Author: Chen Tianyu Universe

It is unclear when the changes in payment began, but a new round of fierce competition is about to unfold.

Have you noticed

that whether in groups, on social media, or during conversations, familiar terms like third-party, fourth-party, aggregation, and clearing seem to have started to fade away?

They have been replaced by some new stories and models.

Yesterday in a group, I saw a cross-border remittance startup, OpenFX, completed a financing of $94 million. The group members sent their blessings. I opened the news and saw that this company mainly provides faster and lower-cost settlement services for large cross-border funds by using stable * coins as a bridge connecting the banking system and blockchain infrastructure.

In the morning, I came across a piece of news that Alipay launched the country's first payment integrated AI Skills, allowing users to complete payment functionality integration using plain language through Vibe Coding. This may become a new option for future payment interfaces, allowing payment institutions to integrate their channels into skills for seamless payment access with a single command.

After dropping the kids off at school, I saw another news item while on the road. Mastercard has implemented AI proxy payment transaction acceptance in Hong Kong, with banks like HSBC, Standard Chartered, Citibank, and DBS supporting this type of transaction.

Combining the AI payments from major payment giants

it is not hard to find that today's payment discussions focus on three main areas: cross-border, cryptocurrency, and AI. I think this will also be the hottest direction for payments in the future.

Recently, I had some interactions with global payment service providers like Stripe, Airwallex, Adyen, and Deutsche Bank, and I found their underlying strategic layouts quite impressive.

I must say, payments have truly changed. The deep digitalization of domestic payments has been an old topic; everyone is advancing step by step, chewing through it bit by bit. At least in the capital market, it feels like there is not much buzz around it; people seldom talk about it anymore. Regardless of how creative the approaches are, it is still a game played within the existing market, with low growth.

Unless one gives up on transaction scale as the core indicator and instead pursues "comprehensive rates." Why comprehensive rates? Because for e-commerce platforms like Xiaoe Tech and WeChat Mini Stores, technical commission rates have reached 2%, which is significantly higher than the fees that can easily surpass a thousand.

Therefore, payment institutions should strive to extend their revenue channels through deep digitalization into transaction scenarios, while making transaction fees a thing of the past, transforming technical service fees into a new frontier.

Returning to the new payment hotspots

Recently, a partner from a Hong Kong investment firm approached me, asking if I would be interested in exploring cross-border payments, stable * coins, A2A payments in Hong Kong... Would I be interested? To be honest, I feel a bit torn.

Why the dilemma? Because the current payment window is just like mobile payments were ten years ago, right at the explosion point.

New payment paradigms such as cross-border payments, crypto payments, and AI payments, as well as new payment methods like U Cards / U Codes are emerging...

This is the most chaotic moment for payments, but it is also the period with the greatest opportunity window—lots of opportunities, plenty of models to choose from, and plenty of money...

If ten years ago was a cake-cutting period for market share, today is the time when multiple paradigms emerge simultaneously and opportunities are everywhere with choices in abundance.

The old cake has been divided, and it's about to spoil; now, the new cake is getting bigger, and a new round of division and structure is forming.

It can be said that we have reached the toughest historical turning point in payments, but we are also witnessing the best era of new payments.

That's all I have to say.

Finally, if you were given $50 million to engage in payments, what would you plan to do? Share your passion and vision, make a wish, and wish everyone success!

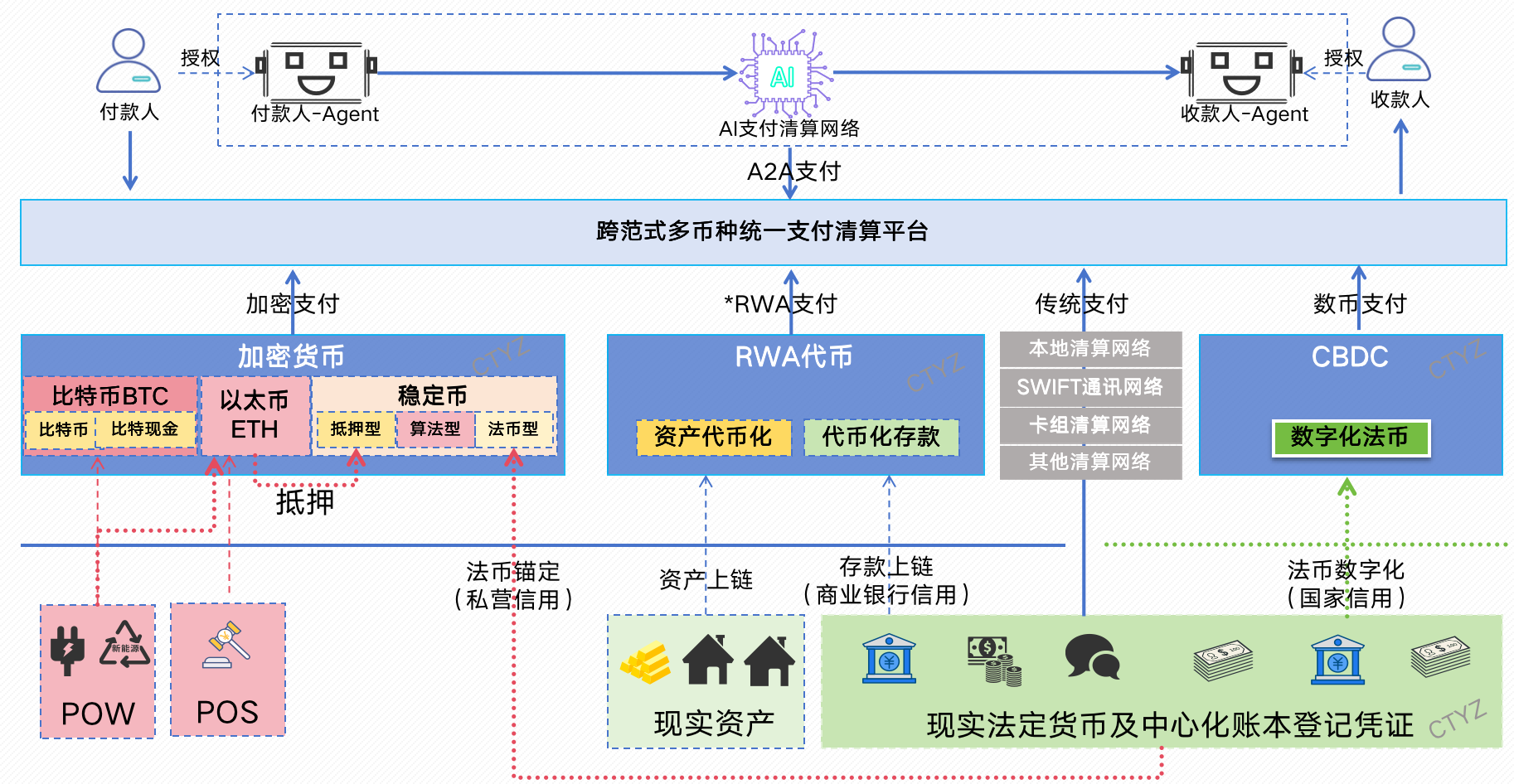

Let me go first: to create a unified multi-currency aggregation payment clearing platform, as shown in the image, allowing users to pay with whatever they want and merchants to receive whatever they want—a unified payment landscape that completely breaks the paradigm boundaries of fund flow!

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。