Author: Joseph Ayoub

Translated by: Deep Tide TechFlow

Deep Tide Guide: Everyone is discussing computing power and models, but this article raises a more fundamental question: Can energy supply keep up? Morgan Stanley predicts that by 2028, the United States will face a 45GW power shortfall, and the delivery time for large transformers has reached 24 to 36 months, while AI data centers consume electricity at an annual growth rate of 15%. The author deduces seven investment logics, from grid fragmentation to solid-state transformers to two-phase cooling, with less common but critical perspectives.

The full text is as follows:

NVIDIA recently released a framework stating "AI is a five-layer cake." Today, I will argue that the energy layer is the binding constraint of intelligent growth and discuss its implications.

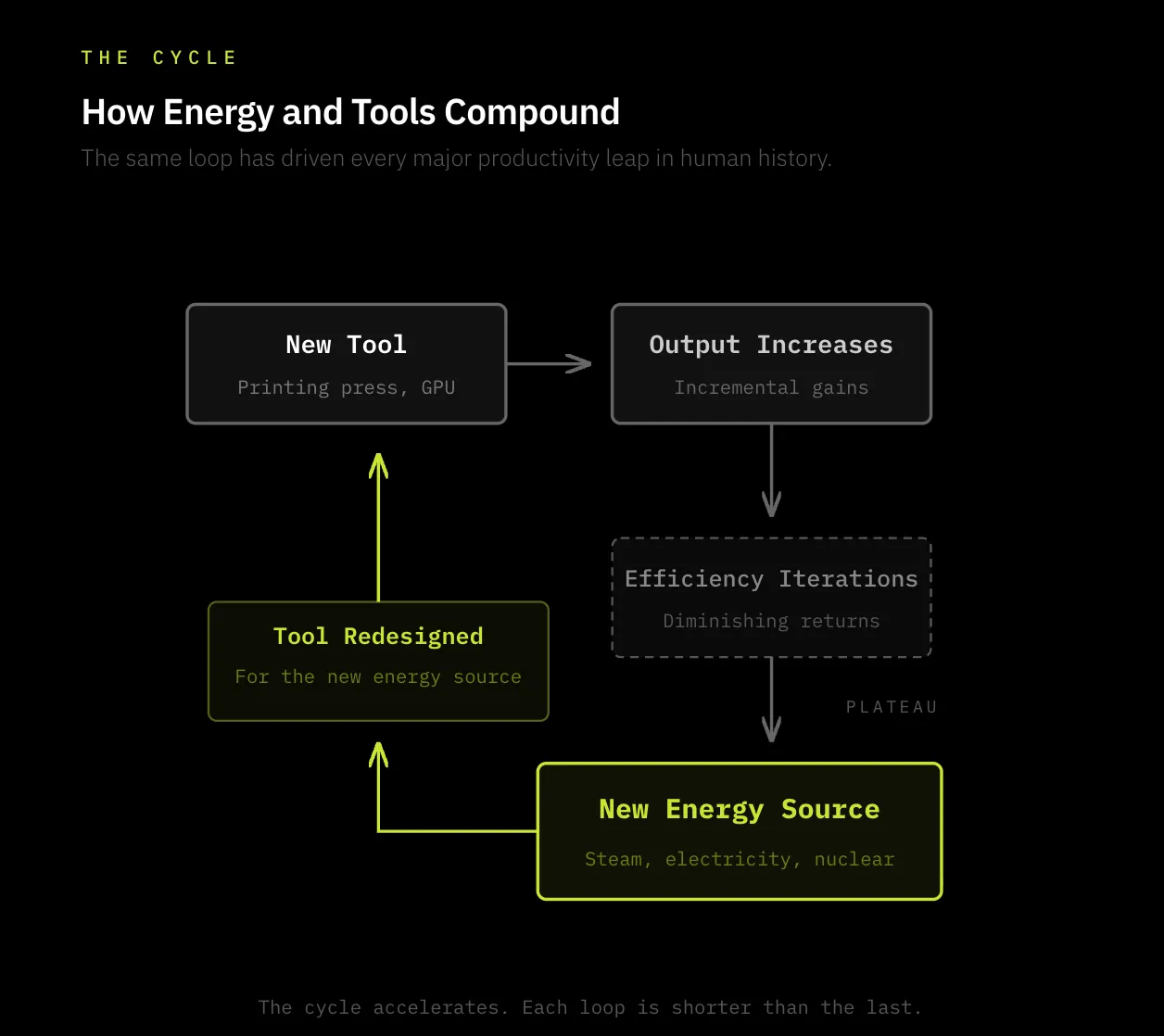

The progress of human civilization is the result of our ability to harness tools—be it hammers, fire, horses, printing presses, telephones, light bulbs, steam engines, radios, or AI. These "tools" are how humanity converts energy into productivity.

Fundamentally, we enhance human productivity by capturing energy and directing it towards goals using tools.

In short, the core logic of human civilization's advancement is as follows:

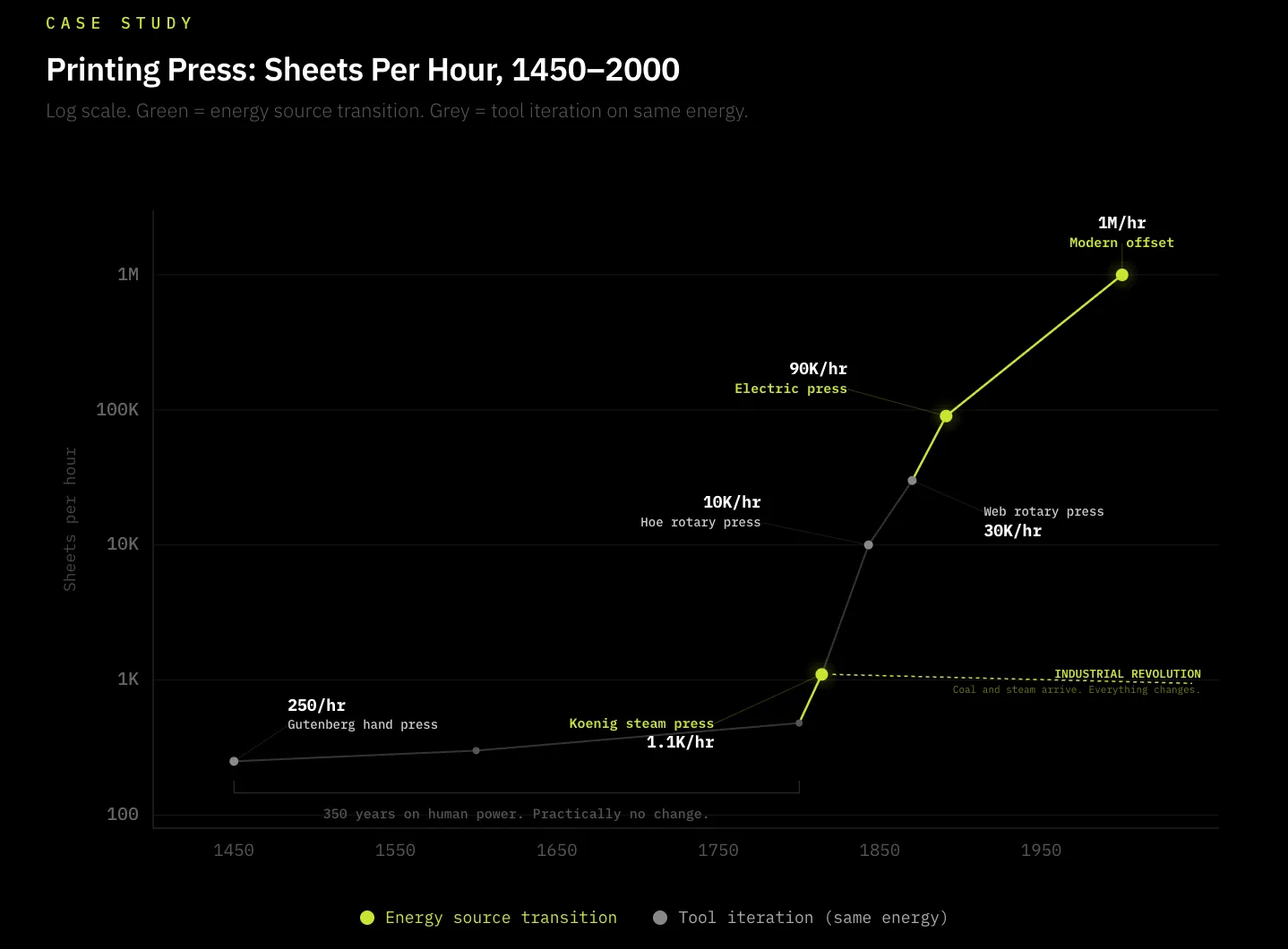

For most of human history, humans relied on bodily energy and hands as tools to advance goals, whether for farming or writing. The printing press is a typical case of how energy and tools progressed in collaboration—it was popularized by Gutenberg in 1440. Before this innovation, humans expended their energy to hand-write information with pens (tools), which was extremely inefficient. The printing press innovated new tools and significantly improved the efficiency of human energy utilization by mechanically printing text, thus enhancing productivity by several orders of magnitude. However, from 1450 to 1800, nearly 350 years saw little substantive innovation in printing presses. Only when humanity harnessed a more powerful energy source—coal—did the energy side of the equation change. In 1814, Friedrich Koenig invented the steam-driven printing press, adapting it to the then-dominant energy innovation—coal, resulting in a fivefold efficiency increase. Since then, the printing press has continuously adapted to new energy sources, increasing output from 250 copies per hour to 30,000 copies 50 years later, and today reaching millions.

Thus, the continual innovation of new tools, breaking through energy harnessing limits, and improving the efficiency of new tools relative to available energy—this ongoing process continues today. Today, intelligence is the new form of productivity we focus on, and energy is its fuel. The key is whether we can continue to advance intelligent growth, which depends on how much sustainable and reliable energy we can produce to power tools (GPUs) and direct them towards goals (intelligence).

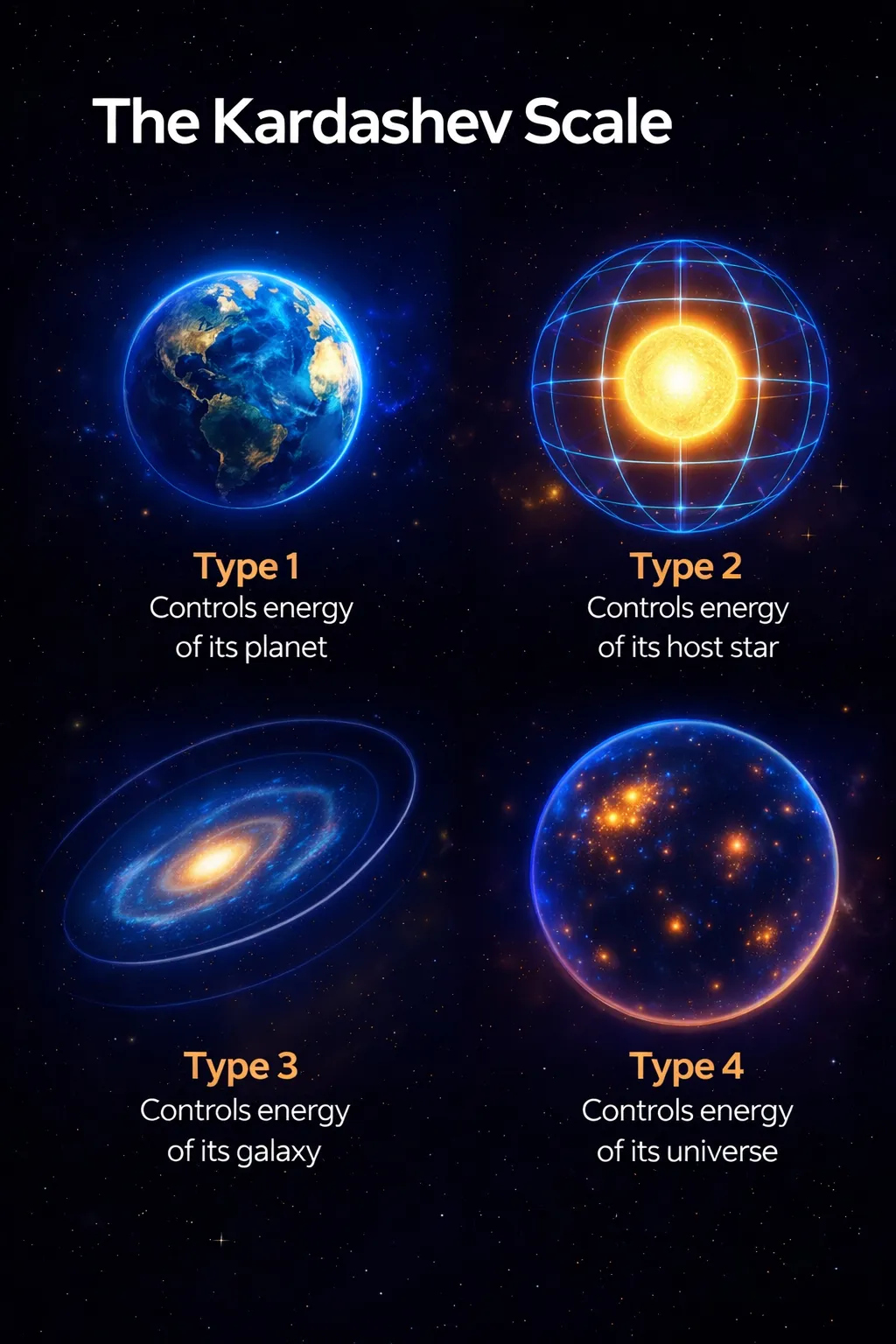

This topic corroborates the Kardashev scale, which measures a civilization's technological advancement by how much energy it can harness—from planetary to stellar to galactic to universal to multiversal. How much energy we can harness signifies how far we have progressed as a civilization. Historically, this rule has always held true, and the future will not be an exception. The ability to harness energy is fundamental to advancing civilization.

The core argument of this article is: energy demand is rapidly outpacing supply, which is the primary bottleneck for advancing intelligence. I will explore the first and second-level impacts of this argument.

Why is energy supply slowing down?

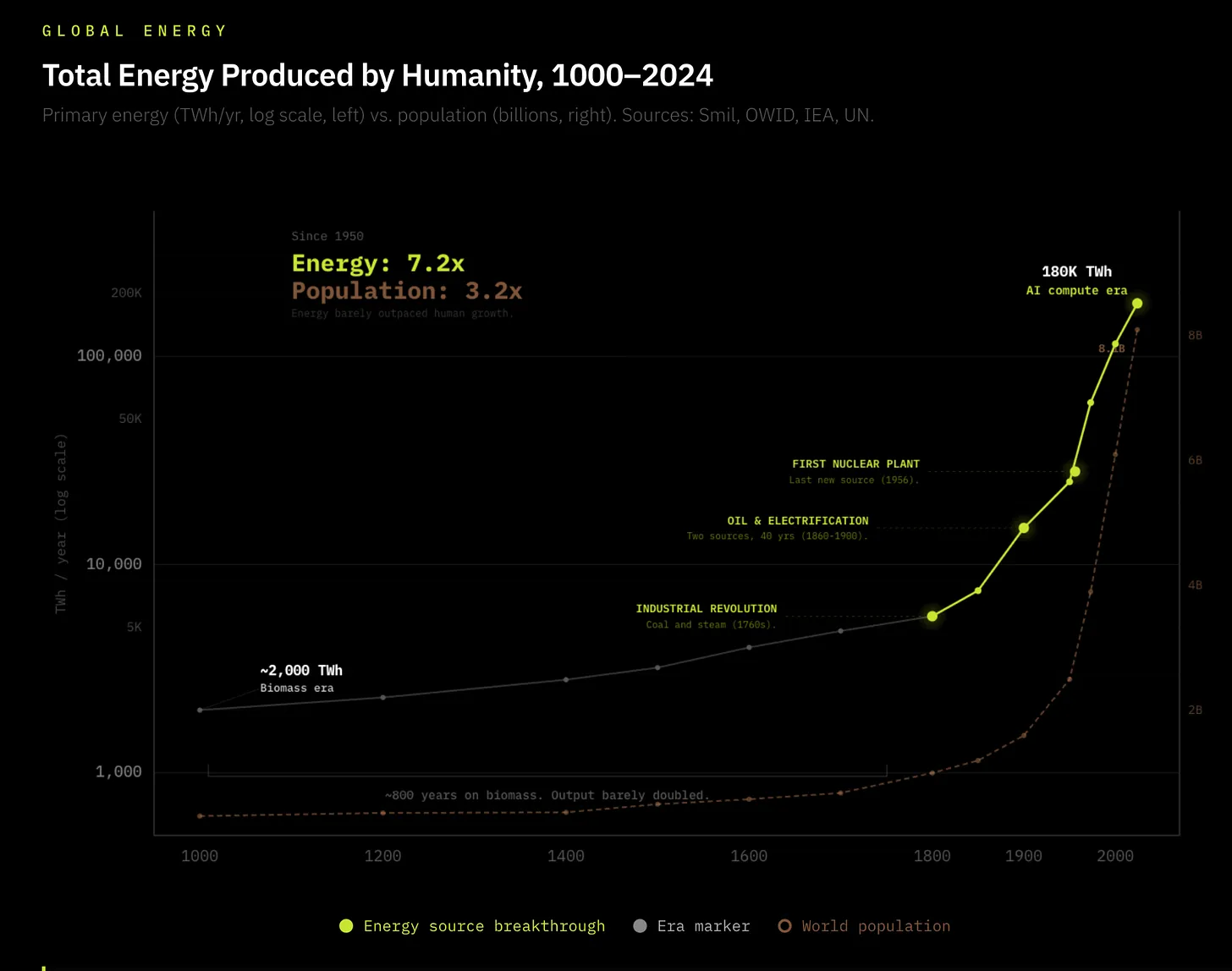

Nuclear fission was discovered in 1939 and remains the last significant transformation in the energy field since the dawn of human civilization. However, due to the Chernobyl accident and a global shift from nuclear power to renewable energy, there has been a clear mismatch between tool innovation and energy progress since 1950. In 1950, global energy production was 2600GW, today it is 19000GW (a 7.3-fold increase). This may seem like a leap, but this gradual linear growth is far from matching the growth of modern computing and technology, and it barely exceeds the 3.5-fold increase in population during the same period.

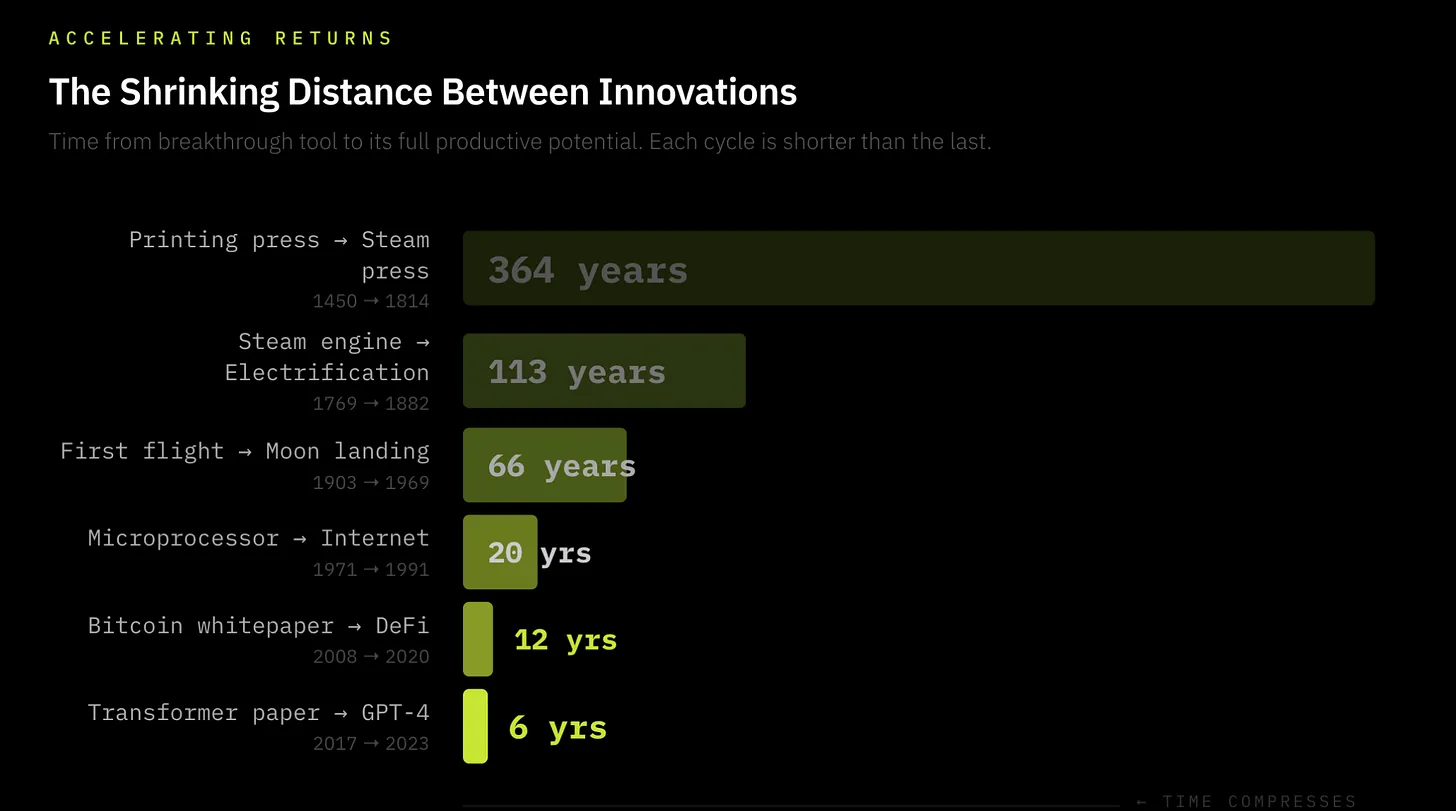

In contrast, the intervals between quantum leaps of tool innovation are shrinking. The first printing press saw its next major improvement 364 years later, the first flight to space took 58 years, and the first microprocessor to the internet took 20 years, whereas today significant upgrades in GPUs occur every two years. We are living in an era of accelerating tool efficiency improvement, where numerous innovations build upon increasingly rapid cycles. From AI to cryptography to quantum computing, the speed of new innovations being discovered is increasing, and their efficiency improvements are becoming more rapid—that is the law of accelerating returns.

Today, data centers account for 1.5% of global electricity consumption, and it is expected to reach 3% by 2030—accomplishing in 6 years what the steam engine took 50 years to achieve. The key difference between the Industrial Revolution and the current explosion of intelligence is: the Industrial Revolution built its energy supply in tandem with growing demand—coal mines, canals, and rail networks expanded concurrently with the machines consuming them. Every prior energy revolution established its own supply chain as it scaled; AI inherits a supply chain that is already starting to fracture.

The grid is fundamentally unprepared to cope with the annual electricity consumption growth of 15% driven by the explosion of intelligence, while U.S. electricity demand has seen almost zero growth in the past decade. Cracks are already appearing in the U.S.: the longest historical queue for grid access, the average delivery time for large transformers has reached 24 to 36 months, and in 2025, electricity transformers will face a 30% supply gap. Morgan Stanley estimates that just in the U.S. alone, by 2028, there will be a 45GW power shortfall, equivalent to the electricity demand of 33 million American households. I believe this gap could be even larger.

The problem is clear: humanity needs to radicalize energy scaling to keep pace with innovations in AI, robotics, and autonomous driving.

The Upcoming Energy Gap: First and Second-Level Effects

The consequences of the impending energy gap are historically significant: as energy demand skyrockets while supply falters, we may see the emergence of a quasi-privatized energy market.

Hyperscale cloud service providers have begun to construct behind-the-meter (BTM) power generation facilities and are planning to expand into nuclear-powered data centers, a trend that is starting to emerge. I believe this trend will only become more pronounced.

Below I present seven arguments, which are all derivatives of the intelligent explosion and its impact on the continuing tension in power supply.

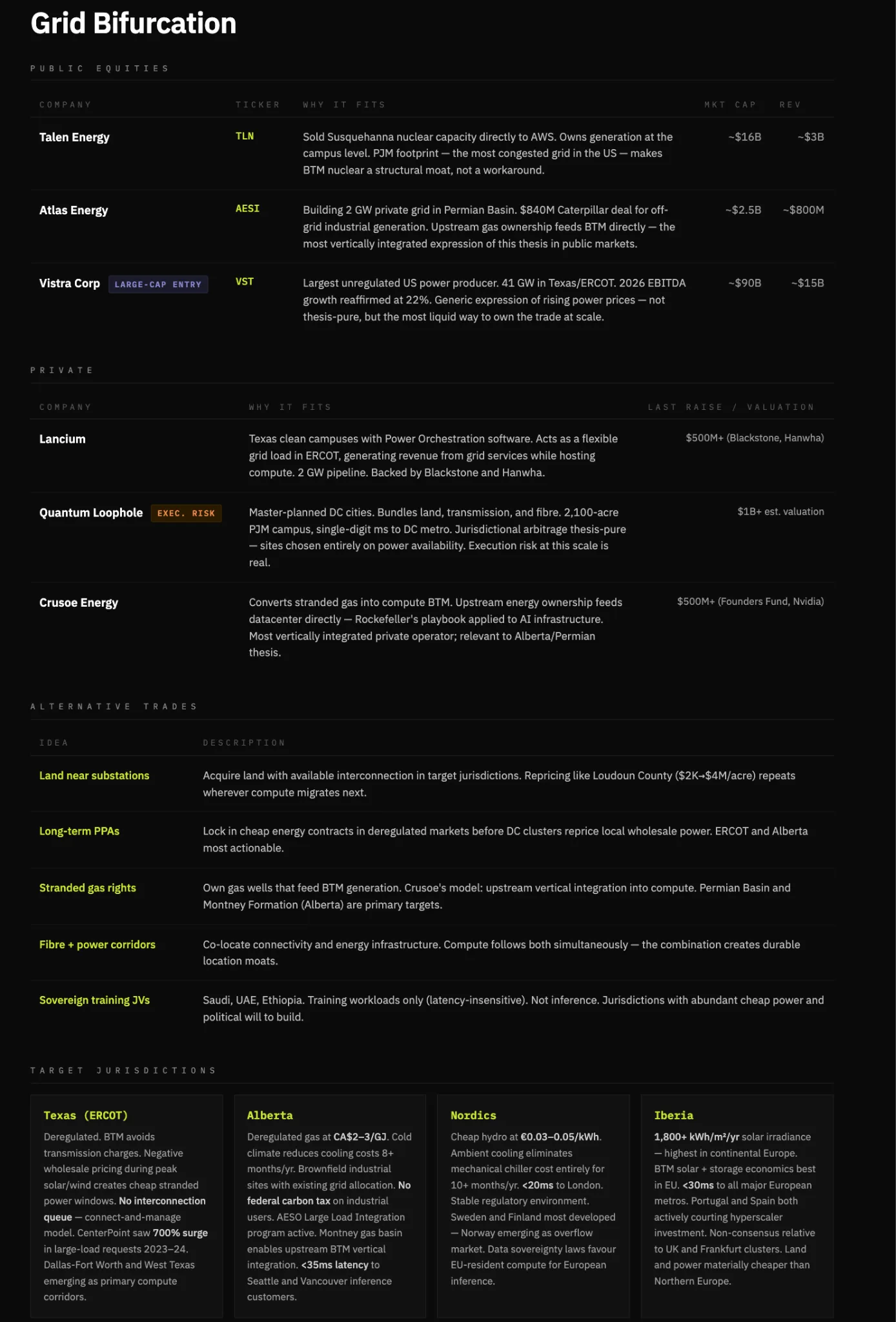

Argument One: Grid Fragmentation—Computing Power Will Migrate Toward Energy, Not the Other Way Around

In regions where computing demand is high, jurisdictions with abundant energy and loose regulations will gain disproportionate value as energy systems fragment.

When energy demand begins to exceed supply, electricity will become politically sensitive. Households have voting power, while data centers do not. In the face of energy shortfalls, it is unlikely that the grid will remain neutral, but rather prioritize residential electricity demands over industrial electricity through pricing, access restrictions, or soft caps.

Given that computing power is extremely sensitive to latency, uptime, and reliability, operating in jurisdictions that prioritize residential electricity is simply not feasible. As grid access becomes unstable or politicized, computing workloads will migrate to behind-the-meter (BTM) generation models, where electricity can be directly secured, controlled, and priced.

This will drive a structural shift: computing power will move to economies with abundant energy and relaxed regulations. The winners will be those entities that can integrate land, connectivity, energy generation, and fiber into deployable and replicable systems, and the jurisdictions where these systems reside will benefit as well.

Argument Two: Energy Becomes a Competitive Moat, BTM Self-Generation Becomes a Core Capability of Computing Providers

In my view, this is the most critical first-order impact of an escalating energy gap. In a world where energy demand exceeds supply, accessing cheap and reliable power represents a structural cost advantage that grows over time. Moreover, data centers prioritizing grid power is politically unsustainable, and that is the trajectory current energy trends are on. The increasingly strained national power grids will force computing providers to generate their own electricity; hyperscale cloud providers have already begun this trend. Facilities without BTM generation will be directly eliminated.

Essentially, companies that own power win, while those that rent power lose. Without BTM generation, computing providers will face issues with power reliability (which is fatal), rising costs, and electricity restrictions. Purely co-located REITs without self-generation (like Equinix and Digital Realty) will see their value decrease relative to vertically integrated operators. Companies that combine energy generation with computing hosting are constructing the deepest moats (Crusoe, Iren, and some hyperscale cloud providers). This could be expressed as long-short trading, but I prefer to emphasize the winners of vertical integration here.

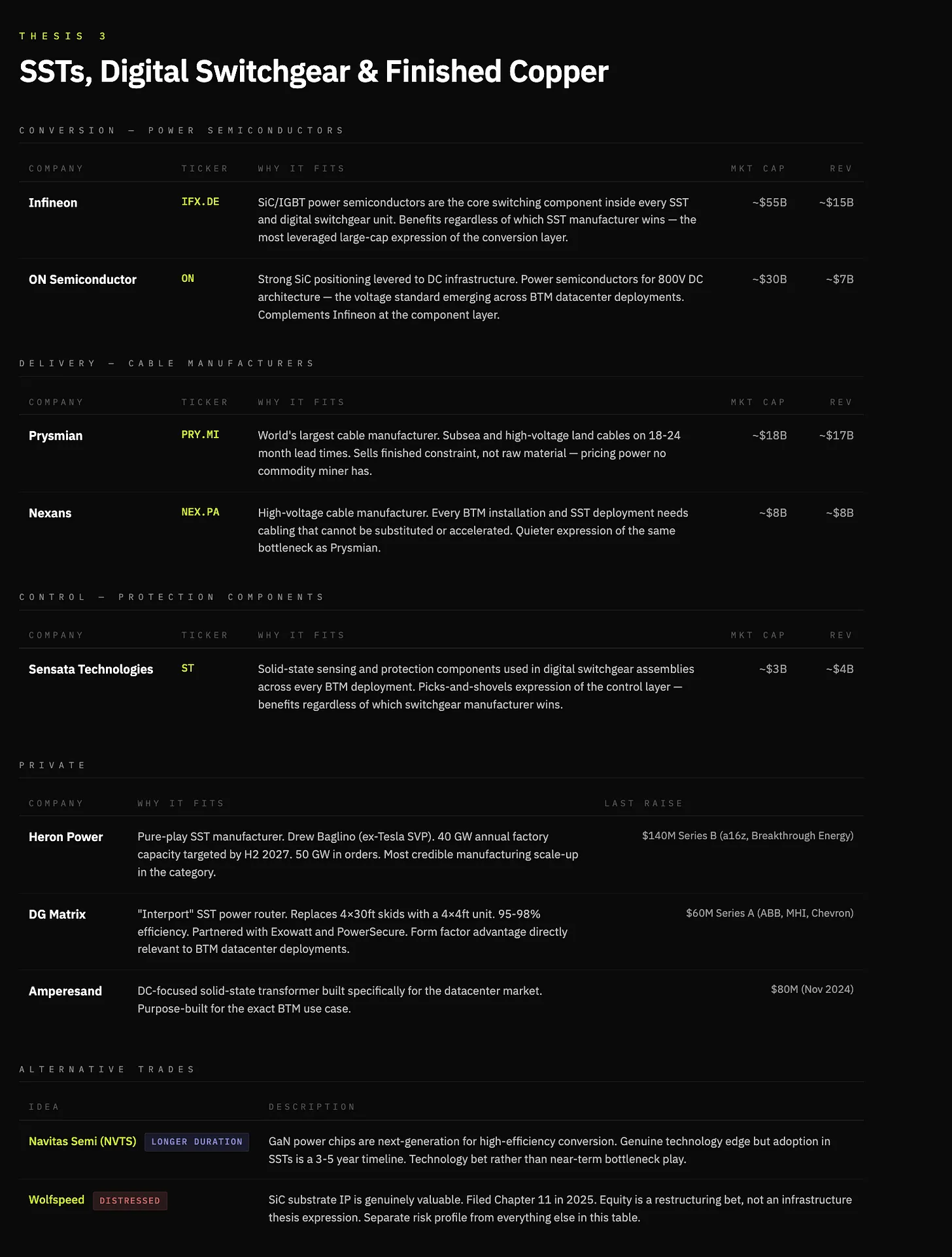

Argument Three: BTM Standardization Sparks Innovation—From Traditional Transformers to Solid-State Transformers, From Traditional Switchgear to Digital Switchgear

Traditional transformers step up or step down AC electricity. Due to their scale and materials, delivery times have extended to 24 to 36 months, and there exists a 30% supply gap. They are also a technology from the 1880s, manufactured manually around constrained materials. The key is that every megawatt of BTM generation must be converted, conditioned, and delivered to the computing end, and there is no way to bypass transformers.

Solid-state transformers replace all of this with high-frequency power electronic devices. They are smaller, faster, and fully controllable, handling AC-DC conversion, voltage regulation, and bi-directional current within a single unit. Manufacturing is also simpler, relying on silicon power semiconductors like silicon carbide/gallium nitride rather than massive copper windings and oil-filled tanks. As BTM becomes the standard architecture, the device between energy and computing becomes the bottleneck, and that device is the solid-state transformer (SST).

Switchgear also faces an 80-week delay and serves as the control layer between generation and load, responsible for routing electricity, isolating faults, and protecting systems. Like transformers, switchgear is a labor-intensive product made around constrained materials, and it has changed very little since the 1880s.

Digital switchgear replaces all of this with solid-state power electronic devices. They are faster, programmable, and fully controllable, achieving real-time fault detection, remote isolation, and dynamic load routing. Equally importantly, they scale like electronic products, rather than industrial equipment.

A note on copper: I maintain a constructive view of copper. Copper is the highway for electronics and will be the primary commodity needed in an increasingly electrified world. However, the expression of this trade is nuanced—traditional mining companies operate with low margins and may see their profitability compressed over time. But at the finished goods side, where copper is irreplaceable and time-limited, significant bottlenecks and future value accumulation opportunities exist. Cable manufacturers like Prysmian and Nexans sell finished product constraints rather than raw materials, and with transformer delivery times greatly extended, this is no longer a commodities market.

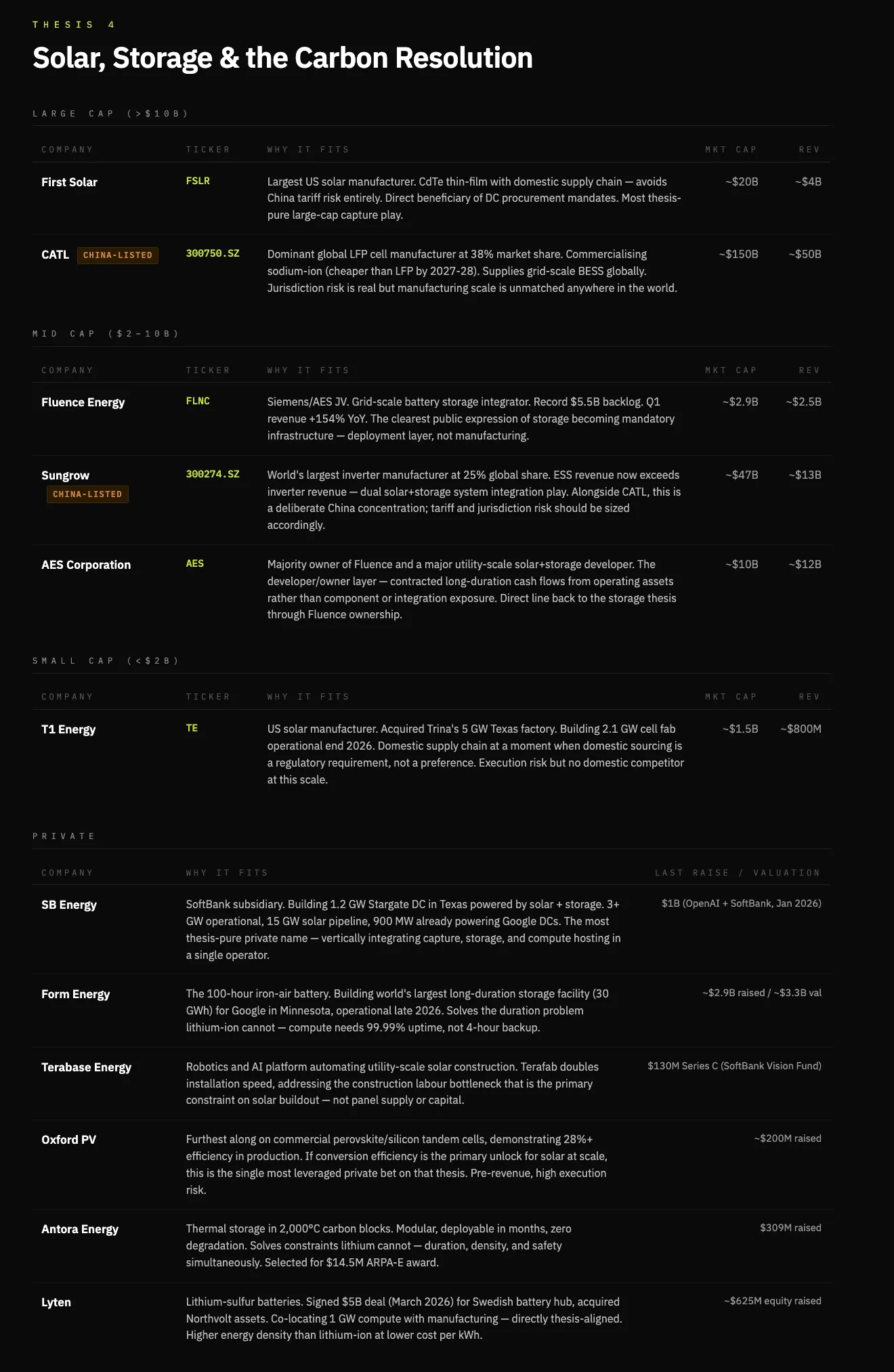

Argument Four: The Carbon Cost of AI Becomes Politically Difficult to Sustain, Forcing Solar and Battery-Dominant Solutions

There is an unpriced carbon issue associated with AI construction, which is a political constraint. Data centers increase electricity prices, massively consume water resources, and raise local emissions. This has already manifested: $18 billion worth of data center projects have been completely canceled, and $46 billion of projects have been delayed.

Today, about 56% of data center electricity comes from fossil fuels. Natural gas solves deployment speed issues but is politically fragile. As demand expands, resistance to fossil energy growth rises, forcing a recent formation of mixed systems of natural gas, nuclear, and renewable energy.

While natural gas has acted as a short-term bridge during the explosive growth of data centers, in a longer time frame, energy abundance is not achieved through fuel extraction, but through energy capture. The energy delivered by the sun to the earth is several orders of magnitude greater than human consumption. The constraint is not availability, but conversion, storage, and deployment.

Solar energy is not an immediate solution to computing power demand but rather the ultimate solution.

Currently, commercial solar captures about 22% of incident energy. Each point increase in conversion efficiency reduces the cost per megawatt, bringing solar energy closer to parity with dispatchable generation in BTM systems.

Battery storage becomes a core component of this architecture. Not only to smooth intermittency but also as a layer of returns. Energy storage arbitrage and load balancing transform historical cost centers into profit contributors for BTM operators.

In this argument, the winners are vertically integrated businesses covering capture, storage, and delivery: specialist solar developers with BTM contracts, battery manufacturers with grid-level and site-level products, and a few operators who can combine self-generation with computing hosting.

Solar energy is a game of procurement and manufacturing, while batteries represent the constraint and monetization layer, integrating capture profits. Cutting-edge technology remains an option rather than the foundational scenario. In this regard, Tesla may continue to be a big winner, but I will choose to focus on non-consensus targets.

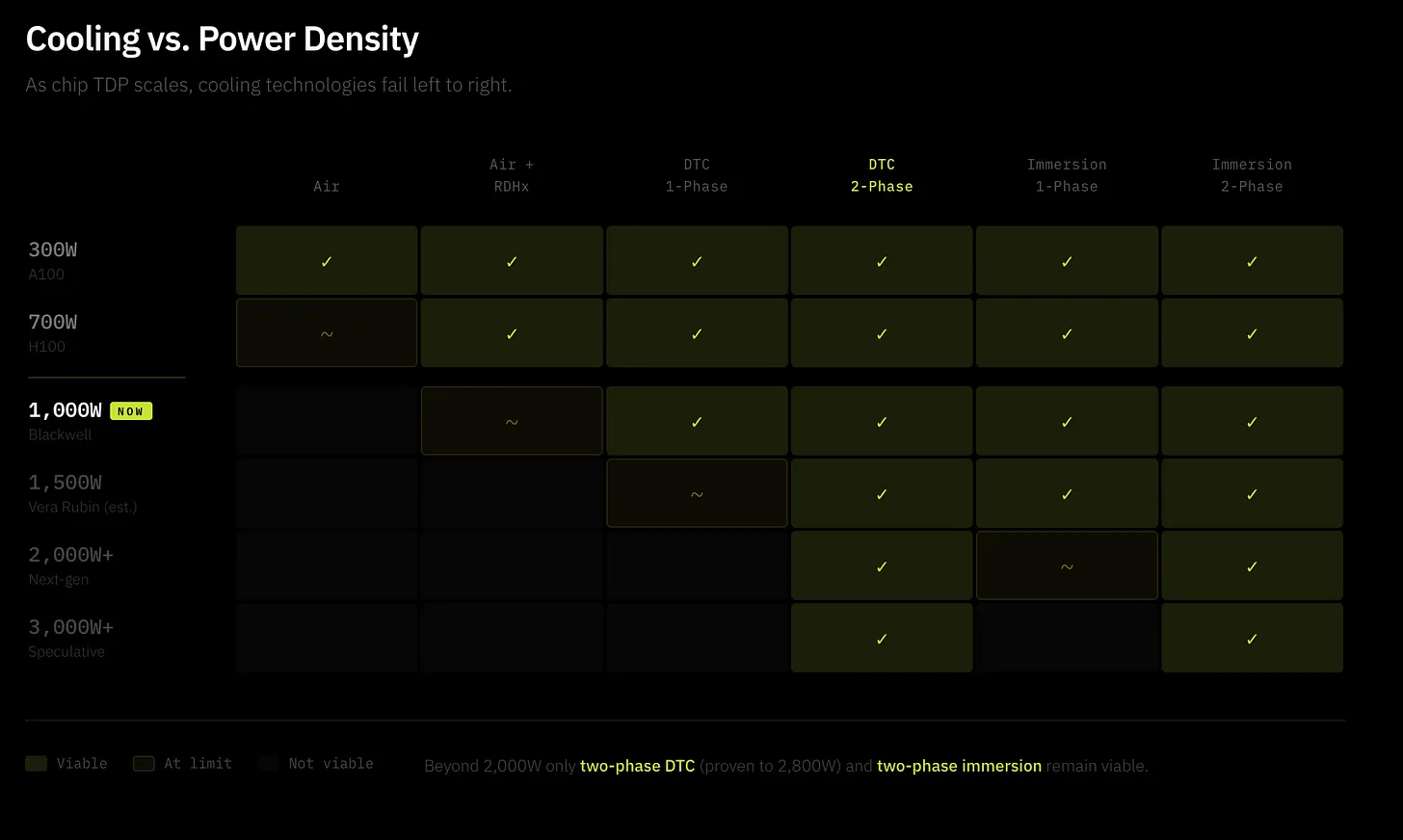

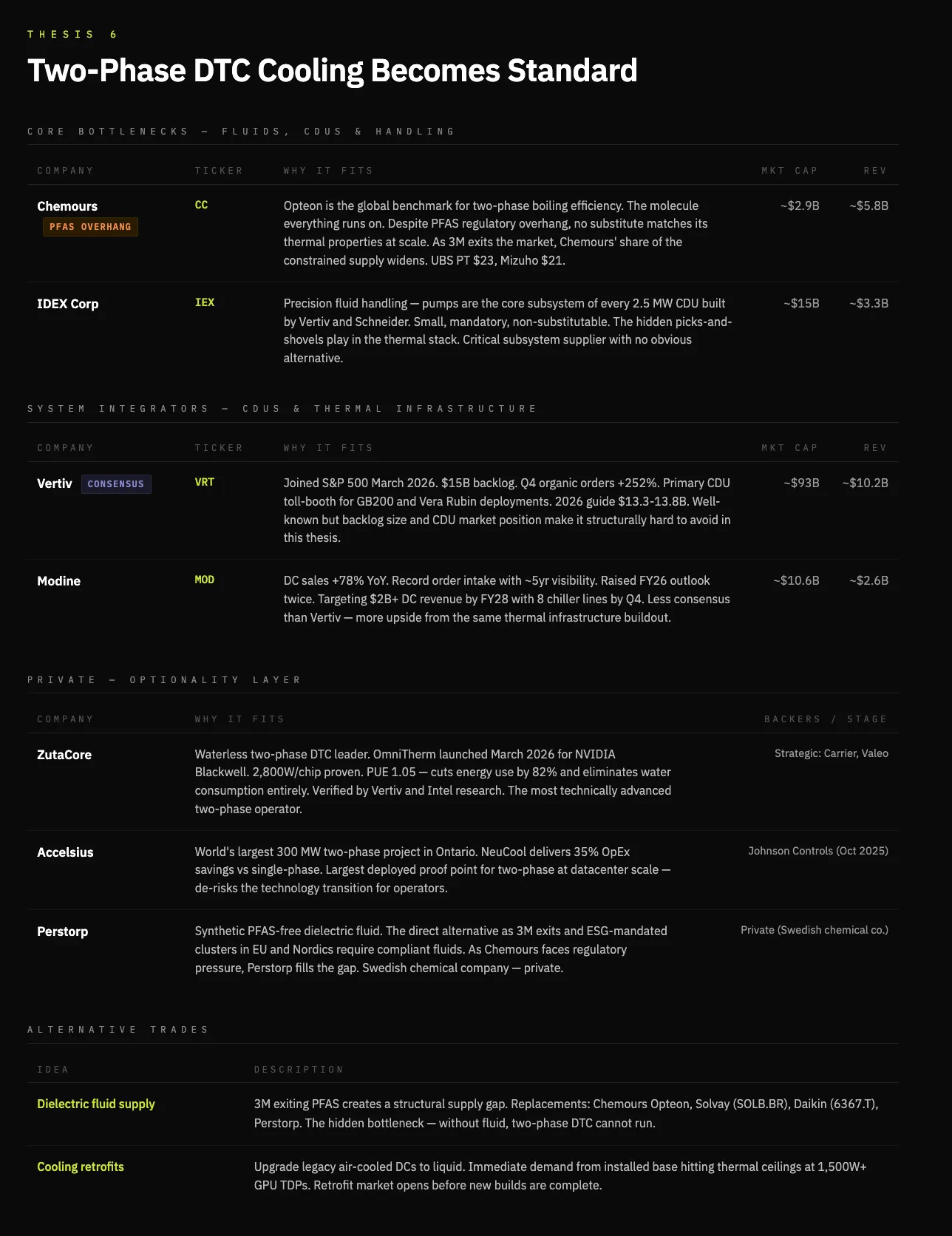

Argument Five: Cooling Becomes a Primary Constraint, Two-Phase Direct Liquid Cooling (D2C) Will Be Essential in Cutting-Edge Applications

Another consequence is the rise of two-phase direct liquid cooling technology. Frankly, this argument also integrates my own judgment: chip power density is growing along a parabolic trajectory, which is becoming an increasingly tricky thermodynamic problem. Traditional air cooling is unsustainable for various reasons, primarily because it fails to work on higher density chips, coupled with environmental issues related to water and energy consumption.

Firstly, D2C cooling advances density and performance without being limited by heat dissipation management—this is a critical issue for scaling. The current market reality is dominated by single-phase cooling because it is simpler: chilled water circulates through cold plates to cool chips, but there is a known upper limit. When chip power density exceeds 1500W, the transition to two-phase cooling will become inevitable. Two-phase cooling pumps dielectric liquids around the chips, designed to boil at low temperatures—the phase change from liquid to gas significantly enhances cooling efficiency.

Two-phase cooling can reduce energy consumption by 20% and water usage by 48%. This performance enhancement allows for more densely packed chiplets, improving performance and ultimately generating higher demand for high-performance cooling.

Leading two-phase DTC companies like Zutacore demonstrate that using dielectric liquids (rather than water) in two-phase D2C cooling reduces energy consumption by 82% and completely eliminates water usage—this result has been validated by research from Vertiv and Intel. Zutacore is a noteworthy private operator in this field, and further exploration of dielectric liquid suppliers may also be valuable.

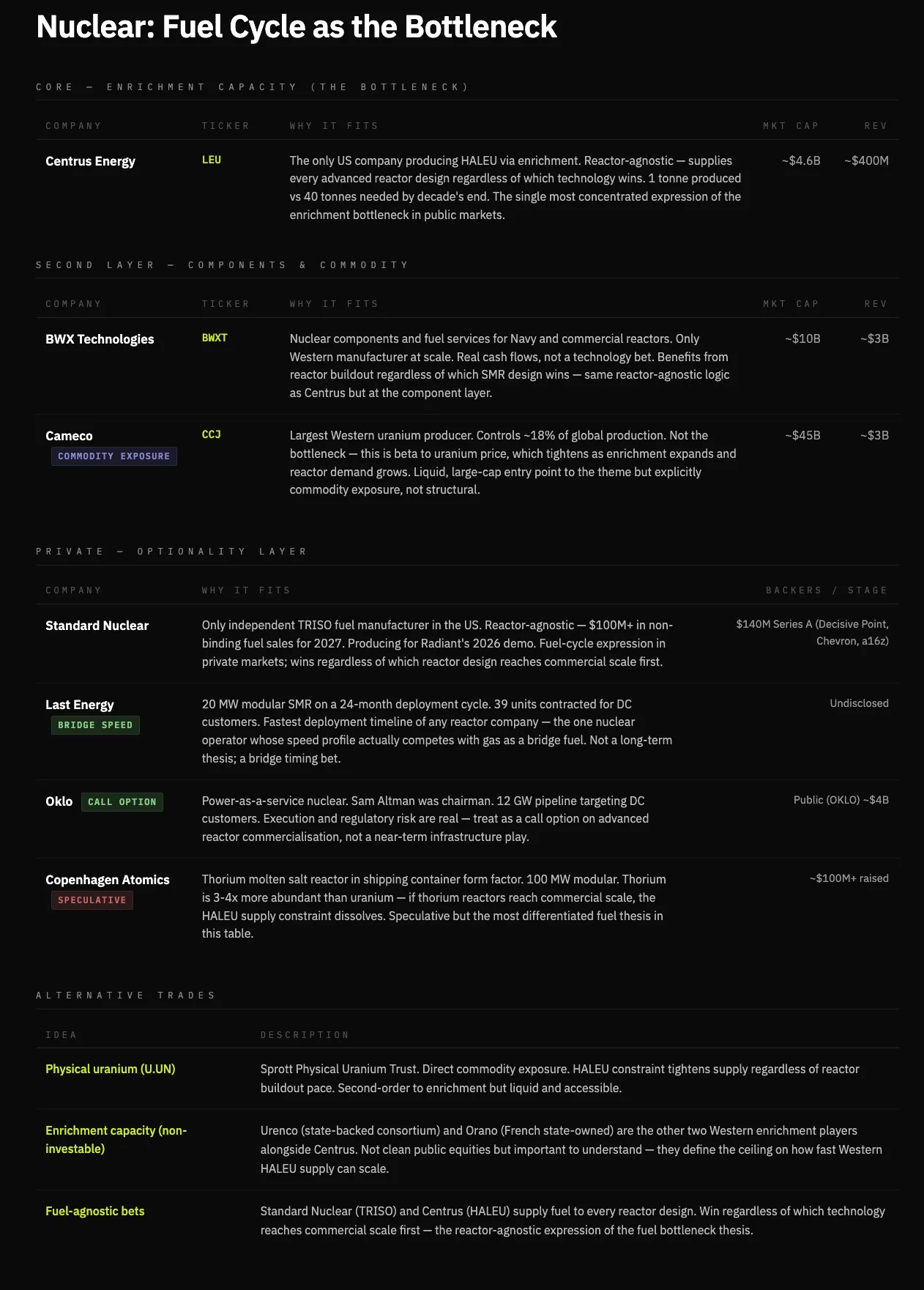

Argument Six: Nuclear Energy Can Serve as a Bridge to Energy Abundance and Stable Power Supply, But Is Not the Long-Term Answer for Energy Expansion

While writing this article, I initially thought nuclear energy was a good way to fill the short-term energy gap. The reality is that the deployment costs of small modular reactors (SMRs) are 5 to 10 times that of comparable natural gas systems (approximately $10,000 to $15,000 per kilowatt), making them practically impossible to deploy and scale in a large way.

Nuclear energy addresses reliability issues, rather than speed or cost issues—especially in BTM installations. It allows for stable, dispatchable base-load electricity in situations where reliability is non-negotiable. Thus, nuclear energy has its role in the energy gap, serving more as a bridge rather than core supply.

Nuclear energy is constrained by fuel cycles and construction timelines. Today's advanced reactors require high-assay low-enriched uranium (HALEU), and this fuel has nearly no commercially available supply today. Even when reactors are built, the ability to supply fuel becomes a key constraint on the pace of nuclear energy expansion.

As such, nuclear energy is unlikely to become the marginal solution for energy expansion—it is slow to market, capital intensive, and constrained by infrastructure and fuel. In contrast, the systems that expand the fastest—recently natural gas and, in the long term, solar and storage—are the options for narrowing the gap.

The investable bottleneck is not the reactors but the fuel. As SMR demand grows, high-assay uranium enrichment will become a critical link—a bottleneck that is independent of specific reactor designs, where value will accumulate regardless of which design ultimately prevails.

Argument Seven: A New Class of Energy Infrastructure Groups Will Emerge; Vertical Integrators Will Convert Electronics into Computing Power

The bottleneck of AI infrastructure lies not only in energy but also in the capacity to transform energy into usable computing power at scale.

In the 1870s, similar to electricity, oil was not scarce, but there were issues with refining and distribution. Rockefeller built one of the largest companies in history (Standard Oil) by vertically integrating crude oil extraction, refining, and its distribution to households.

The intelligent revolution follows the same pattern; electricity is the equivalent of crude oil. Electricity is abundant, but the reliable conversion of electricity into computing power faces constraints in power delivery, cooling, connectivity, and licensing. Refining electronics is where the value lies. Each additional layer of ownership increases reliability, reduces costs, and captures profit margins, leading further self-reinforcement of vertical integration.

Hyperscale enterprises act as the distribution layer of this system and are the end users of computing. However, the structural opportunity lies in the infrastructure that distributors are forced to purchase. This creates a new class of energy infrastructure groups, namely operators that integrate power generation, conversion, cooling, and hosting.

The clearest expression is among vertically integrated operators in the private market, like Crusoe and Lancium, as well as native computing platforms in the public market, such as Iren and Core Scientific, which already possess the most challenging assets to replicate: energy.

Companies that control the flow of electrons to racks are constructing the deepest moats in the AI economy. Software cannot devour physical infrastructure.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。