Written by: Frank, Maitong MSX

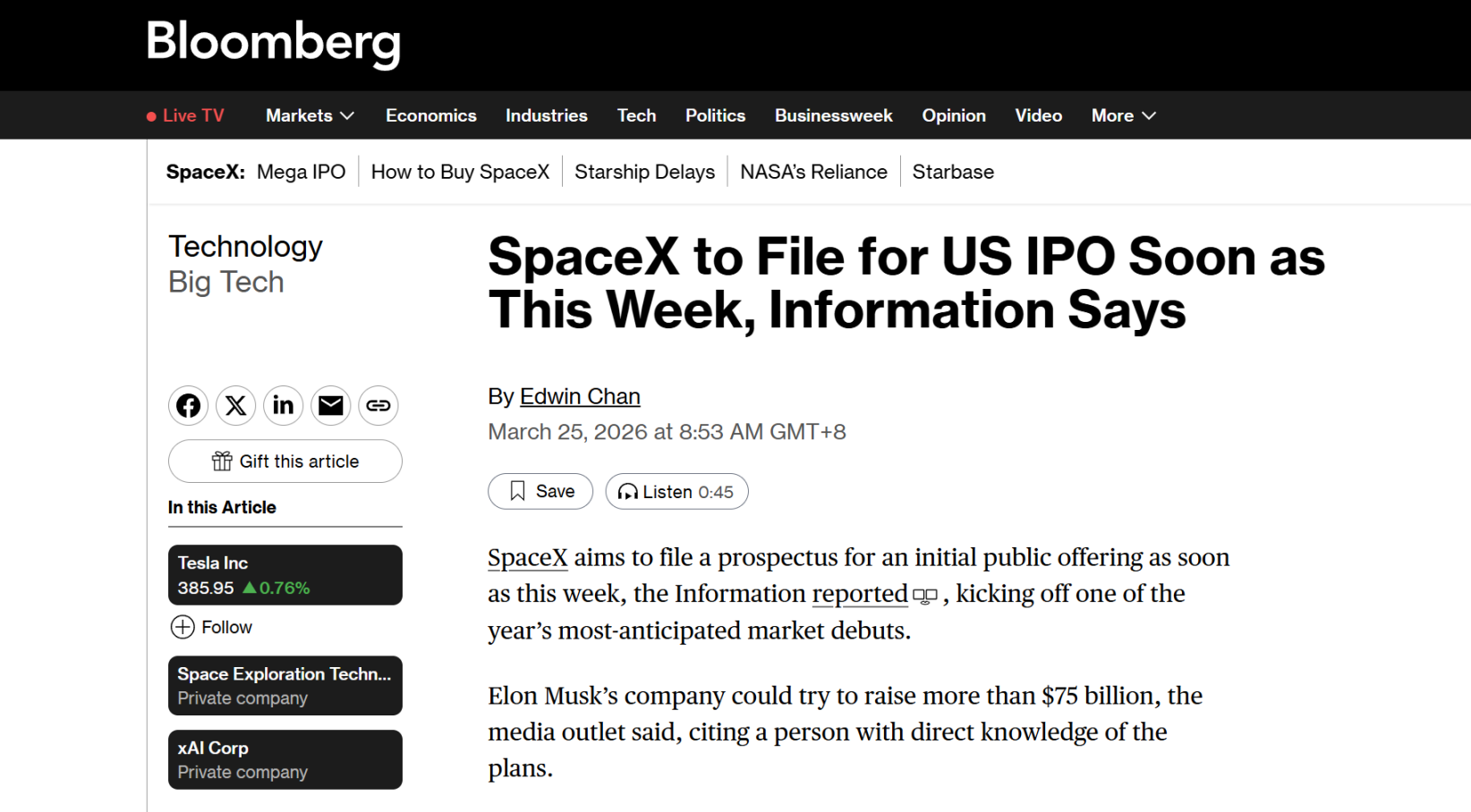

This year's most watched unicorn IPO in the US stock market seems to be just a step away from happening.

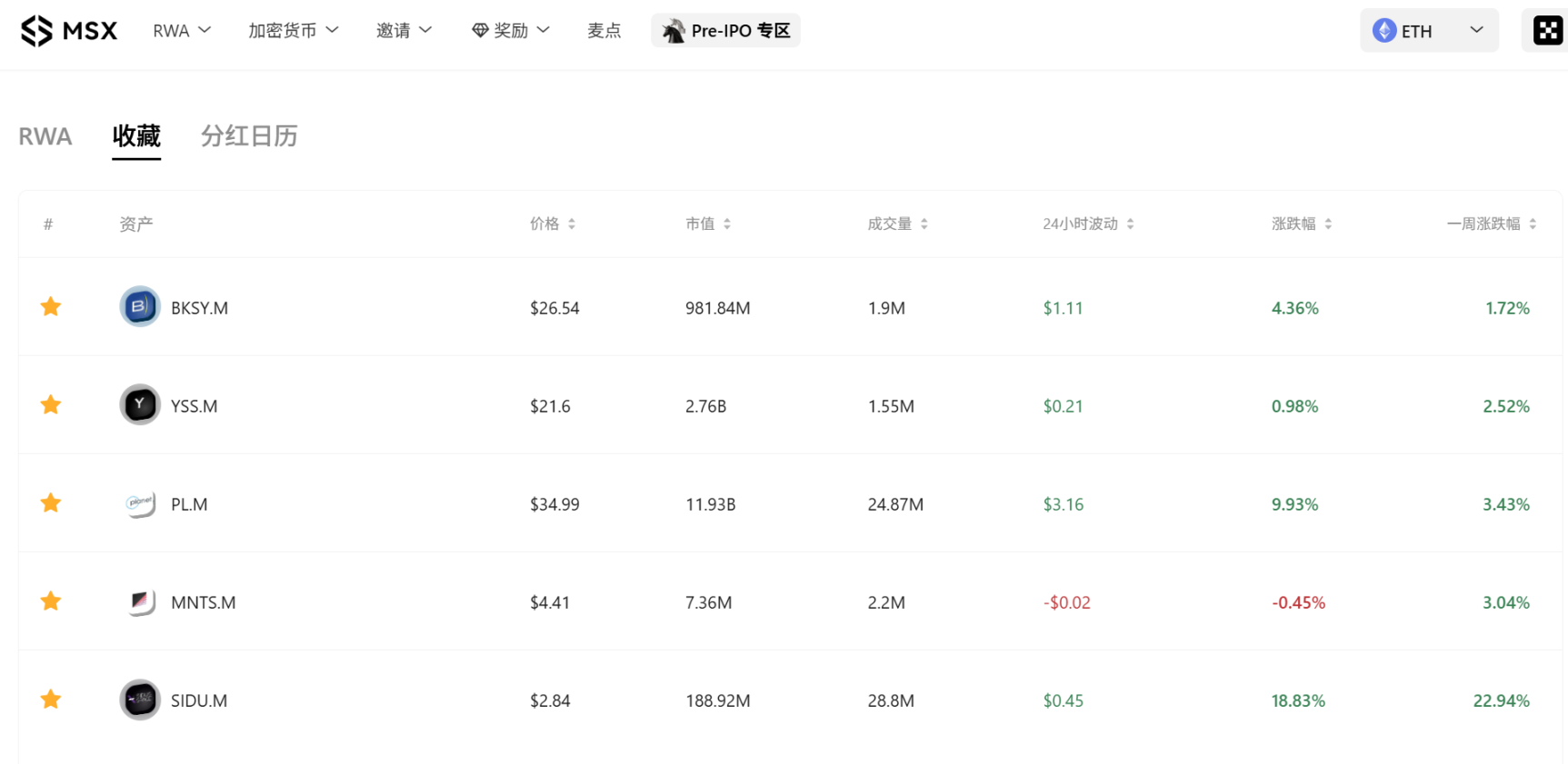

Sources reveal that SpaceX plans to secretly submit its IPO prospectus as early as this week or next week, aiming for a listing in June. The commercial space and space concept sector is responding accordingly. It was just before this wave of market activity that MSX screened and introduced five commercial space US stock tokens MNTS.M, SIDU.M, PL.M, BKSY.M, and YSS.M on March 23, all of which recorded double-digit increases, with some stocks rising nearly 30% during trading, providing investors with a relatively ample window for entry.

Notably, SpaceX's financing scale may exceed $75 billion. If realized, this would not only significantly surpass the previously circulated target of about $50 billion but also far exceed Saudi Aramco's $29.4 billion fundraising record in 2019, making it the largest IPO in history, without exception.

This raises the real question this article seeks to discuss: Aside from the sentiment catalyzed by the rumors surrounding SpaceX, what deeper logic is at play behind this rise in the commercial space sector? And does this wave of revaluation have the foundation for further diffusion?

1. SpaceX IPO, the starting gun for the commercial space sector?

Although SpaceX has never gone public, its influence on the secondary market has never been absent.

Understanding this requires first grasping SpaceX's position within the entire commercial space ecosystem. It is no longer just a rocket company but a key infrastructure provider that supports the entire commercial space industry chain, serving as the strongest "valuation anchor" in global commercial space—from launch capacity to Starlink communications, from orbital transportation to crewed flight, every technological breakthrough by SpaceX contributes to reducing costs and improving efficiency for a several downstream small and medium-sized space companies.

For this reason, the current strength of space stocks is naturally linked to the catalyzing news of SpaceX potentially initiating its IPO. The $75 billion fundraising target and the potential valuation of $1.75 trillion are powerful incentives for the whole commercial space sector.

Thus, we see that it is not just a single company strengthening but the entire space concept sector beginning to heat up in a synchronized manner, forming a noticeable sector resonance.

The most obvious manifestation is that the newly introduced commercial space "Five Little Dragons" MNTS.M, SIDU.M, PL.M, BKSY.M, and YSS.M have solid fundamental support, representing a concentration of the core directions within the commercial space industry chain:

MNTS.M (Momentus) is positioned for "last-mile" orbital transfer services in near-Earth orbit, with its Vigoride spacecraft set to ride aboard SpaceX's Falcon 9 for its next mission, meaning this is not just a simple launch, but a commercial validation indicating that as global satellite networking accelerates, the demand for orbital transfer is shifting from "optional" to "essential."

SIDU.M (Sidus Space) serves as a "stepping stone" within the defense system, having qualified for multiple project office contracts from the U.S. Missile Defense Agency (MDA), providing a ticket to continuously bid within the defense procurement system. For early-stage space companies, government contract qualifications are the most direct trigger for valuation restructuring and serve as the most stable income anchor beyond commercial orders.

PL.M (Planet Labs) is the most solid leader in remote sensing in this market surge, also holding the highest total market cap among the five newly introduced US stock tokens by MSX. It has a satellite constellation covering the globe, daily revisit capabilities, and a real-world commercial data subscription model.

This also makes it one of the few space companies where discussions can include ARR and gross margins, with a backlog increasing by 79% compared to the same period last year, nearing $900 million, and has achieved profitability for the first time—this milestone's significance goes beyond just a seasonal report figure.

BKSY.M (BlackSky) is transitioning from a "satellite company" to an "intelligence service provider," with its core competitiveness stemming from high-frequency revisits combined with AI analytic capabilities. Its third-generation (Gen-3) satellite constellation can provide commercially available high-resolution images at 35 centimeters (0.35 meters), layered with geopolitical-driven intelligence demand. The shift from selling data to selling decision support undoubtedly presents a significant premium space compared to merely being a remote sensing data provider.

YSS.M (York Space Systems) is a core supplier of the U.S. Army's proliferated battlefield space awareness (PWSA) project backed by the military, with military contracts providing predictable cash flow principles. As a newly emerging IPO target, the institution's warehouse-building period has not yet ended, and the chip structure is relatively clean, possessing high upward elasticity.

Ultimately, MSX's early introduction of these five targets aims to cover the core directions within the commercial space industry chain: some focus on orbital transport and mission execution, some on satellites and defense orders, some on earth observation and remote sensing data, and others on newly listed, high-elasticity satellite platform companies.

The significance of this set of target combinations lies not merely in betting on a single event but in attempting to pre-leverage various beneficial directions surrounding the "commercial space revaluation" theme, which is a core factor behind MSX’s preemptive bets on the general rise.

2. Moving from "Science Fiction" to "Hard Currency" Revaluation

Of course, if we simply understand this wave of increase as "news-driven," we would be underestimating its historical backdrop.

Revisiting the logic behind the stock selection before this soaring market, MSX was not blindly betting on sentiment but captured two core signals:

- On one hand, at last week's concluded NVIDIA GTC Conference, Jensen Huang announced the strategic layout in the space industry, from exclusive space-grade computing chips to cosmic digital twins tailored for orbital environments, signaling that AI is no longer just a productivity tool on the surface; it is becoming the underlying architecture for satellite autonomous navigation and real-time processing of low Earth data;

- On the other hand, on March 23, SpaceX, Tesla, and xAI jointly announced the launch of the "TERAFAB" project, aiming to leverage AI and highly automated manufacturing capabilities to produce one terawatt of AI computing chips annually, primarily for space deployment, equivalent to painting a large picture of scalable multiplication for the secondary market;

Based on a deep evaluation of these two signals, the MSX research team decisively completed its coverage of the commercial space "Five Little Dragons" on the day of the 23rd.

It is well-known that for a long time, the commercial space sector was viewed as a "monetary drain" in the secondary market, where companies faced high R&D investments, lengthy project cycles, slow realization of profits, and significant cash flow pressures, even though terms like rockets, satellites, moon landings, deep space, and Starlink sound alluring.

But this time, something has begun to change.

Starting in 2025, commercial space will not just be about "launching rockets," but will gradually be dismantled into a clearer and more easily understood reality industrial chain for the capital market. Particularly beyond rocket launches, more and more viable and sustainable business opportunities have begun to surface:

Satellite manufacturing, in-orbit services, earth observation, defense remote sensing, low Earth communication networks, AI-enabled image analysis, and intelligence distribution mean that the value of commercial space no longer solely comes from some distant future vision, but increasingly from verifiable orders, service capabilities, and customer demands.

Furthermore, there are actually three deeper logics occurring simultaneously behind this round of revaluation.

First, the significant reduction in launch costs is changing the economic foundation of the entire industry. The maturity of reusable rocket technology is continuously driving down the unit cost of entering orbit; lower launch costs, in turn, lower the thresholds for satellite networking, in-orbit services, and data commercialization.

For many small and medium-sized commercial space companies, this means that businesses that previously could only remain in the experimental verification stage are beginning to have the potential to move toward scaled deployments and profitability. SpaceX itself is the biggest driver of this cost curve, and it is precisely for this reason that expectations for its IPO would have such a strong spillover effect on the entire sector.

Second, commercial space is beginning to converge with larger thematic trends of the era. The strongest themes in today’s market include AI, national defense, communications, and new energy, and space infrastructure just happens to intersect with these themes. AI requires a continuous stream of high-quality data and stronger edge perception capabilities; defense systems increasingly rely on real-time reconnaissance, space communication, and distributed satellite networks; global geopolitical competition further elevates the strategic value of aerospace capabilities.

When a race starts to embed multiple mainstream narratives at once, it is no longer an isolated niche concept, but is more likely to become a thematic hub for repeated capital allocation.

Finally, the market is starting to accept differentiated pricing within the commercial space sector. In the past, whenever space stocks were mentioned, the market assumed they were emotional thematic assets that rose and fell together. Now, as the industry matures, investors are beginning to realize that the values of different companies do not exist on the same level. For example, some sell satellite platforms, some sell image data, some sell qualifications for defense contracts, some sell in-orbit service capabilities, and some sell liquidity in new stocks.

This signifies that the commercial space sector is gradually transitioning from thematic linkage to "layered pricing within the industrial chain," and once a sector enters this stage, it often means that it is no longer just a short-term concept but has begun to possess the foundation for long-term research and ongoing trading.

3. What This Wave of Space Stock Increases Means for Investors

Thus, on the surface, this round of increases indeed has been ignited by the warming expectations for SpaceX, but on a deeper level, the real driver for the market to re-invest is that commercial space is evolving from a distant narrative sector into a "pricable sector" with industrial stratification.

This also marks a foundational logic shift that capital markets are willing to begin pricing carefully.

However, after the excitement, how far the market can go ultimately must return to the fundamentals. The MSX research institute believes that after short-term sentiment catalysis, the true depth and sustainability of this wave of market trends depend on several key variables:

- Substantial progress in the SpaceX IPO process: the secret submission of the prospectus is only the first step; each node of the roadshow, pricing, and listing will continuously provide topical heat and capital siphoning effects for the sector;

- The rhythm of the realization of U.S. defense and aerospace budgets: the increase in new fiscal year's project budget has been confirmed, but which companies the contracts specifically flow to will gradually be revealed over the next two quarters. This is the main source of stock differentiation; after all, companies supported by contracts will have increasingly different trajectories from those solely driven by sentiment;

- Cash reserves and financing capabilities of various companies: most early-stage space companies are still in a loss-making phase, and the rising market period is often also a window for financing. A particularly noteworthy signal is whether management chooses to supplement ammunition at high positions rather than cashing out—this is the most direct and hardest to disguise indicator of internal confidence;

Of course, no matter how the short term unfolds, one thing's direction is increasingly clear, the SpaceX IPO will not be the endpoint of this industrial story; rather, it is more likely to be the starting point for the entire commercial space industry chain to truly enter the mainstream capital view.

For the past decade, the stories in this race have mostly remained at the PPT and conceptual level, with capital often pricing for "imagination"; while in the coming years, the market will increasingly measure the value of these companies using real income, tangible contracts, and verifiable profitability benchmarks.

This presents both opportunities and demands for investors.

The window of sector resonance is not a common occurrence, but the few that can truly traverse cycles will always be among a select few.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。