Translation: Block unicorn

On March 17, the U.S. Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) issued a long-awaited set of regulatory guidelines for the cryptocurrency industry, which has been anticipated since 2013. I feel relieved about this and am striving to do so.

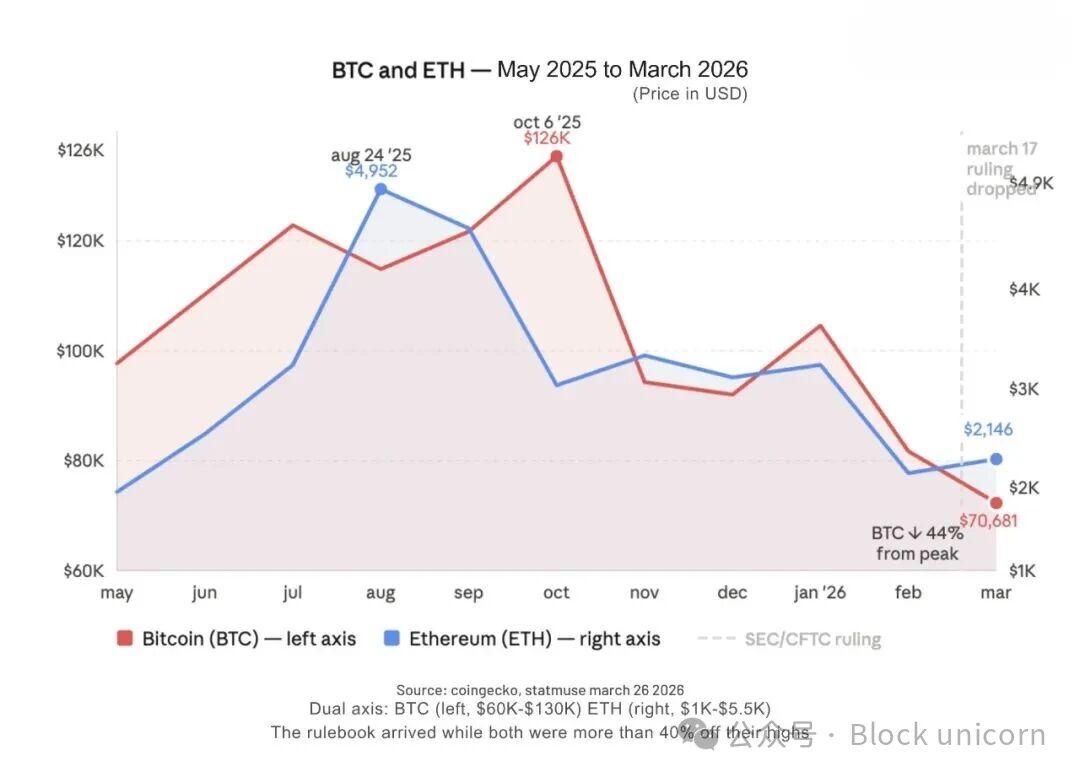

Bitcoin has fallen 44% from its peak in October. Ethereum's price is around $2,000, less than half of what it was seven months ago. The total market value of altcoins has evaporated by $470 billion since its peak. The fear and greed index has reached 11. This is not the score of a bad week but rather a score of 11 out of 100. This means people are no longer debating where the bottom is but are instead beginning to sell off the remaining cryptocurrencies.

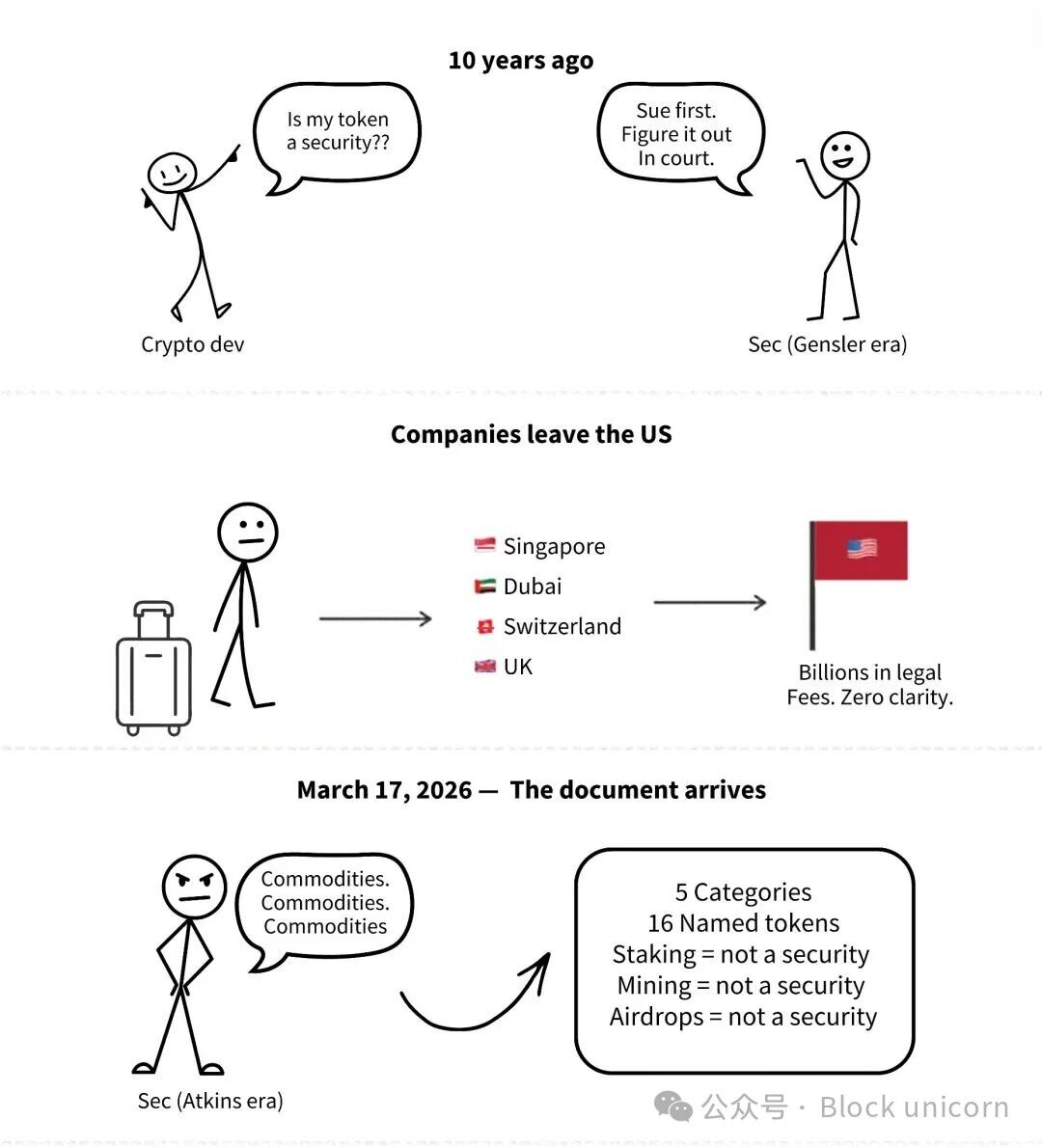

At this moment, on March 17, the SEC and CFTC released a document that finally revealed what the tokens you hold actually are. Prior to this, both parties had gone through a decade-long lawsuit, hundreds of enforcement actions, and billions of dollars in legal fees. Some companies even chose to relocate to Singapore rather than continue playing guessing games with Gary Gensler. And right in the week when Ethereum's price fell below $1,900, the answer was finally unveiled.

But the key point is that, despite the token economy being severely hit, everything underlying it is thriving. The circulation of stablecoins has exceeded $316 billion, and the scale of real-world assets (RWA) on-chain has reached $26.5 billion and continues to grow. Because of this, Morgan Stanley is building a crypto trust bank. Meta has given up its metaverse project but is bringing stablecoins to WhatsApp. Stripe is handling $400 billion worth of stablecoin transactions. Nasdaq is building a tokenized stock trading platform. Cryptocurrency is becoming a pillar of global finance, and in most cases, it does not rely on tokens.

Cryptocurrency is no longer just a speculative asset class. The regulatory policy rolled out on March 17 was originally designed for first-generation cryptocurrencies, but it was officially implemented only after the second generation of cryptocurrencies arrived.

But this does not mean it is meaningless.

SEC Chair Gary Gensler once said: We are no longer the 'Securities and Everything Commission.' Is this statement a bit late?

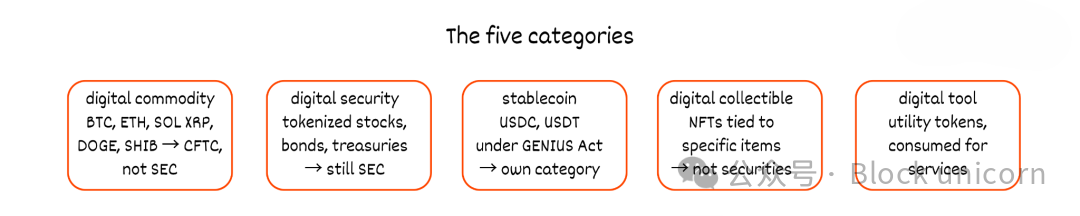

For the first time, U.S. regulators have a unified definition of cryptocurrency. There are five categories, with each token belonging to one of them. Next, I will provide these definitions, so please read them as if you have never heard of these concepts before.

Digital commodities are the main focus. Digital commodities are a type of crypto asset whose value derives from the programmed operation of a well-functioning cryptographic system and supply-demand dynamics. Its value does not depend on the management of a central issuer. If the network is truly decentralized and functions correctly, without any company supporting it, then the asset is a commodity. This is governed by the CFTC, not the SEC.

Major cryptocurrencies including Bitcoin, Ethereum, Solana, XRP, Cardano, Avalanche, Polkadot, Chainlink, Dogecoin, and Shiba Inu coin have been officially recognized as digital commodities. Dogecoin and Shiba Inu coin meet this definition because there is no issuer or organization driving their value growth. They have no promises, roadmaps, or teams whose continuous work is critical to the value of the tokens. For this reason, they are seen as commodities rather than securities. The criterion is whether anyone promises returns based on their work.

Digital securities refer to tokenized stocks, bonds, and government bonds. In short, these assets were securities before being placed on the blockchain and remain securities afterward. The SEC is responsible for regulating these assets. It's that simple.

Digital collectibles refer to NFTs tied to specific items or experiences. Digital tools refer to assets used to access software or services, with no expectation of investment returns. Stablecoins have their own category under the GENIUS Act.

Staking, mining, and airdrops have been permitted. The ruling explicitly states that receiving mining rewards, participating in on-chain staking, or receiving digital commodity airdrops do not constitute securities trading. This eliminates one of the biggest legal risks faced by proof-of-stake networks since the Gensler era. Packaging non-security tokens has also been permitted.

The 16 named tokens are all foundational infrastructures, having undergone years of decentralized development. DeFi protocol tokens—such as JUP, POL, METEOR, and most tokens launched in the past two years—have not been named and clearly do not meet the criteria. The threshold for a well-functioning and decentralized crypto system is high. Most actively developed protocols do not meet this standard. This interpretation should resolve the gray area that remains ambiguous for most tokens that individuals actually hold.

Value must derive from the programmatic operation of a well-functioning system, not from someone’s promises. This test standard could transform a decade of ambiguity into content that compliance officers can truly address.

There is more to the story

The announcement does not constitute a formal rulemaking process under the Administrative Procedure Act and does not carry the binding authority of law or formally promulgated regulations.

You might want to read that sentence again. This 68-page document we've been waiting for is just an explanatory announcement, not law or regulation, but merely a statement of the agency's position issued by the current chairs of the SEC and CFTC, who can revoke it at any time.

This clarification serves as a formal agency action by the SEC and CFTC and is binding. However, without relevant legislation, future administrations can modify it. The document itself reserves the right for the agencies to refine or expand their views. A future SEC chair with a different political stance wouldn’t need congressional approval to overturn this interpretation. The next administration may not even require new laws, just new leadership.

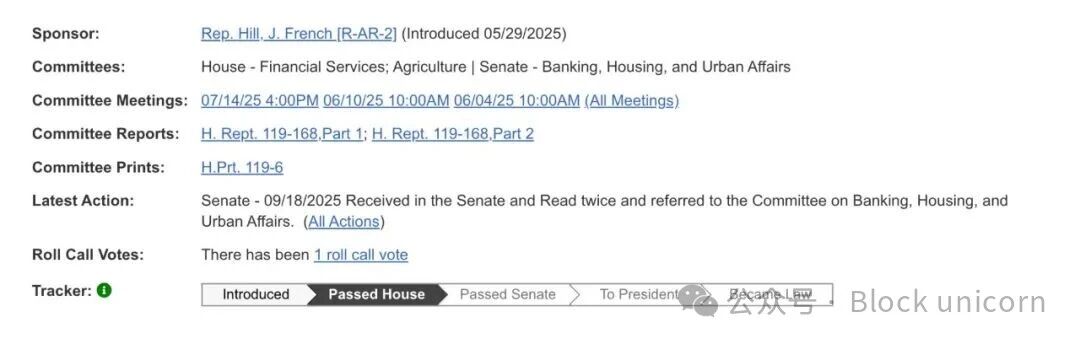

Atkins is well aware of this. He expressed this view on the day of the release, calling on Congress to take action to provide more lasting clarity. He views this explanation as a transitional measure, waiting for Congress to act on comprehensive market structure legislation. This legislation is the CLARITY Act. Currently, the CLARITY Act is undergoing review in the Senate.

The CLARITY Act

The House passed the CLARITY Act with a vote of 294 in July 2025. The bipartisan support at such a high level indicates that a real consensus has been reached.

Then it went to the Senate and stalled.

The key obstacle to passing the bill is the yield on stablecoins. Banks believe that allowing crypto platforms to pay interest on stablecoin balances would trigger deposit outflows. People would withdraw money from savings accounts and deposit it into USDC for higher returns. Subsequently, the banking lobby initiated lobbying efforts. The Senate Banking Committee canceled a scheduled review for January 2026. The bill made no progress in the following two months.

On March 20, Senators Thom Tillis and Angela Orsborn confirmed a principled agreement regarding stablecoin rewards, which has support from the White House. The agreement states: passive returns on stablecoins are prohibited; however, activity rewards linked to payments and platform usage are still allowed. Both sides are dissatisfied, and compromise often arises this way.

However, the yield agreement is just one of five tasks that need to be completed before the CLARITY Act can take effect. The completion of the other four legislative steps occurs during this year’s most tense period.

Review by the Senate Banking Committee and a full Senate vote (requires 60 votes).

Coordination with the Agriculture Committee.

Coordination with the House version.

- The President's signature.

The work of the Banking Committee is scheduled for late April, after the Easter recess. Senator Bernie Moreno warned that if the bill fails to be submitted to the full Senate for consideration by May, legislation on digital assets may not progress for several years.

In addition, the Iran war is taking up a large amount of discussion time in the Senate. Also, Trump is pushing for a voter ID bill to be passed first. Terms related to decentralized finance (DeFi) remain unresolved, with Senate Democrats expressing concerns about illegal financial risks. Ethical clauses have also yet to be finalized, particularly regarding whether senior government officials should be prohibited from profiting from cryptocurrency—this issue is obviously politically sensitive, given the cryptocurrency held by this administration. Senate Republicans are currently discussing adding provisions for easing regulations on community banks as a political bargaining chip to the bill, which would spark a new round of negotiations.

The House Financial Services Committee recently held a hearing titled “Tokenization and the Future of Securities: Modernizing Capital Markets.” Witnesses at the hearing included Kenneth Bentsen of the Securities Industry and Financial Markets Association (SIFMA), Summer Mersinger of the Blockchain Association, Christian Sabella of the Depository Trust & Clearing Corporation (DTCC), and John Zecca of Nasdaq. Both Nasdaq and the New York Stock Exchange are building tokenized stock trading platforms. DTCC is responsible for current settlements. If DTCC recognizes the efficiency of blockchain, then this debate would effectively end.

Thus, infrastructure development is based on a set of regulatory guidelines that may not exist two years from now. This is the dilemma currently faced by the industry. Companies are making billion-dollar decisions to build custodial systems, tokenization platforms, and staking infrastructure, all based on a persuasive yet non-binding explanatory document.

What is eternal, and what is not

For readers holding the aforementioned 16 tokens (e.g., ETH, SOL, XRP), these tokens have now been officially recognized as digital commodities under U.S. law due to statements from the leaders of both regulatory agencies. As long as these two leaders or their successors maintain this classification, it will continue to be valid.

If the CLARITY Act passes, it will become law. Any future chair will have no authority to overturn it without congressional approval. The listed assets will be permanently defined, and the classification standards will be binding.

If it is not passed by May, then the current classification system will depend solely on the opinion of a single government agency. At present, the 16 named assets are temporarily safe, but not all assets have been named. Most decentralized finance (DeFi), most new tokens, and any unpermissioned assets with no clear issuer remain in a gray area, and this issue has not been explicitly resolved in previous interpretations.

The most anticipated sentence is like a draft written in pencil.

Someone needs to pick up a pen to formalize this matter. Everything depends on the direction of the Senate in the next six weeks. Will these rules last long enough to make it all meaningful?

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。