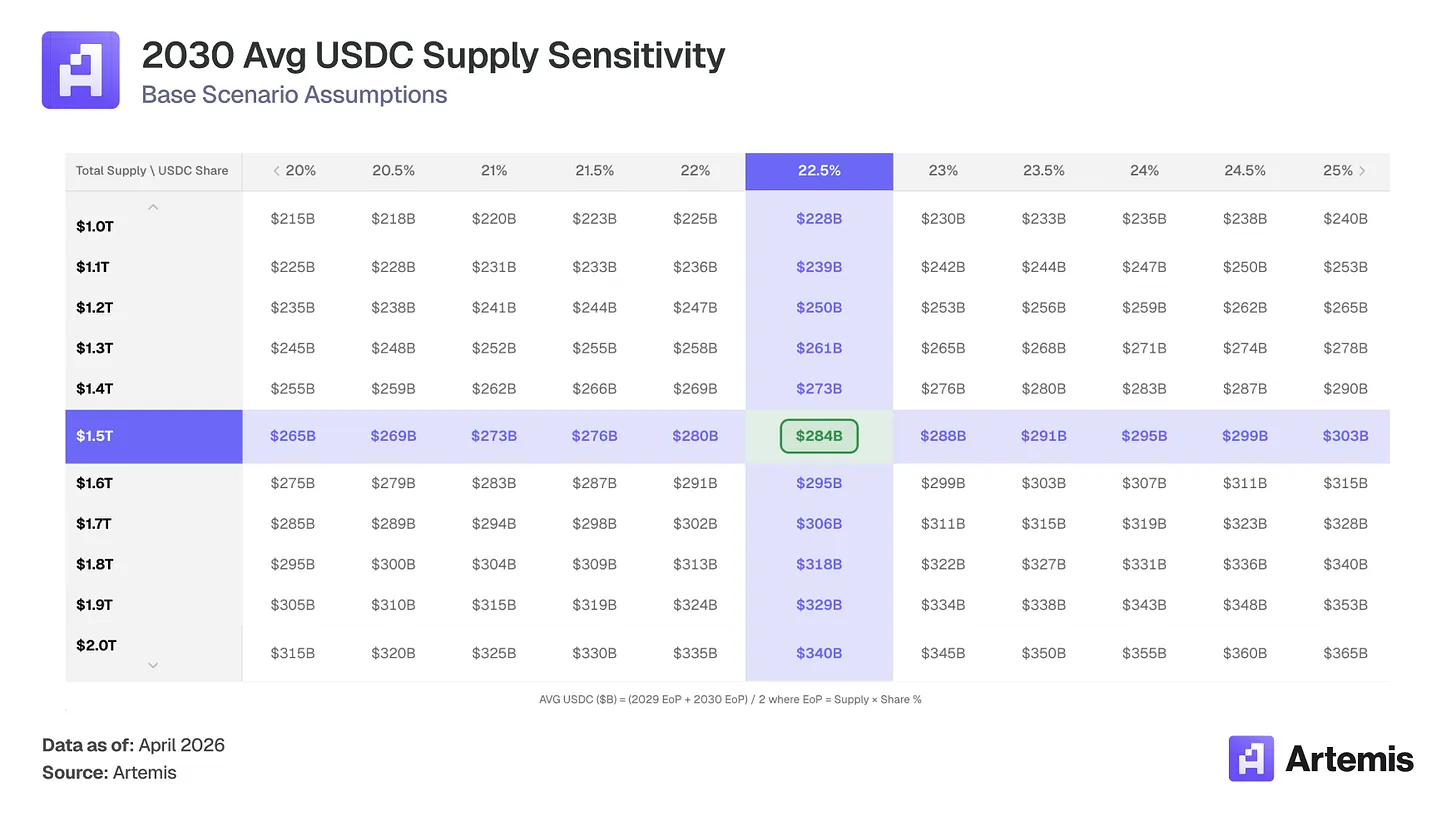

The total market for stablecoins is expected to grow from approximately $137 billion in 2022 to about $308 billion by 2025. Our model predicts around $1.5 trillion by 2030, reflecting a compound annual growth rate of approximately 37%. Today, the total value of stablecoins in circulation (approximately $316 billion) represents about 1.4% of the $22.7 trillion US M2 money supply. Our base case suggests about 6%, still a modest share of dollar-denominated liquidity.

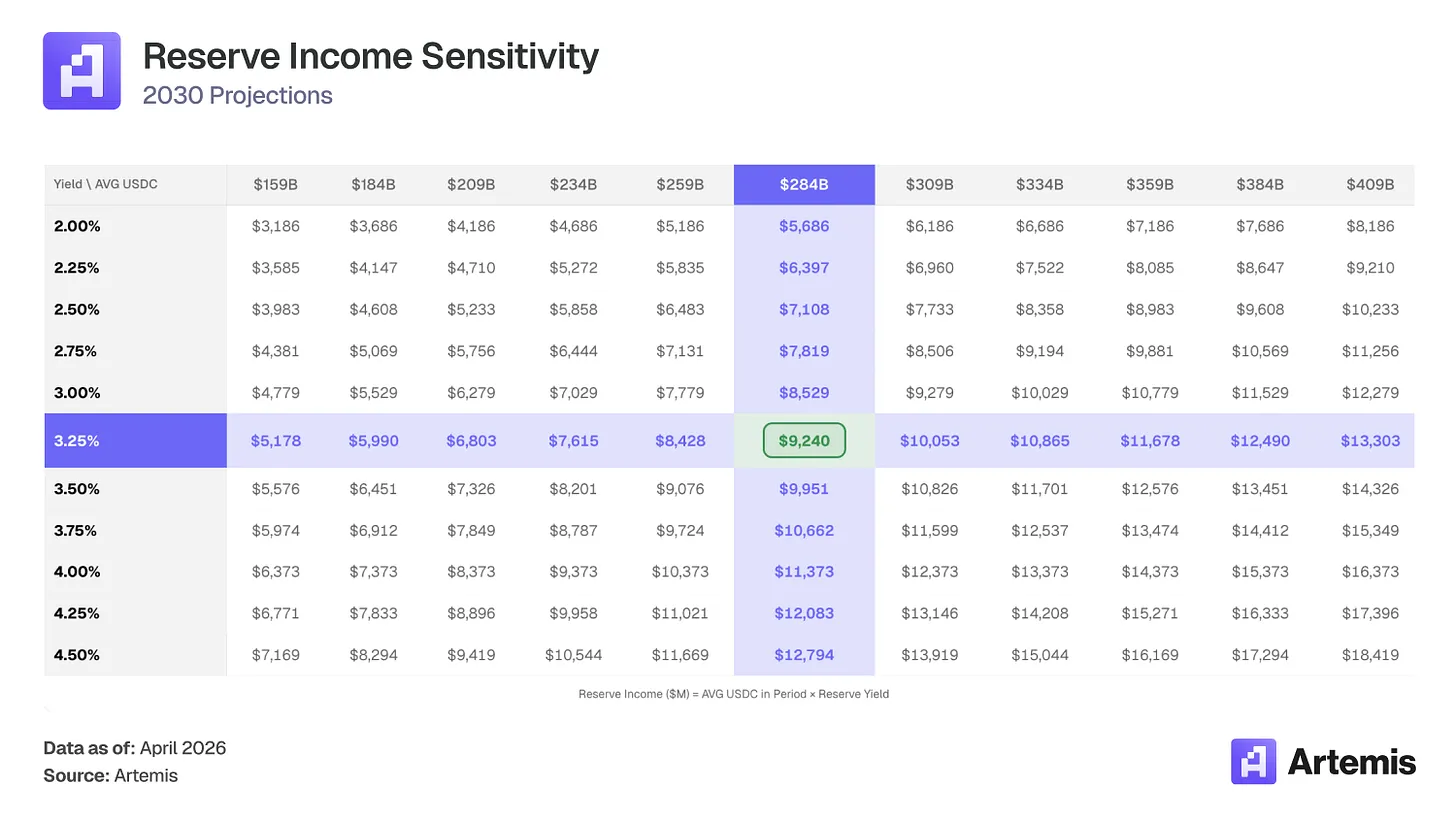

We project that USDC maintains a 22-25% market share (a moderate decline from 24.8% due to space being split with white-label and bank stablecoins), resulting in a supply of $338 billion of USDC by 2030 (about a 4.5 times growth from today). Simply put, even if Circle's effective reserve yield declines, the pure growth of USDC supply from $63 billion to an average of $284 billion is sufficient to compensate. As a result, reserve income grows 3.5 times, from $2.64 billion to $9.24 billion.

Argument #2: Agency Commerce Will Drive the Next Wave of Stablecoin Demand

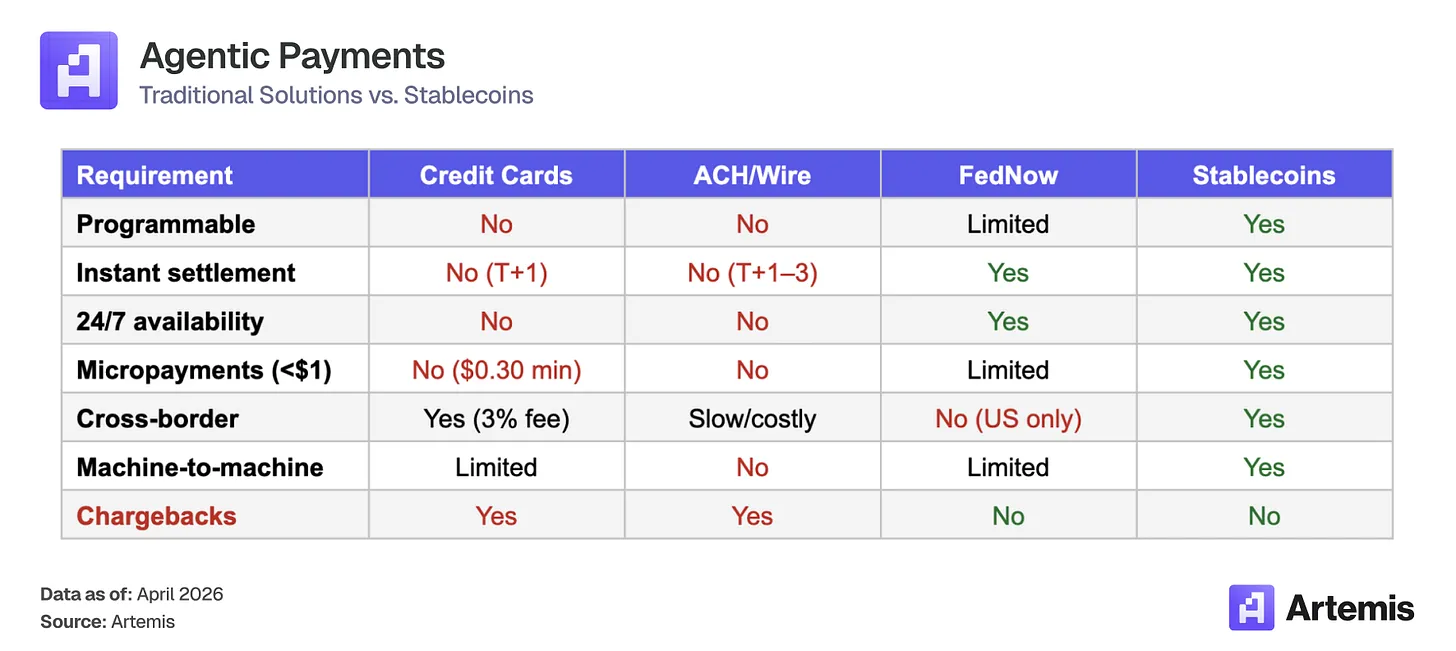

AI agents are on a trajectory towards autonomously executing transactions by 2030. McKinsey predicts that global agency commerce sales will reach $3-5 trillion by 2030; Gartner estimates that AI agents will mediate over $15 trillion of B2B procurement by 2028. These transactions structurally require stablecoin tracks:

Stablecoins are becoming the settlement layer for this emerging agency economy, with Circle's business model expanding accordingly. As agents hold USDC in wallets to fund autonomous transactions, Circle earns yield on every dollar sitting in those reserves. The larger the pool of USDC held by agents, the broader the revenue base, regardless of transaction frequency.

USDC is already the default stablecoin for agent payments. In the six months since the x402 payment standard (HTTP-native micropayments) gained traction, it has processed around 17.7 million transactions with a transaction volume of approximately $106 million. Of that, over 99.6% of the transaction volume is settled using USDC.

First-mover advantage creates a flywheel where new builders default to supporting USDC as it has the deepest integration, further entrenching the integration and making alternatives harder to break through. We do not model agent revenue in our base case, but agent demand is embedded as an upside optionality in our bull case scenario. If 1-2% of McKinsey's lower-end $3 trillion forecast is settled on the USDC track, it implies an incremental USDC float of $30-60 billion in agent wallets, from which Circle could earn passive yield.

Valuation and Scenarios

We value CRCL using a terminal P/E ratio based on the 2030 forecast EPS. Our base case generates $1.84 billion in net income on 273.9 million diluted shares, resulting in an EPS of $6.73. A 25x terminal P/E—above the comparable weighted average, reflecting Circle's structural growth trajectory, CPN-driven revenue diversification, and regulatory moat—implies a share price of about $168 by 2030, representing an 83% upside relative to current levels.

The 25x multiple sits between JPMorgan's (JPM) roughly 15x and Coinbase's approximately 38x, suited for a high-growth infrastructure business transitioning to recurring, interest rate-insensitive revenue.

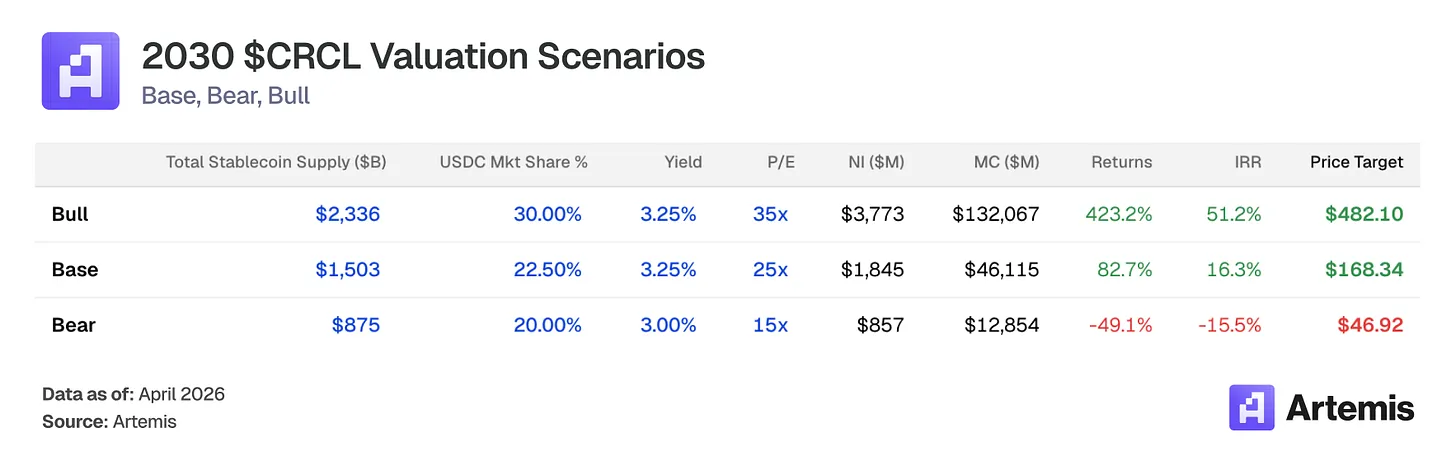

Base Case: Assumes supply growth and CPN expansion continue to execute, with the stablecoin market reaching $1.5 trillion and USDC maintaining a 22.5% share. Distribution costs moderately decrease to 55%, as new financial institution partners negotiate lower income shares. Exiting at a 25x terminal P/E ratio based on 2030 projected earnings implies a target price of $168.34—an 82.7% upside with a 16.3% internal rate of return.

Bull Case: Assumes accelerated stablecoin adoption driven by favorable regulation, CPN network effects, and widespread access to traditional finance. The total stablecoin market reaches $2.3 trillion, with USDC gaining a 30% share. Distribution costs compress to 50% as non-Coinbase origins expand. Exiting at a 35x terminal P/E based on 2030 projected earnings implies a target price of $482.10—over 423% upside with a 51.2% internal rate of return.

Bear Case: Assumes slowed stablecoin adoption, with white-label stablecoins eroding USDC's market share to 20%, and interest rate cuts compressing reserve yields to 2.75%. CPN's appeal wanes. Exiting at a 15x terminal P/E based on 2030 projected earnings implies a target price of $46.92—about 49% downside with a -15.5% internal rate of return.

We believe that the quality of the management team is above average in the crypto infrastructure space, with a particular edge in regulatory navigation (49 state MTLs, first MiCA compliant).

Jeremy Allaire co-founded Circle in 2013 and serves as Chairman and CEO. A serial entrepreneur (former CTO of Macromedia, founder/CEO of Brightcove, IPO in 2012), Allaire pivoted Circle from a consumer payments application to a stablecoin infrastructure, launching USDC in 2018 with Coinbase, completing a traditional IPO on the NYSE in June 2025 after a failed SPAC in 2022.

Heath Tarbert serves as President, promoted from Chief Legal Officer in January 2025. Tarbert is the former Chair and CEO of the CFTC (2019-2021), former Assistant Secretary of the Treasury, and former Chief Legal Officer of Citadel Securities.

Jeremy Fox-Geen has been CFO since January 2021. He previously served as CFO of iStar/Safehold (NYSE-listed REITs) and CFO of North America for McKinsey. He oversees Circle's IPO and manages the structure supporting over $70 billion in circulating USDC reserves.

Dante Disparte serves as Chief Strategy Officer and Global Head of Policy and Operations. Formerly the founding CEO and Vice Chair of the Diem Association (Meta's stablecoin project), he leads global regulatory strategy, public policy, market expansion, and international operations.

The primary management risk is founder concentration and high equity incentive post-IPO (over $500 million in 2025, including $424 million in IPO-related RSU acceleration), which is currently normalizing (equity incentives of $59 million and $48 million in the third and fourth quarters of 2025, trending towards a sub-$200 million annual run rate).

White-Label and Platform-Native Stablecoins

The most underestimated risk to USDC's market share is the potential for platforms, major applications, and financial institutions to launch their own branded stablecoins. For example, Hyperliquid has USDH, PayPal has PYUSD, Fidelity has FIDD, and JPMorgan has JPMD. Recently, Polymarket launched "Polymarket USD," currently wrapped in USDC but potentially a stepping stone towards independent settlement. If this strategy expands under the GENIUS Act framework, USDC could gradually lose its status as the default settlement track. Our base case forecasts USDC's market share to decline from 24.8% to 22.5% by 2030 to reflect this fragmentation.

Mitigating Factors: White-label stablecoins still require reserve infrastructure, compliance, and—most importantly—deep liquidity. Given USDC's integration across major exchanges, wallets, DeFi protocols, and bridging, new branded stablecoins would need to replicate that liquidity network to function as independent settlement tokens. Deep liquidity pools, tight spreads, and instant redeemability are not easily initiated, and fragmented stablecoins with weak liquidity create worse executions for users. The transition cost to launch fully independent reserves is high enough that most platforms might never complete the transition.

Federal Fund Rate Sensitivity

Reserve income is directly tied to interest rates. A forecast average USDC of $284 billion by 2030 means a loss of approximately $2.8 billion in total reserve income for every 100 basis point cut. If the Federal Reserve cuts rates to 2.0%, reserve income is projected to decline by 25-30% compared to our base case. Kalshi's prediction market currently prices a 63% probability of further rate cuts before 2027.

Mitigating Factors: Even at a 2.5% yield, an average USDC of $284 billion generates $7.1 billion in reserve income, still 2.7 times the $2.64 billion earned at a 4.19% yield in 2025. Supply growth outweighs all scenarios except the most extreme interest rate conditions.

Single Product Concentration and Coinbase Dependence

USDC reserve income accounts for over 96% of total revenue in 2025. Coinbase controls approximately 67% of US crypto exchange share, earning 51% of reserve income. As mentioned, if Coinbase launches its own stablecoin, aggressively renegotiates terms, or if regulatory headwinds slow USDC supply growth, the entire revenue base is at risk.

Mitigating Factor 1: Given that Coinbase earns $1.35 billion annually from its arrangement with Circle, with virtually zero balance sheet risk, their choice to launch a competitive stablecoin seems unlikely. If they do, it would require Coinbase to build regulatory infrastructure and liquidity that Circle has spent years developing.

Mitigating Factor 2: The market has raised similar criticisms of Visa for years (claiming it to be a single product business), but Visa's value-added services generated over $10.9 billion in 2025 (a 24% year-on-year growth), showing a reduction in reliance on interchange fees. We believe CPN is Circle's key diversification lever. By the end of 2030, we estimate CPN will generate $350 million in transaction-based revenue (about 4% of total revenue), which is both interest rate insensitive and independent of its relationship with Coinbase. Over time, institutions and B2B USDC origins bypassing Coinbase should also organically reduce blended distribution costs.

Tether Resilience and Competitive Landscape

USDT currently has a supply nearly 2.5 times that of USDC, and Tether is actively narrowing the regulatory gap with USDC. In January 2026, Tether introduced USAT, a stablecoin issued through Anchorage Digital Bank (OCC regulated) that complies with the GENIUS Act, providing Tether a pathway into the previously locked US institutional market. If Tether successfully runs a dual strategy (USDT for global liquidity, USAT for US compliance), USDC's regulatory moat will significantly narrow.

Mitigating Factors: The competitive landscape is nuanced. USDT dominates trading on centralized exchanges outside the US and remittances in emerging markets, while USDC leads in DeFi collateral (the default choice for Aave, Compound, Uniswap), US institutional adoption, cross-chain bridging (CCTP accounts for 47-50% of bridging transaction volume), and B2B payments (expected to reach $235 billion in 2025, up 733%, with USDC comprising about 65%). These actually serve different products for different total addressable markets. That said, our argument is built on the expansion of the total stablecoin market rather than market share growth at the expense of Tether. Both stablecoins will grow significantly.

Disclosure: This material is for informational purposes only and does not constitute investment advice, financial advice, trading advice, or any other form of recommendation. The views expressed are those of the authors and should not be construed as a recommendation to buy, sell, or hold any asset. The authors or affiliated entities may hold positions in the discussed assets. You should conduct your own research and consult appropriate financial professionals before making any investment decisions.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。