Author: Apoorv Agrawal

Translated by: Deep Tide TechFlow

Deep Tide Introduction: This is the third article by the author in the series on ChatGPT's business model, with the first two articles addressing usage (900M weekly active users, 70% market share) and stickiness (retention smile curve, comparable usage depth to Slack). This article addresses the most critical question: How much is this attention actually worth? The core conclusion is counterintuitive— for leading AI applications, the ceiling for ad revenue may be higher than for subscription revenue, while 95% of ChatGPT's free users currently contribute nearly zero revenue, representing an unexploited monetization space in the entire industry.

The full text is as follows:

The first two articles in this series demonstrated ChatGPT's user scale and real engagement. The first two articles discussed "quantity" in the equation revenue = price × quantity—how many users, how often they return, and whether usage is genuine. This article discusses "price." How much can you actually earn?

Usage time is the bridge connecting the two. In consumer technology, time is the raw material for monetization. Subscription businesses convert time into perceived value and willingness to pay, while advertising businesses transform time into ad inventory. Both start from the same point: How much time does your product occupy for users?

The conclusion upfront: I believe that the advertising revenue opportunity for leading consumer AI applications may exceed that of subscription revenue. The reason is simple: consumer AI is accumulating the same raw materials as the largest internet companies—time and attention. The formula for ad revenue is straightforward: ad revenue = total duration × ad density × ad price. From these three variables, the data shows:

The total usage time of AI applications is experiencing explosive growth. The share of attention for AI follows a power-law distribution similar to the number of users, even when adjusted for usage time per user.

Per capita usage time is increasing, indicating a larger and more sustained growth of ad inventory. AI applications currently lag behind consumer benchmarks but are beginning to approach enterprise applications. The behavior pattern of ChatGPT resembles work and productivity tools rather than social media feeds. This is a strong signal for future enhancement of ad density.

ChatGPT’s query intent signals are stronger than search, implying a higher ad price. See Section 3 below for details.

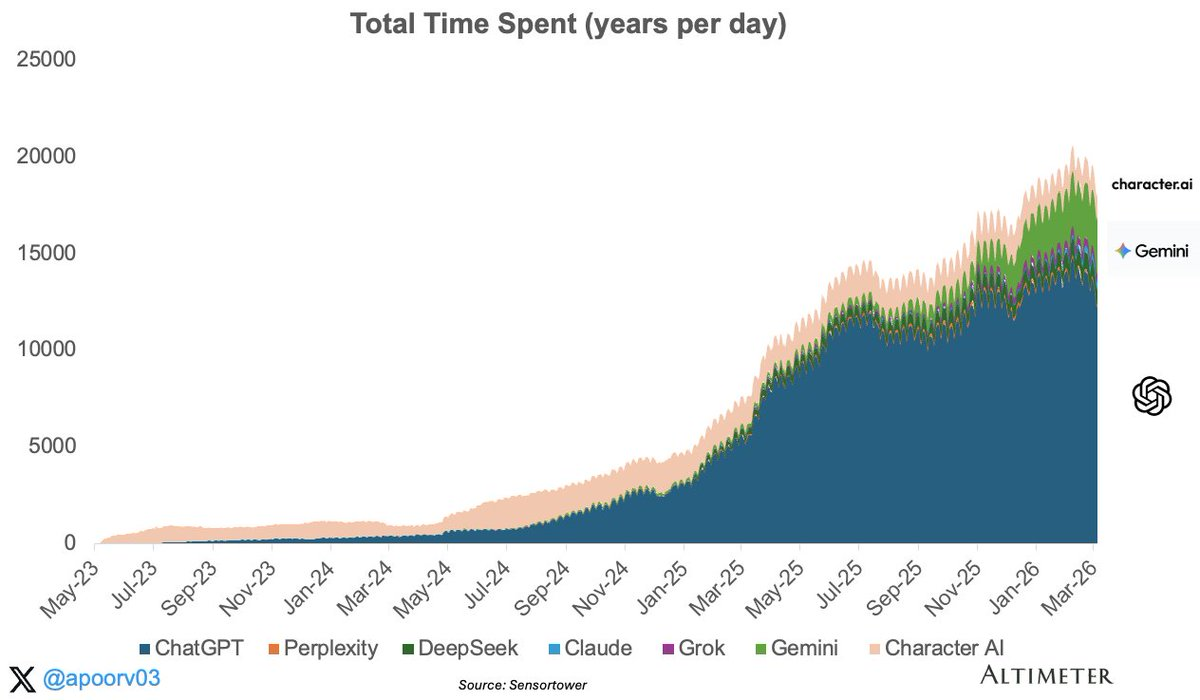

1. Total Duration: ChatGPT Captures 68% of Consumer AI Attention

The total usage time of generative AI applications has grown approximately 10 times over the past two years, with a growth of 3.6 times in just 2025. No application category expands this quickly.

There are a few points worth noting. First, the inflection point around January 2025 is very clear. Driven by the expansion of ChatGPT's voice, image generation, and search functionalities, the total usage time roughly doubled in the first half of 2025. Second, Gemini made a significant appearance in mid-2024 and achieved meaningful growth but still lags far behind the leader.

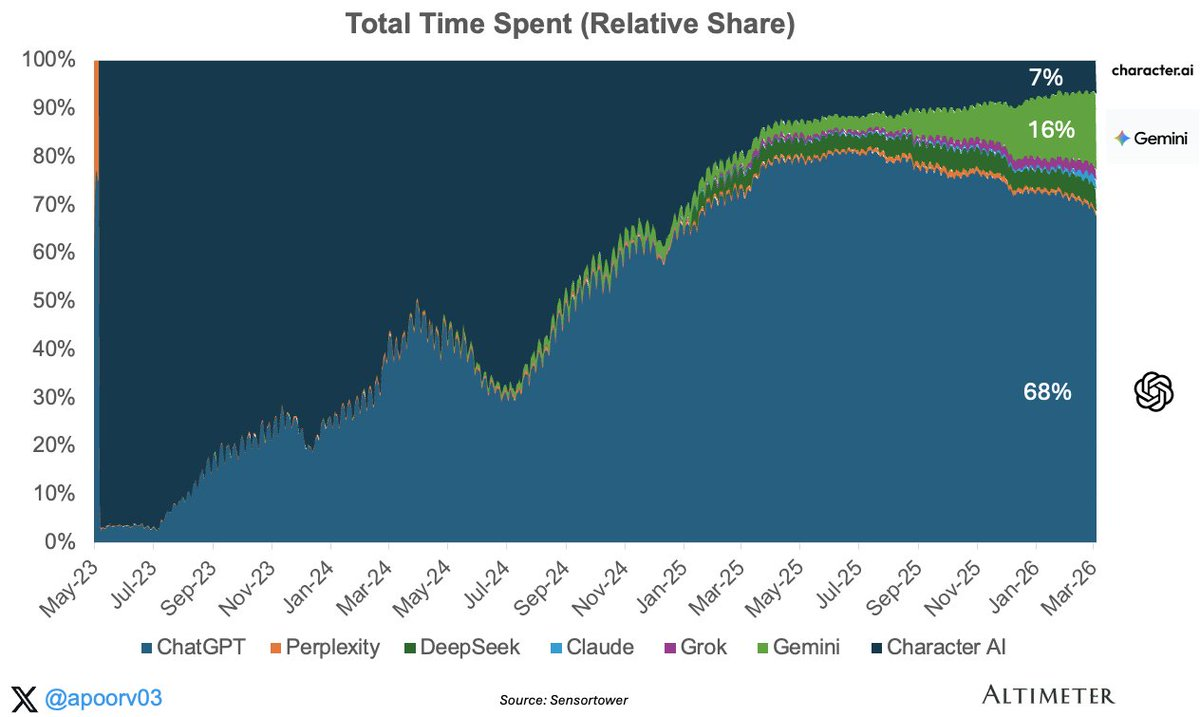

ChatGPT accounts for 68% of total AI usage time, Gemini 16%, and all other applications combined account for approximately 16%. This concentration makes ChatGPT the most likely place for the first-scaled AI native advertising business to emerge. It also helps explain why OpenAI has been quicker and more aggressive in monetization attempts compared to peers with smaller attention shares. This is important because you cannot advertise on a platform that lacks scale.

The places where users spend time are the ad spaces available to advertisers. And that 68% of inventory is concentrated in the ChatGPT product alone. This fact of high attention being focused on a single product is hard for advertisers assessing AI native ad placements to ignore.

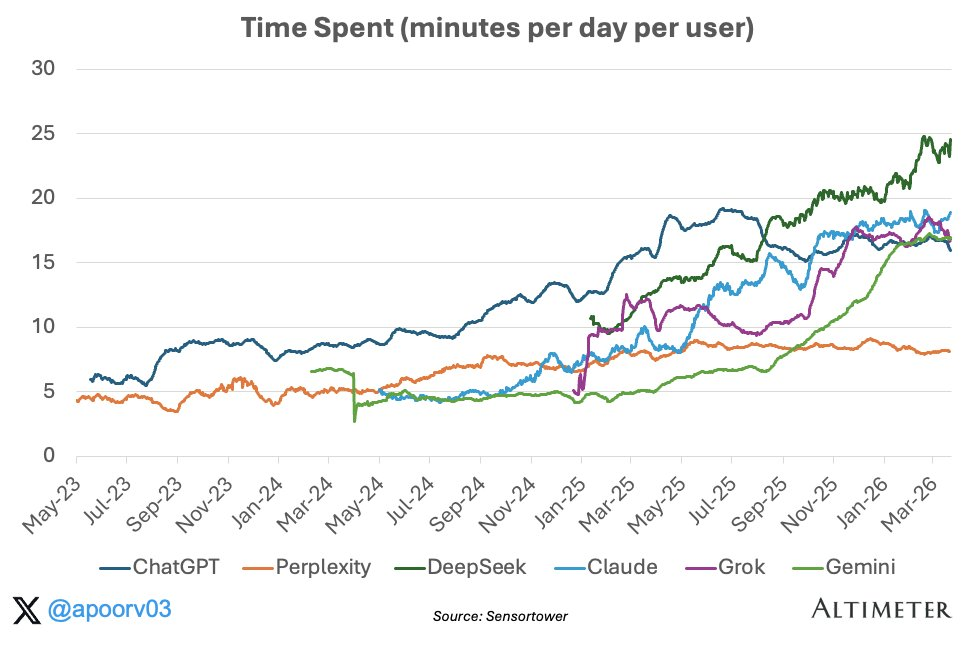

2. Increasing Per Capita Usage Time Means More Ad Space

Every AI application on this chart is trending upwards. Since the beginning of 2023, ChatGPT's per capita usage time has roughly tripled. Claude, Gemini, and Grok have all surged dramatically in the past year. The trend is clear: people are spending more time on AI applications rather than dropping off after download.

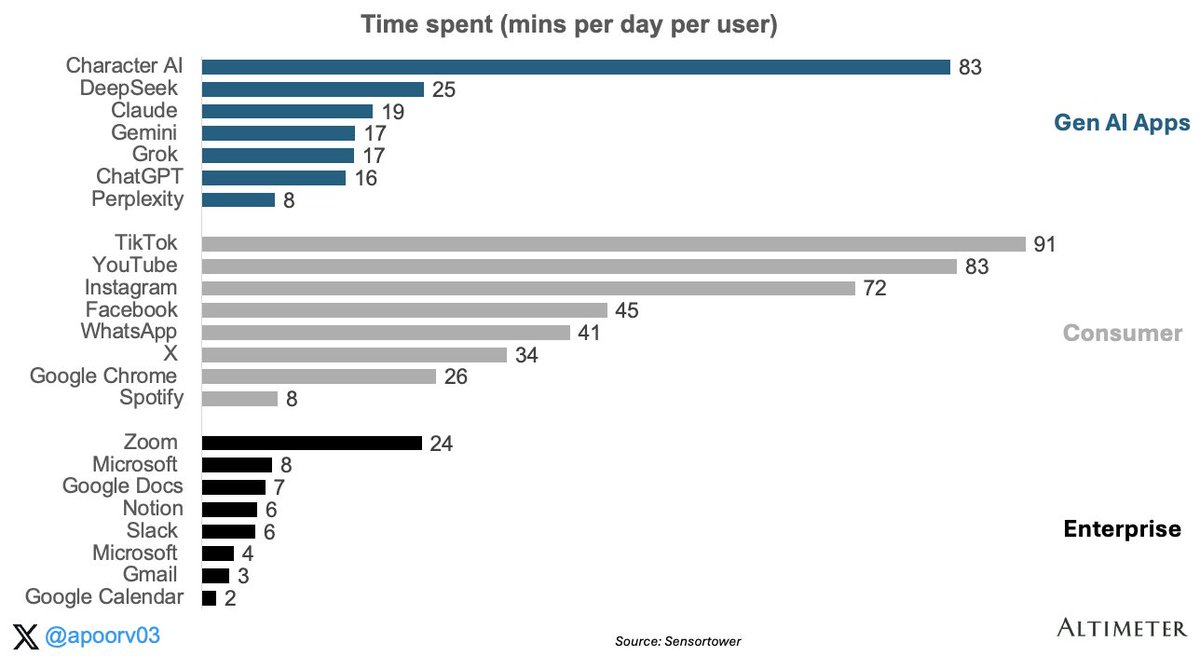

But how much is this duration compared to known consumer and enterprise application benchmarks?

Compared to consumer applications: still much lower. ChatGPT averages 16 minutes daily, far below TikTok, YouTube, Instagram, and others. But this gap is not a fair comparison because ChatGPT lacks two key elements that drive massive usage time in consumer applications.

First, it lacks social network effects. The stickiness of TikTok and Instagram stems partly from friends, creators, and communities being there. Content is personalized and generated by people you follow. This creates pull for continual returns and refreshes. ChatGPT does not have that; there is no information feed, no followers, and no social graph.

Second, it lacks dopamine loops. You don’t open ChatGPT to scroll through cat videos or check on an ex. Consumer social applications are designed for variable reward interactions: you never know if the next scroll will be boring or interesting, this unpredictability keeps you glued to the screen. AI assistants are the opposite. You come with specific tasks, get answers, and then leave.

Compared to enterprise applications: higher than most. The comparison to enterprise applications is more relevant, but there’s an important caveat: this comes from pure mobile data from SensorTower, and products primarily on desktop like Slack, Gmail, Google Docs are underrepresented. Even so, the signals remain significant. On mobile alone, ChatGPT appears to behave like a high-frequency productivity tool. This is important because productivity products can achieve good monetization even when their usage time is far below that of consumer entertainment applications.

Slack charges $7-12 per user per month. If AI assistants operate at this level of daily usage time under consumer scale, substantial monetization space exists.

Increasing per capita usage time means two things in the revenue equation: more perceived value to support subscription willingness to pay, and more ad placement space. Both point in the right direction.

3. Revenue Opportunities

3a. Why Advertising Can Surpass Subscriptions

Now let's look at the pricing side: how much is this attention actually worth? Under consumer scale, the two most important monetization models are subscriptions and ads. The key point is not that the subscription model is weak; rather, historically, the largest consumer internet companies have earned far more from ads than from subscriptions.

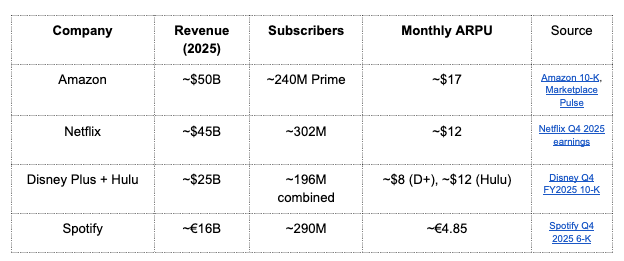

The largest consumer subscription business:

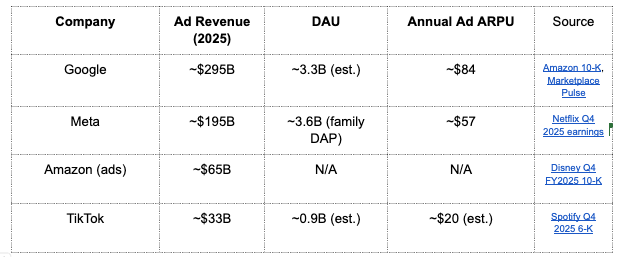

The largest consumer advertising business:

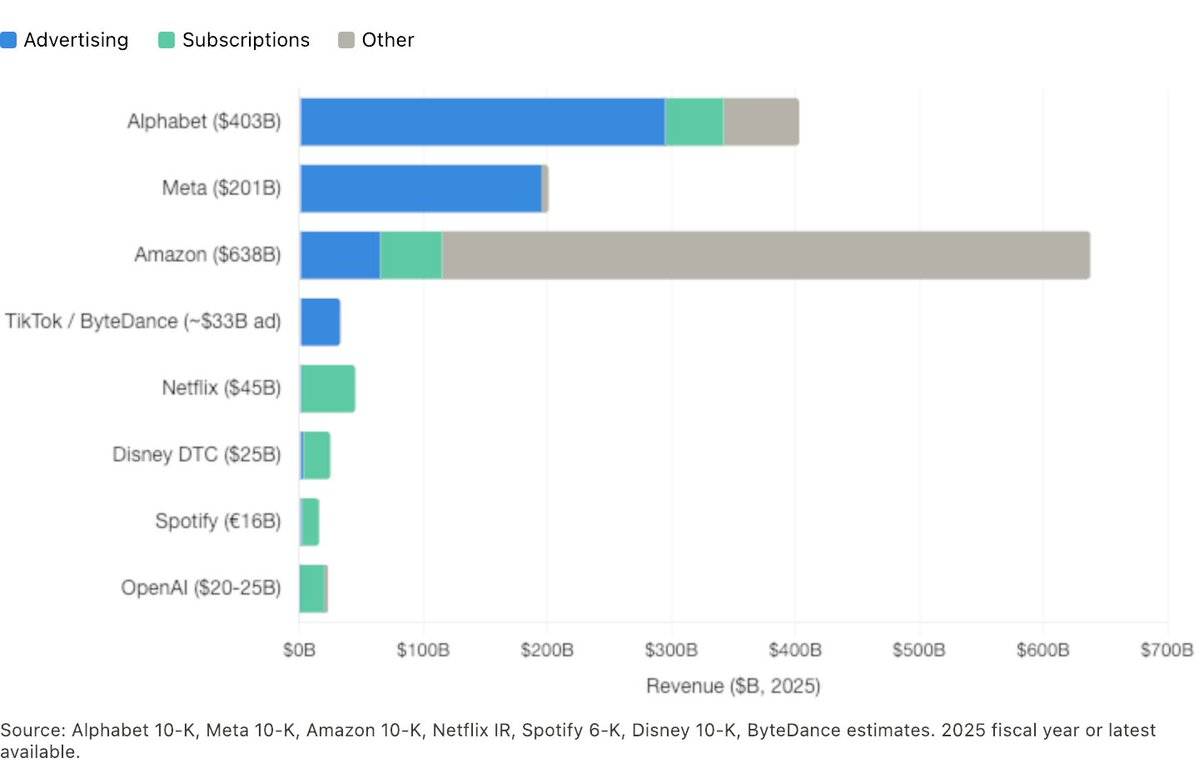

The magnitude gap is core. Google's ad revenue is about 5 times that of Netflix, and Meta's ad revenue is about 4 times that of Netflix. Even Amazon's ad business, which barely existed a decade ago, has now surpassed Netflix. A natural question arises: can higher subscription ARPU compensate for a smaller paying user base? For some businesses, it indeed can. But at scale, the larger monetization base from ads often prevails.

Alphabet and Amazon are particularly interesting because they simultaneously possess both models. In both cases, the ad business is larger than the subscription business and growing faster. Netflix, Disney, and Spotify largely rely on subscriptions, whereas Meta and TikTok almost entirely depend on ads. OpenAI currently almost entirely relies on subscription revenue, with a recent small-scale introduction of ads to about 5% of free users in the U.S. This represents a huge pool of attention that currently contributes nearly zero revenue. OpenAI is a pioneer here, but the same free user monetization problem applies to every AI application with a large unpaid user base.

3b. How AI Attention Is Priced

Ad revenue = total duration × ad density × ad price

Total duration: We have learned about total duration from Sections 1 and 2. ChatGPT has about 900 million weekly active users with a DAU:MAU ratio of 45%, averaging about 16 minutes daily on mobile.

Ad density (i.e., ad load) is a product decision. How many ads are shown per session? Google displays 3-4 ads per search results page, while Meta inserts an ad every 3-5 posts in the feed. Currently, ChatGPT displays a maximum of one ad per conversation, targeting only about 5% of mobile users. This restraint is wise for maintaining trust but signifies that the ad density variable is currently very low.

Ad price (CPM) is the price advertisers are willing to pay per thousand impressions. This is where it gets interesting because not all pricing for attention is the same. CPM is ultimately a function of the question: will this user purchase something? This breaks down into three components: intent (is the user actively making a decision?), attribution (can the advertiser trace the ad back to a purchase?), audience quality (does this user have purchasing power?).

Different advertising businesses rely on different advantages. Google Search has strong intent signals because when someone types in "best mortgage rates 2026," they are expressing commercial intent in real time. CPM ranges from $15-200+, varying by category, with global user annual income around $84. Meta’s intent signals are weaker, but it has massive usage time. Users scroll for 30-90 minutes daily, and Meta compensates for this with extraordinary precision targeting, inferring intent via behavior and social graph, with user annual income around $57. YouTube sits in between: moderate CPM, long sessions, video creativity.

In summary: Google sells intent, Meta sells attention, and YouTube sells watch time.

3c. Positioning of AI Assistants—Using ChatGPT as an Example

Using ChatGPT as a test case because it has the largest free user base and the most advertising data. The ad pricing for ChatGPT is likely closer to Google than to Meta, and it may have an advantage in categories where conversational context can enhance commercial intent.

When someone opens ChatGPT to ask for laptop recommendations, compare insurance plans, or plan a family trip, this interaction is similar to a search but with richer context. Users often provide budget, preferences, constraints, and intent in a single prompt. This can make commercial signals more interpretable for advertisers, even if it doesn’t automatically make every AI query more valuable than a search query.

I expect ChatGPT’s actual CPM to be at least comparable to Google Search and potentially higher in certain categories. Early data supports this assessment. OpenAI's premium ad slot is priced around $60 CPM, far higher than display advertising, and situated within the price range of high-intent search ads.

Currently, ChatGPT has about 800-900 million free users (accounting for 95% of weekly active users). If ChatGPT can generate $30 in ad revenue per year from each free user, at the current scale, it would mean $25 billion in ad revenue. For reference, Meta generates $57 per user, and Google generates $84, therefore $30 is not aggressive for a high-intent product that requires login.

Early data shows no impact on trust metrics, but the testing is still in its early stages. The real execution challenge is to scale ads 20 times without compromising the user habit-building experience. The primary reason this opportunity remains unverified is that not all AI usage time has commercial value. A significant portion of ChatGPT’s usage falls under information queries, creative generation, or productivity-oriented, rather than transaction-oriented. Moreover, unlike information feeds or search result pages, the conversational interface has fewer obvious placements to insert ads without compromising trust. Thus, the upside is real, but the execution constraints are equally real: OpenAI must monetize without damaging the product experience that builds habits.

There is a more optimistic possibility. AI is not just creating ad inventory; it can also create entirely new ad formats. Conversational ads, where product recommendations are woven into dialogues rather than attached to sidebars, could actually enhance rather than detract from user experience. Imagine asking ChatGPT to plan a weekend trip, and it recommends a relevant hotel discount based on your unique preferences and memories within the conversation. That isn’t intrusive; it’s functional. If AI can achieve hyper-personalization, agent-like behavior, and genuinely conversational brand interaction moments, the ad opportunities could not only scale enormously but also be entirely different from any existing ad experience today.

3d. Why Google Can Afford to Wait

Google's strategy is distinctly different from OpenAI's. Google has repeatedly stated that there are no plans to introduce ads in Gemini. In January at Davos, DeepMind CEO Demis Hassabis expressed his surprise at OpenAI's eagerness to push ads in ChatGPT. Google Ads VP Dan Taylor stated in December 2025, "There are no ads in Gemini applications, and there are currently no plans to change that."

This is a unique strategic luxury for Google. Google already has a money-printing machine in the search space with annual revenues of $295 billion. It can subsidize Gemini as a loss-leading product to grow users with an ad-free experience while monetizing AI through existing search infrastructure (AI Overview and AI formats have already introduced ads). OpenAI does not have that luxury. Lacking an independent cash cow to rely on, it must monetize directly from the chat interface.

Currently, Gemini monetizes only through subscriptions. Compared to the ad + subscription model that OpenAI is building, this represents a much smaller revenue opportunity per user. But Google is playing a different game, protecting the assistant to retain users while aggressively monetizing on search result pages. Whether this strategy remains viable when free user reasoning costs rise, and Gemini’s user base surpasses 750 million monthly active users, is an open question. At some point, the economics of operating a large-scale free AI assistant may compel even Google to take action.

In Summary

This series posed a simple question: Is consumer AI just about large usage, or is it becoming a real business? The first article showcased the reach, the second article demonstrated user habits, and the third article suggests that monetization opportunities may be greater than many believe.

One often underestimated point is that leading AI assistants, especially ChatGPT, possess the best characteristics for monetization seen in the largest consumer internet companies: scalable, repeatable attention. Approximately 95% of its weekly active users remain free users, meaning that today a large portion of attention is nearly unmonetized.

This does not guarantee that an ad business will reach the scale of Google or Meta. Conversation interfaces are harder to monetize cleanly, and trust is the product’s most valuable asset. However, if OpenAI can demonstrate that ads can coexist in high-intent assistants without harming the user experience, long-term advertising opportunities might eventually surpass subscription business. If that does occur, the real strategic issue facing Google will no longer be whether Gemini should remain ad-free, but rather how long it can sustain that.

Thanks to Sarah Friar and Fidji Simo for reviewing this article and drafts of the series.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。