Author: Pink Brains

Translated by: Shenchao TechFlow

Shenchao Guide: Pendle, PancakeSwap, and Balancer have successively abandoned the ve token model within 12 months. The combined TVL of these three protocols once reached several billion dollars. This article presents the most systematic post-analysis on the market: where each protocol's specific breaking point is, what alternative mechanisms were adopted, and whether the underlying failure logic is the same. The conclusion is not that "ve tokens are dead," but a more precise judgment—what types of protocols can work, and which cannot.

The full text is as follows:

Three major DeFi protocols have abandoned the voting escrow model within 12 months. Pendle, PancakeSwap, and Balancer each have different breaking points but ultimately arrived at the same conclusion.

The economics of voting escrow tokens (ve tokens) were supposed to be the ultimate solution for DeFi token economics. Locking tokens, gaining governance rights, earning fees, and aligning incentives permanently—all without central governance. Curve proved that it could work, and dozens of protocols replicated this model between 2021 and 2024.

But that has changed.

In the 12 months of 2025, three protocols with a combined TVL of several billion dollars determined that this mechanism was more harmful than beneficial. Not because the theory was wrong, but because the execution failed: low participation rates, governance being captured, emissions flowing into unprofitable liquidity pools, and tokens plummeting while usage increased.

Pendle: vePENDLE → sPENDLE

Where the problem occurred

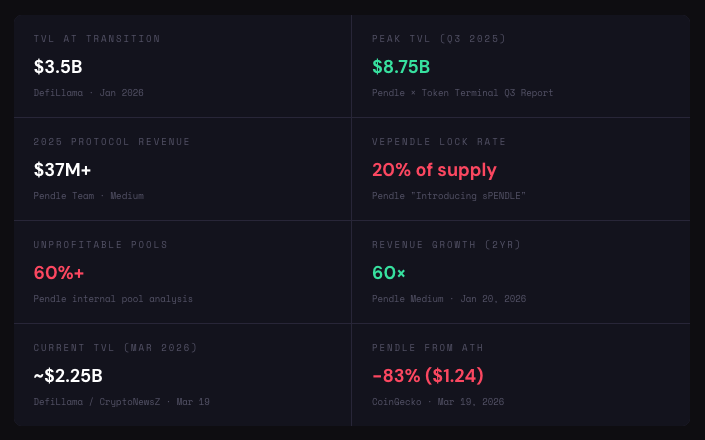

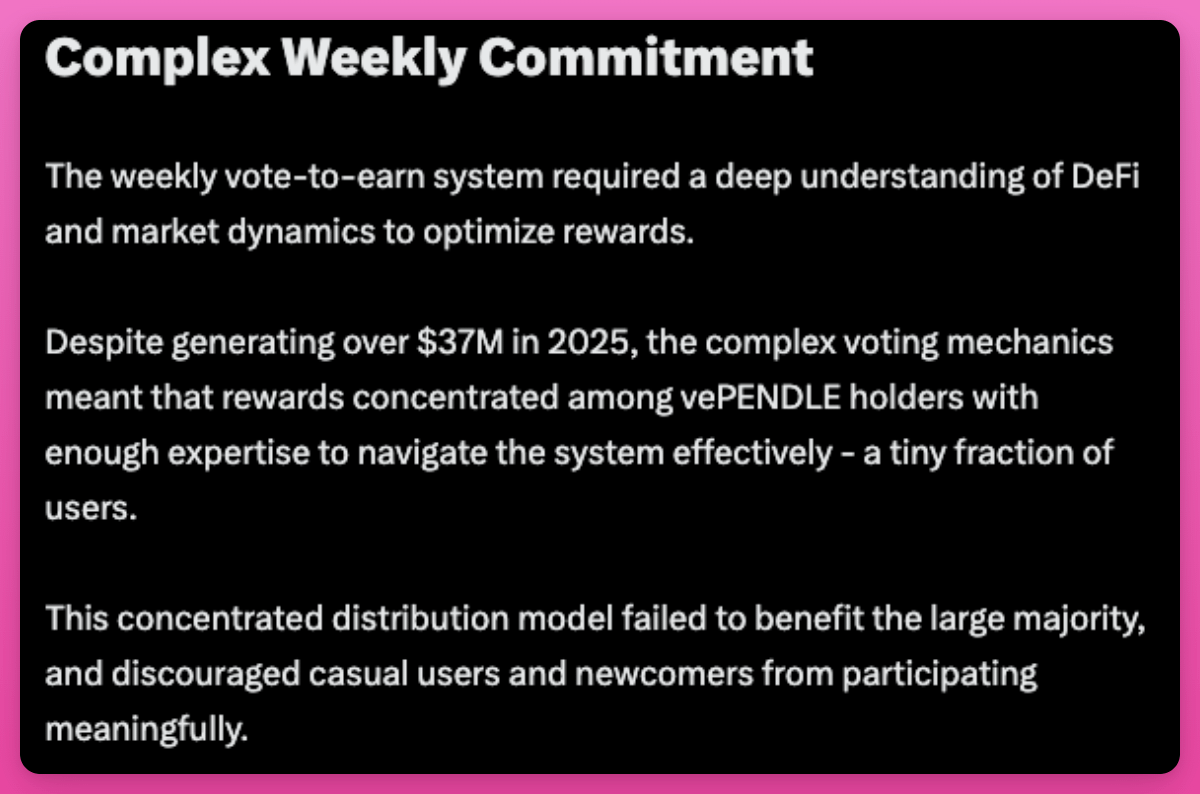

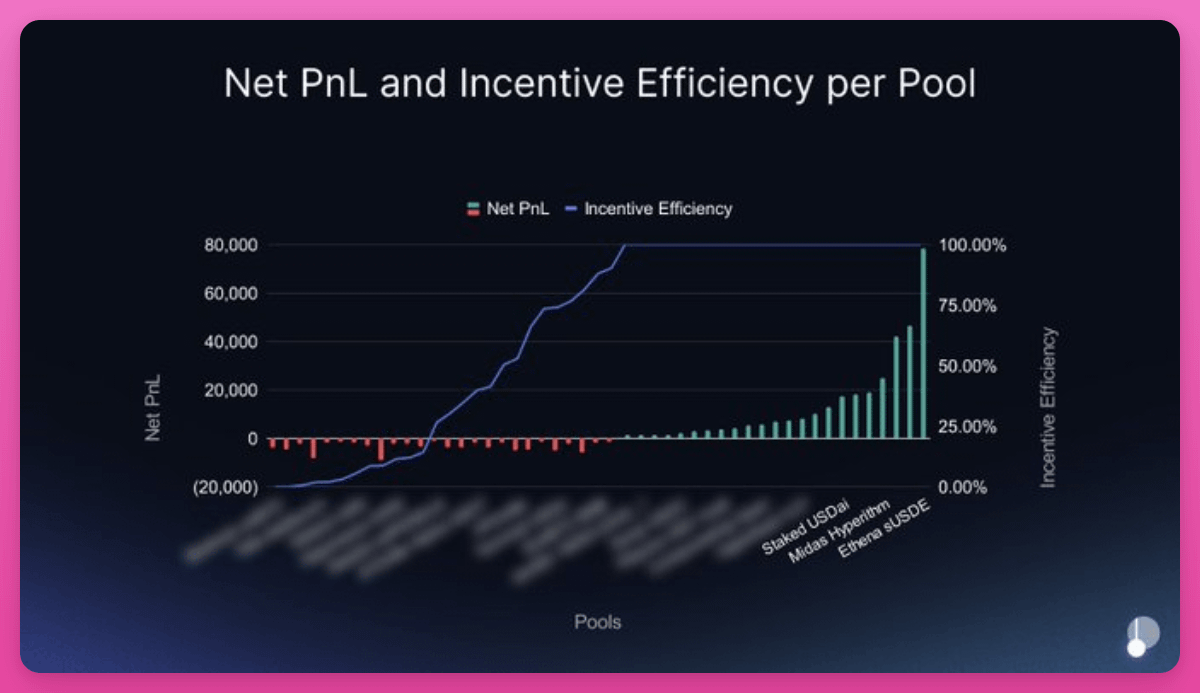

The Pendle team revealed that even though revenues grew 60-fold over 2 years, vePENDLE had the lowest participation rate among all ve token models—only 20% of the PENDLE supply was locked.

This mechanism, designed to align incentives, excluded 80% of holders. The fatal blow came from the detailed breakdown by liquidity pool: over 60% of the pools accepting emissions were unprofitable.

A few high-performing pools subsidized the majority of pools that destroyed value. Highly concentrated voters meant emissions flowed to where large holders had positions—these were the wrapper products, before being distributed to end-users.

In contrast, Curve's veCRV locking rate is about over 50%, Aerodrome's veAERO locking rate is about 44%, with an average locking duration of about 3.7 years. Pendle's 20% is too low. Compared to the capital opportunity cost of revenue markets, the locking incentives lack attractiveness. As of March, Aerodrome has distributed over 440 million dollars to veAERO voters.

Alternative: sPENDLE

14-day withdrawal window (or instant withdrawal with a 5% fee)

Algorithmic emissions (cutting about 30%)

Passive rewards, only for key PPP voting

Transferable, composable, re-stakable

80% of revenue → buy back PENDLE

sPENDLE is a liquid staking token at a 1:1 ratio with PENDLE, with rewards coming from income-supported buybacks rather than inflationary emissions. The algorithmic model will reduce emissions by about 30%, while guiding funds to profitable liquidity pools. Existing vePENDLE holders will receive a loyalty bonus (up to a 4x multiplier, decreasing over 2 years from the snapshot on January 29). A wallet associated with Arca accumulated over 8.3 million dollars in PENDLE within six days.

However, not everyone agrees with this decision. Curve founder Michael Egorov believes that ve token economics is a very powerful mechanism for aligning DeFi incentives.

PancakeSwap: veCAKE → Token Economics 3.0 (Burn + Direct Staking)

Where the problem occurred

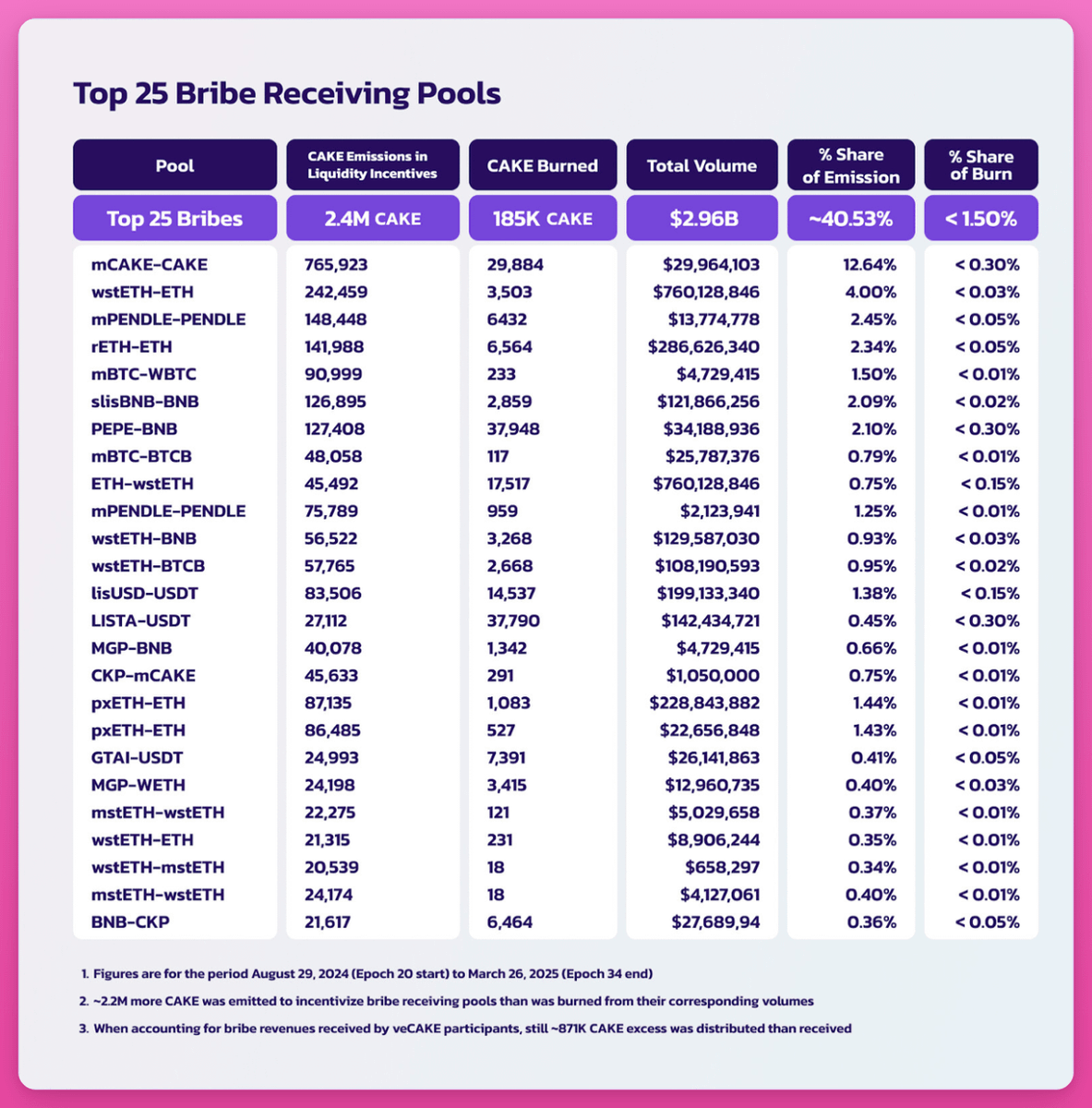

PancakeSwap's veCAKE is a textbook example of bribery-driven resource misallocation. The Gauge voting system has been captured by a Convex-style aggregator, most notably Magpie Finance, which siphoned off emissions while providing very little actual liquidity to PancakeSwap.

Data before the shutdown: liquidity pools receiving over 40% of total emissions contributed less than 2% of CAKE burned. The ve model created a bribery market where aggregators extracted value, while the liquidity pools generating fees were inadequately incentivized.

However, this shutdown was deliberately designed. Michael Egorov described it as "a model governance attack," believing that insiders of CAKE erased the governance rights of existing veCAKE holders and may have forced the unlocking of their tokens after voting. Cakepie DAO, as one of the largest CAKE holders, questioned the voting due to the existence of irregularities. PancakeSwap offered up to 1.5 million dollars in CAKE compensation to Cakepie users.

Alternative: 100% fee revenue → CAKE burning

The team directly manages emissions

1 CAKE = 1 vote (simple governance)

Approximately 22,500 CAKE per day (targeting 14,500 CAKE)

100% fee revenue → CAKE burning, no dividends

Target: annual deflation of 4%, reaching 20% by 2030

All locked CAKE/veCAKE positions can unlock without penalty, providing a 6-month 1:1 redemption window. Income dividends were changed to burning, with the destruction rate of key liquidity pools increased from 10% to 15%. PancakeSwap Infinity was launched simultaneously, adopting a redesigned liquidity pool structure.

Results after the transformation: a net supply reduction of 8.19% in 2025, continuous deflation for 29 months, with 37.6 million CAKE permanently burned since September 2023, and over 3.4 million CAKE burned just in January 2026, accumulating a trading volume of 35 trillion dollars (23.6 trillion dollars in 2025).

The deflation scheme looks good, but the CAKE price is still about 1.60 dollars, down about 92% from its historical peak.

Balancer: veBAL → Risk Liquidation (DAO + Zero Emissions)

Where the problem occurred

Balancer's failure is a cascading collapse of captured governance, security incidents, and economic bankruptcy.

The battle of the whales arrived first. In 2022, a whale named "Humpy" manipulated the veBAL system, directing 1.8 million dollars worth of BAL to their controlled CREAM/WETH liquidity pool within six weeks. In contrast, the revenue this liquidity pool brought to Balancer was only 18,000 dollars during the same period.

Then came an exploit incident. A rounding flaw in Balancer V2's exchange logic was exploited across multiple chains, leading to approximately 128 million dollars being drained, with TVL dropping 500 million dollars within two weeks, leaving Balancer Labs facing unmanageable legal risks again.

Alternative: 100% fees → DAO treasury

BAL emissions go to zero

100% of fees allocated to DAO treasury

Buy back BAL at a fixed price for exit

Focus: reCLAMM, LBP, stable liquidity pools

Maintain a streamlined team through Balancer OpCo

The models built around token rewards in the old DeFi paradigm are being phased out. Despite token economic issues, Martinelli pointed out that Balancer "is still generating real income," exceeding 1 million dollars in the past three months: "The problem is not that Balancer doesn't work, the problem is that the economics around Balancer don't work. These can be fixed."

Whether a streamlined DAO can maintain a TVL of 158 million dollars without incentives remains an open question. Notably, Balancer's market cap (9.9 million dollars) is currently lower than its treasury (14.4 million dollars).

Underlying Mechanisms

The above three exits are symptoms; the root cause is structural.

A recent analysis by Cube Exchange outlines three scenarios in which the ve token model may fail.

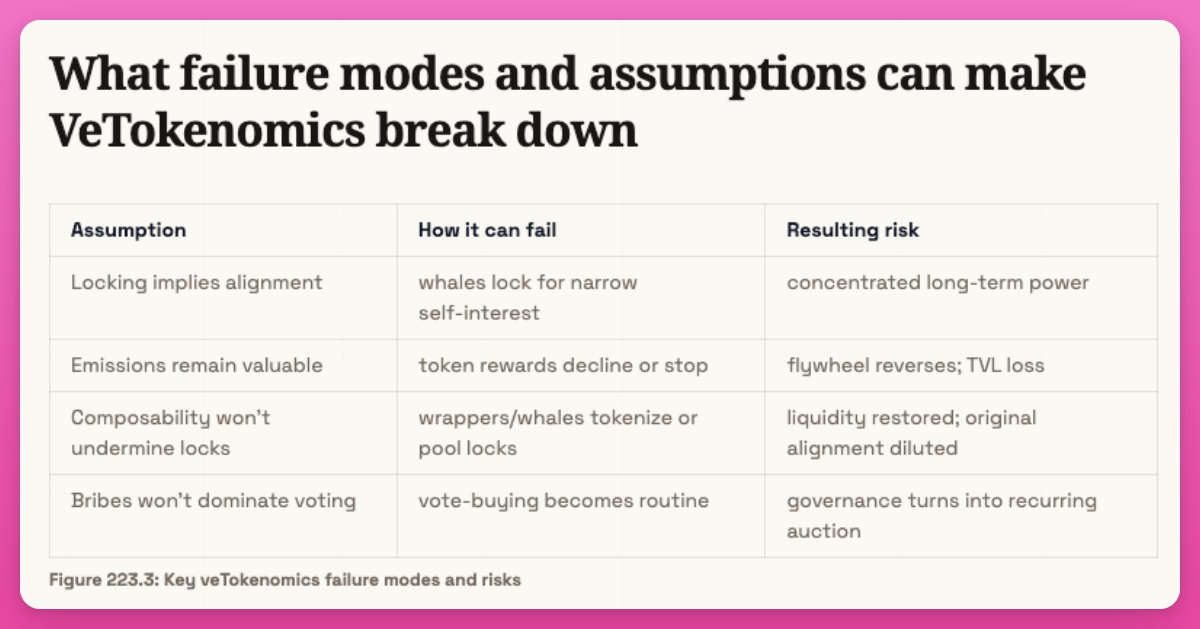

Assumption 1: Emissions must maintain value. If the token price crashes, emissions lose value → LP exits → liquidity, trading volume, and fees drop → more selling pressure. This is a classic reverse flywheel (observed in CRV, CAKE, BAL).

Assumption 2: Locking must be real. If locked tokens can be wrapped into liquid versions (Convex, Aura, Magpie), "locking" loses significance and creates accessible inefficiencies.

Assumption 3: There must be a real allocation problem. The effectiveness of ve assumes the protocol needs to constantly decide where to direct incentives (e.g., AMM). Without this, gauge voting becomes an unnecessary expense.

Diagnostic test: Does the protocol have a real, recurring allocation problem that allows community-driven emissions to create significantly more economic value than team-driven allocations? If not, ve token economics is merely increasing complexity without adding value.

Fee to Emission Ratio

The fee to emission ratio is the dollar value of fees generated by the protocol divided by the dollar value of the emissions distributed. When this ratio is above 1.0, the revenue earned from liquidity exceeds the spending to attract liquidity. Below 1.0, it indicates subsidized loss-making activities.

Here is a detail revealed by Pendle's exit: the overall ratio masks the real situation of each liquidity pool. Pendle's overall fee efficiency exceeds 1.0 (revenue greater than emissions). However, when the team breaks it down by liquidity pool, over 60% of pools viewed individually are unprofitable. A few high-performing liquidity pools (likely large stablecoin yield markets) subsidize other pools. Manual gauge voting directs emissions to benefit large voters rather than to the liquidity pools generating the most fees.

PancakeSwap experienced a similar situation, but it's reflected in CAKE burning.

Liquidity Locking Contradictions

Ve token economics creates a problem: capital locking is inefficient. Liquidity locking products solve this problem by wrapping locked tokens into tradable derivatives. However, while addressing capital efficiency issues, they create governance centralization problems. This is the core paradox of every ve token economics model.

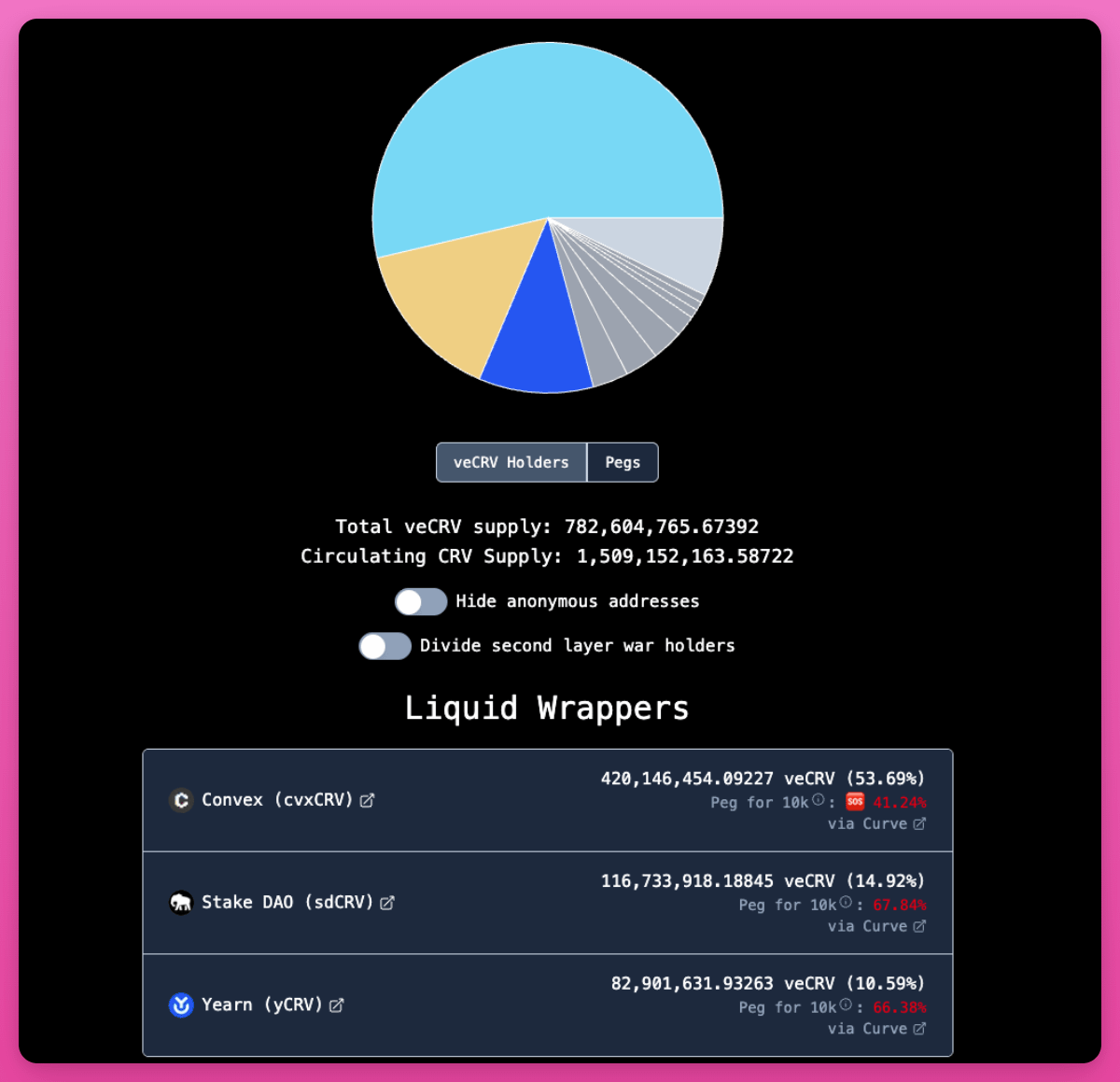

In Curve's case, this paradox resulted in stability (although centralized) outcomes. Convex holds 53% of all veCRV, and StakeDAO and Yearn hold additional shares. Through Convex, individual governance is effectively mediated through vlCVX voting. However, Convex's incentives align with Curve's success, and its entire operation relies on Curve's good performance. Centralization is structural, but not parasitic.

In Balancer's case, this paradox is destructive. Aura Finance became the largest veBAL holder and the de facto governance layer. The lack of other strong competitors led to a predatory whale (Humpy) independently accumulating 35% of veBAL and manipulating gauge caps to siphon off emissions.

In PancakeSwap's case, Magpie Finance and its aggregator captured gauge voting through bribery and directed emissions to liquidity pools providing very little value to PancakeSwap.

Ve token economics requires locking capital to operate, but locking capital is inefficient, leading to the emergence of intermediaries to unlock it, which centralizes governance power that was supposed to be decentralized. This model creates the conditions for being captured by itself.

Curve's Rebuttal on Why ve Token Economics Still Matters

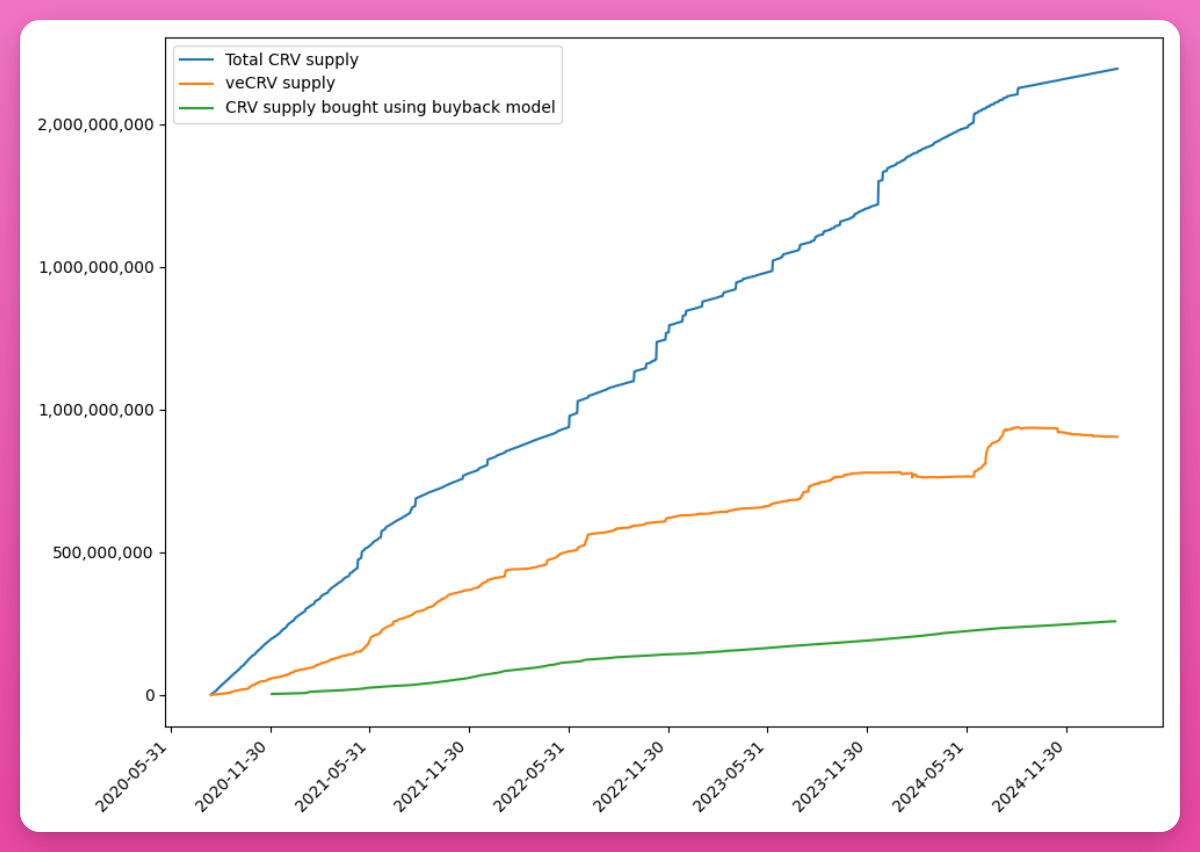

Curve's conclusion: the ongoing volume of locked veCRV tokens is always about three times the amount that a comparable burning mechanism could remove.

Scarcity based on locking is structurally deeper than scarcity based on burning, as it simultaneously generates governance participation, fee distribution, and liquidity coordination, rather than just a reduction in supply.

In 2025, Curve's DAO removed the veCRV whitelist, expanding access to DAO governance. The protocol's metrics are equally impressive: trading volume grew from 119 billion dollars in 2024 to 126 billion dollars in 2025, and liquidity pool interactions more than doubled to 25.2 million transactions, with Curve's share of Ethereum DEX fees rising from 1.6% at the beginning of 2025 to 44% in December, an increase of 27.5 times.

However, there is a rebuttal to the rebuttal: Curve occupies a unique position as the backbone of stablecoin liquidity on Ethereum, and 2025 is the year of stablecoins. Gauge-directed liquidity has real, market-driven, organic demand. Stablecoin issuers like Ethena are structurally dependent on Curve's liquidity pools. This creates a bribery market rooted in real economic value.

The three protocols that left ve token economics lack these. Pendle's value proposition is yield trading rather than liquidity coordination; PancakeSwap's is a multi-chain DEX; Balancer's is programmable liquidity pools. None of them provides a structural reason for external protocols to compete for their gauge emissions.

Conclusion

Ve token economics is not universally dead. Curve's veCRV and Aerodrome's ve(3,3) are doing well. However, the model only works when gauge-directed emissions can create liquidity that generates real economic demand. On the other hand, other protocols are choosing income-supported buybacks, deflationary supply mechanisms, or liquid governance tokens as alternatives to ve token economics.

Perhaps it is time for DeFi to have a new incentive mechanism that benefits both protocols and token holders' long-term interests.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。